Alex Sacerdote is the founder and portfolio manager of Whale Rock Capital Management, a TMT-focused hedge fund managing over $8 billion in assets. Known for his "S-Curve" investment framework, he identifies technological inflection points to capture exponential growth before the broader market recognizes it. This profile unpacks his three-part investment thesis, his evolving views on artificial intelligence, and the mechanics of his research engine.

Part 1: The Origins & The Amazon Epiphany

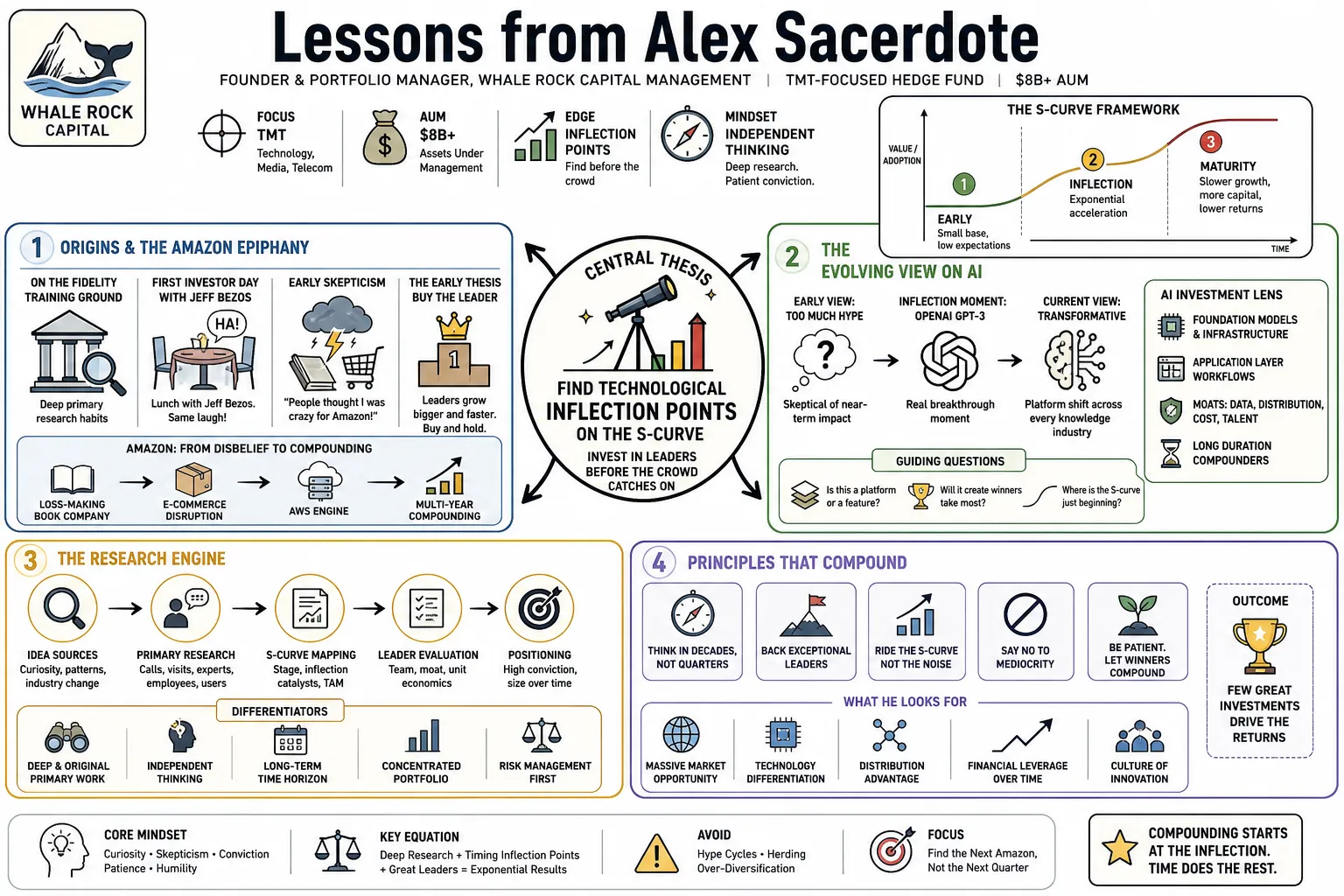

- On the Fidelity training ground: "Fidelity was an incredible training ground where I learned to do deep primary research, which eventually led me to specialize in technology." — Source: Capital Allocators

