Lessons from Abby Joseph Cohen

Abby Joseph Cohen spent thirty years as Goldman Sachs’ Chief Investment Strategist, famously calling the structural shifts behind the 1990s bull market. Now teaching at Columbia Business School, she focuses on valuation fundamentals, long-term global risks, and the economic weight of human capital.

Part 1: Market Strategy and Valuation

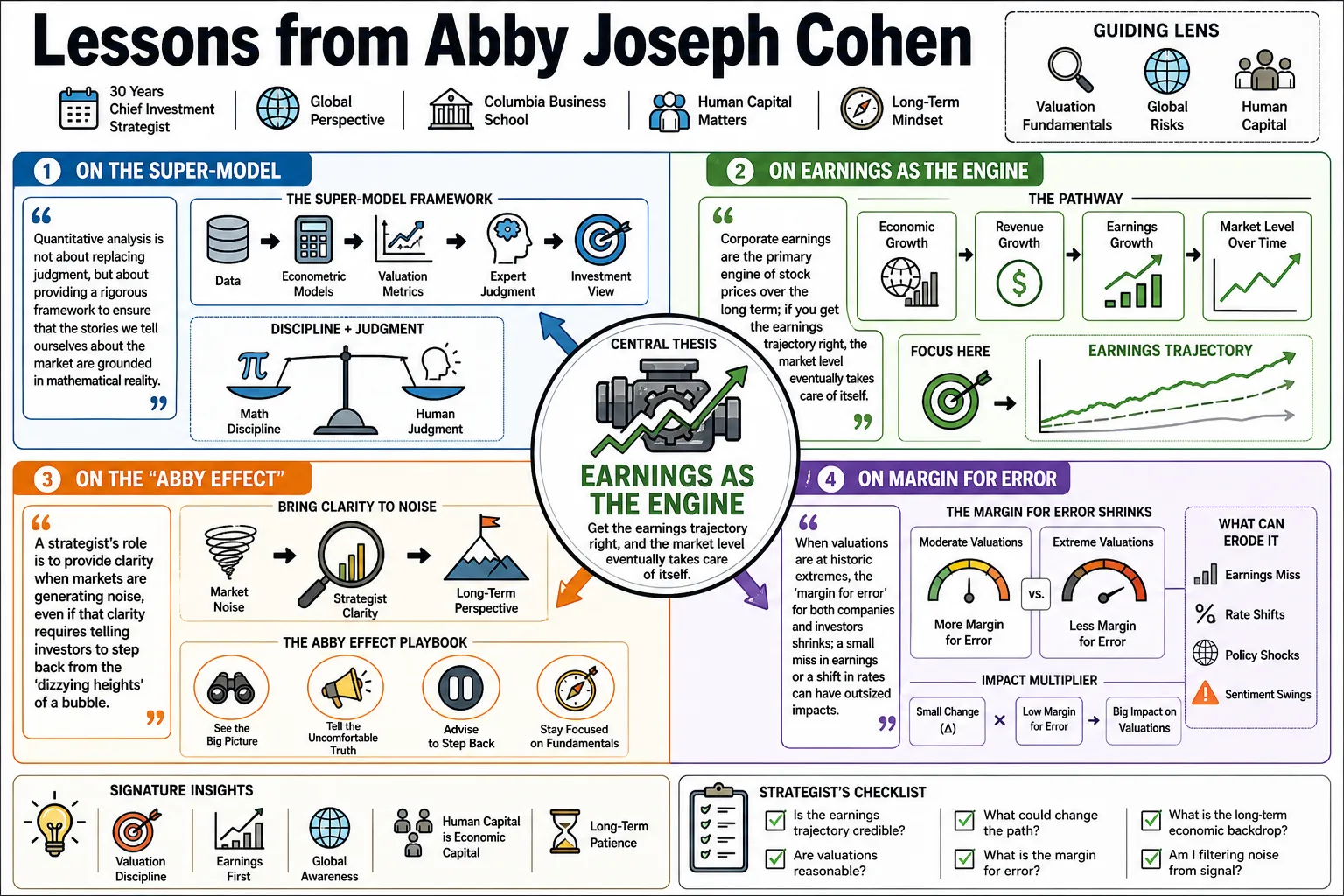

- On the Super-Model: "Quantitative analysis is not about replacing judgment, but about providing a rigorous framework to ensure that the stories we tell ourselves about the market are grounded in mathematical reality." — Source: JWA

