Roelof Botha is the Managing Partner of Sequoia Capital and the former CFO of PayPal, where he guided the company through its 2002 IPO after the dot-com crash. He is widely known for his framework of "crucible moments"—the irreversible, high-stakes decisions that permanently alter a company's trajectory. This profile organizes his core lessons on managing early-stage startup chaos, evaluating long-term founder ambition, and navigating the harsh mathematical realities of venture capital.

Part 1: Crucible Moments & Navigating Survival

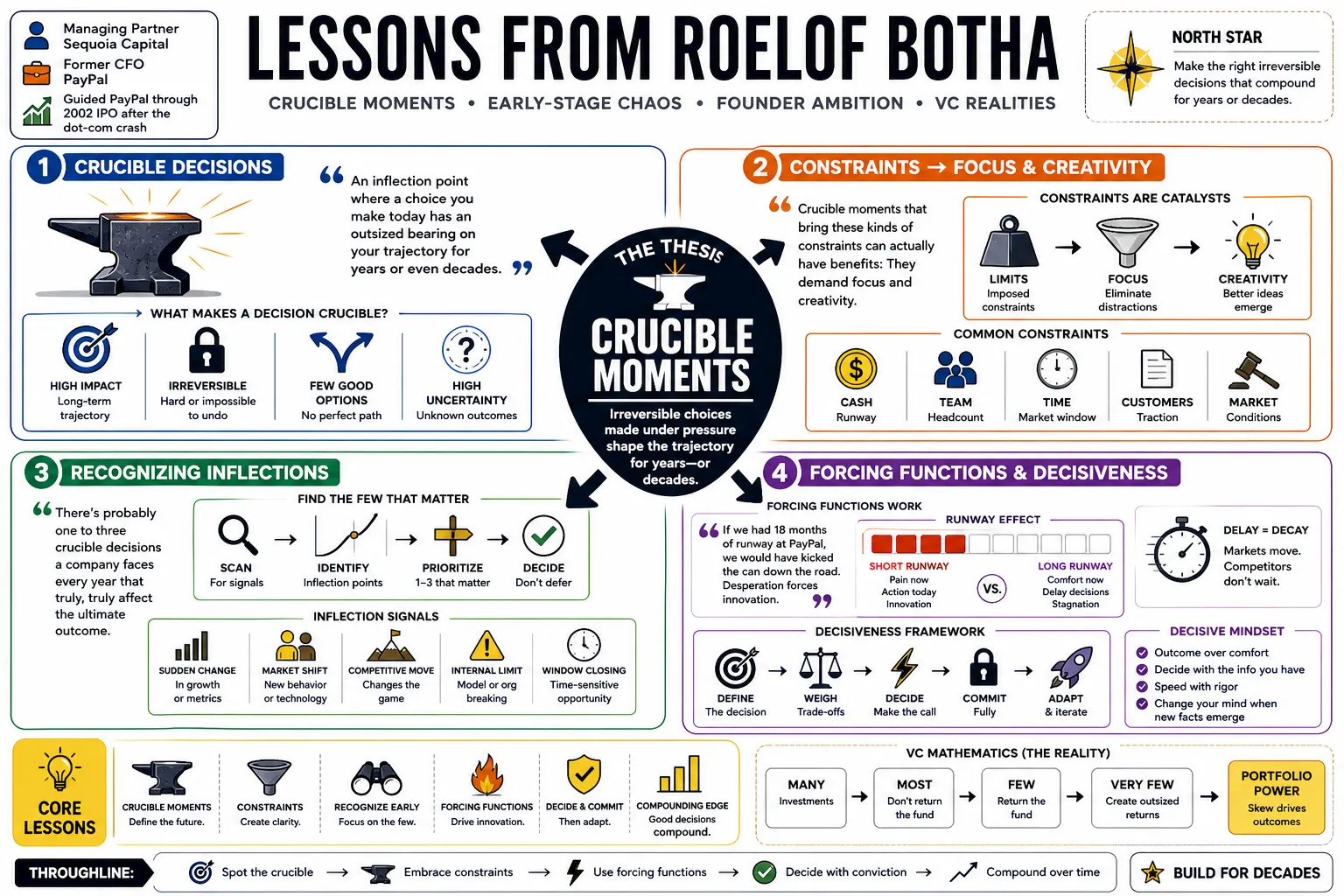

- On Crucible Decisions: "An inflection point where a choice you make today has an outsized bearing on your trajectory for years or even decades." — Source: [Crucible Moments Podcast]

