Lessons from Jeffrey Gundlach

DoubleLine Capital founder Jeffrey Gundlach built his fixed-income track record on contrarian trades and mathematical reads of the yield curve. This collection outlines his specific mechanics for pricing risk in bond markets and measuring the long-term fallout of national debt.

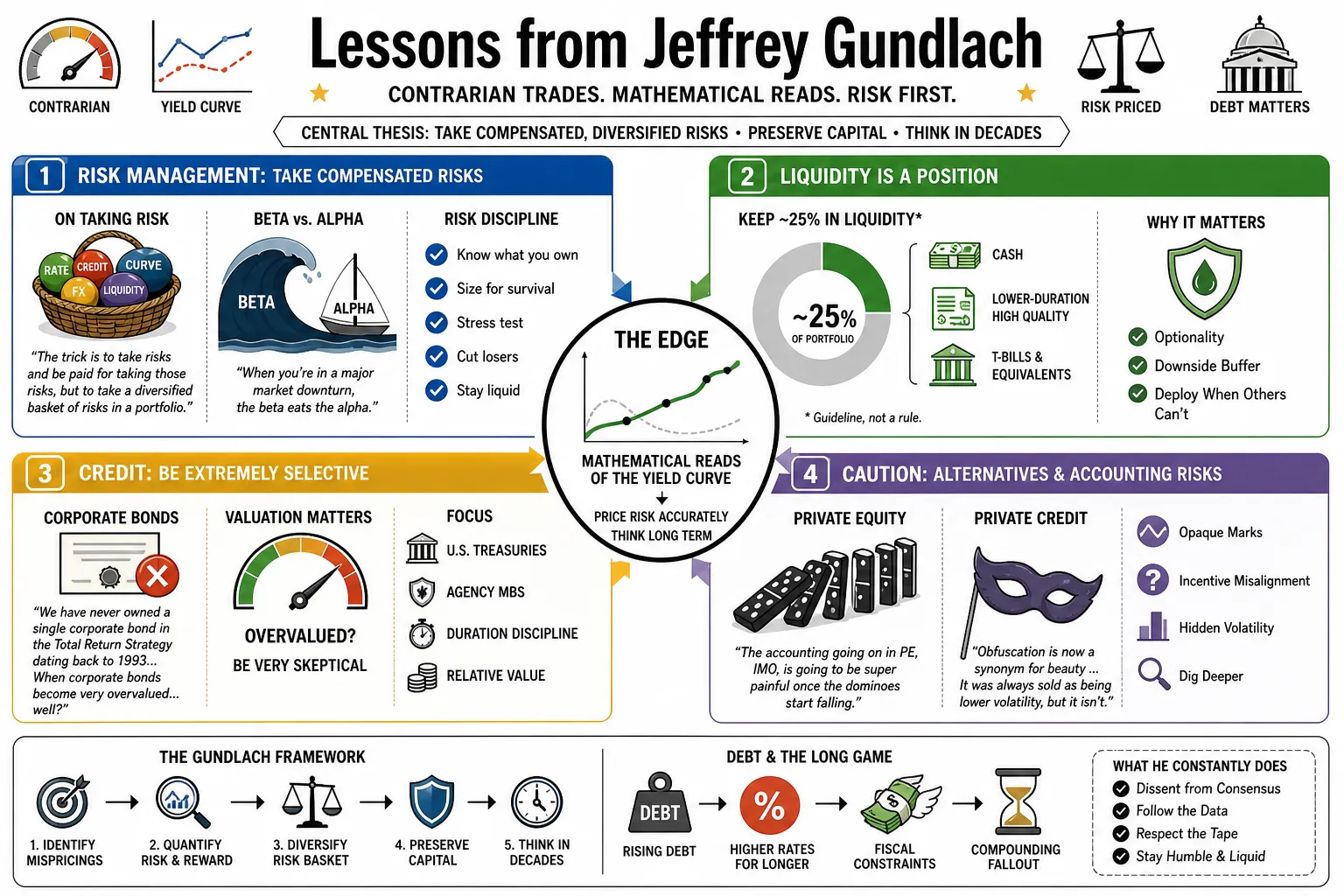

Part 1: Risk Management and Asset Allocation

- On taking risk: "The trick is to take risks and be paid for taking those risks, but to take a diversified basket of risks in a portfolio." — Source: [Medium]

- On beta vs. alpha: "When you're in a major market downturn, the beta eats the alpha." — Source: [Forbes]

- On corporate debt: "We have never owned a single corporate bond in the Total Return Strategy dating back to 1993... When corporate bonds become very overvalued... well?" — Source: [The Street]

- On liquidity: Maintaining roughly 25% of a portfolio in cash is vital, not restricted to T-bills but including lower-duration, high-quality fixed income. — Source: [DoubleLine]

- On private equity: "The accounting going on in PE, IMO, is going to be super painful once the dominoes start falling." — Source: [Business Insider]

- On private credit volatility: "Obfuscation is now a synonym for beauty [in private credit]... It was always sold as being lower volatility, but it’s really just 'laundered volatility'." — Source: [YouTube]

