Lessons from Carl Icahn

Carl Icahn built his fortune by buying stakes in undervalued companies and forcing their management to change course. Instead of passively waiting for a turnaround, he uses voting power to pressure boards into offloading assets, firing executives, and buying back shares. His approach reduces corporate activism to its bare mechanics: extracting immediate value, punishing complacent leadership, and winning hostile negotiations.

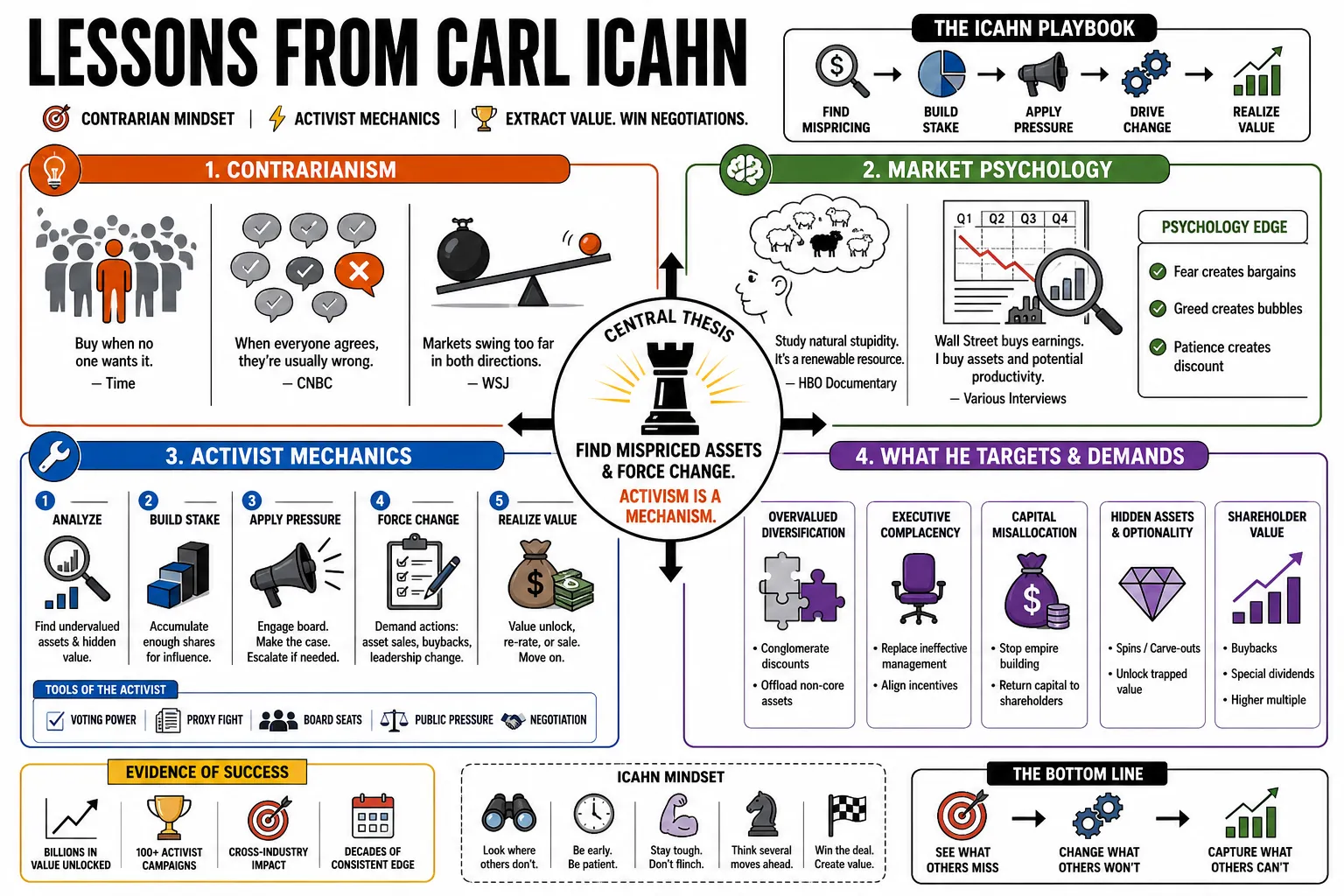

Part 1: Contrarianism and Market Psychology

- On Contrarianism: "My investment philosophy, generally, with exceptions, is to buy something when no one wants it." — Source: Time

- On Market Consensus: "When most investors, including the pros, all agree on something, they're usually wrong." — Source: CNBC

- On Price Dislocations: "A lot of times, events are overblown—overblown on the good side, overblown on the bad side." — Source: The Wall Street Journal

- On Natural Stupidity: "Some people get rich studying artificial intelligence. Me, I make money studying natural stupidity." — Source: HBO Documentary

