Lessons from David Rolfe

David Rolfe is the Chief Investment Officer at Wedgewood Partners, where he runs a concentrated portfolio of roughly twenty stocks. He applies the strict pricing discipline of traditional value investing to high-growth businesses. This profile covers his views on business quality, time arbitrage, and why investors shouldn't use outdated philosophies as an excuse to miss modern opportunities.

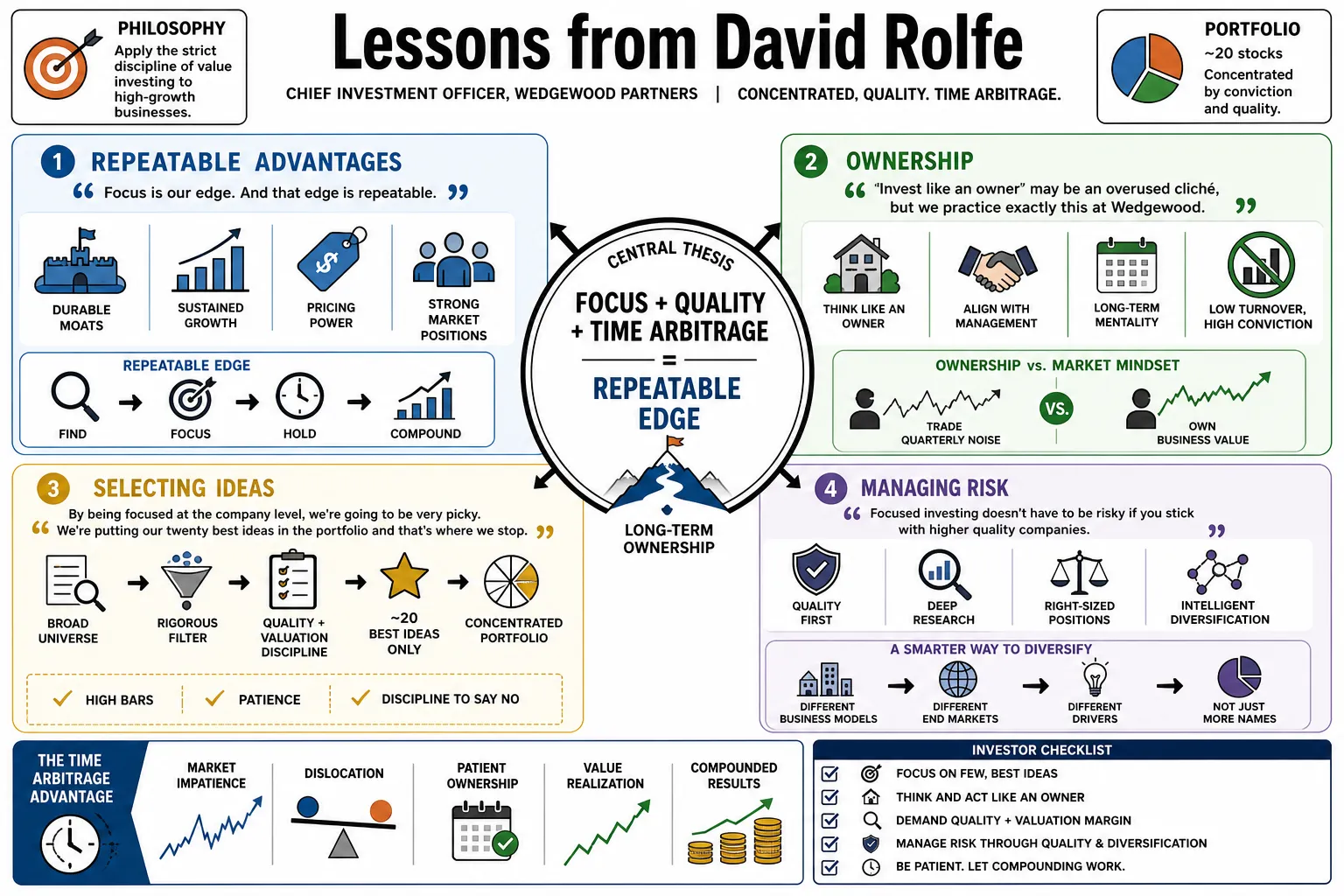

Part 1: The Focused Growth Philosophy

- On Repeatable Advantages: "Focus is our edge. And that edge is repeatable." — Source: [The Motley Fool]

- On Ownership: "'Invest like an owner' may be an overused cliché, but we practice exactly this at Wedgewood. Such a mentality becomes very powerful when so many of our active management peers profess such, but their portfolio turnover stats tell another, much different tale." — Source: [The Motley Fool]

