Lessons from Vlad Barbalat

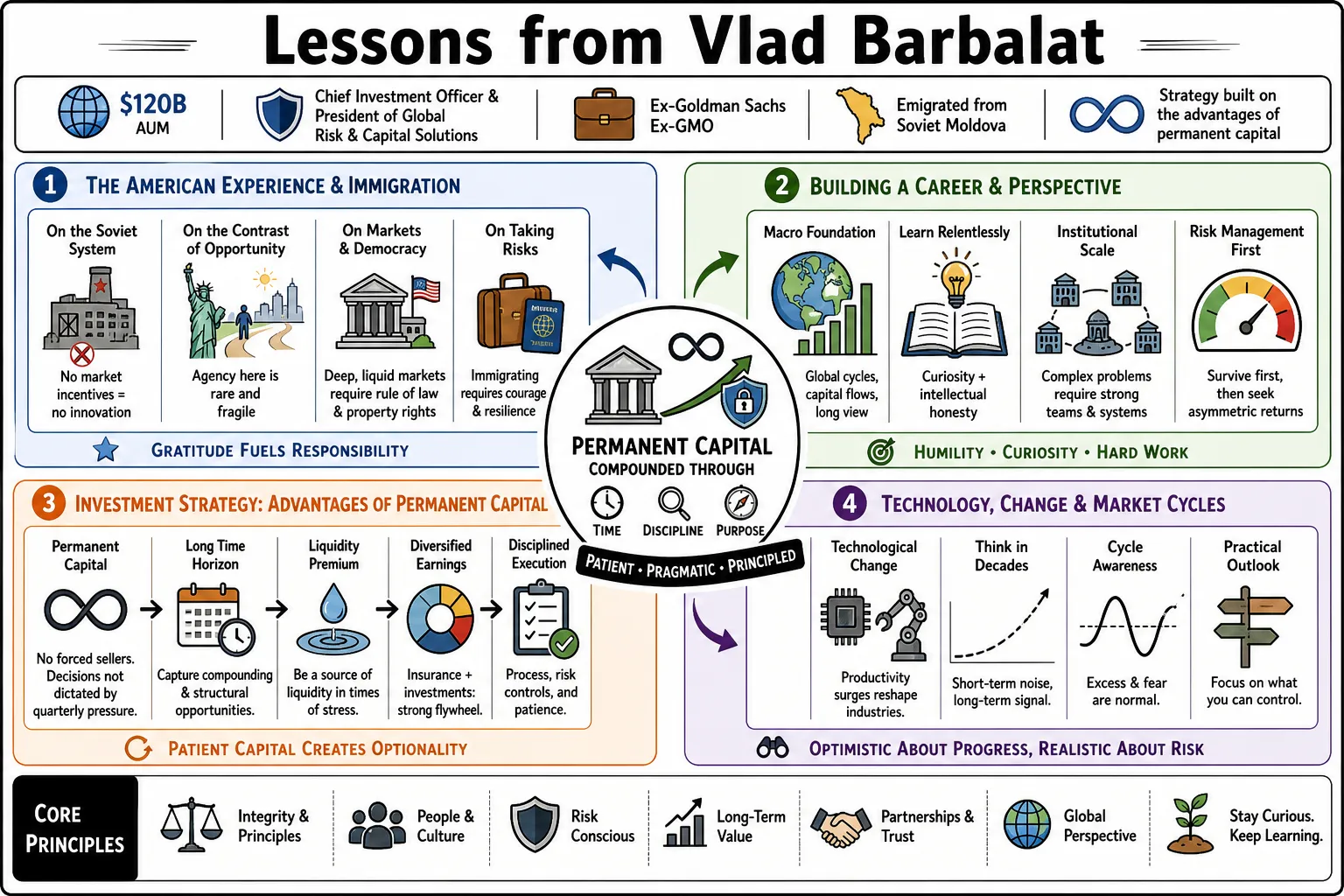

Vlad Barbalat manages a $120 billion portfolio as Liberty Mutual’s Chief Investment Officer and President of Global Risk & Capital Solutions. He built a macro background at Goldman Sachs and GMO after emigrating from Soviet Moldova, and his investment strategy now relies on the advantages of permanent capital. This collection details his approach to large balance sheets, technological change, and maintaining a practical outlook through market cycles.