- On meeting Jeff Bezos: "I was able to attend Amazon's first investor day and had lunch with Jeff Bezos. He had the same laugh back then too!" — Source: Capital Allocators

- On early skepticism: "People thought I was crazy for investing in Amazon! Many viewed it as a fraud because it was a loss-making book company competing with established giants." — Source: Capital Allocators

- On the 'buy the leader' thesis: "My early thesis was that the leader grows bigger and faster, leading me to recommend buying Amazon and shorting its competitors." — Source: Capital Allocators

- On the value of conviction: "While half the investment team thought the Amazon pitch was crazy, Will Danoff was one of the few who listened and bought the stock, which was a pivotal moment in my career." — Source: Capital Allocators

- On recognizing the internet shift: "My experience at an early internet advertising startup gave me the context to understand e-commerce while traditional analysts were dismissing it." — Source: Capital Allocators

- On ignoring high early valuations: "Identifying a company at the beginning of a massive adoption cycle despite high valuations and skepticism became the foundation for the S-curve philosophy." — Source: Capital Allocators

- On the value of specialization: "The transition from generalist to TMT specialist at Fidelity allowed me to focus purely on the mechanics of technological disruption." — Source: Invest Like the Best

- On early career lessons: "Starting in investment banking and early internet startups provided both the financial rigor and the operational reality needed to evaluate tech companies." — Source: Capital Allocators

Part 2: The S-Curve Framework

- On the flat start: "Technologies begin slowly due to barriers like high costs, complexity, or a lack of an ecosystem, keeping them in the tinkering phase." — Source: Invest Like the Best

- On the inflection point: "Once barriers are removed, the technology moves from early adopters to the majority. This triggers three to five years of massive, predictable unit growth." — Source: Invest Like the Best

- On identifying the shift: "We focus on the S-curve of new technologies, specifically looking for the inflection point where a technology moves from infancy to mass adoption." — Source: Capital Allocators

- On predictability of demand: "The inflection point reduces risk because massive unit growth and demand become more predictable, making it harder for companies to fail due to lack of demand." — Source: Invest Like the Best

- On the plateau phase: "Growth decelerates naturally as adoption nears the 50 to 80 percent mark, signaling the maturity of the S-curve." — Source: Capital Allocators

- On mapping historical cycles: "The S-curve framework has remained consistent across the PC, internet, mobile, and cloud eras, providing a reliable lens for timing market entries." — Source: Invest Like the Best

- On avoiding the hype cycle: "The key is distinguishing between a technology that is stuck in the flat start and one that has genuinely crossed into the steep part of the S-curve." — Source: Capital Allocators

- On the duration of exponential growth: "When a technology inflects, it doesn't just grow for a year; it creates a multi-year runway of compound growth that the market usually underestimates." — Source: Invest Like the Best

- On overlapping curves: "Often, a company will ride one S-curve to maturity and successfully jump to a new one, as seen in the transition from desktop to mobile to cloud." — Source: Capital Allocators

- On continuous application: "We have used the S-curve framework for over twenty years; it is the fundamental mental model for how we view technological change." — Source: Invest Like the Best

Part 3: The AI "L-Curve" & Infrastructure

- On the L-Curve: "The enterprise AI market is less than 1% penetrated, and we've never seen—we talk about S-curves—we call this an L-curve, just straight up." — Source: Invest Like the Best

- On friction-less adoption: "Cloud was like the dishwasher—it had to be plugged in—so it was growing 30-50%. But what's amazing about AI is you just open up the browser and it's there. That's why we're getting this straight up." — Source: Invest Like the Best

- On the scale of AI penetration: "Currently, only 10 basis points of global knowledge workers are using AI in a genuinely agentic way, but we expect this to jump to 15% in the next four years." — Source: Invest Like the Best

- On hardware decommoditization: "Hardware categories previously seen as commodities, like fiber, PCBs, and power supplies, are being decommoditized as they are pushed to their physical limits." — Source: Sohn Conference

- On the foundational model oligopoly: "The foundational model layer is an emerging oligopoly between OpenAI, Anthropic, and Gemini, much like the cloud infrastructure race." — Source: Invest Like the Best

- On Anthropic's trajectory: "Anthropic has achieved escape velocity, with Claude's user base surging and its revenue run rate accelerating at an unprecedented scale." — Source: Sohn Conference

