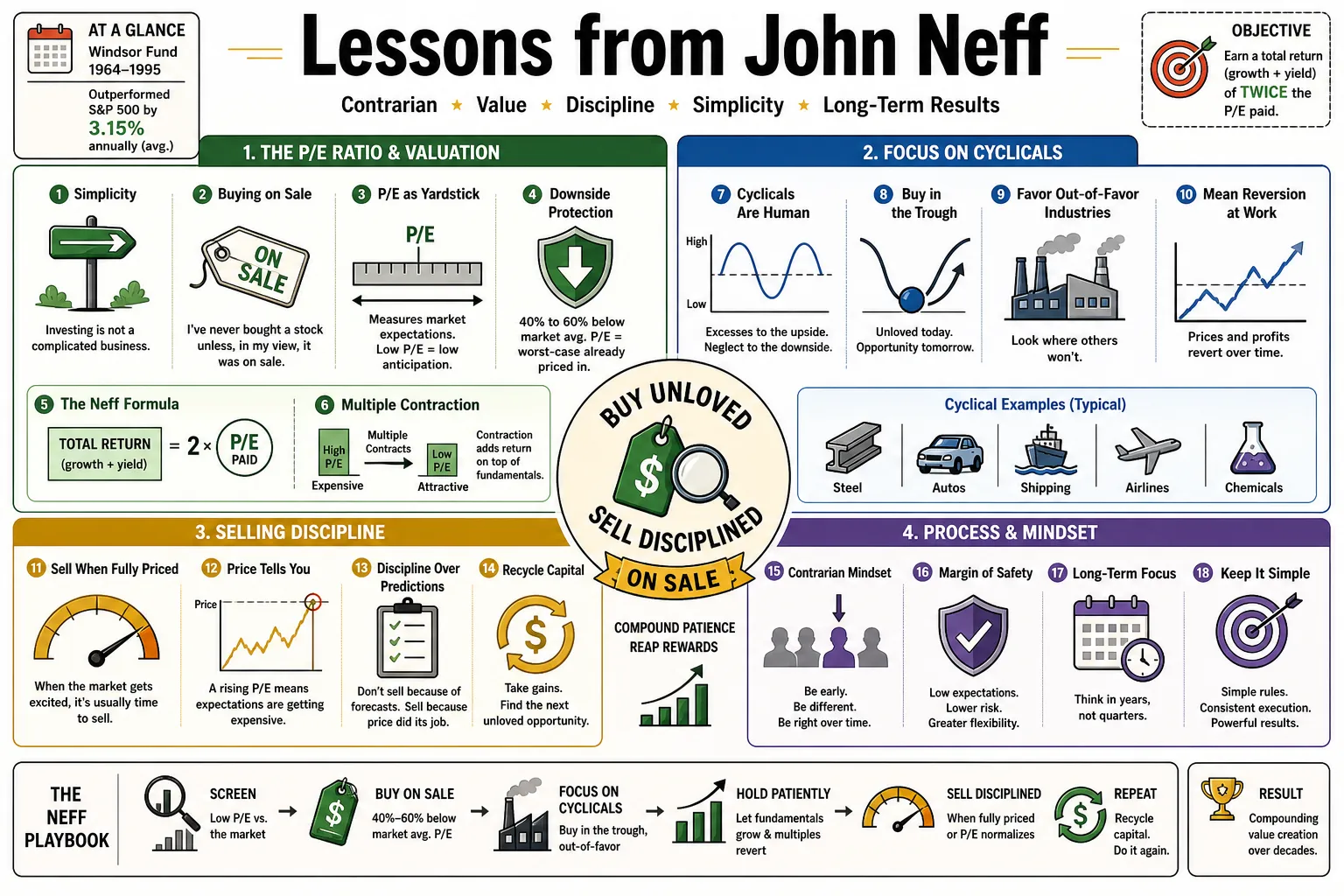

John Neff managed Vanguard's Windsor Fund from 1964 to 1995, famously outperforming the S&P 500 by an average of 3.15% annually over his three-decade tenure. He is best known for his strict, low-P/E investing framework and a contrarian methodology that actively sought out "unloved" stocks. This profile explores his specific rules for valuation, cyclicals, and selling discipline.