- On Constraints: "Crucible moments that bring these kinds of constraints can actually have benefits: They demand focus and creativity." — Source: [Sequoia Capital]

- On Recognizing Inflections: "There’s probably one to three crucible decisions a company faces every year that truly, truly affect the ultimate outcome." — Source: [The Twenty Minute VC]

- On Forcing Functions: "If we had 18 months of runway at PayPal, we would have kicked the can down the road. Desperation forces innovation." — Source: [Invest Like the Best]

- On Decisiveness: "Instead of thinking like a consultant or a banker, you have to be a principal and decide, and live with the consequences." — Source: [The Tim Ferriss Show]

- On Early Failure Rates: "50% of the time that we made a seed or a venture investment, we failed to fully recover capital. It’s humbling." — Source: [Private Markets Insights]

- On Pre-Mortems: "Before making a major decision, imagine the company has failed to identify hidden risks, or succeeded wildly to understand requirements for scale." — Source: [Stanford View From The Top]

- On Enduring Hardship: "Those who have a why to live can bear almost any how. If you have a purpose, you can endure the crucible moments of a startup." — Source: [The Twenty Minute VC]

- On Strategic Slack: "Capital-abundant environments cause companies to develop strategic slack. Efficiency is learned during near-collapse." — Source: [ChainCatcher]

- On Taking Action: "The challenge for management is identifying those crucible moments and actively navigating them rather than letting them pass by." — Source: [The Twenty Minute VC]

Part 2: The Art of Board Leadership & Investing

- On Board Members: "A good board member should be a shock absorber for the company, because there will be shocks and people will be rattled." — Source: [The Twenty Minute VC]

- On Restraint: "Investors are meant to be shock absorbers, not amplifiers. You slow the process a little bit down and guide the leadership into a thoughtful process." — Source: [The Twenty Minute VC]

- On Socratic Leadership: "I think much more about taking a Socratic approach to being on the board. Asking questions and truly asking questions, not asking questions that are really suggestions." — Source: [The Twenty Minute VC]

- On Consensus: "Consensus ensures every investment is ours, meaning all partners are incentivized to help a founder, rather than viewing it as one individual's problem." — Source: [Sequoia Culture Memo]

- On Naivete: "You need to retain an element of naivete, a sort of childlike innocence and willingness to dream and imagine as you look to new opportunities." — Source: [The Twenty Minute VC]

- On Valuation Anchoring: "Always adhere to discounting future value rather than tracing past prices. Buy discounts to the future, not premiums to the past." — Source: [ChainCatcher]

- On Imagination: "The thing I find most often is failure of imagination on my part. I didn't think big enough about how this company could progress." — Source: [The Twenty Minute VC]

- On Patience: "It’s important to choose initial investors who are not twitchy and rushing for an exit." — Source: [AZ Quotes]

- On Relationships: "Friends come and go; enemies accumulate. Treat every founder with respect, regardless of whether you invest." — Source: [Invest Like the Best]

- On Partnering: "We don’t make deals; we partner with outlier founders to help them reach the full scale of their ambition." — Source: [Sequoia Capital]

Part 3: Founder Psychology & Ambition

- On Founder-Problem Fit: "A lot of people talk about founder-market fit; the thing I actually look for is founder-problem fit. Why are you the one who has the insight in this particular problem?" — Source: [Invest Like the Best]

- On Discontent: "If you’re not a little discontent, I don’t think you’re alive." — Source: [The Tim Ferriss Show]

- On the Founder Matrix: "The quadrant that makes the most money is the exceptional but difficult to get along with founder, as they challenge the status quo most aggressively." — Source: [The Twenty Minute VC]