- On Earnings as the Engine: "Corporate earnings are the primary engine of stock prices over the long term; if you get the earnings trajectory right, the market level eventually takes care of itself." — Source: Netfigo

- On the 'Abby Effect': "A strategist’s role is to provide clarity when markets are generating noise, even if that clarity requires telling investors to step back from the 'dizzying heights' of a bubble." — Source: The Street

- On Margin for Error: "When valuations are at historic extremes, the 'margin for error' for both companies and investors shrinks; a small miss in earnings or a slight change in interest rates can lead to outsized price corrections." — Source: CNBC

- On Fully Priced Markets: "In a fully priced market, you are no longer paying for the 'average' outcome, but for the 'best-case' scenario, which makes the risk-reward ratio inherently less attractive." — Source: Barron's

- On Flow of Funds: "Understanding where money is coming from and where it is going—the flow of funds—is often more instructive for identifying market trends than looking at price action alone." — Source: WealthTrack

- On Concentration Risk: "The high concentration of the U.S. market in just a few technology names creates a vulnerability; investors should look for sectors that haven't been bid up to challenging multiples." — Source: Bloomberg

- On Long-Term Views: "The stock market is not the economy, but over long periods, the two tend to rhyme; successful investing requires distinguishing between temporary market noise and fundamental economic shifts." — Source: Netfigo

- On Fundamental Risk: "Investors who confuse short-term market volatility with long-term fundamental risk make very expensive mistakes by exiting the market at exactly the wrong moments." — Source: Grokipedia

- On Corporate Resilience: "Corporate America has repeatedly demonstrated an extraordinary ability to adapt and grow earnings even in difficult inflationary or regulatory environments." — Source: JWA

Part 2: The 1990s Bull Market & Economic Cycles

- On Structural Shifts: "The 1990s were not just a typical cyclical upswing; they represented a structural shift driven by the massive integration of technology into every aspect of business productivity." — Source: Wikipedia

- On the 'New Economy': "A 'New Economy' doesn't mean the old rules of math are gone; it means that the productivity coefficients have changed, allowing for faster growth with lower inflation." — Source: JWA

- On Technology as a Driver: "The power of technology in the 1990s was its ability to lower the marginal cost of production and distribution across almost every industry, not just in the tech sector itself." — Source: Columbia Business School

- On Exceptional Durability: "The U.S. economy has shown exceptional durability because of its flexible labor markets and the speed at which it reallocates capital to more efficient uses." — Source: Economic Club of New York

- On Distinguishing Noise: "Most of what we read daily in the financial press is noise; the strategist's job is to filter that noise to find the three or four fundamental variables that actually matter." — Source: Netfigo

- On Resilience and Flexibility: "The resilience and flexibility of the U.S. economic system often surprise those who focus too narrowly on short-term data misses." — Source: JWA

- On Productivity Identification: "Identifying productivity gains early is the holy grail of economic forecasting, as it allows you to see non-inflationary growth before the Fed or the bond market reacts." — Source: Grokipedia

- On Long-Term Shifts: "Major economic shifts rarely happen overnight; they are the result of decade-long trends in capital investment, education, and demographic change." — Source: WealthTrack

- On Market Cycles: "Cycles are inevitable, but their duration and depth are determined more by policy responses and productivity than by the calendar." — Source: CNBC

Part 3: Macroeconomic Forecasting & Data

- On Econometrics: "My early training at the Fed taught me that data-first discipline is essential; you cannot have a strong opinion on the market without a deep understanding of the underlying econometric models." — Source: JWA

- On Macro-Micro Integration: "The best forecasts are those that integrate broad macroeconomic trends with micro-level corporate data, such as capital expenditure plans and labor cost trends." — Source: Columbia Business School

- On Data-First Discipline: "The numbers don't lie, but they often whisper; you have to listen closely to the revisions and the secondary data to see the true direction of the economy." — Source: WealthTrack

- On Economic Modeling: "Modeling is an iterative process; you must be willing to discard your old assumptions the moment the data proves the environment has changed." — Source: JWA

- On the 2022 Recession Call: "The U.S. avoided a recession in 2022 because consumer balance sheets were much stronger than the headlines suggested and corporate capex remained robust." — Source: WealthTrack

- On Inflation vs. Sticker Shock: "There is a significant difference between the rate of inflation cooling and prices actually coming down; families experience 'sticker shock' long after the CPI has stabilized." — Source: WealthTrack

- On the Cooling Rate of Inflation: "Inflation has moved back toward the 2% range, but the secondary effects on wages and service costs are stickier and require continued vigilance." — Source: Bloomberg