Part 1: The P/E Ratio and Valuation

- On Simplicity: "Investing is not a complicated business. People just make it complicated." — Source: [Medium]

- On Buying on Sale: "I’ve never bought a stock unless, in my view, it was on sale." — Source: [Hedge Fund Alpha]

- On the Price-to-Earnings Yardstick: Neff viewed the P/E ratio not just as a math formula, but as a yardstick for market expectations, noting that low P/E stocks have little anticipation built into their price. — Source: [The P/E Investor]

- On Downside Protection: Stocks trading 40% to 60% below the market average P/E provide inherent downside protection because the market has already priced in the worst-case scenario. — Source: [AAII]

- On the Neff Formula: "Our goal at Windsor was always to earn a total return—growth rate plus yield—of twice the P/E we paid." — Source: [Masters Invest]

- On Multiple Contraction: Buying stocks with high P/E multiples leaves no margin for error; if earnings growth slows even slightly, the resulting multiple contraction will devastate the stock price. — Source: [Interactive Brokers]

- On Paying for Earnings: "Windsor hunted for stocks with a cheapo profile; their total return divided by the P/E ratio was notably out of line with industry or market benchmarks." — Source: [Masters Invest]

- On Glamour Stocks: Investment success does not require chasing glamour stocks; in fact, avoiding them is often the prerequisite for long-term outperformance. — Source: [QuotesWise]

- On Terminal Relationships: He specifically looked for what he called "terminal relationships," where the fundamental value of a company was totally disconnected from its suppressed valuation multiple. — Source: [Fincash]

Part 2: Contrarianism and Market Psychology

- On Popularity: "It’s not always easy to do what’s not popular, but that’s where you make your money." — Source: [Business Insider]

- On Arguing with the Market: "My whole career, I have argued with the stock market. Happily, as the Windsor Fund’s record shows, I won more arguments with the market than I lost." — Source: [QuotesWise]

- On Ugly Stocks: "To us, ugly stocks were often beautiful." — Source: [Masters Invest]

- On Market Irrationality: "The market is irrational and unsentimental. It is cantankerous and hostile. At times, it is forgiving and congenial... You can't predict them, but you can learn to cope with them." — Source: [QuotesWise]

- On Extending Straight Lines: "Most investors are great at extending straight lines… that culminate in disappointment when enthusiasm wanes." — Source: [QuotesWise]

- On the Risk of Embarrassment: "Windsor's success ultimately flowed from our willingness to step outside the crowd's embrace and be exposed to the risk of embarrassment." — Source: [Masters Invest]

- On Conventional Wisdom: "Conventional wisdom and preconceived notions are stumbling blocks as well as signs of opportunity." — Source: [QuotesWise]

- On Out-of-Fashion Opportunities: "Being out of fashion ultimately enhances opportunities on the other side." — Source: [QuotesWise]

- On Reversion to the Mean: "Frenzies end, fundamentals prevail, and every tub sits on its own bottom." — Source: [QuotesWise]

Part 3: Growth, Dividends, and Total Return

- On the Total Return Ratio: He popularized evaluating a stock by adding its earnings growth rate to its dividend yield, and then dividing that sum by its P/E ratio. — Source: [Wikipedia]

- On Dividend Yield as Free Return: Neff considered dividends a "free plus" that rewarded an investor's patience while waiting for the broader market to recognize a stock's true value. — Source: [The P/E Investor]

- On the 2% Edge: Of his 3.15% annualized outperformance against the market, Neff attributed roughly 2% entirely to the superior dividend yields of the stocks he selected. — Source: [Invest Wizardry]

- On Yield Protection: He actively targeted companies offering dividend yields in the 4% to 5% range to act as a safety net during severe market downturns. — Source: [AAII]

- On Sustainable Growth: He favored companies with steady earnings growth of 7% to 20%, noting that anything higher was rarely sustainable over the long term. — Source: [AAII]

- On Hyper-Growth Dangers: He actively avoided hyper-growth companies, arguing that the expectations baked into their prices carried unacceptable levels of risk. — Source: [The P/E Investor]

- On Future vs. Past Stocks: "My emphasis was on stocks with a future instead of stocks with a past." — Source: [Sahm Capital]