- On Ambition: "One of the questions I love to ask a founder is: 'What’s the scale of your ambition? Do you dare to dream?'" — Source: [Crucible Moments Podcast]

- On Refusing Reality: "Founders are these people who don't accept the way the world is. They seek to remake it as it should be." — Source: [Stanford GSB]

- On Self-Belief: "Nobody is an authority on your potential but you. At some point, you’re going to have to raise your hand and not be timid." — Source: [Stanford View From The Top]

- On Authentic Problems: "Solve authentic, personal problems you understand viscerally." — Source: [Invest Like the Best]

- On The Second Meeting Test: "The real test is the second conversation—do I lose interest? Or does my imagination start to run off as I think about what this company can become?" — Source: [The Twenty Minute VC]

- On Operating at the Edge: "To be exceptional, operate on the edge of competence and overcome the fear of failure." — Source: [Invest Like the Best]

- On Continuous Effort: "Success is never the summit. We’re never at the top; we’ve always got to keep going." — Source: [Stanford GSB]

Part 4: Startup Metrics & Growth Economics

- On Slope vs. Intercept: "I’ll take slope over intercept any day. Rate of improvement matters more than the starting point." — Source: [Invest Like the Best]

- On Early Data: "Truly world-changing companies often do not have impressive data in their early stages. If you only apply traditional financial metrics, you are likely to miss them." — Source: [ChainCatcher]

- On Consumer Engagement: "You don't want to be the site that people should use. You want to be the site they can't stop using." — Source: [Sequoia Insights]

- On The Wedge Strategy: "Win a specific beachhead before expanding. Focus on a narrow wedge to solve one problem perfectly." — Source: [Invest Like the Best]

- On Market Timing: "Pair a unique insight with a compelling 'Why Now'. Ask if the infrastructure is finally ready for this to scale." — Source: [Sequoia Capital YouTube Memo]

- On Defensibility: "Community and ease of use create defensibility that makes a platform harder to replicate than a purely technical solution." — Source: [Sequoia Capital YouTube Memo]

- On Growth Fundamentals: "We had to get religion on cost reduction and figuring out a business model, knowing that we were months away from being profitable and on our way to being a public company." — Source: [Invest Like the Best]

- On Market Entry: "If an investor has a deep thesis and intuition for a space, moving fast and preempting a round is a fabulous recipe for success." — Source: [The Twenty Minute VC]

- On Pricing Discipline: "Throwing more money into Silicon Valley doesn’t yield more great companies; it actually dilutes talent." — Source: [Stanford View From The Top]

Part 5: Silicon Valley Realities & The Power Law

- On Venture Capital Viability: "I don't think venture is an asset class. It doesn't support the numbers. There’s too much money and too many people who want to be investors." — Source: [Private Markets Insights]

- On Return-Free Risk: "In my opinion, investing in venture is a return-free risk for most." — Source: [Business Insider]

- On The Math of VC: "You’d need 40 Figmas a year for the industry to make the returns work on current capital, which means that they don’t." — Source: [Private Markets Insights]

- On The Power Law: "We get it wrong a lot. 30–40% of early-stage investments are complete write-offs, and success comes from the power law of a few spectacular winners." — Source: [LDV Capital]

- On Performance: "We are only as good as our next investment. Nothing wilts as fast as laurels that have been rested on." — Source: [Stanford GSB]

- On Stewardship: "My title is Steward for a reason. It’s just a notch above Usher. Partners are temporary caretakers of the firm." — Source: [Stanford View From The Top]

- On Longevity: "Most top venture firms from 1990 no longer exist. To avoid the innovator's dilemma, a firm must constantly innovate and stay performance-focused." — Source: [Stanford View From The Top]

- On Cynicism: "Retain a childlike innocence. Cynicism is the enemy of great investing." — Source: [The Twenty Minute VC]

- On Overcapitalization: "A flood of capital makes it harder to achieve traditional VC returns, as it props up companies that shouldn't survive." — Source: [Business Insider]