- On the Cost of Capital: "The return of the 'cost of capital'—meaning interest rates that are no longer zero—will force companies to be much more disciplined about their investment choices." — Source: WealthTrack

- On GDP Growth Easing: "We should expect U.S. GDP growth to ease toward a more sustainable 2% to 2.5% as the post-pandemic recovery matures and fiscal stimulus fades." — Source: WealthTrack

- On the Fiscal Mismatch: "There is a dangerous mismatch between the revenue that can be raised from tariffs and the massive costs associated with proposed tax cuts and growing debt interest." — Source: Bloomberg

Part 4: Education, Labor, and Human Capital

- On Education as Economic Policy: "Education is the most important economic policy we have; a nation that fails to invest in the technical literacy of its workforce is a nation choosing to fall behind." — Source: Barron's

- On Math and Science Underinvestment: "The U.S. is cutting off its status as a scientific leader at the knees by failing to prioritize K-12 math and science education compared to our global competitors." — Source: CNBC

- On Wealth Inequality: "The mismatch in wealth inequality isn't just a social issue; it's an economic drag that limits the 'denominator' of our consumption-based economy." — Source: Grokipedia

- On Immigration and Growth: "Immigration has historically been a secret weapon for U.S. economic growth, providing the labor and the entrepreneurial energy needed to offset aging demographics." — Source: Columbia Business School

- On a Skilled Workforce: "Our competitive edge depends entirely on having a literate and technically skilled workforce that can adapt to the rapid changes brought by AI and automation." — Source: Barron's

- On Scientific Leadership: "Maintaining our status as a global scientific leader requires long-term public funding for basic research that the private sector is often too short-sighted to provide." — Source: Barron's

- On Labor Force Demographics: "The 'denominator' of our labor force—the number of available workers—is shrinking due to demographic shifts, which makes productivity gains even more critical." — Source: CNBC

- On Training Needs: "We need a revolution in worker retraining; the skills required for the modern economy are changing faster than our traditional education cycles can keep up." — Source: Columbia Business School

- On Intangible Assets: "Traditional book value fails to capture the true worth of modern companies, where the primary assets are intangible: patents, software, and human capital." — Source: Columbia Business School

Part 5: Trade Policy and Geopolitics

- On Tariff Skepticism: "Broad-based tariffs are extraordinarily painful for consumers and represent a return to 19th-century economic thinking that failed in the 1930s." — Source: Bloomberg

- On the Regressive Nature of Tariffs: "Tariffs are essentially a sales tax that disproportionately hurts people at the lower end of the income spectrum who spend a larger share of their earnings on imported goods." — Source: Bloomberg

- On Erratic Trade Policy: "The erratic nature of modern trade policy makes it nearly impossible for multinational corporations to engage in long-term capital planning and supply chain investment." — Source: Barron's

- On the Weakening Dollar: "While a weaker dollar can help exporters, it also signals a decline in the global demand for U.S. assets and can fuel domestic inflationary pressures." — Source: Bloomberg

- On Supply Chain Resilience: "We are moving from a 'just-in-time' supply chain model to one focused on resilience and 'friend-shoring,' which increases security but at a permanently higher cost." — Source: WealthTrack

- On 'Opening Bids' in Trade: "Treating massive tariffs as merely an 'opening bid' for negotiations ignores the real-world damage done to international relationships and business confidence in the interim." — Source: Bloomberg

- On the Lack of Economic Rationale: "There is often no clear economic rationale behind the specific tariff percentages proposed; they appear more political than mathematical." — Source: Bloomberg

- On Corporate Planning Disruption: "Global companies require stability to invest; when trade rules change by tweet or overnight decree, the risk premium on all investments goes up." — Source: Bloomberg

- On Dangerous Economic Thinking: "A tariff-based economy is something that didn't work in the 1930s and won't work in our much more highly integrated global economy today." — Source: Bloomberg

- On Geopolitical Uncertainty: "Geopolitical risk is no longer a 'tail risk'; it is a central variable that must be priced into every investment model and corporate strategy." — Source: WealthTrack

Part 6: Career, Leadership, and Trailblazing

- On Being a Woman on Wall Street: "In the 1980s, one of the few advantages of being a woman in finance was that at major conferences, there was never a line at the ladies' room." — Source: JWA

- On the Drexel Reputation: "I emerged from Drexel with my reputation intact because I stayed focused on the rigorous research and avoided the speculative excesses that eventually brought the firm down." — Source: JWA