- On structural defensive posture: A defensive posture should include 40% in intermediate-term fixed income. — Source: [DoubleLine]

- On illiquid funds: "I expect redemption requests from interval funds to surge... When you can’t get out, it makes you want to get out even more." — Source: [YouTube]

- On tail risk hedging: Hold about 10% in long Treasuries with the lowest coupon possible as crash protection against government debt restructuring. — Source: [DoubleLine]

- On preparation: "It won’t matter if it’s raining a half an inch an hour, or raining two inches an hour—in either case you need an umbrella." — Source: [Business Insider]

Part 2: The Macroeconomic Environment

- On economic regimes: "A lot of the things that we thought we knew... may have been informed by a secular environment that has changed." — Source: [YouTube]

- On broken indicators: "Some of the traditional recession indicators don’t work... because they worked during a different secular regime." — Source: [YouTube]

- On the yield curve shape: "In spite of the fact that inflation is going to be reluctant to come down, I just think the shape of the yield curve is the best indicator of the forward economy." — Source: [Business Insider]

- On de-inversion: "The curve deinverting is highly suggestive of recession, and the dollar is going to have big problems in the next recession." — Source: [Business Insider]

- On recession probabilities: The economy often tips from a 50% chance of recession rapidly to a "75% chance of running into recession." — Source: [Business Insider]

- On the post-pandemic economy: "We are never going back to the January 2020 'You blow dry my hair and I'll blow dry your hair' economy." — Source: [Business Insider]

- On valuing skills: "Saving money and having a net economically productive skill will be the new cool." — Source: [Business Insider]

- On organic growth vs. debt: The United States struggles to grow in an organic way when national debt growth constantly outstrips GDP growth. — Source: [Real Vision]

- On consumer spending: "We’ve had a moment of respite because of all the free money from the government... It’s gone back to credit card spending; we’re starting to see those write-offs." — Source: [YouTube]

- On unemployment averages: Rising unemployment rates crossing above their 12-month and 36-month moving averages is a definitive recessionary signal. — Source: [Moomoo]

Part 3: The Bond Market and Treasuries

- On the traditional safe haven: "There's an awareness now that the long-term Treasury bond is not a legitimate flight-to-quality asset." — Source: [The Street]

- On the 30-year Treasury: "I think this is going to be a very long drawdown period for the price of the 30-year Treasury." — Source: [YouTube]

- On duration risk: Long-duration maturities are dangerous because a bond "doesn’t pull to par very quickly because of its long duration maturity." — Source: [YouTube]

- On the 10-year Treasury: "The sell-off in the 10-year Treasury for the short term might be overdone... directionally [the yield and economic surprise index] are very different." — Source: [YouTube]

- On finding his niche: The bond market perfectly matched his quantitative skills, allowing mathematical discipline to lead decision making. — Source: [Wave]

- On short-duration preference: Favor shorter-duration assets and agency mortgages over long-term risk. — Source: [DoubleLine]

- On U.S. debt restructuring: A U.S. Treasury debt restructuring is a legitimate tail risk worth understanding as the fiscal trajectory continues to deteriorate. — Source: [YouTube]

- On national debt sustainability: "A reckoning is coming" regarding the sustainability of U.S. national debt and deficits. — Source: [The Street]

- On government borrowing limits: "If endless borrowing is a viable solution, why did we have any taxation in the first place?" — Source: [YouTube]

Part 4: The Federal Reserve and Monetary Policy

- On Jerome Powell: "The guy is really at heart Mr. Magoo. He can’t see very well. He’s got that jalopy and crashes into dumpsters and stuff." — Source: [DoubleLine]

- On the 'Mr. Magoo' economy: "We are back in the situation of 'Mr. Magoo,' driving around in the car crashing everywhere... we can just wait and see what tree we will crash into." — Source: [Moomoo]

- On QE permanence: "Quantitative easing is NOT going away. Every major country is running a deficit." — Source: [Business Insider]

- On central bank balance sheets: "If they are all net borrowers then who is the lender? The central banks." — Source: [Business Insider]

- On the Powell Put: Federal Reserve policy pivots might temporarily save market pricing, but they consistently fail to fix underlying economic deterioration. — Source: [Real Vision]

- On slashing rates: "If you slash interest rates, then you're not only running a weaker dollar policy, but you're running an inflationary policy." — Source: [Business Insider]

- On future rate policy: "We’re going to have an inflationary response to the next period of economic weakness." — Source: [Business Insider]

- On funny money: When central banks distribute money people do not need, the public begins to treat capital like casino house money. — Source: [YouTube]

- On momentum-based markets: Massive central bank intervention creates market structures that are 100 percent momentum-based rather than fundamental. — Source: [Business Insider]

Part 5: Inflation and the U.S. Dollar

- On a doomed currency: The dollar is doomed in the long term due to the explosion of trade and budget deficits. — Source: [Real Vision]

- On the secularly weak dollar: "My central investment theme now for about two years has been center your portfolio positioning around the idea that the dollar is going to be secularly weak." — Source: [Business Insider]

- On interest expense: The U.S. dollar will decline in future recessions because the national interest expense problem is becoming mathematically real. — Source: [YouTube]

