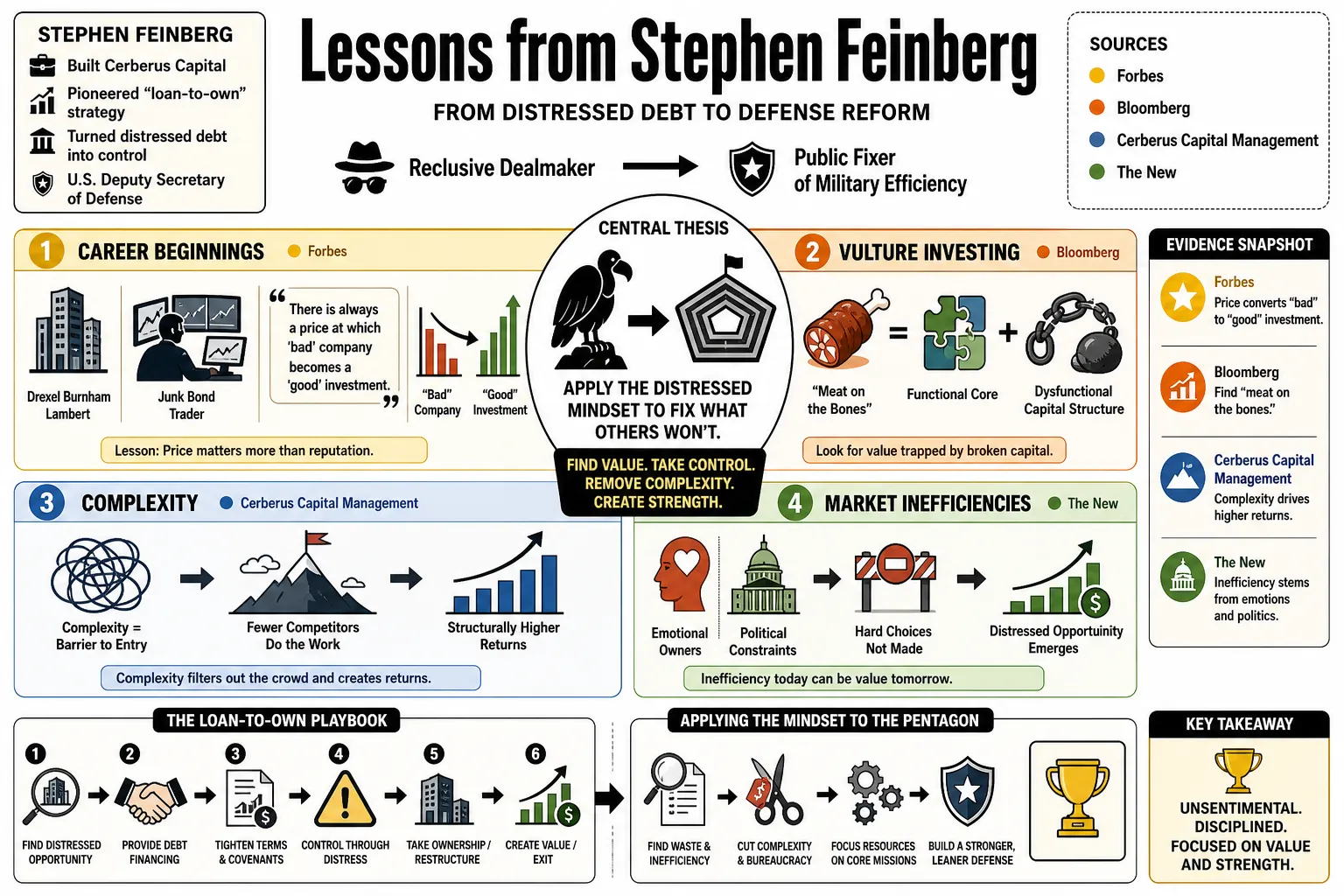

Lessons from Stephen Feinberg

Stephen Feinberg built Cerberus Capital on a "loan-to-own" strategy that turned distressed debt into control of failing companies. Now serving as U.S. Deputy Secretary of Defense, he is attempting to apply that same unsentimental logic to the Pentagon. This profile examines his move from a reclusive dealmaker to a public fixer of military efficiency.