Part 1: The American Experience & Immigration

- On the Soviet system: "Growing up in Soviet Moldova taught me early on that a system completely devoid of market incentives cannot sustain innovation or basic human prosperity." — Source: [Brave New World Podcast, Episode 84]

- On the contrast of opportunity: "When you arrive in the United States from a place where outcomes are predetermined by the state, you recognize that the agency afforded here is exceptionally rare and fundamentally fragile." — Source: [JFK Library Naturalization Speech]

- On financial markets and democracy: "The depth and liquidity of American financial markets are inextricably linked to the underlying legal and democratic frameworks that protect property rights." — Source: [Brave New World Podcast, Episode 84]

- On taking risks: "Immigrating inherently requires taking a massive, unhedged risk. That lived experience makes the concept of calculated financial risk-taking feel much more manageable." — Source: [Brave New World Podcast, Episode 84]

- On the meaning of citizenship: "Becoming an American citizen is an active commitment to participating in a system that rewards curiosity and the willingness to question the status quo." — Source: [JFK Library Naturalization Speech]

- On systemic resilience: "America's economy often looks chaotic from the outside, but that very friction is what makes it resilient to shocks that would break more rigid systems." — Source: [Invest Like the Best, Episode 479]

- On economic mobility: "The ability to start over and reallocate your own human capital is the defining feature of the American economic experiment." — Source: [Brave New World Podcast, Episode 84]

- On gratitude as a tool: "Maintaining a baseline of gratitude for the systemic stability we enjoy prevents the kind of cynicism that often clouds objective investment judgment." — Source: [Brave New World Podcast, Episode 84]

- On the rule of law: "Investors often take the predictability of contracts for granted. Having lived where that didn't exist, I view the rule of law as the fundamental asset class." — Source: [JFK Library Naturalization Speech]

- On contributing to the system: "True integration means utilizing the platform you are given to allocate resources in a way that generates real economic growth." — Source: [JFK Library Naturalization Speech]

Part 2: Managing Permanent Capital

- On defining permanent capital: "Permanent capital is an active psychological advantage that allows you to underwrite risks others are forced to sell during distress." — Source: [Invest Like the Best, Episode 479]

- On time horizons: "The greatest inefficiency left in modern markets is time arbitrage. When you manage $120 billion without third-party fund cycles, your edge is patience." — Source: [Invest Like the Best, Episode 479]

- On ignoring volatility: "When your capital base is permanent, you can distinguish between true impairment of capital and mere mark-to-market volatility." — Source: [Invest Like the Best, Episode 479]

- On liquidity premiums: "We are uniquely positioned to harvest the illiquidity premium because we do not have to architect our portfolio around sudden client withdrawals." — Source: [CFA Society New York]

- On counter-cyclical investing: "Permanent capital requires you to be a provider of liquidity when the rest of the market is desperately seeking it." — Source: [Invest Like the Best, Episode 479]

- On portfolio construction: "You build a permanent capital portfolio to ensure compounding survives the inevitable severe drawdowns, rather than to maximize the return of any single year." — Source: [CFA Society New York]

- On quarterly pressures: "The pressure of quarterly earnings often forces public companies and traditional asset managers into suboptimal, short-term decisions that we can entirely avoid." — Source: [Invest Like the Best, Episode 479]

- On compound interest: "Compounding works best when it is uninterrupted. Permanent capital is the structural defense against forced interruption." — Source: [Invest Like the Best, Episode 479]

- On true alignment: "When capital is permanent, the alignment between the investment team and the ultimate stakeholders is absolute. We eat our own cooking over decades." — Source: [Institutional Investor]

- On scale and access: "Deploying $120 billion allows us to access capacity, structures, and partnerships that simply aren't available to smaller or transient pools of capital." — Source: [Liberty Mutual Press Release]

Part 3: The Mutual Structure Advantage

- On policyholder alignment: "In a mutual company, the policyholder is the owner. Every dollar of return generated by the investment portfolio directly strengthens the promise made to them." — Source: [Invest Like the Best, Episode 479]

- On surviving cycles: "Mutual insurance companies are built to survive centuries. That structural durability dictates a fundamentally different approach to asset allocation." — Source: [Invest Like the Best, Episode 479]

- On structural independence: "Without public shareholders demanding immediate dividends or share buybacks, we can confidently recycle capital into higher-yielding, long-duration private assets." — Source: [Institutional Investor]

- On matching liabilities: "Our investment strategy is intrinsically linked to our liability profile. We invest to meet very specific, long-tail future obligations." — Source: [CFA Society New York]

- On corporate governance: "The governance of a mutual company inherently biases towards preservation of capital and filters out the noise of market fads." — Source: [Invest Like the Best, Episode 479]

- On risk capacity: "Because our core business generates steady premium float, we have a continuous influx of capital that increases our capacity to absorb market dislocations." — Source: [Invest Like the Best, Episode 479]

