Lessons from Chuck Akre

Investor Chuck Akre evaluated stocks using a straightforward model he called the three-legged stool: great businesses, honest managers, and wide reinvestment runways. He bought companies that met these criteria and held them for decades, ignoring market fluctuations as long as the underlying economics stayed intact.

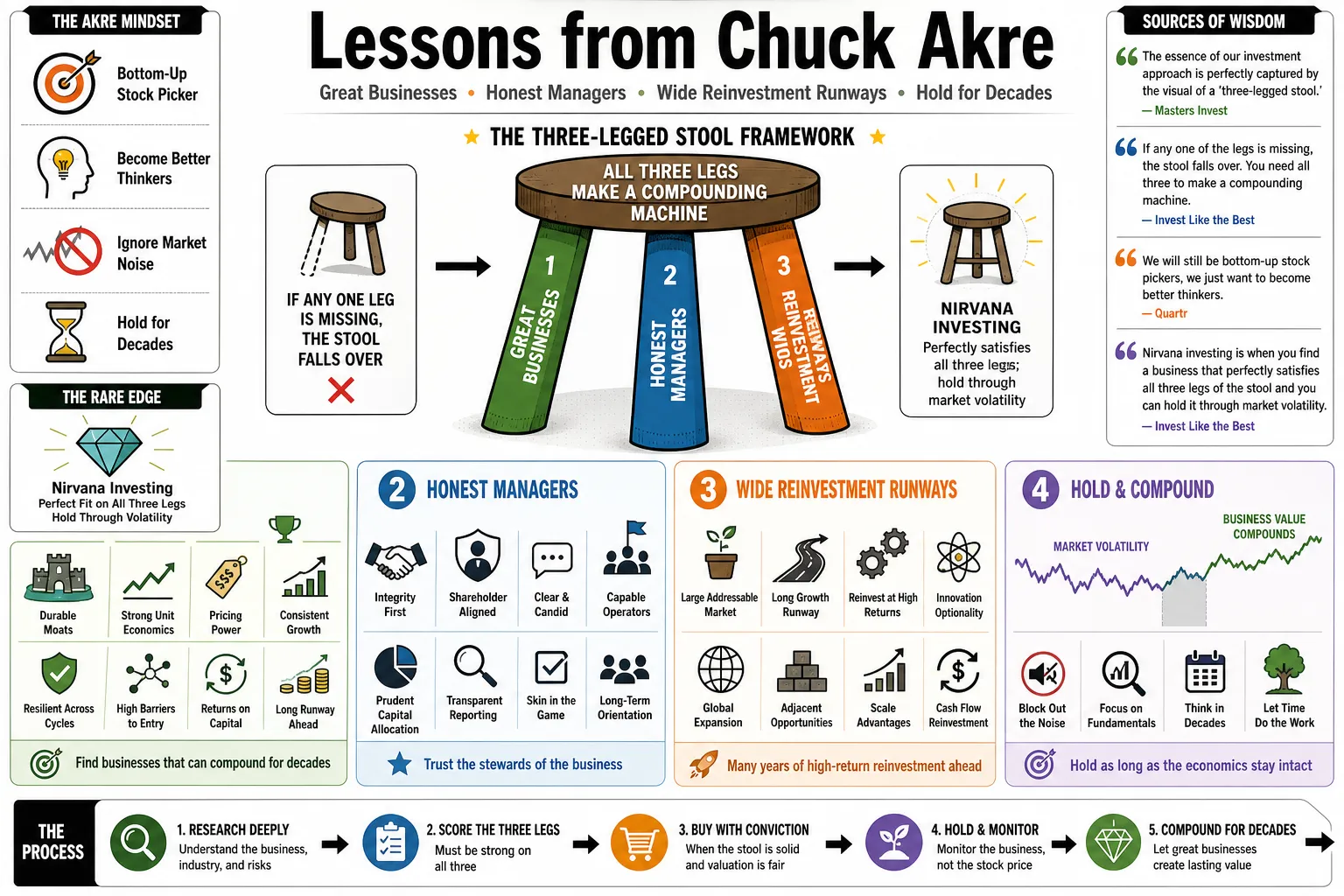

Part 1: The Three-Legged Stool Framework

- On the visual metaphor: "The essence of our investment approach is perfectly captured by the visual of a 'three-legged stool.' This metaphoric three-legged stool describes what we look for in an investment: extraordinary business, talented management, and great reinvestment opportunities." — Source: Masters Invest

