Lessons from Nelson Peltz

Nelson Peltz is an activist investor and founder of Trian Partners who buys large stakes in struggling consumer brands to force operational overhauls. Instead of financial engineering, his approach relies on targeting corporate bloat, tying executive pay to actual results, and simplifying the income statement. This profile collects his operating principles from decades of proxy fights at companies like Snapple, Wendy's, P&G, and Disney.

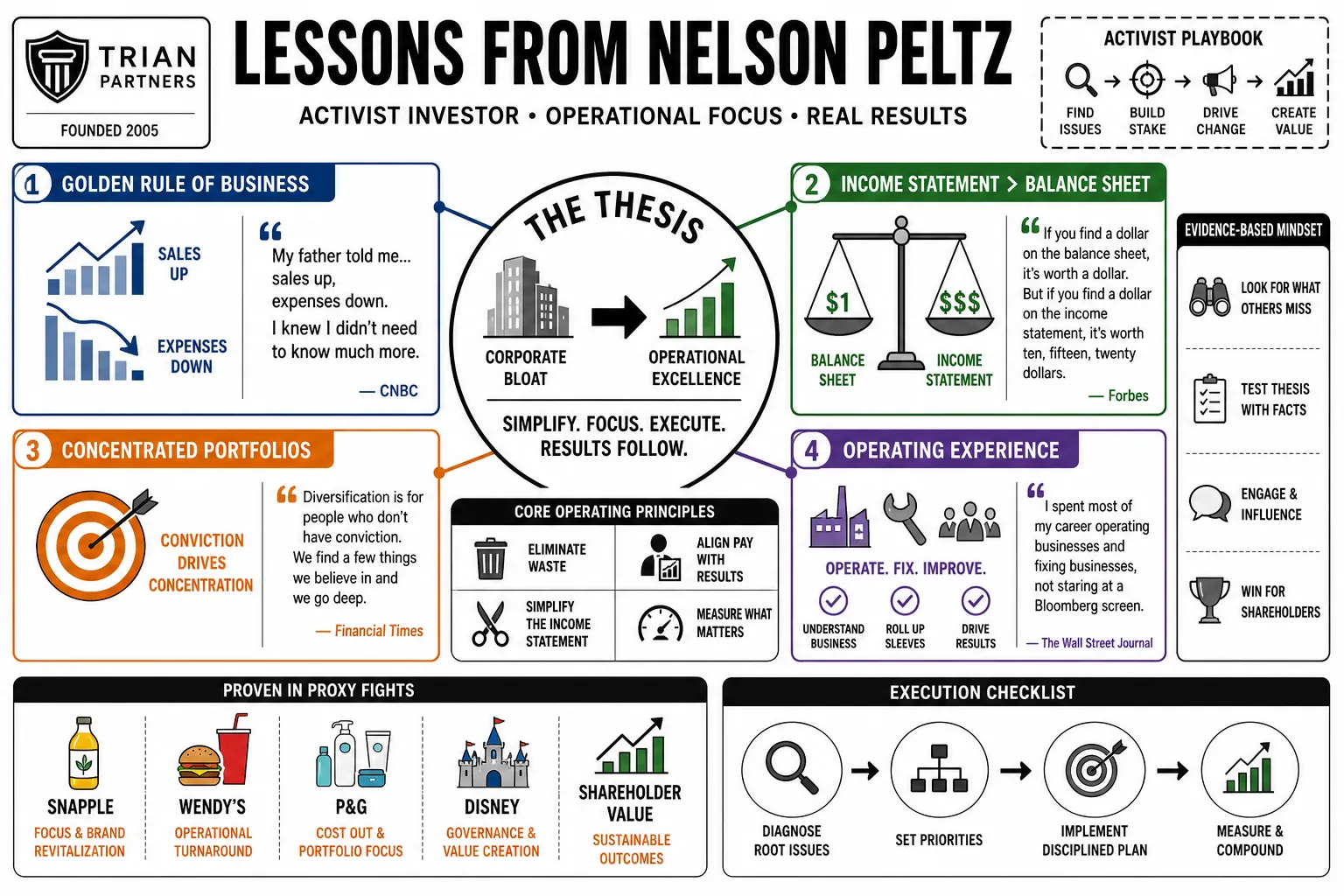

Part 1: Operational Fundamentals

- On the Golden Rule of Business: "My father told me... sales up, expenses down. I knew I didn't need to know much more." — Source: CNBC Delivering Alpha