- On stakeholder trust: "Trust is our primary currency. The mutual structure reinforces that trust because our incentives are not distorted by external equity markets." — Source: [Brave New World Podcast, Episode 84]

- On capital efficiency: "Aligning the Global Risk Solutions underwriting side with the Liberty Mutual Investments side allows us to optimize our capital efficiency across the entire enterprise." — Source: [Liberty Mutual Press Release]

- On competitive advantage: "Our corporate structure is our ultimate moat. It allows us to play a completely different game than our publicly traded peers." — Source: [Institutional Investor]

Part 4: Asset Allocation & Strategy

- On global macro views: "You cannot manage a portfolio of this size without a rigorous, top-down view of global macroeconomics paired with bottom-up execution." — Source: [CFA Society New York]

- On avoiding dogmas: "Investment strategy requires intellectual flexibility. What worked in a zero-interest-rate environment will destroy capital in an inflationary regime." — Source: [Invest Like the Best, Episode 479]

- On fixed income: "Fixed income remains the anchor of the insurance portfolio, but the definition of fixed income has expanded to include complex private credit and structured products." — Source: [CFA Society New York]

- On private markets: "We look to private markets for the illiquidity premium, better structuring, tighter covenants, and deeper operational control." — Source: [Invest Like the Best, Episode 479]

- On inflation protection: "Real assets and infrastructure serve as essential structural hedges against long-term currency debasement, moving beyond simple diversification." — Source: [Institutional Investor]

- On manager selection: "When allocating externally, we are less interested in past performance than we are in the repeatability of the investment process under stress." — Source: [Invest Like the Best, Episode 479]

- On correlation breakdowns: "The traditional 60/40 portfolio assumes negative correlation between stocks and bonds. We must construct portfolios that survive when that correlation turns positive." — Source: [CFA Society New York]

- On cash as an option: "Holding liquidity during periods of tight spreads is effectively owning a call option on future market distress." — Source: [Invest Like the Best, Episode 479]

- On complexity risk: "You only take on complexity if you are being adequately compensated for it. Often, simple structures with clear cash flows outperform engineered products." — Source: [Institutional Investor]

Part 5: Navigating Market Disruption & AI

- On technological paradigm shifts: "Artificial intelligence operates as a horizontal disruption that will reprice the cost of labor and capital across every industry we invest in." — Source: [Invest Like the Best, Episode 479]

- On AI and valuations: "We are likely to see the creation of new trillion-dollar entities driven by AI, while legacy businesses that fail to adapt will face rapid multiple compression." — Source: [Invest Like the Best, Episode 479]

- On insurance and data: "The insurance industry is fundamentally a data business. Machine learning allows us to price risk with a granularity that was impossible a decade ago." — Source: [Invest Like the Best, Episode 479]

- On automation: "Automation in underwriting and investment research frees up human capital to focus on the edge cases where alpha actually lives." — Source: [Brave New World Podcast, Episode 84]

- On assessing tech investments: "When looking at technological shifts, you have to separate the fundamental structural change from the speculative froth that inevitably accompanies it." — Source: [Invest Like the Best, Episode 479]

- On energy infrastructure: "The hidden trade of the AI boom is the massive energy infrastructure required to power the compute. That is a tangible, investable asset class." — Source: [Invest Like the Best, Episode 479]

- On speed of adaptation: "The halflife of a competitive advantage is shrinking. Investment teams must have the operational agility to pivot as new technologies invalidate old theses." — Source: [Institutional Investor]

- On systemic risk of AI: "As markets become more algorithmic, we must prepare for flash crashes and correlated drawdowns that behave differently than historical panics." — Source: [CFA Society New York]

- On the limits of models: "No matter how advanced the AI, it trains on historical data. It cannot predict exogenous geopolitical shocks, which is where human intuition remains necessary." — Source: [Invest Like the Best, Episode 479]

Part 6: Risk Management & Underwriting

- On the nature of risk: "Risk is the permanent loss of capital and the inability to meet the promises we made to our policyholders, rather than simple price volatility." — Source: [CFA Society New York]

- On enterprise alignment: "By aligning the investment strategy directly with the global risk divisions, we ensure the entire balance sheet is pulling in the same direction." — Source: [Liberty Mutual Press Release]

- On tail risks: "You do not get paid for taking unquantifiable tail risks. Our job is to identify them and either price them accurately or avoid them entirely." — Source: [Invest Like the Best, Episode 479]

