Lessons from Bill Miller

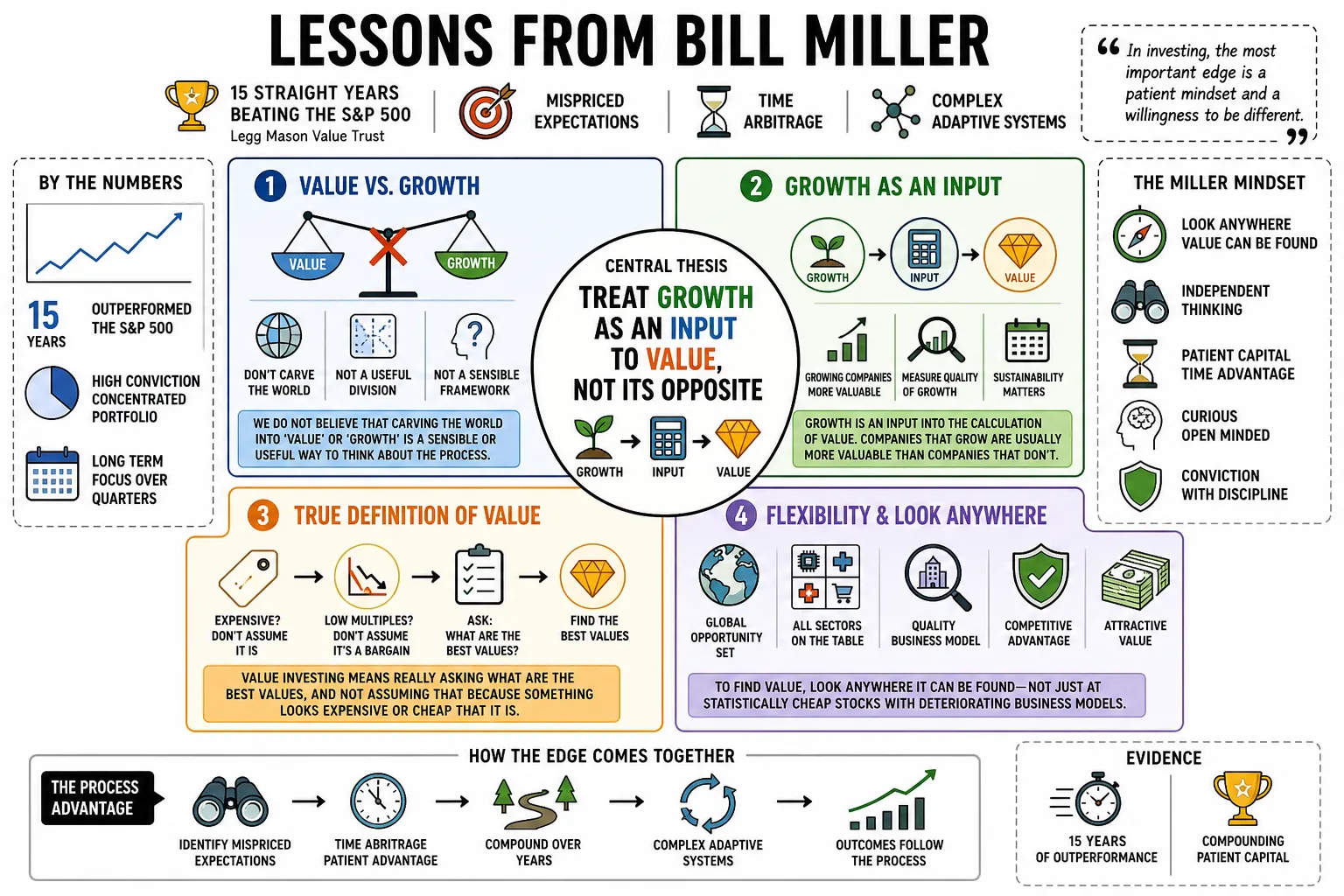

Bill Miller beat the S&P 500 for 15 straight years while managing the Legg Mason Value Trust. By treating growth as an input to value rather than its opposite, he bought technology stocks that traditional value investors avoided. This collection covers his approach to mispriced expectations, time arbitrage, and complex adaptive systems.