- On the Income Statement vs. Balance Sheet: "If you find a dollar on the balance sheet, it's worth a dollar. But if you find a dollar on the income statement, it's worth ten, fifteen, twenty dollars." — Source: Forbes

- On Concentrated Portfolios: "Diversification is for people who don't have conviction. We find a few things we believe in and we go deep." — Source: Financial Times

- On Operating Experience: "I spent most of my career operating businesses and fixing businesses, not staring at a Bloomberg screen." — Source: The Wall Street Journal

- On Long-Term Holding: "We are accused of being short-term investors. But the average length of stay in an investment is five years." — Source: Trian Partners Shareholder Letter

- On Defining Value: "Value isn't created by financial engineering. It is created by better products, better margins, and dominant market share." — Source: CNBC Squawk Box

- On Capital Expenditures: "You don't just spend money because you have it. Every dollar of Capex needs to earn its keep." — Source: Business Insider

- On Organic Growth: "You cannot cut your way to greatness. Cost cutting buys you time to fix the top line, but organic sales growth is the only sustainable engine." — Source: Trian Partners White Paper

- On Corporate Complexity: "Complexity is the enemy of execution. When a business has too many layers, nobody is responsible for the customer." — Source: The Wall Street Journal

- On Asset-Light Models: "By shifting to a heavily franchised model, you reduce capital needs, de-risk the balance sheet, and let the brand operators focus on local execution." — Source: Nation's Restaurant News

Part 2: The Constructivist Approach

- On Activism vs. Constructivism: "I want to make love, not war. I want to be constructive, not destructive. I’m looking for people to embrace me." — Source: Financial Times

- On the 'Bully' Label: "What sense is being a billionaire if you're not a bully?" — Source: Business Insider

- On Management Alignment: "Our goal is to work with management, not to replace them. We don't fire CEOs, we try to help them." — Source: CNBC

- On Post-Fight Relationships: "We can fight like hell in a proxy contest, but the day after the vote, we can be fast friends because we all want the stock to go up." — Source: Forbes

- On the Bifocal Strategy: "We encourage management teams to operate as if wearing bifocals—with a watchful eye on the near-term, but always focusing on maximizing long-term value." — Source: Trian Partners

- On Identifying Targets: "We try to find a business, a good business, that is just not living up to its potential." — Source: CNBC Delivering Alpha

- On Corporate Rhetoric: "Management often asks shareholders to believe their strategy is working. We step in to separate the rhetoric from the reality." — Source: SEC Filings

- On Board Room Friction: "A little friction in the boardroom is healthy. If everyone agrees all the time, nobody is thinking critically." — Source: The Wall Street Journal

- On the Threat of Intervention: "Sometimes just the threat of a proxy fight is enough to get a stagnant board to finally take action." — Source: Bloomberg

Part 3: Corporate Governance & Board Accountability

- On Board Entrenchment: "The root cause of chronic underperformance is usually a board that lacks focus, alignment, and accountability." — Source: Trian Partners Disney White Paper

- On CEO Succession: "A board's most critical job is CEO succession. When a company fails at this repeatedly, the board has failed its essential duty." — Source: CNBC

- On Director Skin in the Game: "Directors need to own real stock, not just options granted to them. They need to feel the pain when shareholders lose." — Source: Forbes

- On Matrix Organizations: "A matrixed organization is where accountability goes to die. Only the CEO has P&L responsibility, and that is a recipe for disaster." — Source: Financial Times

- On Insular Cultures: "When a company promotes entirely from within for decades, it builds an insular culture that ignores outside innovation." — Source: Trian P&G White Paper