- On finding balance: "If any one of the legs is missing, the stool falls over. You need all three to make a compounding machine." — Source: Invest Like the Best

- On the goal of the framework: "We will still be bottom-up stock pickers, we just want to become better thinkers." — Source: Quartr

- On finding nirvana: "Nirvana investing is when you find a business that perfectly satisfies all three legs of the stool and you can hold it through market volatility." — Source: Invest Like the Best

- On the rarity of these companies: "We know from experience that these businesses are rare. They do not exist on every corner." — Source: Masters Invest

- On valuation vs. quality: "Once we have those three legs in place, we say we're just not willing to pay very much for these businesses." — Source: Akre Capital

- On the origin of the stool: Akre keeps a literal physical milking stool in his office to remind himself and his team of the three non-negotiable pillars of their strategy. — Source: Invest Like the Best

- On classifying his style: "We're neither value nor growth investors. We are compounding investors." — Source: Alpha Picks

- On the business model: "Our business model is to compound our capital. Wall Street’s business model, generically, is to create transactions." — Source: Masters Invest

- On long-termism: "The value of a great company is only really seen over the long term. They say there's no free lunch in finance, but I do think long-termism in a great company is a free lunch." — Source: Invest Like the Best

Part 2: Leg One — The Extraordinary Business

- On return on equity: "Our conclusion is that a stock’s return will approximate the company’s ROE over time, given a constant valuation and absent distributions." — Source: RSSing

- On the pond to fish in: "We like to fish in the pond of high return businesses... If you want to earn above-average returns, you need to own above-average businesses." — Source: Stock Unlock

- On defining a moat: "The definition of a moat is the ability to charge more. Having that freedom to price is, in effect, the essence of what an economic moat is." — Source: Steve Pomeranz

- On widening the moat: "We tell our managers we want the moat widened every year. That doesn’t necessarily mean the profit will be more this year than it was last year, but the business will do very well over time." — Source: Masters Invest

- On simplicity of operations: "They are understandable. They do not take a genius to run." — Source: Akre Capital

- On cash vs. accounting: "We try to find companies that... see their profits in cash. They are not natural targets of competition." — Source: Akre Capital

- On Mastercard's business model: "In regards to return on capital, there isn't a word in the English language superlative enough to talk about them. You could cut the margins in half twice and you'd still be above average for an American business." — Source: Masters Invest

- On the power of incumbency: A durable competitive advantage often comes from scale and scope that makes it nearly impossible for a new entrant to unseat an incumbent. — Source: Invest Like the Best

- On analyzing special circumstances: "High return businesses have something unusual going on. In our firm, the goal is to properly identify what is the nature of the moat; what exactly is it that’s causing this good result." — Source: ValueWalk

- On judging success: "How else is someone able to judge the success of a business enterprise than through some measurement of the growth in real economic value? It correlates to the real return on owner's capital." — Source: Novel Investor

Part 3: Leg Two — Talented Management & Integrity

- On the nature of theft: "Our experience is that once a guy sticks his hand in your pocket, he'll do it again." — Source: Invest Like the Best

- On stock price obsession: "The managers we have owned don’t have a screen in their office showing them the price of their stock." — Source: Akre Capital

- On treating shareholders as partners: Management must demonstrate not just operational skill, but a history of acting with integrity and treating outside investors as equal partners. — Source: Dokumen

- On skin in the game: He actively looks for managers who have significant personal wealth tied up in the business alongside outside shareholders. — Source: Meb Faber

- On qualitative judgment: Assessing the quality and integrity of the people who run the business is a subjective process that requires imagination, curiosity, and reading between the lines of corporate communications. — Source: Invest Like the Best

- On executive compensation: When an executive prioritizes their own compensation over the long-term compounding of the business, it is a fatal flaw for the second leg of the stool. — Source: Invest Like the Best

- On tracking capital allocation: "We evaluate management by looking at their historical record of allocating capital and the return they achieved on that incremental capital." — Source: MOI Global