Part 1: Redefining Value and Growth

- On Value vs. Growth: "We do not believe that carving the world into 'value' or 'growth' is a sensible or useful way to think about the investment process." — Source: [Novel Investor]

- On the True Definition of Value: "Value investing means really asking what are the best values, and not assuming that because something looks expensive that it is, or assuming that because a stock is down in price and trades at low multiples that it is a bargain." — Source: [Macro Ops]

- On Growth as an Input: "Growth is an input into the calculation of value. Companies that grow are usually more valuable than companies that don't." — Source: [LiveMint]

- On Flexibility: To find value, an investor must look anywhere it can be found, rather than restricting themselves to statistically cheap companies with deteriorating business models. — Source: [Morningstar]

- On Traditional Metrics: "You will not find value defined in terms of low P/E or low price–to–cash flow in the finance literature." — Source: [SFBW Magazine]

- On Valuation Anomalies: Companies that look expensive on current earnings can actually be the cheapest assets in the market if their long-term economic models dictate massive future cash flows. — Source: [Business Insider]

- On the Evolution of Value: The strategy of buying strictly low price-to-book or low price-to-earnings stocks was suited for an industrial economy, but it fails to capture the intrinsic value of modern, capital-light businesses. — Source: [The Motley Fool]

- On Avoiding Dogma: Pragmatism in investing means focusing on what works and changing your mind when the facts change, rather than adhering strictly to traditional value principles. — Source: [Jason Zweig]

- On Value Traps: A stock that trades at a low multiple but is seeing its business fundamentals permanently erode is not a bargain; it is a value trap. — Source: [Economic Times]

- On Recognizing Bargains: "Bargain prices do not occur when consensus is cheery, the news is good, and investors are optimistic." — Source: [Novel Investor]

Part 2: Market Psychology and Contrarianism

- On Great Opportunities: "All of the great investing periods begin when things are terrible and end when they are wonderful." — Source: [Novel Investor]

- On Low Expectations: "The best investments are those with the worst previous returns, where expectations are low, demand is down, and prospects appear at best highly uncertain." — Source: [Novel Investor]

- On Public Information: "If it's in the papers, it's in the price." — Source: [Novel Investor]

- On Constant Worry: "When I am asked what I worry about in the market, the answer is usually nothing because everyone else in the market seems to spend an inordinate amount of time worrying." — Source: [NetFigo]

- On Going Against the Crowd: The only way to achieve superior returns is to hold a variant perception from the market consensus and be proven right over time. — Source: [Jason Zweig]

- On Pricing Disasters: Look for situations where the market has priced in a catastrophe that is highly unlikely to actually materialize. — Source: [Macro Ops]

- On the Role of the Fed: Investors spend too much time trying to guess short-term interest rate movements instead of focusing on the underlying quality of the businesses they own. — Source: [Seeking Alpha]

- On Psychological Agnosticism: Being volatility agnostic is a structural advantage, as it prevents emotional reactions to normal market fluctuations. — Source: [The Big Picture]

- On Consensus Thinking: It is mathematically impossible to outperform the market if your portfolio exactly mimics the market's consensus views. — Source: [ValueWalk]

- On Adapting to Panic: The best time to add to a position is when the market is indiscriminately selling off an asset despite its intrinsic value remaining intact. — Source: [Patient Capital Management]

Part 3: Time Arbitrage and Horizon

- On Wealth Creation: "Time, not timing, is key to building wealth in the stock market." — Source: [Gracious Quotes]

- On Structural Advantage: "If you can think in terms of three to five years, you already have a structural advantage over most of the market." — Source: [NetFigo]

- On Exploiting Short-Termism: "Time arbitrage just means exploiting the fact that most investors... tend to have very short-term time horizons." — Source: [Gracious Quotes]

- On Discounting the Future: "The most important question in markets is always: what is discounted?" — Source: [LiveMint]

- On Holding Periods: Patience is an active strategy; holding a position for five years or more allows the compounding mechanism of a strong business to outpace short-term noise. — Source: [Business Insider]

- On Reacting to News: The majority of daily market news is irrelevant to the five-year trajectory of a high-quality company's free cash flow. — Source: [Morningstar]

