Ken Fisher is a billionaire investment analyst, the founder of Fisher Investments, and the longest-running columnist in the history of Forbes magazine. He is best known for developing the Price-to-Sales Ratio as a valuation metric in the 1980s and for his contrarian approach to behavioral finance. The following quotes and insights capture his methodology for valuing companies, navigating market history, and finding advantages where the crowd is wrong.

Part 1: Contrarian Thinking & The Crowd

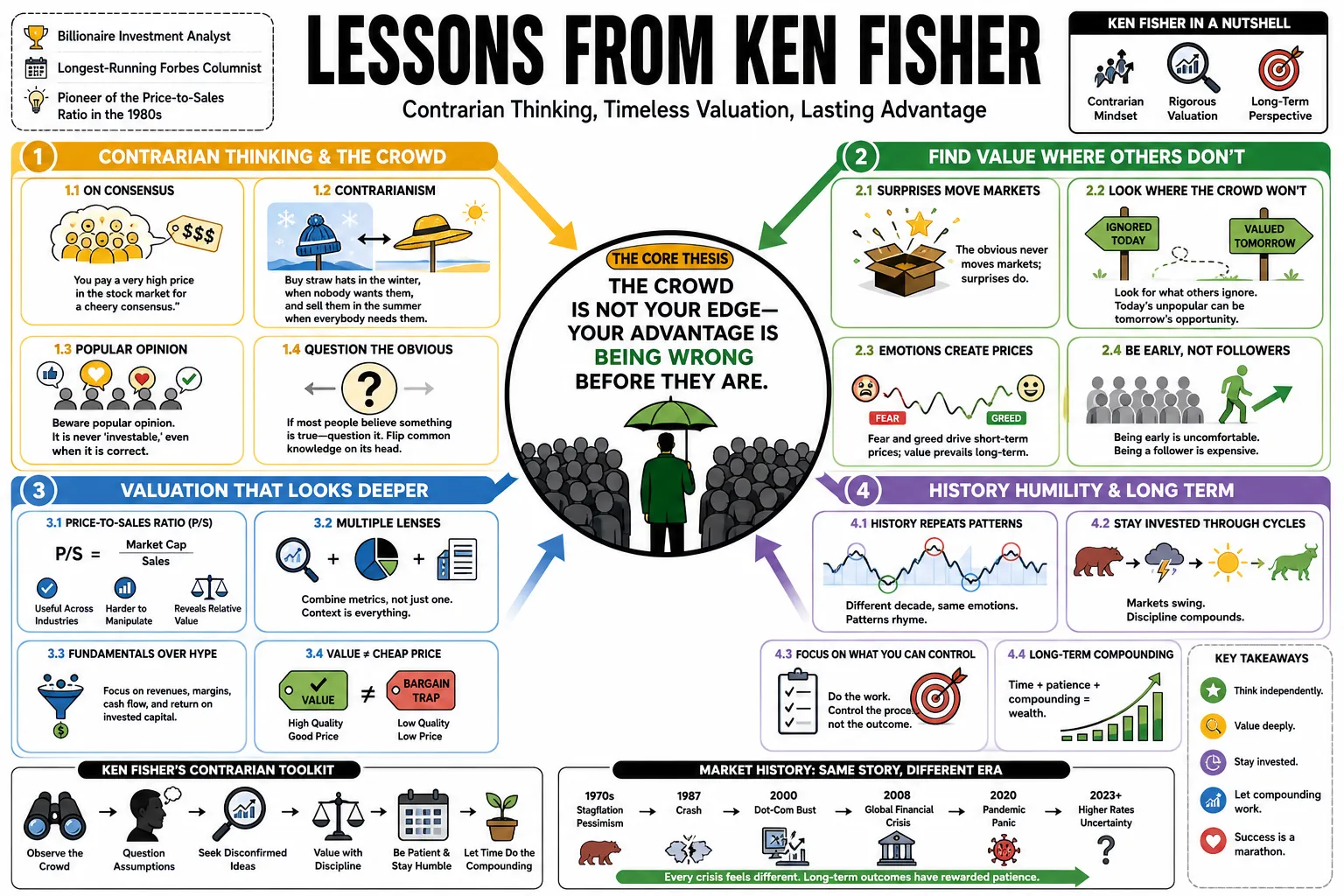

- On Consensus: "You pay a very high price in the stock market for a cheery consensus." — Source: Fisher Investments

- On Contrarianism: "Buy straw hats in the winter, when nobody wants them, and sell them in the summer when everybody needs them." — Source: Goodreads

- On Popular Opinion: "Beware popular opinion. It is never ‘investable,’ even when it is correct. That’s because the market has already discounted popular opinion." — Source: Bookey

- On Questioning the Obvious: "If most people believe something is true—question it. Flip common knowledge on its head. If everyone says something is bad, dare to ask, ‘What if it’s good?’" — Source: Dokumen

- On Surprises: "The obvious never moves markets; surprises almost always do." — Source: Goodreads

- On The Crowd: "In investing, the crowd is wrong much more often than right." — Source: Quoteswise