- On Strategy Leadership: "Leading a strategy team at a major firm like Goldman Sachs requires the ability to maintain conviction when the consensus is shouting the opposite." — Source: Business Insider

- On Work-Life Balance: "My family was always my most important client; I made sure school plays and family events were on my business calendar just like a meeting with a CEO." — Source: Grokipedia

- On Advocacy for Flex Hours: "I advocated for flexible hours and working from home long before they were industry standards because I knew it was the only way to retain the best talent." — Source: JWA

- On the Role of Clarity: "A strategist doesn't need to be right about every tick of the clock, but they must be right about the time of day—the broad direction of the era." — Source: Netfigo

- On Avoiding Speculative Excess: "The best way to survive a market crash is to never participate in the speculative mania that precedes it; discipline is your best defense." — Source: JWA

- On the Global Markets Institute: "Presiding over the Global Markets Institute allowed me to bridge the gap between financial market data and the public policy decisions that shape them." — Source: Wikipedia

- On Transitioning to Academia: "Retiring from Goldman allowed me to focus on the 'Future of the Global Economy' by teaching the next generation of leaders at Columbia." — Source: Business Insider

Part 7: The Future of the Global Economy

- On AI and Labor: "AI will certainly automate tasks, but its most profound impact will be in augmenting the productivity of high-skilled labor in ways we are only beginning to model." — Source: Bloomberg

- On US vs. China Competitiveness: "Our competition with China is not just about trade balances; it is a competition over who produces the most patents and the most skilled scientists over the next twenty years." — Source: Grokipedia

- On the End of Free Money: "The era of 'free money' is over; debt now has a real price, and that will separate the companies with sustainable business models from those that were just floating on liquidity." — Source: WealthTrack

- On Economic Statecraft: "Modern diplomacy must be built on 'economic statecraft,' recognizing that what is economic is strategic, and our allies are our most important economic assets." — Source: State.gov

- On Structural Alterations: "The global economy has been permanently altered by the pandemic, the return of industrial policy, and the shift away from hyper-globalization toward regional blocks." — Source: WealthTrack

- On Schedule F Risk: "Proposals like reclassifying civil service jobs as political appointments risk losing the subject matter expertise that keeps the economy and the regulatory system functioning." — Source: WealthTrack

- On Crypto Instability: "I remain reticent about the push for crypto; it introduces a layer of potential instability into financial markets that we don't yet fully understand or regulate." — Source: Bloomberg

- On Global Diversification Necessity: "U.S. investors are dangerously over-concentrated in domestic tech; true diversification now requires looking toward markets like India and East Asia." — Source: WealthTrack

- On De-globalization: "Deglobalization is not just a buzzword; it is a fundamental re-pricing of global risk that will lead to more localized and expensive production cycles." — Source: Columbia Business School

Part 8: Investment Discipline & Global Outlook

- On Fighting the Fed: "One of the most durable lessons in finance is 'Don't fight the Fed'; when the central bank shifts its policy stance, investors must adjust their portfolios accordingly." — Source: WealthTrack

- On Mid-Cap Undervaluation: "Mid-cap stocks currently offer a much better risk-reward profile than large-caps, as they have higher survival rates than small-caps but haven't seen the valuation bloat of the mega-caps." — Source: WealthTrack

- On India as a Destination: "India represents one of the most compelling long-term growth stories because of its favorable demographics and its massive infrastructure theme." — Source: Barron's

- On Energy as a Buy: "Global energy companies remain a long-term 'buy' because the transition to green energy will take decades, and fossil fuels remain essential for global growth in the interim." — Source: Barron's

- On International ETFs: "Using broad international ETFs like the EAFE index is a prudent way to reduce tech-heavy concentration and gain exposure to pharmaceuticals and industrials." — Source: WealthTrack

- On 'Self-Help' Stocks: "In an environment of slowing growth, look for 'self-help' stocks—companies that can grow their earnings through internal efficiency and market share gains regardless of the macro backdrop." — Source: Barron's

- On Balance Sheet Strength: "Balance sheet strength becomes the ultimate differentiator for companies when interest rates stay higher for longer and liquidity starts to dry up." — Source: Barron's

- On Providing Clarity: "My goal has always been to simplify the complex and help investors see the three or four variables that actually drive long-term returns." — Source: Columbia Business School

- On the Strategic Outlook: "The next decade will be defined by how well we manage the transition to a higher-cost-of-capital environment while sustaining our investments in human capital." — Source: WealthTrack