- On trust: If you cannot implicitly trust the people running the business, no amount of discount in the share price makes it a worthy investment. — Source: MOI Global

- On evaluating CEOs: Akre’s 2002 meeting with American Tower CEO Steven Dodge solidified his conviction; Dodge laid out a clear plan to pay down debt without hurting common shareholders, and followed through. — Source: Investing Daily

Part 4: Leg Three — The Runway for Reinvestment

- On the most crucial leg: "The third leg ties this together—there’s an expectation for substantial free cash flow. It asks whether the history of reinvestment of free cash flow is better than good, whether the opportunity for reinvestment is high quality, and whether the runway is broad and long." — Source: Latticework

- On dividends vs. reinvestment: "If a business has a high return on owner’s capital, we would like them to be able to take all the free cash they generate and put it back into that business to continue to earn those high rates of return. It’s way more efficient than paying us a dividend." — Source: Economic Times

- On the runway: A great business with great management is only a true compounding machine if it has the opportunity to redeploy its excess cash back into the business at similarly high rates for a long time. — Source: Masters Invest

- On American Tower's model: "Akre calls this high profit-margin business model 'vertical real estate.' The cost of tower construction had already occurred and did not need to be repeated for additional tenants." — Source: Investing Daily

- On identifying bottlenecks: "We believe that cell towers are the 'bottleneck' business within wireless data and communications, spanning countries, wireless carriers, handset manufacturers, and connected devices." — Source: GuruFocus

- On the limits of compounding: Without a broad and long runway for reinvestment, the mathematical magic of compounding eventually stalls as the business runs out of high-return projects. — Source: Invest Like the Best

- On cash generation: "We want to see what’s happening from a cash basis perspective... We are trying to look at businesses in terms of what kind of cash can they produce." — Source: GeoInvesting

- On capital redeployment: The skill of management in finding new avenues to reinvest cash flow is what prevents a high-return business from stagnating into a slow-growth dividend payer. — Source: Fifth Person

- On book value growth: "The best way to see if a business is adding shareholder value is by the growth in its book value per share." — Source: Invest Like the Best

Part 5: The Math and Magic of Compounding

- On the Thomas Phelps influence: "In 1972, I read a book... called 100 to 1 in the Stock Market by Thomas Phelps. Reading the book really helped me focus on the issue of compounding capital." — Source: The COBF

- On seeking 100-baggers: "Peter Lynch often spoke about ten-baggers. Here was Phelps talking about 100-baggers... Phelps laid out a series of examples where an investor would in fact have made 100 times his money." — Source: Market Folly

- On the math of a penny: "Double a penny a day for a month gets you $10,737,000. That's 100% returns for 31 periods, the mathematical reality that drives our patient approach." — Source: Substack

- On basis points: "Every basis point of return — let alone every 100 basis points — has a staggering difference in outcomes in the long run. That’s why you stay focused on the long term and the rate of return; that is where the difference is." — Source: Novel Investor

- On driver of returns: "Rate of return is what drives us." — Source: Dokumen

- On setting realistic expectations: "If we buy companies in which shareholders' capital compounds at a 20% rate of return over a reasonable time period and we pay a below-average multiple for it, our investors will do extremely well." — Source: Dokumen

- On the core thesis of investing: "To make money in the stock market you must have the vision to see them, the courage to buy them and the patience to hold them." — Source: Market Folly

- On time as an ally: Compounding requires uninterrupted time; every time you interrupt the process to trade, you reset the clock and introduce friction. — Source: Invest Like the Best

- On the coffee can portfolio: He advocates for buying great businesses and "putting them in a coffee can," allowing compounding to work without the drag of taxes or emotional trading. — Source: Invest Like the Best

- On obsession with compounding: He describes his daily routine as spending "nearly every waking hour" trying to identify businesses capable of sustaining high compounding rates. — Source: Invest Like the Best

Part 6: The Art of Not Selling (And When to Sell)

- On the most costly mistakes: "Of our most costly mistakes over the years, almost all have been sell decisions. The mistake, in virtually every instance, has been selling too soon." — Source: Scribd