- On Unloved Assets: "A stock only has real potential if most folks think it has none at all." — Source: Quoteswise

- On Knowing What Others Don't: "The only way to consistently beat the markets is by knowing something others don’t know." — Source: VDoc

- On Being Different: "Different, not opposite. That’s the key to using professional forecasts—and the key to being a contrarian." — Source: VDoc

Part 2: The Great Humiliator & Market Mechanics

- On Market Intent: "The stock market—or rather, by its proper name, The Great Humiliator—wants to use your intuition and gut instincts against you." — Source: Dokumen

- On Discounting Information: "TGH is a discounter of all known information. It succeeds by making sure that whatever we all know is either wrong or is already priced into securities." — Source: VDoc

- On False Confidence: "People must be right sometimes, must feel good sometimes, or we’d never have a herd... The occasional rightness fosters false confidence." — Source: VDoc

- On Market Efficiency: "It's a good idea to remember that whenever there is a buyer and a seller, somebody is wrong. Make sure it's not you." — Source: Fisher Investments

- On Markets Leading the Economy: "The stock market is almost magical because it always leads the economy. It goes down long before the economy drops and then heads higher long before the economy rebounds." — Source: Goodreads

- On Supply and Demand: "The only two things that move stock prices are the supply of securities, such as IPOs and buybacks, and the demand for them based on investor sentiment and liquidity." — Source: Fisher Investments

- On Forecasting Economic Downturns: "It is impossible to outguess the stock market based on estimates of where the economy is headed, but… the stock market is a good forecaster of economic downturns." — Source: CXO Advisory

- On IPOs: "IPOs sell on their sizzle and sex appeal. They're usually classified as high-risk growth stocks." — Source: Goodreads

- On The Wall of Worry: "Bull markets climb a wall of worry and typically end not when things look bad, but when they look perfect and euphoric." — Source: Masnar Capital

- On Presidential Cycles: "The third and fourth years of a presidential term are historically the strongest for stocks regardless of which party is in power." — Source: Fisher Investments

Part 3: Behavioral Finance & Cognitive Bias

- On Self-Deception: "The first principle is that you must not fool yourself—and you are the easiest person to fool." — Source: VDoc

- On Evolutionary Biology: "Our reptilian brains are not well adapted for our current environment." — Source: VDoc

- On Running Alone: "There is always a temptation to let popular opinion dissuade you from acting on your own proprietary knowledge. It’s hard to run alone." — Source: VDoc

- On Investor Psychology: "The investor's principal problem is likely to be himself. How your investments behave is a lot less crucial than how you behave." — Source: Inc

- On Emotion: "Investors should be wary of making investment decisions based on emotion—especially during tumultuous times." — Source: Fisher Investments

- On Loss Aversion: "Humans feel the pain of a loss about two and a half times more than the joy of a gain, which often causes investors to sell at the bottom during volatility." — Source: Fisher Investments

- On Pessimism: "Readers regularly ask what can go wrong but almost never what could positively surprise." — Source: Medium

- On Handling Emotion: "How you handle your emotions is more important than how you handle your stocks." — Source: Fisher Investments

- On Cognitive Errors: "Many investors fail to question if what they believe is true—and are therefore blinded by tradition, biases, ideology, or any number of cognitive errors." — Source: Goodreads

Part 4: Time vs. Timing

- On Patience: "Buy into good well-researched companies and then wait. Let's call it a sit-on-your-hands investment strategy." — Source: Meb Faber

- On Action vs. Inaction: "You usually make more money sitting on your hands than dancing on your feet." — Source: Simtrade

- On Duration: "The duration on an investment (the time in the market) is a significantly better factor of success for your investments than the quality of your attempts to optimize entry and exit points." — Source: Simtrade

- On The Golden Rule: "Time in the market beats timing the market—almost always." — Source: Simtrade

- On Timing Perfection: "Even the greatest investors are wrong maybe a third of the time. But here's some good news: You don't need perfect timing to achieve marvelous returns." — Source: Simtrade

- On Easing In: "If the market rises more than it falls most of the time, easing in is, by definition, a loser's game." — Source: Medium

- On Cost of Being Out: "Because the stock market rises in roughly two out of every three years, the cost of being out of the market during its inevitable rebounds usually far exceeds the risk of staying in during downturns." — Source: Fisher Investments

- On Market Timing Success: "Consistently timing the market is nearly impossible. Rather than worrying about where the market is headed in the short term, stick to your long-term investment plan." — Source: Fisher Investments

- On Selling: "The right time to sell a Super Stock is almost never." — Source: Business Insider

Part 5: Super Stocks & Valuations

- On Super Stocks: "A Super Stock is the stock of a Super Company bought at a price appropriate to an inferior company." — Source: Portfolio123

- On Super Companies: "To find Super Stocks, you must first find Super Companies. A Super Company is one that can grow at a rate of 15% to 20% per year, has a long-term average after-tax profit margin of 5% or more, and has a competitive advantage that is difficult for others to duplicate." — Source: Scribd

- On Valuing Growth Without Earnings: "Very few investors have a rational basis for valuing growth stocks in the face of a lack of earnings. The stock loses supporters and falls, in time, much too far." — Source: Business Insider

