Lessons from Geoff Lewis

Geoff Lewis is the founder of Bedrock Capital and a former partner at Founders Fund. He built his firm to back "narrative violations," deliberately investing in companies that contradict market consensus. This profile collects his views on evaluating founders, concentrating capital, and ignoring industry groupthink.

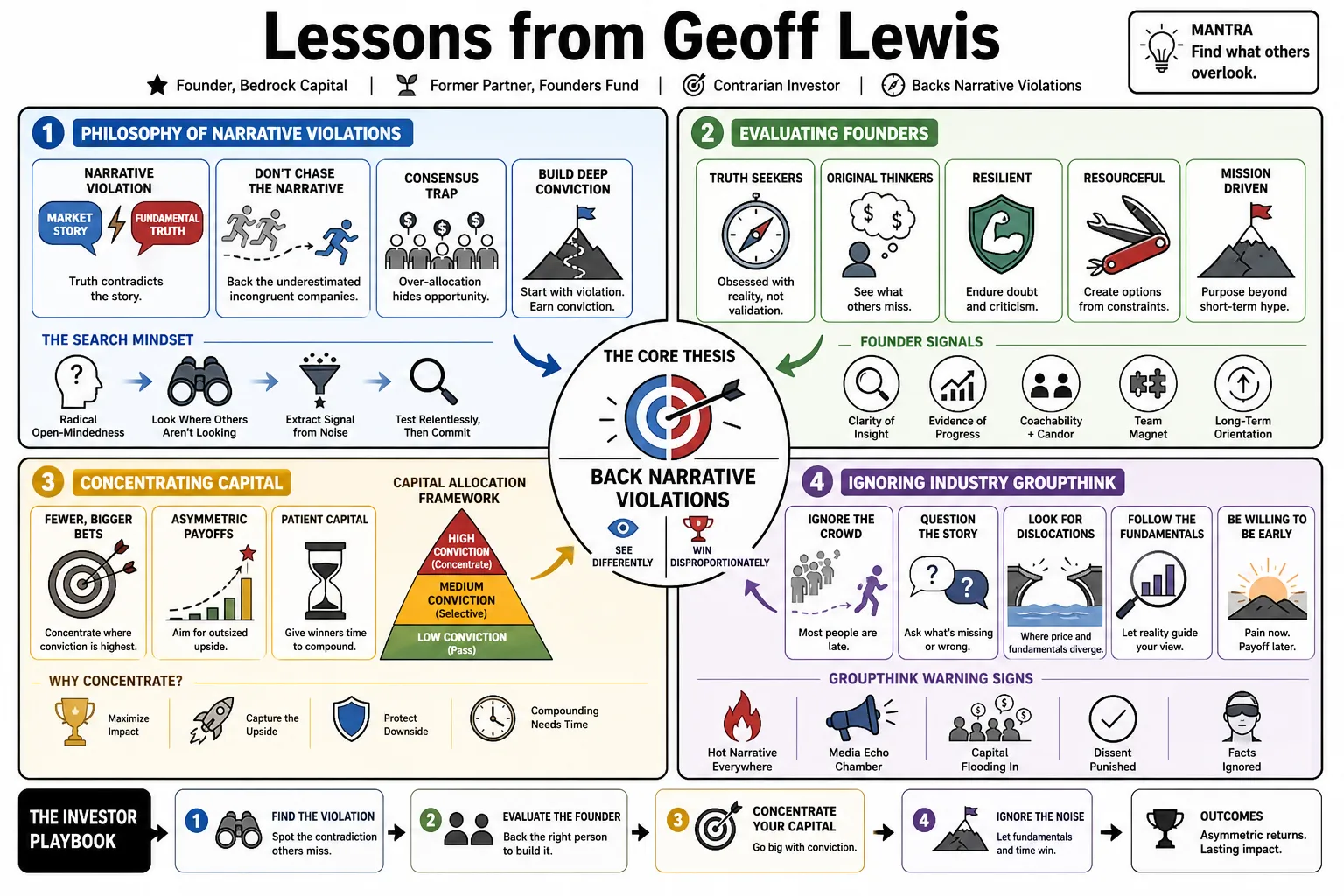

Part 1: The Philosophy of Narrative Violations

- On narrative violations: "Rather than chase the narrative, Bedrock's approach is to invest in promising companies that are underestimated precisely because they are incongruent with the storyline." — Source: [Bedrock Manifesto]