- On Selecting Ideas: "By being focused at the company level, we're going to be very picky. In other words, we're putting our twenty best ideas in the portfolio and that's where we stop." — Source: [GuruFocus]

- On Managing Risk: "We contend focused investing doesn't have to be risky if you stick with higher quality companies; however, we think a more intelligent way to diversify is to diversify by business model." — Source: [GuruFocus]

- On The New Idea Treadmill: "Our process is not designed to spit out a bunch of new ideas all the time—we just don't think they exist. If we had a 50-stock portfolio with 100% turnover, we would be on the new idea treadmill all day long." — Source: [MOI Global]

- On Selectivity: "Less is more. Fewer ideas. Let's be very patient. Let's try to swing a big fat bat when valuation makes sense... and if there are a lot of times that we're just not going to do anything, that's okay too." — Source: [Excess Returns Podcast]

- On Position Sizing: "Why waste time with tiny positions that are either benchmark weight or too small to move the performance needle?" — Source: [Excess Returns Podcast]

- On Anti-Momentum: "We are the antithesis of momentum investing, which is a staple in large-cap growth investing." — Source: [The Motley Fool]

- On Distance from Wall Street: Being based in St. Louis rather than New York helps maintain the independent temperament necessary to ignore daily market noise and execute long-term, concentrated investing. — Source: [Excess Returns Podcast]

Part 2: Defining Best-In-Class Businesses

- On The Ultimate Safety Net: A true best-of-breed business often bails you out; even if your timing or initial valuation is slightly off, the underlying quality of the enterprise eventually drives the stock higher. — Source: [Masters in Investing]

- On Irreplaceable Products: The core of a great investment is finding companies that possess dominant, practically irreplaceable products or services that maintain high barriers to entry. — Source: [MOI Global]

- On Super-Companies: We look for super-companies that possess persistent competitive moats allowing them to stay highly profitable for decades, rather than just a few good quarters. — Source: [Masters in Investing]

- On Longevity: Good companies tend to stay good. The true value of a dominant business is only realized over a multi-year or multi-decade horizon. — Source: [Masters in Investing]

- On Financial Moats: A qualitative moat is meaningless unless it is reflected in a company's financial performance, specifically through high cash flow returns on invested capital. — Source: [Masters in Investing]

- On The Free Lunch: Because the vast majority of the market is focused on the next twelve to twenty-four months, holding onto dominant companies for a decade is one of the few remaining free lunches in finance. — Source: [Masters in Investing]

- On Capital Independence: Best-in-class businesses are those market-share dominating leaders that do not require excessive debt or financial leverage to fund their continued growth. — Source: [MOI Global]

- On Infrastructure Moats: Companies with massive, hard-to-replicate physical networks, like Copart's yard infrastructure or Old Dominion's freight lines, build physical moats that deter new competitors. — Source: [Wedgewood Partners]

- On Portfolio Composition: The goal is to filter down the entire Russell 1000 Growth Index into a highly curated basket of about twenty businesses that are structurally superior to the rest of the index. — Source: [The Motley Fool]

Part 3: Profitability as the North Star

- On The Driver of Value: "Profitability is the mother's milk of growth. Best-in-class profitability is our process North Star." — Source: [The Motley Fool]

- On Capital Efficiency: "Businesses that require the least amount of capital to maintain their competitive position and support future growth are inherently better businesses." — Source: [The Motley Fool]

- On Reinvestment: "We want to own a select list of companies that are competitively advantaged earning high returns on capital, but also have the ability to reinvest a healthy portion of retained earnings at continued high rates of capital." — Source: [Masters in Investing]

- On Cash Flow Focus: We use a proprietary Cash Flow Return on Invested Capital calculation because it strips out accounting distortions and isolates the actual cash generated relative to the capital tied up in the business. — Source: [Masters in Investing]

- On Filtering for Quality: If a company does not meet strict historical and projected profitability hurdles, it is immediately eliminated from consideration, regardless of how exciting its growth narrative might be. — Source: [The Motley Fool]

- On Compounding Wealth: Massive long-term shareholder wealth is created when a business pairs a high return on invested capital with a long runway to redeploy cash back into its own operations. — Source: [The Motley Fool]

- On Defending Big Tech: Companies like Alphabet and Meta justify their portfolio presence not just through top-line expansion, but through exceptional cash returns on invested capital despite heavy infrastructure investments. — Source: [Wedgewood Partners]

- On Return on Equity: Consistently high Return on Equity, achieved without dangerous levels of debt, is a reliable marker of a management team intelligently allocating resources. — Source: [GuruFocus]