Part 1: The Distressed Mindset

- On Career Beginnings: "I started as a trader in the junk bond market at Drexel Burnham Lambert, which taught me that there is always a price at which a 'bad' company becomes a 'good' investment." — Source: Forbes

- On Vulture Investing: Identifying "meat on the bones" means looking for companies that have a functional core but are suffocating under a dysfunctional capital structure. — Source: Bloomberg

- On Complexity: Complexity is a barrier to entry for most investors, which means the returns for those willing to do the work are structurally higher. — Source: Cerberus Capital Management

- On Market Inefficiencies: Distressed opportunities often arise because the current owners are emotionally or politically unable to make the hard choices required for survival. — Source: The New York Times

- On Identifying Value: "We thrive where others see only 'hair' on a deal—bankruptcy, massive pension liabilities, or toxic labor relations are often just solvable math problems." — Source: Reuters

- On Contrarianism: Buying when everyone else is selling requires a clinical detachment from the prevailing market sentiment. — Source: Wall Street Journal

- On the "Cerberus" Name: The three-headed dog was chosen to symbolize the firm’s guarding of investor capital with a multi-layered, aggressive approach. — Source: Business Insider

- On Early Discipline: Playing varsity tennis at Princeton taught the value of individual intensity and the reality that you cannot hide from the scoreboard. — Source: Princeton University Athletics

- On Financial Decay: Most failing companies don't need a "visionary" as much as they need a disciplined accountant with the power to act. — Source: Financial Times

Part 2: The Mechanics of Control

- On the Fulcrum Security: Successful distressed investing requires identifying the specific layer of debt that will convert to equity during a restructuring. — Source: Wall Street Prep

- On Loan-to-Own: Buying debt at a discount is a strategy to acquire the company at a fraction of its replacement cost while maintaining a legal priority over other stakeholders. — Source: Institutional Investor

- On Blocking Positions: Controlling a large enough portion of a single debt class allows an investor to veto any reorganization plan that does not favor their position. — Source: Harvard Business Review

- On Bankruptcy as a Tool: Chapter 11 should be viewed as a surgical room, not a graveyard; it is where you excise the liabilities that prevent the business from breathing. — Source: CNBC

- On Leverage: High debt loads in a buyout are not just for returns; they create a sense of urgency that forces management to prioritize cash flow every single day. — Source: The Guardian

- On Exit Timing: "We were too optimistic on the timing of the Chrysler turnaround; you cannot always predict when a macro cycle will overwhelm a micro fix." — Source: CNN Business

- On Asset Stripping Myths: The goal isn't to sell the parts, but to make the whole work well enough that someone else will pay a premium to own it later. — Source: Washington Post

- On Dividend Recaps: Extracting capital early through debt is a way to de-risk the initial investment, even if it leaves the company with a tighter margin for error. — Source: Forbes

- On Risk Hedging: In distressed debt, your downside should be protected by the hard assets of the company, not just its projected future earnings. — Source: Investopedia

Part 3: The Operator-Investor Model

- On COAC: The Cerberus Operations and Advisory Company (COAC) ensures that we are never just "passive" owners of a problem. — Source: Cerberus Capital Management

- On Interim Leadership: If the existing management cannot meet the new metrics within ninety days, we have a roster of fifty former CEOs ready to step in. — Source: Fortune

- On Information Commodities: "The most important commodity in this business is information, and we hire former government leaders because they provide the best strategic vision." — Source: Bloomberg

- On Operational Audits: Every portfolio company must undergo a line-by-line review of costs that is independent of the management's own reporting. — Source: Reuters

- On Executive Overpayment: "In general, I think that all of us are way overpaid in this business. It is almost embarrassing... General partners make absurd amounts of money." — Source: Fortune