- On Earnings vs. Assets: "Wall Street analysts look for quarterly earnings performance. I buy assets and potential productivity. Wall Street buys earnings, so they miss a lot of things that I see." — Source: Forbes

- On Public Perception: "You have to buy things where the rest of the world is looking at you and thinking you’re a little bit crazy." — Source: Bloomberg

- On Institutional Blindspots: "When nobody wants something, that creates an opportunity." — Source: Business Insider

- On Emotional Discipline: "After '62, the market broke. Terrible. I was wiped out... After that, I never played the market again in the same impulsive way." — Source: The New York Times

- On Betting Big: "When you believe in something, you have to be willing to bet the ranch on it." — Source: Financial Times

- On Recognizing Opportunities: "You learn to look for the things that other people are ignoring." — Source: Harvard Business Review

Part 2: Corporate Governance and Board Incompetence

- On Board Bureaucracy: "I don't have to watch Saturday Night Live anymore; I just go to the board meetings." — Source: CNBC

- On Corporate Democracy: "We have bloated bureaucracies in Corporate America. The root of the problem is the absence of real corporate democracy." — Source: SEC Filing

- On Social Dynamics: "Boards don't like tough, abrasive guys. They prefer people who won't rock the boat." — Source: The Wall Street Journal

- On Lack of Accountability: "Companies are the backbone of our society, and many are terribly managed and there’s no accountability." — Source: Bloomberg

- On Board Compensation: "None of the above has caused the board to hesitate in paying themselves $10,000 per week to do nothing." — Source: SEC Filing

- On Rubber Stamping: "The board is often just a rubber stamp for the CEO, operating more like a country club than a governing body." — Source: Forbes

- On Director Skin in the Game: "Most board members have no real stake in the companies they oversee, which explains why they tolerate mediocrity." — Source: Icahn Enterprises

- On Entrenchment Mechanisms: "Poison pills are designed to protect bad managers and entrench boards, not to protect shareholders." — Source: SEC Filing

- On Institutional Laziness: "The index funds and large mutual funds are completely failing in their duty to police these underperforming boards." — Source: Financial Times

Part 3: The CEO Sickness

- On Executive Importance: "The CEO is, by far, the most important decision for a company. The company is going to rise and fall with the CEO." — Source: CNBC

- On Unearned Wealth: "CEOs are paid for doing a terrible job. If the system wasn't so messed up, guys like me wouldn't make this kind of money." — Source: HBO Documentary

- On Executive Survival: "Too often it's not the most creative guys or the smartest. Instead, it's the ones who are best at playing politics and soft-soaping their bosses." — Source: Business Insider

- On Willful Blindness: "How can shareholder value be discussed when the CEO seems to be completely asleep or, even worse, either naive or willfully blind?" — Source: SEC Filing

- On Necessary Replacements: "The current board has failed to bring in a talented and experienced CEO to replace the incumbent and stop the exodus of talent." — Source: SEC Filing

- On the Imperial CEO: "In many of these companies, the CEO rules the board like a dictatorship, dictating terms to the very people supposed to oversee him." — Source: The Wall Street Journal

- On Corporate Perks: "Executives use corporate jets and treat the company treasury like a personal piggy bank while shareholders bleed." — Source: Time

- On Systemic Mediocrity: "The corporate system actively selects for executives who avoid rocking the boat rather than those who innovate." — Source: Forbes

- On the Activist's Role: "If management teams actually did their jobs and held themselves accountable, the activist model wouldn't need to exist." — Source: Bloomberg

Part 4: Activist Strategy and Hostile Takeovers

- On Takeover Preparedness: "In takeovers, the metaphor is war. The secret is reserves. You must have reserves stretched way out ahead." — Source: TradeBrains

- On Leverage Capacity: "You have to know that you could buy the company and not be stretched." — Source: Forbes

- On Taking Control: "Don't go in and tell somebody else how to run their business. Buy it and run it yourself." — Source: AZQuotes

- On Proxy Fights: "Sometimes you have to bypass the board entirely and take the argument directly to the shareholders." — Source: SEC Filing

- On the "Icahn Lift": "The market prices in the end of bad management the moment a credible activist takes a meaningful stake." — Source: Financial Times

- On Agitation: "You have to be willing to be the bad guy and face public criticism if you want to unlock trapped value." — Source: The Wall Street Journal

- On Media Pressure: "Public letters put necessary pressure on entrenched boards who would otherwise ignore private requests for change." — Source: Bloomberg

- On Corporate Campaigns: "Treat proxy battles exactly like political campaigns; it is about winning votes and proving the incumbent has failed." — Source: The New York Times

- On Forcing Action: "Activism is about forcing an event that realizes value, not passively hoping the stock price goes up." — Source: CNBC