- On Creative Businesses: "People say you don't manage creativity like a hedge fund. But even a creative business must be held accountable to margins and capital allocation." — Source: The Wrap

- On 'Yes Men': "Too many boards are just an echo chamber for a long-tenured CEO. They rubber-stamp decisions instead of stress-testing them." — Source: Business Insider

- On the Proxy Fight Purpose: "A proxy contest isn't about ego. It's a mechanism to force a referendum on a failed corporate strategy." — Source: The Wall Street Journal

- On Splitting Chairman and CEO Roles: "When the CEO is also the Chairman, the board's ability to provide independent oversight is fundamentally compromised." — Source: Trian Partners Letters

- On Executive Compensation: "Pay must be tied to operational outperformance, not just a rising stock market. If peers are doing better, management shouldn't get a bonus." — Source: Bloomberg

Part 4: Managing Brands & Turnarounds

- On the Snapple Turnaround: "We bought Snapple losing $28 million on the EBITDA line, and when we sold it, it was making $80 million." — Source: Forbes

- On Market Position: "Being the third leading cola brand in America is sort of like being the world's tallest midget." — Source: Financial Times

- On the Heinz Strategy: "Everybody has a bottle of Heinz in their pantry. The key was how to get it out of the pantry, on the table, and turn it upside down." — Source: Shareholder Forum

- On Product Testing: "We'd make 10,000 cases in a flavor we liked and ship it. If it didn't sell well, we would never make it again." — Source: CNBC

- On Brand Innovation: "The innovation machine at large consumer companies is often broken. They rely on legacy products while small disruptors steal shelf space." — Source: Trian P&G White Paper

- On Advertising Spend: "Cutting marketing to hit a quarterly earnings number is eating your seed corn. You have to reinvest in the brand to drive the top line." — Source: The Wall Street Journal

- On Local execution: "Great consumer brands are built on the ground, store by store, distributor by distributor. You cannot manage retail entirely from a corporate tower." — Source: Nation's Restaurant News

- On Distribution Relationships: "Fixing the brand often means fixing the relationship with independent distributors. If they don't believe in the product, the customer never sees it." — Source: Bloomberg

- On Heritage Brands: "A brand with a century of heritage is a massive asset, but heritage does not excuse irrelevance in today's market." — Source: Forbes

Part 5: Capital Allocation & Strategy

- On Conglomerate Discounts: "A conglomerate structure often destroys value. It is burdened by byzantine structures and excessive holding company costs." — Source: Trian DuPont White Paper

- On Resource Conflict: "When a company houses fast-growth and slow-growth businesses, there is an inherent conflict in allocating resources that hurts both." — Source: Trian PepsiCo White Paper

- On Buying Right: "The asking price for Snapple was $300 million, we bought it for $300 million. You make your money when you buy." — Source: Financial Times

- On Dividends vs. Buybacks: "We favor returning capital to shareholders, but it must be balanced. Buying back overvalued stock is just as bad as wasting money on a bad acquisition." — Source: CNBC

- On Private Equity: "In a high-interest-rate environment, traditional private equity is falling on its face. The math doesn't work when money isn't free." — Source: CNBC Delivering Alpha

- On Bankers vs. Operators: "If you just want to add a few turns of leverage, you don’t need us. You can hire a banker. We bring operational discipline." — Source: Bloomberg

- On Corporate Overhead: "We consistently find billions in excess corporate costs at legacy companies. That is money that should be given back to the owners." — Source: Trian Partners Letters

- On Mergers and Acquisitions: "M&A should be a tool to consolidate market power or acquire necessary technology, not an excuse for empire building." — Source: The Wall Street Journal

- On Spinoffs: "Sometimes the best way to unlock value is to set a division free. It forces the spun-off entity to stand on its own two feet." — Source: Business Insider

Part 6: Leadership & Management Dynamics

- On the Ownership Mentality: "We have a simple goal: ensuring that companies function with a strong ownership mentality. Managers must act like it is their own money." — Source: Trian Partners