- On the Cost of Trading: Frequent trading not only incurs taxes and fees but also disrupts the process of long-term capital compounding. — Source: [The Motley Fool]

- On Assessing Long-Term Value: While most participants focus on the next two quarters of earnings, predicting a company's cash generation over the next decade yields a far more accurate assessment of value. — Source: [Macro Ops]

- On Enduring the Streak: The famous 15-year streak of beating the S&P 500 was achieved not by trading in and out of the market, but by holding core positions through extreme volatility. — Source: [Jason Zweig]

Part 4: Risk, Volatility, and Portfolio Management

- On Real vs. Perceived Risk: "The perception of risk is not the same thing as risk." — Source: [Novel Investor]

- On the True Definition of Risk: "Risk is the probability of a permanent loss of capital." — Source: [NetFigo]

- On Market Myopia: "The problem is that real risk and perceived risk are two different things... people perceive risk to be high when prices are low and they perceive risk to be low when prices are high." — Source: [Economic Times]

- On Price Declines: "A stock that goes down 50% is only risky if the business is impaired." — Source: [NetFigo]

- On Defining Skill: "I'd define skill as actually just surviving in markets over long periods of time without blowing yourself up." — Source: [Novel Investor]

- On Factor Diversification: True diversification comes from owning assets driven by different fundamental factors, not just buying different companies in the same cyclical industry. — Source: [Hedge Fund Alpha]

- On Averaging Down: Buying more shares as a stock price falls is a logical mechanism for lowering average cost, but only if the initial thesis regarding intrinsic value remains completely valid. — Source: [Patient Capital Management]

- On Position Sizing: Conviction should dictate position sizing; when a rare, asymmetric opportunity presents itself, it warrants an outsized allocation in the portfolio. — Source: [The Investors Podcast]

- On Accepting Losses: Experiencing deep drawdowns is an inevitable cost of outperforming the market over long periods. — Source: [The Big Picture]

Part 5: Capital Allocation and Free Cash Flow

- On the Core Metric: "Empirically, free cash flow yield is the most useful metric." — Source: [SFBW Magazine]

- On Present Value: "The value of any investment is the present value of future free cash flows, so that is ultimately of the most importance to us." — Source: [Fox Business]

- On Assessing Intrinsic Value: "We try to understand the intrinsic value of any business, which is the present value of the future free cash flows." — Source: [Macro Ops]

- On the Cost of Capital: "It's important to note that growth does not always create value. A company can grow, but if it doesn't earn above the cost of capital, that growth destroys value." — Source: [SFBW Magazine]

- On Expected Returns: "If a company is earning above its cost of capital, free cash flow yield plus growth is a good rough proxy for expected annual return." — Source: [Macro Ops]

- On Management's Job: "The best management teams make rational decisions based upon evidence, exhibit independent thinking, and allocate capital with an objective of earning returns above the cost of capital." — Source: [SFBW Magazine]

- On Reinvestment: "If a company can invest in its business and earn returns in excess of the cost of capital, it should usually do that." — Source: [SFBW Magazine]

- On Returning Cash: "If a company returns cash to shareholders in the form of dividends, that capital earns the market return." — Source: [Fox Business]

- On Share Buybacks: "If a company buys back stock, the return depends on whether the stock is under-, over- or fairly valued." — Source: [Fox Business]

- On Accounting vs. Reality: "GAAP earnings are not the same as value creation. There's a reason they're called 'generally accepted accounting principles' and not 'divinely inspired accounting principles.'" — Source: [The Investors Podcast]

Part 6: Complex Adaptive Systems and Philosophy

- On Science and Markets: "The Santa Fe Institute's research focus is on complex adaptive systems such as the stock market, the economy, cultures, the immune system, evolution, and so on." — Source: [Miller Value]

- On Market Imbalances: "Complex adaptive systems such as markets and economies are characterized by imbalances. They are non-linear, non-equilibrium systems; the imbalances are a reflection of the systems' adaptation to change." — Source: [Novel Investor]

- On the Value of Philosophy: "Philosophy involves critical thinking and reasoning about highly complex issues. At its best it is rigorous and analytical. These skills are exactly what are required to think through and understand capital markets and the analysis of businesses." — Source: [Jason Zweig]