- On diversification: "In a liquidity crisis, all asset classes tend to correlate to one. You must diversify by underlying economic drivers instead of asset labels." — Source: [CFA Society New York]

- On underwriting discipline: "The hardest thing in both insurance underwriting and investing is the discipline to walk away when the pricing does not reflect the exposure." — Source: [Institutional Investor]

- On geopolitical risk: "We have transitioned from a unipolar world to a multipolar one. Geopolitics is a primary driver of asset pricing today." — Source: [Invest Like the Best, Episode 479]

- On stress testing: "Our portfolios are built to survive environments that models say should only happen once a century, because history shows those events happen every decade." — Source: [CFA Society New York]

- On liquidity management: "Liquidity is a spectrum. We manage our liquidity profile meticulously so that we are never forced sellers into a declining market." — Source: [Institutional Investor]

- On the role of the CIO: "The Chief Investment Officer is ultimately the Chief Risk Officer of the balance sheet. Generating yield is secondary to protecting the fortress." — Source: [Liberty Mutual Press Release]

Part 7: Career Trajectory & Lessons Learned

- On his time at Goldman Sachs: "Starting at Goldman Sachs provided a rigorous framework for understanding how global markets connect and taught me the intensity required to succeed in finance." — Source: [Invest Like the Best, Episode 479]

- On managing macro at GMO: "Running a global macro fund forces you to recognize that you can be right about the economics and completely wrong about the timing and the market reaction." — Source: [Brave New World Podcast, Episode 84]

- On transitioning to insurance: "Moving from a hedge fund to a massive insurance balance sheet shifted my focus from absolute return in a vacuum to risk-adjusted return relative to complex liabilities." — Source: [Institutional Investor]

- On building teams: "The most effective investment teams possess cognitive diversity. If everyone in the room has the same background, you have a massive blind spot." — Source: [Invest Like the Best, Episode 479]

- On intellectual honesty: "The ability to say 'I was wrong' and quickly cut a losing position is a highly valuable trait an investor can develop." — Source: [Brave New World Podcast, Episode 84]

- On mentorship: "No one navigates this industry alone. The mentors who forced me to defend my thesis under pressure shaped my entire approach to risk." — Source: [Brave New World Podcast, Episode 84]

- On the value of history: "Financial history is the best textbook. If you haven't studied the panics of the 19th and 20th centuries, you will be blindsided by the panics of the 21st." — Source: [Invest Like the Best, Episode 479]

- On continuous learning: "The markets are a humbling mechanism. The moment you believe you have figured out the game, the rules change." — Source: [CFA Society New York]

- On institutional memory: "At an organization like Liberty Mutual, you inherit decisions made decades ago. Your job is to make decisions that your successors will be grateful for in twenty years." — Source: [Liberty Mutual Press Release]

- On personal drive: "When you know what it means to have nothing, the drive to build and protect value becomes an inherent part of your psychology." — Source: [JFK Library Naturalization Speech]

Part 8: Philosophy & Pragmatic Optimism

- On pragmatic optimism: "You have to be a long-term optimist to invest in equities, but that optimism must be grounded in a pragmatic assessment of immediate risks." — Source: [Invest Like the Best, Episode 479]

- On human progress: "Despite the noise and the cycles, human ingenuity continues to compound. Betting against the collective capability of free markets is a historically bad trade." — Source: [Brave New World Podcast, Episode 84]

- On separating signal from noise: "Most financial news is designed to provoke an emotional reaction. Our job is to ignore the noise and focus entirely on structural realities." — Source: [CFA Society New York]

- On the burden of capital: "Managing a hundred billion dollars is an immense responsibility where you are directly stewarding the security of millions of policyholders." — Source: [Liberty Mutual Press Release]

- On adaptability: "The survival of a portfolio depends entirely on its capacity to adapt to a changing environment." — Source: [Invest Like the Best, Episode 479]

- On the illusion of certainty: "In macro investing, certainty is dangerous. We deal in probabilities, and the most dangerous investors are those who mistake a high probability for a guarantee." — Source: [Brave New World Podcast, Episode 84]

- On the purpose of wealth: "Capital is ultimately a tool for solving problems. The more efficiently we allocate it, the faster society progresses." — Source: [JFK Library Naturalization Speech]

- On dealing with setbacks: "Drawdowns are the tuition you pay for long-term returns. The key is to structure your balance sheet so that you never fail the course." — Source: [Invest Like the Best, Episode 479]

- On legacy: "True success in this role is leaving the platform stronger, more resilient, and better positioned for the next generation of leadership." — Source: [Liberty Mutual Press Release]