- On Moderate Growth: He categorized a large portion of his portfolio as "Moderate Growth"—solid, boring citizens in mature industries that compounded wealth quietly. — Source: [Forbes]

- On Dividend Discipline: A high dividend yield forced management to remain disciplined with capital allocation, preventing them from squandering cash on foolish acquisitions. — Source: [Interactive Brokers]

Part 4: Finding the "Cheapo" Profile

- On Beaten-Down Stocks: "The stocks Windsor bought usually had had the stuffing beaten out of them." — Source: [QuotesWise]

- On Bargain Basement Opportunities: He believed the market frequently overreacts to bad news, creating artificial "bargain basement" pricing for fundamentally sound businesses. — Source: [Gracious Quotes]

- On Less Recognized Growth: Neff hunted for smaller, low-visibility companies growing at 12% to 20% that the broader market simply hadn't noticed yet. — Source: [The P/E Investor]

- On the Core Windsor Fare: "Typical Windsor fare featured good companies with solid market positions and evidence of room to grow." — Source: [Hedge Fund Alpha]

- On Catching Falling Knives: He was willing to buy stocks that were actively dropping, provided his underlying calculations of total return and intrinsic value remained intact. — Source: [Interactive Brokers]

- On Highly Recognized Growth: He only bought big-name, highly recognized growth stocks when they were temporarily "in the dumper" due to short-term market panic. — Source: [AZ Quotes]

- On Wait Times: "If you buy stocks when they are out of favor and unloved, and sell them into strength when other investors recognize their merits, you’ll often go home with handsome gains." — Source: [QuotesWise]

- On Ignoring the Noise: He ignored the daily fluctuations of stock prices, focusing exclusively on whether a company's "cheapo" profile still offered a mathematical advantage. — Source: [Masters Invest]

- On Unloved Industries: He routinely screened for entire sectors that had fallen out of favor, knowing that cyclical pessimism eventually creates deep value. — Source: [The P/E Investor]

Part 5: Cyclical Stocks and "Measured Participation"

- On Cyclical Allocation: Neff routinely allocated up to one-third of the Windsor Fund to basic industry cyclical stocks, provided the price was right. — Source: [SlideShare]

- On the Compensating Multiple: He refused to buy cyclical stocks without a "compensating multiple"—a P/E ratio low enough to justify the extreme volatility of the business cycle. — Source: [The P/E Investor]

- On Contrarian Timing: He preferred to buy cyclicals 6 to 9 months before an anticipated economic recovery, stepping in exactly when pessimism was highest. — Source: [The P/E Investor]

- On Selling Cyclicals: Neff was ruthlessly disciplined about selling cyclicals just before their earnings hit absolute peak, never waiting for the cycle to actually turn downward. — Source: [SlideShare]

- On Indirect Paths: To avoid overpaying for trending cyclical industries, he bought the underlying suppliers—for example, buying pipe manufacturers instead of expensive oil drillers. — Source: [SlideShare]

- On Measured Participation: He developed a system of "measured participation" to limit his exposure to any single cyclical downturn, spreading risk across different basic industries. — Source: [The P/E Investor]

- On Timing the Bottom: He acknowledged that timing the exact bottom of a cyclical stock was impossible, which is why the dividend yield was required to offset the wait. — Source: [AAII]

- On Earnings Upturns: He required concrete, measurable evidence that an earnings upturn was imminent before committing capital to a depressed cyclical company. — Source: [The P/E Investor]

- On Cyclical Traps: He warned that buying cyclicals at high multiples during boom times was one of the most reliable ways for an investor to destroy their capital. — Source: [Interactive Brokers]

Part 6: Risk Management and Fundamental Analysis

- On Information Overload: "Conventional wisdom suggests that, for investors, more information these days is a blessing and more competition is a curse. I'd say the opposite is true." — Source: [QuotesWise]

- On Focusing on Key Variables: "Coping with so much information runs the risk of distracting attention from the few variables that really matter." — Source: [QuotesWise]

- On the Durability of Earnings: "I assigned great weight to a judgement about the durability of earnings power under adverse circumstances." — Source: [Sahm Capital]

- On Broad Diversification: "Obsession with broad diversification is the sure road to mediocrity." — Source: [QuotesWise]