Part 6: Career Strategy & Risk Tolerance

- On Career Horizons: "Expand the time horizon over which you’re thinking. Most people make career decisions one step at a time instead of looking at the decade arc." — Source: [Stanford GSB]

- On Taking Bets Early: "Take risks in your career. Even if a risky job doesn't work out, as long as you worked with great people, you will land on your feet." — Source: [Stanford GSB]

- On Avoiding Safety: "Avoid safe jobs. The startup world offers multiple rolls of the dice, where failure in one venture provides the skills for the next." — Source: [Stanford GSB]

- On Choosing Upside: "Bet on yourself over guaranteed payouts. Long-term potential is worth sacrificing immediate certainty." — Source: [Stanford View From The Top]

- On Creating Luck: "You have to put yourself in a position to be lucky. I try getting in front of as many opportunities as possible." — Source: [Stanford GSB]

- On Goal Setting: "Write your long-term target on every sheet of paper. Let it serve as a constant reminder of the scale of impact you want to achieve." — Source: [Recall.it]

- On Authenticity: "Ditch the polish, it's about raw authenticity." — Source: [Stanford GSB]

- On Optionality: "Focus on decisions that open doors and create options rather than close them." — Source: [Stanford View From The Top]

- On Foundational Skills: "Classes like cost accounting and strategy are directly applicable. Practical skills matter more than mere networking." — Source: [Stanford GSB]

Part 7: PayPal Lessons & Capital Efficiency

- On The Value of Desperation: "The threat of having only seven months of runway forced us to solve three critical problems in three months." — Source: [Stanford View From The Top]

- On Entrepreneurship vs Founding: "Entrepreneurship is not synonymous with being a founder. Join a high-growth company first to learn the ropes." — Source: [Stanford View From The Top]

- On High-Stress Iteration: "Brutal, high-stress environments force teams to iterate quickly and build a culture of absolute candor." — Source: [Crunchbase]

- On Knowing the Math: "As a CFO, you have to know exactly where the money is going and stop the bleeding before you can scale the operations." — Source: [Invest Like the Best]

- On Going Public: "Executing an IPO in a down market requires extreme discipline, but it separates generational companies from those dependent on hype." — Source: [Sequoia Capital]

- On Finding the Fix: "At PayPal, we realized we were losing money on every transaction. We had to invent bank transfers to lower processing costs." — Source: [Invest Like the Best]

- On Asking Questions: "Those inside the company always have more daily context. Ask questions rather than being prescriptive." — Source: [Invest Like the Best]

- On the Fixer-Upper Rule: "Nobody wants to buy a fixer-upper. Build structural soundness from the start." — Source: [Stanford GSB]

- On Team Networks: "The true value of early startup experience is the network of intense operators you build for your entire career." — Source: [Crunchbase]

Part 8: Building Enduring Companies

- On the Company as a Product: "Founders should think of their company as a product and build it and shape it with the same passion and care as the software itself." — Source: [Invest Like the Best]

- On Customer Obsession: "Be competitor-aware but customer-obsessed." — Source: [Invest Like the Best]

- On Enduring Value: "Build enduring businesses rather than those built for quick exits." — Source: [AZ Quotes]

- On Multiple Founding Moments: "Great companies must reinvent themselves. Companies have multiple founding moments." — Source: [Stanford View From The Top]

- On Continuous Reinvention: "You cannot rely on your original insight forever. You must force secondary and tertiary acts of innovation." — Source: [Stanford View From The Top]

- On the Innovator's Dilemma: "The greatest threat to a successful company is its own success. You have to maintain the paranoia of an underdog." — Source: [Invest Like the Best]

- On Tension: "Maintain tension between individualism and teamwork. It’s not either/or, it’s and. We want both." — Source: [The Tim Ferriss Show]

- On Permanent Structures: "Breaking from traditional venture cycles to create a permanent, open-ended structure allows you to hold enduring companies forever." — Source: [Marcellus Investment]

- On the Long Game: "There is no summit. There’s only the climb." — Source: [The Tim Ferriss Show]