- On consensus thinking: The strongest market narratives often attract an over-allocation of capital and lead investors away from overlooked opportunities. — Source: [Bedrock Manifesto]

- On defining the framework: A narrative violation happens when the fundamental truth of a company directly contradicts the popular consensus or media storyline surrounding its market. — Source: [The Pomp Podcast: Geoff Lewis]

- On building conviction: Identifying a narrative violation is the starting point for building deep conviction where most other investors only see risk. — Source: [20VC]

- On the search process: True contrarian investing requires radical open-mindedness and constantly questioning popular stories in search of hidden truths. — Source: [Bedrock Manifesto]

- On market sentiment: Opportunities that operate independently of dominant market trends often yield the most significant returns precisely because they are ignored early on. — Source: [Medium]

- On independent thought: We constantly question popular narratives in search of hidden truths rather than accepting the conventional wisdom of Silicon Valley. — Source: [Bedrock Manifesto]

- On avoiding the herd: Venture capital is frequently over-allocated to startups that fit comfortably within existing and popular market stories. — Source: [Bedrock Manifesto]

- On incongruence: The best investments often feel uncomfortable or wrong to the broader market because they do not fit the expected storyline. — Source: [The Pomp Podcast: Geoff Lewis]

- On uncovering value: By focusing on companies that defy expectations, investors can find high-potential businesses that are significantly undervalued. — Source: [IO Podcast: Geoff Lewis]

Part 2: Evaluating Founders and Character

- On self-awareness: The best founders are those who know themselves best rather than those who are simply insecure or feel they have something to prove. — Source: [20VC]

- On authenticity: Assessing a founder's authenticity and character is far more important than evaluating their ability to pitch a perfect market narrative. — Source: [IO Podcast: Geoff Lewis]

- On intrinsic drive: Elite founders possess power plant energy, a relentless and almost inevitable drive to build massive and enduring companies. — Source: [20VC]

- On founder ambition: "This is a rare human who, to wholly self-actualize, has to build one of the largest companies on the planet and he has the ability to do it." — Source: [20VC]

- On founder execution: In evaluating companies like Rippling, the investment thesis often rests on the belief that no other company will be able to out-execute the founder. — Source: [20VC]

- On resilience: True resilience in a founder is revealed when they persist in building despite the broader market rejecting their narrative. — Source: [Medium]

- On founder motivation: We look for entrepreneurs driven by a deep internal necessity to solve a problem rather than the desire for external validation. — Source: [IO Podcast: Geoff Lewis]

- On assessing character: Character assessment involves looking beyond the resume to understand the fundamental wiring and psychological makeup of the founder. — Source: [20VC]

- On the founder's reality: The most successful entrepreneurs often operate in their own reality that is initially at odds with the prevailing industry consensus. — Source: [The Pomp Podcast: Geoff Lewis]

- On long-term commitment: We seek founders who view their company as their life's work instead of just a stepping stone. — Source: [Medium]

Part 3: Investment Conviction and Capital Concentration

- On portfolio strategy: "You identify your best company correctly and can't get that one wrong if you're going to concentrate capital." — Source: [20VC]

- On high conviction: Bedrock prefers making fewer and higher-conviction investments rather than adopting the traditional spray-and-pray model of venture capital. — Source: [Bedrock Manifesto]

- On deal flexibility: The firm prioritizes principles over rigid rules and avoids strict ownership percentage requirements to remain flexible for the best opportunities. — Source: [20VC]

- On the conviction process: Building conviction requires asking the same question ten different ways to uncover the fundamental truth of a business. — Source: [IO Podcast: Geoff Lewis]