- On Managing from the Bottom: You cannot fix a logistics company from a boardroom; you have to send an operations team to the loading docks. — Source: Wall Street Journal

- On Accountability: We don't use consultants; we use owners. When a COAC executive goes into a company, their bonus is tied to the same exit as the fund. — Source: Cerberus Official Site

- On Functional Expertise: Generalist MBAs are less valuable in a turnaround than a supply chain veteran who has lived through three recessions. — Source: New York Post

- On Stability: Our primary goal is stability; a boring, profitable company is far more valuable than a "visionary" one that loses money. — Source: The New York Times

- On Due Diligence: The due diligence for a distressed deal should look like a forensic audit of every single contract the company has signed. — Source: Bloomberg Law

Part 4: The Strategic Value of Secrecy

- On Radical Privacy: "We try to hide religiously. If anyone at Cerberus has his picture in the paper... we will do more than fire that person. We will kill him." — Source: Rolling Stone

- On Media Avoidance: Public attention is a distraction that serves the ego of the investor, not the performance of the fund. — Source: Business Insider

- On Competitive Advantage: The less the market knows about what you are buying, the less likely they are to bid against you in a bankruptcy auction. — Source: The New Yorker

- On Corporate Neutrality: We are investors, not statesmen; it is not our role to take positions on social debates unless they affect the math of the deal. — Source: New York Times

- On Talent Poaching: Hiring the "unhireable" or the "unloved" from other firms is a cheap way to acquire massive amounts of institutional knowledge. — Source: Reuters

- On Working in the Shadows: Most of the best deals never make the front page because they are negotiated in private before a public auction can even begin. — Source: Financial Times

- On Discretion: If a partner cannot keep a secret about a deal, they cannot be trusted with the capital required to execute that deal. — Source: Business Insider

- On Reputation: We are willing to take the reputational hit of being "vultures" if it means we can buy assets at a 70% discount. — Source: Bloomberg

- On Investor Letters: We write letters to our investors to explain the math, not to provide fodder for journalists. — Source: Wall Street Journal

Part 5: Pragmatism and the "No-Heroics" Rule

- On Avoiding Heroism: "We do not need to be heroes to earn a good return on the investment in Chrysler... we just need to make it slightly better than it was." — Source: New Mexico State Investment Council

- On Realistic Goals: You don't have to "save" an industry; you just have to fix the specific leaks in one company’s bucket. — Source: Reuters

- On Sunk Costs: Knowing when to walk away from a deal—even after spending millions on diligence—is the difference between a partner and a gambler. — Source: New York Times

- On Relative Performance: In a downturn, you don't need to grow; you just need to shrink slower and more efficiently than your competitors. — Source: Bloomberg

- On Pension Obligations: Unfunded liabilities are not "vague" risks; they are senior debt that must be renegotiated for the company to ever be profitable again. — Source: Financial Times

- On Industrial Icons: Investing in a company like Chrysler is an act of "pragmatic patriotism"—if we can fix it, we save an American icon and make a fortune. — Source: ABC News

- On Management Change: "Maybe what we should have done [with Chrysler] was not bought it... we were too optimistic about the speed of cultural change." — Source: Reuters

- On Complexity Fatigue: Some deals are too "hairy" even for us; if the legal complexity outweighs the operational upside, we pass. — Source: Wall Street Journal

- On Capital Preservation: The first rule of distressed investing is not to lose the principal; the second is to remember that every asset has a floor value. — Source: Cerberus Capital Management

Part 6: Operational Efficiency and Fat Trimming

- On the Productivity Engine: Our "productivity engine" at Albertsons isn't about making people work harder; it's about using data to stop them from doing useless work. — Source: Supermarket News

- On Warehouse Automation: Target 30% automation of distribution volume to remove the human error that leads to supply chain spoilage. — Source: Food Logistics

- On Real Estate Value: A grocery store is often a real estate play disguised as a retail business; the land underneath is the true margin of safety. — Source: Bloomberg