- On The Glitch Theory: "Almost every young, high-growth company eventually hits a temporary operational or marketing setback, causing a panic sell-off that presents the ultimate buying opportunity." — Source: Coreenne

- On Rebounds: "The best managements react to difficulties and overcome them... Simultaneously with the profit resurgence, the stock price begins to rebound." — Source: Business Insider

- On Buying Ranges: "Look for stocks with a Price-to-Sales Ratio below 0.75 as the primary tool for identifying undervalued growth." — Source: Scribd

- On Avoidance Limits: "Never buy a stock with a Price-to-Sales Ratio greater than 3.0." — Source: Portfolio123

- On Selling Points: "Consider selling a stock when its Price-to-Sales Ratio reaches 3.0 to 6.0." — Source: Substack

- On Research Valuation: "For technology and growth companies, utilize the Price-to-Research Ratio, targeting an ideal PRR between 5 and 10." — Source: Forbes

- On Innovation Caps: "Avoid any stock with a Price-to-Research Ratio greater than 15." — Source: Portfolio123

Part 6: Debunking Conventional Wisdom

- On Myths: "If everyone knows something, question it." — Source: SoBrief

- On Market Returns: "Normal returns are extreme. Average returns are made up of the average of extreme returns. You’ve got to like extreme." — Source: Meb Faber

- On Volatility Nature: "The so-called average annual return of 10% rarely actually happens in a single year; instead, markets usually swing wildly above or below that number." — Source: SoBrief

- On Small-Caps: "While small caps have periods of outperformance, they also have long periods of underperformance. No single asset class is strictly best for all time." — Source: Goodreads

- On Bonds vs. Stocks: "While bonds have less price volatility, they carry significant inflation and opportunity cost risk over long periods, making them potentially riskier for long-term goals." — Source: Wiley

- On Unemployment: "By the time unemployment is high, markets, which are forward-looking, have often already priced in the bad news and are starting to recover." — Source: YouTube

- On Trade Deficits: "Trade deficits are often a symptom of strength, representing a wealthy nation buying more, rather than a cause of economic weakness." — Source: Fisher Investments

- On History: "The past is never predictive. That something happened a certain way in the past doesn't mean it must happen that way in the future." — Source: Quoteswise

- On Memory: "Markets never forget, but people do." — Source: Quoteswise

Part 7: Risk, Volatility, & Uncertainty

- On Uncertainty: "Uncertainty is the friend of the buyer of long-term values." — Source: Fisher Investments

- On Risk Management: "Divide capital into 10 equal parts and never risk more than a tenth of it on any one trade." — Source: Goodreads

- On Volatility as a Tool: "Volatility is your friend, it’s not your enemy, if you use it correctly." — Source: Meb Faber

- On Hidden Risks: "Volatility risk is just one kind of risk. Investors often ignore the risk of not growing their capital enough to outpace inflation." — Source: SoBrief

- On Probabilities: "Investing is a probabilities game, not a certainties game." — Source: Quoteswise

- On Global Diversification: "Limiting a portfolio to one country increases risk and misses opportunities in the global capitalist engine." — Source: Fisher Investments

- On Capitalism: "Capitalism is a bigger force than any anti-capitalistic forces." — Source: SoBrief

- On Priced-In Risks: "If a risk is widely discussed in the media, it is almost certainly already priced into the market." — Source: Fisher Investments

- On Panic: "Most investors give too much credence to the theory that prices are rational; they presume that a market collapse must have been justified by serious economic trouble." — Source: Masnar Capital

Part 8: Strategy & Avoiding Mistakes

- On Avoiding Errors: "The most important thing in investing is to avoid big mistakes—not to be perfectly right." — Source: Seeking Alpha

- On Investment Success: "Investing success is two-thirds avoiding mistakes, one-third doing something right." — Source: Quoteswise

- On Grit: "Investing success requires grit, discipline, alligator skin, and the clearer vision you can get through debunkery." — Source: SoBrief

- On Lowering Error Rates: "Your goal as an investor shouldn't be to be error-free—that's impossible. Rather, to be more successful, you should aim to lower your error rate." — Source: SoBrief

- On The Most Common Mistake: "What is the most common investor mistake? Trading – getting in and getting out at all the wrong times, for all the wrong reasons." — Source: Medium

- On Simplicity: "Wall Street is skeptical of simplicity." — Source: Quoteswise

- On Homemade Dividends: "Retirees can create homemade dividends by selling small portions of principal rather than chasing high-yield stocks, allowing for better diversification and tax efficiency." — Source: Fisher Investments

- On Financial Discipline: "A hallmark of a great company is financial discipline, where debt should remain less than 40% of total assets." — Source: Forbes

- On Asking Better Questions: "The first question challenges readers to examine their beliefs... highlighting that many are based on myths rather than truths." — Source: Bookey

- On The Value of Statistics: "If you get nothing else out of my book except to go to ABEbooks.com and get a copy of Huff’s book How to Lie with Statistics, my book will have been well worth your time." — Source: Seeking Alpha