- On Multidisciplinary Thinking: "Investing is an idea business... Our involvement [with SFI] gives us the opportunity to sit down with Nobel Prize winners in physics and economics, and with historians, biologists, and computer scientists to get a broad look at the issues on which they are working." — Source: [Fox Business]

- On Shifting Perspectives: "Once you learn about markets as a complex adaptive system and appreciate its implications, I find it difficult to go back to a more traditional point of view." — Source: [SFI Press]

- On Wittgenstein's Influence: "When we think about the future of the world, we always have in mind its being where it would be if it continued to move as we see it moving now..." — Source: [Patient Capital Management]

- On Finding an Edge: "The only way to arrive at a different answer from everybody else is to organize the data in different ways, or bring to the analytic process things that are not typically present." — Source: [Jason Zweig]

- On Activity at the Margin: "All important activity in complex adaptive systems begins at the margin." — Source: [Novel Investor]

- On Evolution of Capital: Viewing markets biologically means recognizing that businesses must constantly adapt to survive, which makes static financial models unreliable. — Source: [The Big Picture]

Part 7: Amazon, Technology, and New Business Models

- On IPOs: "When people say, 'What's the best investment decision you ever made?' Buying Amazon in the IPO." — Source: [Business Insider]

- On Selling Great Companies: "What's the worst [decision] ever? Selling a share of Amazon." — Source: [Business Insider]

- On Hidden Value: "AWS' value alone basically justifies Amazon's current market cap, meaning investors get its other businesses like e-commerce and logistics for free." — Source: [The Motley Fool]

- On Sum-of-the-Parts: "If you look at Amazon Web Services, and you look at the advertising business alone... you get almost the entire value of Amazon in those two businesses alone." — Source: [Gracious Quotes]

- On Holding Through Panics: Despite a massive drawdown during the dot-com bust, maintaining conviction in Amazon's structural dominance was the key to realizing its eventual return. — Source: [Validea]

- On Obvious Winners: Amazon became "one of the easiest names in the market" once its free cash flow engine and competitive moat became undeniable. — Source: [LiveMint]

- On Concentration: "I am likely the largest individual shareholder of Amazon whose last name isn't Bezos." — Source: [Validea]

- On Letting Winners Run: "I still think Amazon is a double in three years, so why would I sell?" — Source: [Business Insider]

- On Capital-Light Growth: Traditional valuation methods failed to capture the potential of technology platforms because they fundamentally misunderstood the scalability of capital-light software models. — Source: [The Investors Podcast]

Part 8: Bitcoin and the Future of Money

- On Asymmetric Asymmetry: "I could make 100x off my money, I could make 1,000x maybe more than that. I can only lose 100 percent." — Source: [Forbes]

- On Price Discovery: "Bitcoin is a lot less risky at $43,000 than it was at $300. It's now established, huge amounts of venture-capital money have gone into it, and all the big banks are getting involved." — Source: [Business Insider]

- On Geopolitical Insurance: "Bitcoin is insurance against financial catastrophe, as we see in Lebanon or in Afghanistan and many of these other countries." — Source: [Gracious Quotes]

- On Digital Scarcity: "I think of bitcoin as digital gold. The key is the demand for this particular type of protection against financial catastrophe." — Source: [Business Insider]

- On Inelastic Supply: "It's the only economic entity where the supply is unaffected by the demand or the price. Currencies, for sure, but even gold—there's a certain amount of gold that we produce every year." — Source: [Forbes]

- On Absolute Conviction: "I'm willing to go over the waterfall with this one too." — Source: [Validea]

- On Portfolio Allocation: "Every portfolio manager should have some Bitcoin. The asymmetry is remarkable — you could lose 100% of a small position, or you could make ten times your money." — Source: [NetFigo]

- On Institutional Adoption: As more venture capital and institutional money flows into the digital asset space, the foundational risk of holding Bitcoin drops significantly compared to its early days. — Source: [Business Insider]

- On Fiat Currency Debasement: Holding a decentralized, supply-capped asset is a rational response to the historical reality that governments consistently debase their fiat currencies to manage debt. — Source: [Macro Ops]