- On the second wave of inflation: The government's standard response to recessions by printing money will inevitably cause secondary waves of inflation. — Source: [Barron's]

- On yield curve and inflation: "With yield curve steepening we may get inflation in 2026." — Source: [Substack]

- On needs-based inflation: "Consumers are getting crushed because the things that you need are still very high in price and they’re not going down." — Source: [ThinkAdvisor]

- On hidden inflation drivers: "Auto insurance... is a major force driving inflation." — Source: [ThinkAdvisor]

- On market trends and policy: "Market trends and policy outcomes are interconnected evidence pointing to structural shifts." — Source: [YouTube]

- On the limits of monetary solutions: Modern monetary theory and perpetual easing have led global central banks into a mathematical dead end. — Source: [Barron's]

Part 6: Equities, Gold, and Alternatives

- On the tech bubble parallel: "I turned negative on the Nasdaq September 30th, 1999... I feel like we're in that type of an environment [again]." — Source: [Business Insider]

- On stock market sentiment: "Consumers' expectation of higher stock prices were on a moonshot already... I do not view this as bullish." — Source: [YouTube]

- On equity downside: The S&P 500 holds significant downside risk in a recessionary environment, potentially falling to 4,600 points. — Source: [Moomoo]

- On emerging markets: A diversified equity portfolio should lean toward foreign stocks like emerging markets over domestic concentrations. — Source: [YouTube]

- On gold vs. crypto: "It’s apparent that gold has outperformed Bitcoin for four years... I think gold is the real money." — Source: [YouTube]

- On gold's track record: "Gold has also done better than the S&P 500 for the past 25 years going back to 2000." — Source: [YouTube]

- On gold price targets: Gold should be a permanent allocation and could rise to $4,000 due to geopolitical turmoil, tariffs, and massive national debt. — Source: [Moomoo]

- On cryptocurrency: While initially open to Bitcoin at lower valuations, the crypto space has become a poster child for speculative fervor. — Source: [YouTube]

- On hard assets: "Less than one month of 2026, what's outperforming? It's the precious metals, it's commodities... that train just keeps on rolling." — Source: [Business Insider]

- On commodities allocation: Maintain a sizable allocation of up to 20 percent in real assets and gold to hedge against fiat debasement. — Source: [YouTube]

Part 7: Housing and the Consumer Economy

- On home price ceilings: "It’s hard to see how home prices can go up much more without significant income expansion." — Source: [Substack]

- On housing affordability: "Affordability has decreased very markedly... the monthly payment for the same house from two years ago is now double." — Source: [Fox Business]

- On stagnating property markets: "Home prices... are rising about 2.0% year-over-year, but for the last several months prices have declined." — Source: [Substack]

- On consumer fatigue: The average consumer is fundamentally exhausted by the compound effect of high prices and high interest rates. — Source: [Fox Business]

- On real estate dynamics: Housing functions less as a speculative growth engine and more as a trap for new buyers when rates stay elevated. — Source: [Fox Business]

- On wage stagnation: Without real, inflation-adjusted wage growth, the foundational pillars of the U.S. consumer economy begin to fracture. — Source: [Substack]

- On credit card debt: The exhaustion of pandemic-era stimulus forces consumers to bridge the gap with high-interest credit, accelerating write-offs. — Source: [YouTube]

- On living standards: The standard of living is stealthily eroding because the cost of necessities outpaces nominal wage gains. — Source: [ThinkAdvisor]

- On the illusion of wealth: Rapidly rising asset prices give consumers an illusion of wealth that vanishes the moment credit conditions tighten. — Source: [YouTube]

Part 8: Intellectual Models, Mathematics, and Art

- On infinity: "My thesis was the probabilistic implications of the nonexistence of infinity... There is no infinity. It's an illusion." — Source: [Forbes]

- On mathematical application: "There is absolutely nothing empirical that suggests infinity exists and nothing that operates under the assumption of infinity that has any practical implications." — Source: [Forbes]

- On market observation: "I really kind of interpret society through how the markets work." — Source: [Forbes India]

- On the illusion of philosophy: "Wittgenstein was a mathematical philosopher, and his whole thing is that philosophy is just words that don't mean anything. It's like a fly that goes into a fly bottle and can't find its way out." — Source: [Forbes]

- On constant change: Relying on Heraclitus's maxim to explain markets: "No man ever steps in the same river twice, for it's not the same river, and he's not the same man." — Source: [Forbes India]

- On emotional discipline: The core tenet of his entire intellectual framework is simply that discipline beats emotion. — Source: [Forbes]

- On art appreciation: After dismissing modern art as a scam, a 2002 viewing of John Singer Sargent changed his perspective: "The quality of the paint in the light is just beautiful." — Source: [Forbes India]

- On artistic geometry: Art can be deeply mathematical; minimalist works are often governed by the Fibonacci sequence, a rule that happens to describe the shape of the solar system. — Source: [Forbes India]

- On taking decisive action: Borrowing a physical metaphor for market execution: "Paint or get off the ladder." — Source: [Forbes India]