- On Healthy Business Conditions: When a company consistently outperforms the majority of its competitors in capital returns, it indicates strong underlying pricing power and a healthy industry structure. — Source: [Focus DST]

Part 4: The Discipline of Valuation

- On Intrinsic Value: "Value never dies. Never. Price is what you pay, value is what you get." — Source: [GuruFocus]

- On Overpaying: "Buying expensive stocks is a recipe for sustained underperformance—no matter how great the underlying business may be." — Source: [The Motley Fool]

- On Ransom Prices: While seeking best-of-breed growth companies is paramount, investors must flatly refuse to pay ransom valuations for that quality. — Source: [Excess Returns Podcast]

- On The Key to Returns: Reasonable valuations act as a necessary margin of safety, and strict valuation discipline is the absolute key to generating attractive returns over a multi-year horizon. — Source: [Apple Podcasts]

- On Contrarian Growth: The most lucrative entry points occur when contrarian growth investors take advantage of periods where a great enterprise temporarily stumbles and falls out of favor. — Source: [RiverPark Funds]

- On Inverting the Model: Instead of building overly complex growth forecasts, invert the process by calculating exactly what future expectations are currently priced into the stock, and buy when those expectations are too low. — Source: [Apple Podcasts]

- On Long-Duration Assets: Equities are effectively long-duration zero-coupon bonds; when interest rates are artificially suppressed, the present value of future cash flows becomes dangerously inflated. — Source: [GuruFocus]

- On Avoiding Growth Traps: We actively avoid hyper-growth companies with risky balance sheets, preferring proven compounding machines that trade at discounts to their historical growth rates. — Source: [MOI Global]

- On Waiting for Sales: You must be willing to wait years for a top-tier company to become misunderstood or put on sale by the broader market before initiating a position. — Source: [Excess Returns Podcast]

Part 5: Conviction and Concentration

- On True Diversification: Managing risk does not mean owning fifty average companies; it means owning twenty elite companies that operate across entirely different business models. — Source: [GuruFocus]

- On The Cost of Churn: Active managers who hold fifty stocks and trade constantly are diluting the impact of their best ideas and incurring unnecessary friction. — Source: [MOI Global]

- On Raising the Bar: New additions to the portfolio must be significantly better than the weakest current holding; otherwise, you are just adding pointless turnover. — Source: [RiverPark Funds]

- On Portfolio Management: While position sizes may be trimmed or added to based on valuation, true philosophical turnover—exiting a business completely to buy another—should rarely exceed 5% to 10% annually. — Source: [GuruFocus]

- On High Conviction: Focusing strictly on the most profitable businesses allows an investor to confidently maintain weights that are several hundred basis points over the benchmark. — Source: [GuruFocus]

- On Avoiding Averages: Including small, benchmark-weighted positions in a portfolio is a waste of analytical time and does nothing to move the performance needle. — Source: [Excess Returns Podcast]

- On Knowing When to Stop: Once you have found your twenty best, competitively advantaged ideas, the smartest portfolio management decision is simply to stop buying. — Source: [GuruFocus]

- On Differentiated Portfolios: You cannot expect to significantly outperform passive indices if your portfolio looks exactly like them in composition and weight. — Source: [The Motley Fool]

- On The Mental Edge: Concentrating your investments requires a mental framework that values deep business understanding over the false security of broad sector diversification. — Source: [MOI Global]

Part 6: Time Arbitrage and Holding Power

- On Time Arbitrage: Time horizon arbitrage is one of the few remaining repeatable edges in an increasingly efficient market obsessed with the next ninety days. — Source: [Masters in Investing]

- On Voting vs. Weighing: While most market participants vote on stocks based on quarterly earnings noise, patient investors weigh them based on their intrinsic value over five to ten years. — Source: [Masters in Investing]

- On Institutional Short-Termism: Because many institutional peers are forced into short-termism by performance pressure, they routinely underreact to structural improvements and overreact to transient setbacks. — Source: [Masters in Investing]

- On Bumps in the Road: "You've got to be patient. No company clicks along without any bumps in the road forever." — Source: [MOI Global]

- On the Danger of Activity: The urge to constantly do something is the enemy of compounding; often, the best action for a portfolio manager is deliberate inaction. — Source: [Excess Returns Podcast]

- On Corporate Resilience: A truly great business model possesses the inherent resilience to outlive temporary hiccups, management transitions, and cyclical economic downturns. — Source: [MOI Global]

- On Partnership: Treating stock ownership as a long-term partnership aligns your interests with the management team and protects you from the emotional volatility of stock charts. — Source: [The Motley Fool]