- On Sale-Leasebacks: Turning a building you own into a lease you pay is a way to pull your cash out today, provided you can grow the core business faster than the rent. — Source: Equity CRE

- On Regional Decentralization: Organize by regions so that local "banners" can keep their brand loyalty while the back-end stays ruthlessly centralized. — Source: Albertsons Companies

- On Divestitures: "Setting up" a smaller competitor by selling them your worst-performing stores during a merger is a legitimate way to satisfy regulators. — Source: Haggen v. Albertsons Filing

- On Debt as Discipline: Carrying $7 billion in debt forces a company to find every penny of waste in the supply chain to make the interest payments. — Source: Reuters

- On Data Analytics: Use AI to personalize rewards for forty million members; it’s easier to sell more to an existing customer than to find a new one. — Source: Business Chief

- On Vision AI: Reducing "shrink" (theft) in retail is not a security problem; it’s an inventory accuracy problem that machines solve better than guards. — Source: Built In

- On Micro-Fulfillment: Fulfillment should happen inside the store, not in a massive warehouse five miles away; the "last mile" is the only mile that matters. — Source: Grocery Dive

Part 7: Sovereignty and National Security

- On Sovereign Assets: There are certain businesses, like subsea fiber cables, that are so critical to national security they should never be allowed to fail. — Source: SubCom

- On Supply Chain Resilience: "Our supply chain is definitely weak... a big part of strengthening it is working more closely with private industry." — Source: Senate Armed Services Committee

- On Defense Tech: We launched Cerberus Ventures because the government needs "hard tech"—hypersonics and autonomous systems—not just software. — Source: Responsible Statecraft

- On Building the "Easy Button": Private firms should build products that solve mission-critical problems instead of trying to force commercial tech into military use. — Source: Defense News

- On Domestic Manufacturing: Moving manufacturing away from China isn't just about costs; it's about "trusted" domestic partners who won't turn the lights off. — Source: Bloomberg

- On Global Competition: "China is the first nation we've ever competed with that has both a great economy and a great military... they have unlimited funding." — Source: Department of Defense

- On Hypersonics: The U.S. is underinvested in hypersonics, and the only way to catch up is to treat it like a private-sector "war room" project. — Source: Reuters

- On National Security Risks: "Data hoarding is now a national security risk; the government must become the final arbiter of data access for AI." — Source: War.gov

- On Private Capital in Defense: We need to embrace the role of private capital to accelerate capital formation in areas where the government is too slow. — Source: Defense Scoop

- On Sovereign Ownership: When a critical asset like SubCom is owned by a private equity firm with a "patriotic" mandate, the government gets a better partner. — Source: Washington Post

Part 8: Reforming the Military-Industrial Complex

- On the Pentagon Audit: "We're going to identify where the costs are... and then develop a plan to fix them, line by line, program by program." — Source: Senate Armed Services Committee

- On the "War Room" Approach: The deputy secretary’s job is to go line-by-line through the budget, not to hand it off to a general. — Source: Defense One

- On Legacy Systems: The current system rewards large defense firms for maintaining old technology rather than those that are most innovative. — Source: Reuters

- On "Gold-Plated" Requirements: "Loosen up the requirements. Make it more based on mission... Less gold-plated, quicker, more nimble." — Source: National War College Address

- On Program Rigidity: We need to stop changing the requirements once we set them; that is how a $100 million project becomes a $1 billion project. — Source: Defense Scoop

- On Mission Speed: In a war for tech dominance, being 80% correct today is better than being 100% correct in five years. — Source: Breaking Defense

- On Industrial-Military Fusion: China’s private sector is fully committed to their military; we must make our private sector a better partner for our own. — Source: Senate Armed Services Committee

- On High Production Rates: "I want to see production. I want to see a high rate of production... we need to move from prototypes to platforms." — Source: Munitions Acceleration Council Directive 2026

- On the "Golden Dome": Developing a missile defense shield is not just a technology project; it is an enterprise-level operational challenge. — Source: White House Press Release