- On concentrated bets: Writing massive checks demands an unshakeable belief that the company is fundamentally misunderstood by the market. — Source: [20VC]

- On false diversification: Spreading bets too thin dilutes returns and prevents investors from truly backing their highest-conviction ideas. — Source: [Medium]

- On the danger of rules: Rigid investment rules can prevent you from backing an exceptional company, while strong principles are far more useful. — Source: [20VC]

- On independent thinking: True conviction cannot be borrowed from other investors and must be built from the ground up through independent analysis. — Source: [The Pomp Podcast: Geoff Lewis]

- On backing winners: When you find a truly exceptional company that violates the prevailing narrative, the logical response is to concentrate capital aggressively. — Source: [20VC]

- On breaking conventions: Securing the right investment sometimes requires breaking standard VC conventions like using uncapped notes for exceptional opportunities. — Source: [20VC]

Part 4: Contrarian Thinking and Market Reality

- On market delusions: "The external validation of things like markups, it's not real. It's only real to me when the company has either been acquired or has IPOed." — Source: [20VC]

- On future pricing: "No one knows where these prices are going to land two years from now." — Source: [20VC]

- On challenging assumptions: Radical open-mindedness involves systematically dismantling your own assumptions and the assumptions of the broader market. — Source: [Bedrock Manifesto]

- On hidden truths: The most valuable insights are often hidden in plain sight and obscured only by the market's refusal to look past its preferred storylines. — Source: [Medium]

- On going against the grain: If your investment thesis feels comfortable and widely accepted, you are likely too late. — Source: [The Pomp Podcast: Geoff Lewis]

- On the illusion of safety: Investing alongside the consensus feels safe in the short term but usually leads to mediocre returns in the long run. — Source: [IO Podcast: Geoff Lewis]

- On identifying mispricing: Narrative violations naturally lead to mispriced assets because the market discounts companies that do not fit the current paradigm. — Source: [Bedrock Manifesto]

- On maintaining independence: To be a successful contrarian you must cultivate the psychological fortitude to stand alone when the market disagrees with you. — Source: [20VC]

- On the value of disagreement: If a startup idea does not spark intense disagreement or skepticism it likely is not a narrative violation worth pursuing. — Source: [The Pomp Podcast: Geoff Lewis]

Part 5: The Venture Capital Industry

- On the commoditization of capital: "Yes, VC is now commodity. Personality and critical thinking skills in an investor remain rare. Lead with vibe." — Source: [Twitter]

- On VC value-add: The traditional notion of value add in venture capital is often overstated, and true value is recognizing and backing exceptional founders without interfering. — Source: [20VC]

- On industry groupthink: Silicon Valley is highly susceptible to groupthink where capital rushes toward the loudest narrative rather than the strongest fundamentals. — Source: [Bedrock Manifesto]

- On the role of the investor: An investor's primary job is to allocate capital to the best opportunities instead of trying to operate the companies they invest in. — Source: [20VC]

- On firm culture: Building a successful venture firm requires cultivating a culture that actively rewards intellectual honesty and independent thought. — Source: [Medium]

- On the evolution of VC: As capital becomes more abundant, the differentiation between firms will increasingly rely on original thinking and deep conviction. — Source: [IO Podcast: Geoff Lewis]

- On questioning the model: We must constantly question whether the traditional VC model actually serves the best interests of the most ambitious founders. — Source: [The Pomp Podcast: Geoff Lewis]

- On intellectual rigor: The venture industry often lacks rigorous critical thinking and relies instead on pattern matching and social proof. — Source: [Bedrock Manifesto]

- On the scarcity of original thought: Capital is everywhere, but investors who are willing to think originally and act decisively remain extremely rare. — Source: [Twitter]

Part 6: Assessing Traction and Valuation

- On evaluating progress: "I mean, for us it's traction and/or perception of traction." — Source: [20VC]

- On the reality of markups: Paper valuations are often a reflection of market sentiment rather than underlying business reality. — Source: [20VC]