- On Transcending Noise: An extended holding period acts as a filter, drowning out the daily macroeconomic noise and allowing fundamental business execution to dictate returns. — Source: [Wedgewood Partners]

- On Patience and Valuations: Holding cash and waiting patiently for a severe market dislocation is a feature, not a bug, of a disciplined investment strategy. — Source: [Wedgewood Partners]

- On Reaping the Free Lunch: The longer you hold a dominant, high-ROIC enterprise, the closer your personal returns will mirror the underlying compounding rate of the business itself. — Source: [Masters in Investing]

Part 7: Assessing Mistakes and Macro Realities

- On True Risk: "Our biggest mistakes over the years have been getting the company wrong, not the valuation wrong." — Source: [MOI Global]

- On Sins of Omission: The most painful and costly mistakes in investing are usually selling massive long-term winners entirely too early. — Source: [Masters in Investing]

- On Permanent Capital Loss: A great business can eventually bail you out if you pay too much, but investing in a fundamentally poor business model is a permanent risk to capital. — Source: [MOI Global]

- On Swallowing Pride: Failing to buy back into a structurally sound company simply because you sold it lower is a classic emotional error that costs investors dearly. — Source: [GuruFocus]

- On Monetary Normalcy: The return of interest rates to historically normal levels should be applauded, as zero-rate environments create absurd valuations and distort capital allocation. — Source: [GuruFocus]

- On Financial Stimulus: Quantitative Easing acted as artificial oxygen for financial markets, and the resulting tightening functions as a painful but necessary steroid withdrawal. — Source: [Forbes]

- On Separating Quality: Higher interest rates act as a necessary sieve, separating businesses that generate genuine organic cash flow from those that survived purely on free capital. — Source: [Wedgewood Partners]

- On Macro Impact: While predicting top-down macro shifts is futile, it is essential to understand exactly how macro factors like inflation or oil prices directly impact the moats of your holdings. — Source: [Wedgewood Partners]

- On The Chain of Causality: Market mechanics often follow a master-of-the-obvious chain: geopolitical conflict impacts energy, which drives inflation, forcing interest rate hikes, which inevitably compresses market multiples. — Source: [Wedgewood Partners]

- On Using Volatility: Broad macroeconomic panic and subsequent market volatility are the primary mechanisms that allow disciplined stock pickers to buy elite companies at intelligent valuations. — Source: [The Motley Fool]

Part 8: Holding Idols Accountable

- On Evolving Frameworks: "It wasn't that long ago the value investing mindset was 'there's no such thing as value in tech, period.' ... I think some of these mental frameworks like circle of competence and moats are wonderful, but sometimes I think maybe people take them to extremes." — Source: [Masters in Investing]

- On Following Gurus Blindly: "Mr. Buffett has made it too easy for too many value folks to say... 'If Buffett refuses to invest in tech stocks... then who am I to even try?' That's a crutch." — Source: [GuruFocus]

- On Criticizing Inaction: In 2019, Wedgewood sold its decades-long stake in Berkshire Hathaway, noting that "thumb-sucking has not cut the Heinz mustard during the Great Bull Market." — Source: [Business Insider]

- On Cash Drag: Hoarding massive amounts of cash during a prolonged economic expansion can shift from being a prudent call option to becoming a considerable impediment to compounding capital. — Source: [Fox Business]

- On Missing Layups: The greatest capital allocators occasionally lose their edge by missing obvious structural shifts, such as ignoring dominant payment networks like Visa and Mastercard when they were clear layups. — Source: [CNBC]

- On Reallocating Capital: Selling stagnant legacy positions to fund investments in emerging infrastructure leaders like Alphabet and Nvidia can transform a portfolio's trajectory. — Source: [Wedgewood Partners]

- On Alphabet's Dominance: Alphabet deserves its position as a core holding because it pairs the traits of a historic profitability machine with being a clear pioneer in structural AI development. — Source: [Wedgewood Partners]

- On The Apple Ecosystem: Apple’s massive free cash flow generation and the unprecedented stickiness of its consumer ecosystem make it a prototype for modern, capital-light compounding. — Source: [ValueSider]

- On Distinct Models: Finding companies like Motorola Solutions that dominate distinct niches like land mobile radio provides necessary variety within a tech-heavy growth portfolio. — Source: [The Motley Fool]

- On Objective Analysis: No holding, regardless of its historical significance or the legendary status of its management team, should be immune from rigorous quarterly scrutiny and eventual sale if the thesis breaks. — Source: [Business Insider]