- On Low-Tech Analysis: He insisted on "low-tech" security analysis, preferring to read physical annual reports and dig into the books rather than relying on complex computer models. — Source: [The P/E Investor]

- On Accounting Tricks: He required proof that a company's growth was driven by actual sales and expanding margins, not just financial engineering or accounting tricks. — Source: [The P/E Investor]

- On M&A Distortions: He warned that corporate earnings data frequently becomes muddied by aggressive mergers and restructuring, requiring investors to manually normalize the numbers. — Source: [The P/E Investor]

- On Corroborating Data: He advised investors to always corroborate company-issued financial data with basic common sense and outside industry sources. — Source: [The P/E Investor]

- On Faulty Fundamentals: In analyzing his own mistakes, he found that misjudging a company's basic economic structure or the effectiveness of its management was his most common error. — Source: [SlideShare]

- On Concentration Risk: He cautioned individuals against investing heavily in their own employer, noting that a business failure could simultaneously destroy their salary and their retirement savings. — Source: [SlideShare]

Part 7: Selling Discipline and Portfolio Management

- On Bragging Rights: "Successful stocks don't tell you when to sell. When you feel like bragging, it's probably time to sell." — Source: [Hedge Fund Alpha]

- On Warm Fuzzies: "An awful lot of people keep a stock too long because it gives them warm fuzzies—particularly when a contrarian stance has been vindicated." — Source: [Business Insider]

- On Losing Bragging Rights: "If they sell it, they lose bragging rights." — Source: [Business Insider]

- On Selling into Strength: "We don't forget to sell into strength. A lot of people can't bear to sell when a stock's price is going up... My attitude is that we're not that smart." — Source: [Novel Investor]

- On Falling in Love: "Falling in love with stocks in a portfolio is very easy to do and, I might add, very perilous." — Source: [Masters Invest]

- On Everything Being for Sale: "Every stock Windsor owned was for sale." — Source: [Masters Invest]

- On Being Stubborn: "There is a thin line between being a contrarian and being just plain stubborn." — Source: [Interactive Brokers]

- On Reaching Fair Value: He insisted on selling the exact moment a stock reached his pre-calculated estimate of fair value, regardless of its upward momentum. — Source: [SlideShare]

- On Admitting Mistakes: If fundamental analysis proved faulty, Neff advocated taking the loss immediately rather than holding on and hoping for a turnaround. — Source: [The P/E Investor]

- On Average Holding Periods: His average holding period for a stock was roughly three years, demonstrating that his contrarian approach required a medium-term horizon to play out. — Source: [Wikipedia]

Part 8: Institutional Groupthink and Investor Temperament

- On Patience: "Patience is a virtue in investing. Sometimes, the best decision is to do nothing and wait for the right opportunities." — Source: [Gracious Quotes]

- On Investment Committees: He believed investment committees often suffocate performance by clinging to safe, well-known names to avoid career risk. — Source: [SlideShare]

- On Institutional Groupthink: He spent his career actively condemning institutional groupthink, preferring a lean operational team with a single, independent vision. — Source: [Masters Invest]

- On the Nifty Fifty: He explicitly warned against chasing "highly recognized growth stocks," noting that market favorites eventually hit ridiculously expensive levels and collapse. — Source: [SlideShare]

- On Fear and Hype: He operated on the age-old market principle: buy on the cannons (fear) and sell on the trumpets (hype). — Source: [The P/E Investor]

- On Open Minds: "Savvy contrarians keep their minds open, leavened by a sense of history and a sense of humour." — Source: [Masters Invest]

- On Tactical Patience: He was not a day trader; he viewed himself as a "tactical contrarian" who bought value and sat on his hands until the market realized it was wrong. — Source: [Gracious Quotes]

- On Following the Herd: He argued that following the herd guarantees average returns at best, and severe capital destruction at worst. — Source: [QuotesWise]

- On Managing Temperament: He believed that successful investing was more a matter of emotional temperament and discipline than raw intellect. — Source: [Interactive Brokers]

- On Arguing with the Market: He viewed the stock market not as an efficient pricing mechanism, but as an emotional entity to be argued with, debated, and ultimately outsmarted. — Source: [QuotesWise]