- On sustainable growth: We look for companies that are building compounding advantages rather than simply buying revenue to fit a growth narrative. — Source: [IO Podcast: Geoff Lewis]

- On ignoring the noise: The noise of competitive funding rounds often distracts from the fundamental mechanics of the business being built. — Source: [The Pomp Podcast: Geoff Lewis]

- On the compound startup: Companies that can successfully execute across multiple product lines simultaneously represent a massive and misunderstood opportunity. — Source: [20VC]

- On long-term value creation: True value is created over decades, which makes short-term valuation fluctuations largely irrelevant for high-conviction bets. — Source: [Medium]

- On recognizing momentum: Real traction often looks messy and unconventional and completely unlike the polished metrics presented in typical pitch decks. — Source: [20VC]

- On the danger of hype: High valuations driven by hype are fragile, and enduring value is built on the solid foundation of actual customer adoption. — Source: [IO Podcast: Geoff Lewis]

- On measuring success: The ultimate measure of a startup's success is not its valuation at the Series B, but its public market performance. — Source: [20VC]

Part 7: The Journey from Founder to Investor

- On foundational experiences: Working at Founders Fund provided a masterclass in contrarian thinking and the mechanics of venture capital. — Source: [The Pomp Podcast: Geoff Lewis]

- On transitioning roles: Moving from an operator to an investor requires a shift in mindset from building the machine to recognizing the machine builders. — Source: [IO Podcast: Geoff Lewis]

- On learning from failure: The most valuable lessons in investing often come from analyzing the companies that failed despite having the perfect narrative. — Source: [Medium]

- On building Bedrock: Launching a new firm was an exercise in applying the concept of narrative violations to the venture capital industry itself. — Source: [Bedrock Manifesto]

- On the power of partnership: Finding the right co-founder is essential for building a firm that can maintain its intellectual independence. — Source: [Medium]

- On early career lessons: Early experiences in the tech ecosystem teach you to distinguish between genuine innovation and well-marketed iteration. — Source: [The Pomp Podcast: Geoff Lewis]

- On maintaining curiosity: A successful investor must remain endlessly curious and constantly seek out new domains while challenging their own expertise. — Source: [IO Podcast: Geoff Lewis]

- On the importance of mentorship: Learning from established investors provides the framework necessary to eventually develop your own distinct investment philosophy. — Source: [20VC]

- On the investor's journey: The evolution of an investor is marked by a gradual shift from following the consensus to confidently trusting one's own judgment. — Source: [Medium]

Part 8: Navigating the Future of Technology

- On the AI landscape: Investing in AI requires looking beyond the immediate hype cycle to identify companies building fundamental and defensible technology. — Source: [IO Podcast: Geoff Lewis]

- On macroeconomic shifts: Understanding broader macroeconomic trends is helpful for contextualizing the future environment for startups. — Source: [The Breakdown Podcast: Geoff Lewis]

- On technological inevitability: We seek to back technologies that feel inevitable even if their current path to market adoption is not yet widely understood. — Source: [Medium]

- On ignoring the consensus: The most transformative technologies often emerge from domains that the consensus currently dismisses as impossible or irrelevant. — Source: [Bedrock Manifesto]

- On the pace of innovation: Investors must remain adaptable as the speed of technological change frequently outpaces the industry's ability to create neat narratives. — Source: [The Pomp Podcast: Geoff Lewis]

- On the future of work: Companies building the infrastructure for the next generation of work represent a massive opportunity hidden in plain sight. — Source: [20VC]

- On the impact of technology: We are ultimately looking for companies that will fundamentally alter the trajectory of human progress rather than just generate a quick return. — Source: [IO Podcast: Geoff Lewis]

- On identifying paradigm shifts: A true paradigm shift is rarely recognized as such in the moment and is often initially dismissed as a narrative violation. — Source: [Bedrock Manifesto]

- On the enduring power of software: Despite market fluctuations, the fundamental ability of software to transform industries remains an incredibly powerful investment thesis. — Source: [The Pomp Podcast: Geoff Lewis]