- On the coding unlock: "AI-powered coding is the first major breakout use case, representing a potential $500 billion market for coding agents alone." — Source: Sohn Conference

- On the golden age of hardware: "We are in a golden age of hardware where compute shortages will persist because token demand is growing 14x annually while chip efficiency improves only 2x-3x." — Source: Sohn Conference

- On AI's deflationary impact: "AI will be a highly deflationary force long-term, particularly in sectors like healthcare, allowing society to get a lot more for a lot less." — Source: Sohn Conference

- On short-term inflation: "AI is currently inflationary due to skyrocketing infrastructure costs and a massive hiring boom of software engineers by old economy companies scrambling to implement LLMs." — Source: Sohn Conference

Part 4: Underappreciated Earnings Power

- On exponential vs. linear thinking: "The market doesn't think exponentially. When a company hits the right part of the S-curve, earnings don't grow linearly; they grow from $1 to $10 to $50." — Source: Invest Like the Best

- On modeling the future: "We model earnings two to four years out; if we are right about the S-curve, a stock that looks expensive today might be trading at a very low multiple of future earnings." — Source: Capital Allocators

- On the Nvidia entry: "We loaded up on Nvidia early in the AI cycle because, despite a high trailing P/E, we were essentially paying 4 times the earnings it would generate just a few years later." — Source: Invest Like the Best

- On the Tesla entry: "We bought Tesla as the EV S-curve inflected, paying 5 times the earnings the company would produce three years later due to unrecognized volume and margin expansion." — Source: Invest Like the Best

- On getting businesses for free: "By buying Amazon for its retail business years ago, investors were essentially getting the high-margin AWS cloud business for free." — Source: Invest Like the Best

- On exiting the curve: "The EV S-curve in the U.S. hit a wall at roughly 10% penetration, causing the underappreciated earnings power to evaporate and prompting us to exit the position." — Source: Invest Like the Best

- On Apple's early cycle: "We owned Apple early in its smartphone cycle at roughly 4 times forward earnings, as the market failed to price in the sheer scale of global adoption." — Source: Capital Allocators

- On the illusion of expense: "High headline valuation multiples are often an illusion that masks the mechanical compounding of a rapidly scaling technology." — Source: Capital Allocators

- On identifying trough valuations: "Trough valuations are not found by looking at trailing metrics, but by accurately mapping the velocity of the S-curve inflection." — Source: Capital Allocators

Part 5: Durable Competitive Advantage & Moats

- On the necessity of moats: "While the S-curve drives growth, the durable competitive advantage prevents competitors from eroding profits and allows the company to capture the lion's share of value." — Source: Capital Allocators

- On internet moats: "Internet companies are driven primarily by network effects, where the value of the service increases as more people use it." — Source: Invest Like the Best

- On software standards: "Software moats are built on standards and ecosystems; the industry coalesces around a single standard, creating incredibly high switching costs." — Source: Invest Like the Best

- On e-commerce scale: "E-commerce dominance is secured by scale, logistics, and brand, which create cost efficiencies and delivery infrastructure that competitors cannot easily replicate." — Source: Capital Allocators

- On hardware monopolies: "Hardware and semiconductor moats are driven by critical intellectual property, leading to near-monopoly positions for specialized components." — Source: Capital Allocators

- On scale as an AI barrier: "The multi-billion dollar cost of training frontier AI models creates a massive capital moat that few startups can successfully cross." — Source: Invest Like the Best

- On data network effects in AI: "Increased AI usage generates more data, which improves the next model, attracting even more usage in an unassailable virtuous cycle." — Source: Invest Like the Best

- On recursive AI improvement: "The ability to use a model's own output to train its successor accelerates innovation for incumbents in a way that has no historical parallel." — Source: Invest Like the Best

- On the new Rule of 40: "For AI investing, we look for AI exposure percentage plus market share in the AI category; this identifies companies with both trend exposure and the moat to capture the economics." — Source: Invest Like the Best

Part 6: The "Whale Rock Learning Machine"

- On compounding knowledge: "We view Whale Rock as a continuous learning machine, aiming to compound knowledge over decades rather than just quarters." — Source: Capital Allocators

- On team dynamics: "It’s not how many brain cells you have, it’s how the synapses fire together; the focus is on internal communication and shared insights." — Source: Capital Allocators