Part 5: Value Extraction and Capital Allocation

- On Cash Hoarding: "Cash sitting idle on a balance sheet is a waste of resources that should be returned to the owners." — Source: SEC Filing

- On Share Buybacks: "The more shares purchased now, the more each remaining shareholder will benefit from that earnings growth." — Source: SEC Filing

- On Spin-offs: "Separating fast-growing divisions from stagnant legacy businesses immediately unlocks trapped value." — Source: SEC Filing

- On Core Competency: "Stop funding vanity projects and return that capital to the shareholders who own the company." — Source: SEC Filing

- On Undervalued Pipelines: "Markets often fail to price in future dominance in new categories, creating massive valuation disconnects." — Source: SEC Filing

- On Dividend Policies: "Excess cash belongs to the owners of the business, not to the managers who want to build empires." — Source: CNBC

- On Corporate Bloat: "Cutting the bureaucracy and redundant layers of management immediately and permanently improves the bottom line." — Source: Forbes

- On Asset Sales: "Sell off non-core real estate and side businesses to fund the operations that actually generate returns." — Source: The Wall Street Journal

- On Industry Consolidation: "Mature industries must consolidate to eliminate redundant overhead and maintain pricing power." — Source: Bloomberg

Part 6: Negotiation and Leverage

- On Getting What You Want: "In business and in life, you don't get what you deserve, you get what you negotiate." — Source: AZQuotes

- On Timing: "In life and business, there are two cardinal sins. The first is to act precipitously without thought and the second is to not act at all." — Source: Business Insider

- On Finding the Weak Point: "Every management team has a pressure point; successful negotiation requires finding it and pressing it." — Source: Harvard Business Review

- On Settlements: "Always leave a way out for the board to save face if they are willing to concede to your terms." — Source: CNBC

- On Litigation: "Lawsuits are not just legal maneuvers; they are another tactical tool in the broader negotiation process." — Source: The Wall Street Journal

- On Patience in Deals: "The moment you show you are desperate to close a transaction, you have surrendered your leverage." — Source: Forbes

- On Confrontation: "You cannot be afraid of a brutal public fight if the underlying math of the deal is on your side." — Source: Bloomberg

- On Holding Out: "The first offer placed on the table by an entrenched board is rarely their best offer." — Source: Financial Times

- On Reading People: "Effective negotiation is largely about understanding the other side's fears and addressing them." — Source: The New York Times

- On Bluffing: "Never make a threat you aren't fully capitalized and prepared to execute immediately." — Source: HBO Documentary

Part 7: Risk, Hubris, and Survival

- On Overconfidence: "Don't confuse luck with skill when judging others, and especially when judging yourself." — Source: AZQuotes

- On Making Mistakes: "The worst mistake you can make in life is to be afraid to make mistakes." — Source: Bookey

- On Market Cycles: "Markets will always correct hubris eventually; you pay a steep price for believing you are smarter than the market." — Source: CNBC

- On Hedging: "Always protect your downside against a macro crisis, even when your individual stock picks are sound." — Source: The Wall Street Journal

- On Dangerous Debt: "Leverage is incredibly dangerous if you do not have absolute control over the underlying cash flow." — Source: Bloomberg

- On Longevity: "Capital preservation is the only mechanism that allows you to survive a downturn and fight another day." — Source: Forbes

- On Adapting: "You have to willingly change your tactics as the regulatory environment and market structure evolve." — Source: Financial Times

- On Recognizing Defeat: "Cut your losses immediately when the facts prove your original investment thesis was wrong." — Source: The New York Times

- On Institutional Memory: "Wall Street consistently forgets the painful lessons of the last crash, which is why bubbles always return." — Source: CNBC

Part 8: Wealth, Drive, and The Game

- On Making Money: "I'm no Robin Hood, I enjoy making the money." — Source: AZQuotes

- On the Thrill of the Hunt: "The money is just a goal. It's like the explorers... I think the actual finding and doing is much more exciting than having it." — Source: Business Insider

- On Friendship on Wall Street: "If you want a friend, get a dog." — Source: AZQuotes

- On Winning: "I like winning. There's also a certain joy in it. I feel fulfilled by it." — Source: CNBC

- On Retirement: "I will never retire because I love the mechanics of the game too much to step away." — Source: Forbes

- On Legacy: "Success is measured by the impact you have on the structures you leave behind." — Source: Bookey

- On Priorities: "Everything I have is for sale, except for my kids and possibly my wife." — Source: AZQuotes

- On Motivation: "The money eventually becomes just a scorecard for how well you are playing the game." — Source: The Wall Street Journal

- On Fighting Tyranny: "A lot of people died fighting tyranny. The least I can do is vote against it in corporate America." — Source: Time

- On Obsession: "You have to be completely obsessed to dig deep enough to find the hidden value that others miss." — Source: HBO Documentary