- On holding through temptation: "Holding on means resisting the temptations to sell—and there are many. We tune out politics and macroeconomics. To the surprise of many, neither valuation nor price targets play a role in our sell decisions." — Source: GuruFocus

- On buy and hold vs exceptionalism: "Buy and hold is not our philosophy. What we want to do is own businesses that are exceptional until they are no longer exceptional. It’s a nuance on the notion of buy and hold." — Source: Substack

- On resisting the urge to trim: "We try to resist the temptation to sell (or trim, even) on the basis of valuation alone. We are unfazed when our businesses are quoted in the market at prices above what we would pay for them." — Source: Substack

- On business reality vs. stock quotes: "We own shares for multi-year periods and so our continued investment success has far more to do with the economics of the underlying businesses than it has to do with their last share price quote." — Source: Substack

- On the hardest thing in investing: "The most difficult thing to do in our business is not sell, if you're a long-term investor." — Source: Dokumen

- On valid reasons to sell: "We sell really when we think we’re reevaluating the economic characteristics of the business... It is typically because of an adverse change in the business itself." — Source: Scribd

- On losing exceptionalism: "We’re not afraid to sell, but we want to know that the company really isn’t exceptional anymore, because it has often taken me a long time to understand just how good the really good ones are." — Source: Scribd

- On quarterly misses: "Our timetable is five and ten years ahead, and quarterly 'misses' often create opportunities for the capital we manage." — Source: Re-Think Wealth

Part 7: Mental Models and Simplicity

- On keeping it simple: "Everything should be made as simple as possible, but no simpler." — Source: Dokumen

- On the power of an English degree: His non-traditional background as an English major allowed him to read widely and synthesize ideas outside of standard Wall Street financial models. — Source: YouTube / Talks at Google

- On relying on intuition: "Curiosity and imagination go hand in hand in being creative and identifying businesses." — Source: Invest Like the Best

- On defining risk: "Volatility is not part of our analysis of risk. Risk involves the exposure of permanent loss of capital." — Source: Substack

- On preventing losses: "The practice of not losing money is significantly advanced by the selection of superior businesses." — Source: Masters Invest

- On true risk management: "Our primary frontier of risk management isn't wide diversification, but the quality of the individual businesses, their balance sheets, and the people who run them." — Source: Dokumen

- On the danger of leverage: "Almost every financial blow up is because of leverage." — Source: Re-Think Wealth

- On the core heuristic: "It is a route that is magnificent in its simplicity and accordingly has some chance of leading us to success." — Source: Akre Capital

- On learning from experience: "I have never been able to learn from other people's mistakes. I have to make my own." — Source: Dokumen

Part 8: Market Noise and Independent Thinking

- On geographical isolation: "The reason we are in a town with one traffic light... is that Wall Street's stuff would be intellectually appealing to us and it would distract us from what it is we do well." — Source: Dokumen

- On market predictions: "It’s not that we don’t care what the market is going to do. It’s that there is nothing in our record that suggests we have any skill in making those predictions, so we don’t bother." — Source: Insider Monkey

- On turning off the TV: "Cable news is not our ambient noise. We think it is bad for your economic health." — Source: Re-Think Wealth

- On contrarianism: "The time to get interested is when no one else is. You can’t buy what is popular and do well." — Source: Re-Think Wealth

- On exploiting false expectations: Wall Street's short-term fears often create "false expectations," which presented the opportunity for Akre to buy MasterCard at 10x earnings during a period of regulatory panic. — Source: Masters Invest

- On true stability: "The relative low level of risk comes not from the absence of volatility, but rather, from the strength of the businesses themselves." — Source: Scribd

- On ignoring price targets: "Valuation plays no role in our sell decisions, and neither do price targets... If you are selling because of a missed earnings report or the trend of the market, you’ve stopped looking at the rate of return the company can achieve over time." — Source: Re-Think Wealth

- On the limits of spreadsheets: While quantitative analysis matters, he insists that recognizing durable moats and management integrity requires looking beyond the numbers to the underlying human and competitive dynamics. — Source: Invest Like the Best

- On doing the hard work: Finding a true compounding machine is exceptionally rare, requiring patience, independent thought, and the discipline to let the math work over decades without interference. — Source: Invest Like the Best