- On meeting volume: "A core component of our learning machine is conducting between 2,000 and 3,000 meetings annually with management teams, customers, competitors, and former employees." — Source: Capital Allocators

- On the scuttlebutt approach: "We rely on the scuttlebutt method to develop high-conviction insights from primary sources that aren't yet reflected in financial data." — Source: Capital Allocators

- On private market context: "You cannot fully understand public leaders without deeply researching their private disruptors, which is why a significant portion of our meetings are with private companies." — Source: Capital Allocators

- On structural stability: "Maintaining a small, stable team with high average tenure allows the learning machine to retain context across multiple technology cycles." — Source: Capital Allocators

- On translating data to conviction: "The goal of conducting thousands of meetings is to identify the subtle clues of technological shifts before they hit the income statement." — Source: Capital Allocators

- On intellectual curiosity: "If you are really intellectually curious and you want to spend 90% of your time critically thinking, the buyside is where you want to be." — Source: Capital Allocators

- On adapting the machine: "The learning machine framework must constantly adapt; applying it to AI requires entirely new vectors of research across compute infrastructure and model orchestration." — Source: Capital Allocators

Part 7: Volatility, Risk & The Long/Short Model

- On accepting volatility: "Volatility is a part of the ball game... it comes with the tech territory, and it is nearly impossible to fully protect against it while seeking high returns." — Source: Invest Like the Best

- On market humility: "When you're at the top, know you're not as smart as you think you are, and when you're at the bottom, know you're not as dumb as you think you are. Humility is an important aspect of this." — Source: Capital Allocators

- On the TMT long/short advantage: "The long/short format is great for TMT because there are always clear winners and losers, and the ability to short can dampen inherent volatility." — Source: Capital Allocators

- On shorting criteria: "On the short side, we target companies negatively impacted by new technology trends, representing the downside of the S-curve." — Source: Capital Allocators

- On the enterprise software short: "Traditional SaaS companies are facing a day of reckoning as CIOs reallocate budgets toward AI tokens and away from traditional software seats." — Source: Sohn Conference

- On legacy AI products: "Many legacy software companies' AI products are not very good and fail to drive meaningful growth or monetization." — Source: Sohn Conference

- On AI seat contraction: "AI-driven productivity will lead to a reduction in the number of software seats required by enterprises, severely compressing the margins of incumbents." — Source: Sohn Conference

- On concentration risk: "We run a concentrated, high-conviction portfolio, mitigating risk by focusing on dominant market players with strong competitive moats rather than speculative bets." — Source: Capital Allocators

- On shorting valuation hype: "We will aggressively short companies that possess deteriorating competitive positions masked by unreasonable valuations or market hype." — Source: Capital Allocators

Part 8: The Art of TMT Investing

- On foundational principles: "Our entire philosophy rests on finding the intersection of S-curve positioning, durable competitive advantage, and underappreciated earnings power." — Source: Capital Allocators

- On the danger of linearity: "The greatest mistake an investor can make in technology is treating a non-linear platform shift as a linear financial projection." — Source: Invest Like the Best

- On the value of specialization: "In the technology sector, it's important to be a specialist; the nuance of infrastructure and adoption cannot be grasped by a generalist approach." — Source: Capital Allocators

- On hardware complexity: "Server racks are no longer commodities but highly complex machinery; networking speeds are jumping annually, creating massive visibility for the few companies capable of innovating at that pace." — Source: Sohn Conference

- On Google's position: "Google has effectively won AI due to their proprietary TPU chips and their position as the only foundational model player among major public companies." — Source: Sohn Conference

- On the 1998 parallel: "The current state of AI infrastructure and adoption is deeply comparable to the internet inflection point of 1998, but moving at an exponentially faster rate." — Source: Sohn Conference

- On holding through swings: "We are willing to hold through short-term performance swings if the underlying mechanics of the S-curve thesis remain firmly intact." — Source: Capital Allocators

- On the limits of financial data: "Financial statements are backward-looking artifacts; true TMT investing requires observing the adoption metrics that dictate tomorrow's reality." — Source: Invest Like the Best

- On ecosystem lock-in: "We look closely at integration through SDKs and orchestration tools because they create high switching costs that a simple model swap cannot overcome." — Source: Invest Like the Best

- On long-term focus: "Ultimately, we are trying to identify generational winners before the broader market recognizes their full architectural and economic potential." — Source: Capital Allocators