- On White-Collar Bloat: "We found 7,500 white-collar jobs that weren't needed. They’re not happy either because they want to be doing something... they’re hiding." — Source: CNBC

- On Defensive Management: "When management fights a reasonable strategic suggestion with tens of millions in shareholder money, they are defending their jobs, not the company." — Source: Financial Times

- On Pragmatism: "We’d rather be rich than right. If the stock goes to 100 without our plan, great. But if it doesn’t, we demand change." — Source: The Wall Street Journal

- On Decentralization: "Decision making must be pushed down to the local level. A centralized bureaucracy suffocates the operators who actually know the customer." — Source: Forbes

- On Intellectual Honesty: "We feel it is necessary to set the record straight so shareholders understand the level of management's intellectual dishonesty." — Source: Trian P&G White Paper

- On Talent Retention: "You cannot build a great company if you are losing your best mid-level operators to leaner, faster-moving competitors." — Source: Bloomberg

- On Transparency: "When a company stops breaking out the financials of a struggling division, it is a massive red flag for investors." — Source: CNBC Squawk Box

- On Arrogance: "The worst trait in a management team is the belief that they have nothing left to learn from the outside world." — Source: Business Insider

- On Speed of Execution: "Time is the enemy of a turnaround. Every month spent debating a reorganization is a month of lost market share." — Source: The Wall Street Journal

Part 7: Macroeconomics, Markets & Trends

- On Artificial Intelligence: "AI is amazing for efficiency, but we are going to hit a bump in the road as it begins displacing employees." — Source: Investing.com

- On Inflation: "Inflation exposes weak pricing power. If your product is indispensable, you can pass on costs. If it's a commodity, you get crushed." — Source: CNBC

- On Tariffs and Trade: "Tariffs are a negotiating ploy. They can be used the wrong way, but the threat of them can bring trading partners in line." — Source: CNBC Delivering Alpha

- On the Cost of Capital: "Zero-percent interest rates allowed bad companies to survive. A normalized rate environment is good for stock pickers." — Source: Bloomberg

- On Index Funds: "The rise of passive investing means a huge portion of the shareholder base is on autopilot. It makes engaged activism more vital than ever." — Source: Financial Times

- On Market Volatility: "Volatility is our friend. It creates the dislocations that allow us to build massive positions at a discount." — Source: Forbes

- On ESG and Investing: "Environmental and social governance must be aligned with shareholder returns. You cannot run a public company as a charity." — Source: The Wall Street Journal

- On Consumer Spending: "Never bet against the American consumer, but always verify exactly what they are willing to pay a premium for." — Source: CNBC Squawk Box

- On Global Supply Chains: "Geopolitics is forcing companies to realize that the cheapest supply chain is not always the most resilient one." — Source: Bloomberg

Part 8: Personal Philosophy, Risk & Winning

- On Gut Instinct: "You can do all your research, but at the end of the day, you have to listen to your stomach." — Source: Forbes

- On Retirement: "If every company is living up to its potential, we'll give the money back and I'll go to the beach. But that hasn't happened yet." — Source: Financial Times

- On Partnership: "Find partners who complement your weaknesses. Peter May and I have worked together for decades because we trust each other implicitly." — Source: The Wall Street Journal

- On Losing: "You learn nothing from a success. You learn everything when you get punched in the mouth and have to figure out why." — Source: Business Insider

- On Persistence: "If you know you are right, you do not back down just because the establishment tells you to go away." — Source: CNBC

- On Simplicity: "I don't like complex financial models. If the thesis cannot be explained on a single piece of paper, it is too complicated." — Source: Bloomberg

- On Legacy: "I want to be remembered as someone who left companies fundamentally stronger than when I found them." — Source: Forbes

- On Debt: "Debt is a tool. In the 1980s, we used high-yield bonds to build Triangle Industries, but you must always respect the leverage." — Source: Financial Times

- On the Drive to Win: "I wake up every morning terrified of losing. That fear is what keeps you sharp." — Source: The Wall Street Journal