Lessons from Henry Ellenbogen

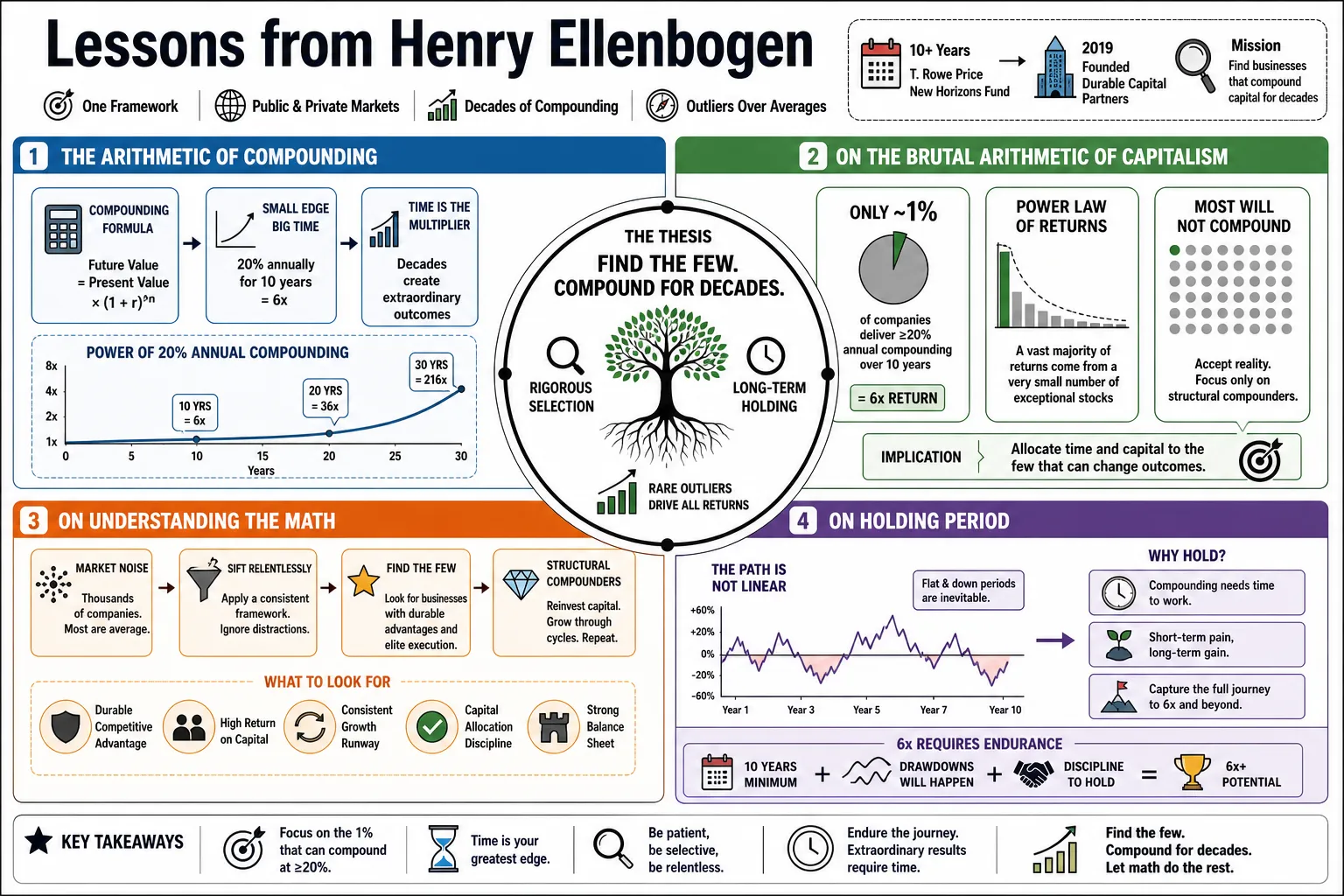

Henry Ellenbogen spent over a decade running the T. Rowe Price New Horizons Fund before founding Durable Capital Partners in 2019. He built his track record by applying a single framework to both public and private markets, searching for businesses that can compound capital over decades. This collection outlines how he spots those outliers, evaluates founders, and structures an investment firm.

Part 1: The Arithmetic of Compounding

- On the Brutal Arithmetic of Capitalism: "Over any ten-year period, only about one percent of companies achieve twenty percent annual compounding or better, resulting in a 6x return." — Source: [Invest Like the Best]

- On the Power Law of Returns: "A vast majority of our historical returns were driven by a very small number of exceptional stocks that compounded capital over long horizons." — Source: [Compound]

- On Understanding the Math: "You have to accept that most companies will not be structural compounders. Your job is to sift through the noise to find the few that consistently execute." — Source: [25iq]

- On Holding Period: "To capture a 6x return, you have to be willing to hold through the inevitable periods of drawdown and flat performance that occur over a decade." — Source: [A Wealth of Common Sense]

- On the Rarity of Greatness: "We define greatness mathematically. It is the ability to sustain high rates of return on capital over a timeframe that most competitors cannot match." — Source: [Frederik Journals]

- On Compounding Capital: "The goal is finding a business that can efficiently reinvest its own cash flows to fuel further growth without relying on outside capital." — Source: [Invest Like the Best]

- On the Cost of Missing Out: "Failing to identify one of these top one percent companies is expensive, but selling one too early is the most costly mistake an investor can make." — Source: [Value Investing with Legends]

- On Long-Term Horizon: "A ten-year timeframe forces you to look past quarterly earnings and focus entirely on the structural advantages that allow a company to multiply its value." — Source: [Compound]

- On Defining Success: "Success in growth investing is less about batting average and more about the slugging percentage when you finally find a true outlier." — Source: [25iq]

Part 2: Identifying the "One Percent"

- On True Outliers: "The top one percent of businesses share common traits: they address massive markets while maintaining highly aligned management and a clear path to win." — Source: [Frederik Journals]

- On Competitive Advantage: "You have to understand why a company's product or service is so essential that customers will rarely churn, even in a difficult macroeconomic environment." — Source: [Invest Like the Best]

- On The 'And' Business: "You have to be in the 'and' business. You have to drive growth, continuous product improvement, and long-term profitability all at once." — Source: [Invest Like the Best]

- On Sustainable Growth: "High growth is easy when money is free. Durable growth requires a business model that scales efficiently and generates real cash." — Source: [Compound]

- On Unit Economics: "Before a company can be a compounder, its unit economics must make sense. We spend a lot of time ensuring the underlying transaction is highly profitable." — Source: [Durable Capital Partners]

- On Market Size: "Outliers avoid merely taking share in an existing category; they expand the market entirely by introducing a new way of doing things." — Source: [25iq]

- On Pricing Power: "The ultimate test of a one percent company is pricing power. If they can raise prices without losing customers, they have a sustainable moat." — Source: [Invest Like the Best]

- On Innovation Cadence: "We look for companies that refuse to rest on their initial product. They must show a track record of successfully launching second and third acts." — Source: [Frederik Journals]

- On Execution: "Great ideas are abundant. The companies that become true compounders are separated purely by the relentless quality of their day-to-day execution." — Source: [Value Investing with Legends]

Part 3: The Advantage of "Act II" Founders

- On Serial Entrepreneurs: "There is a huge advantage when you go do it again, you are essentially solving the same problem but with total clarity at the beginning. If you've been one before, you have a higher probability of being one again." — Source: [Compound]

- On Founder Evolution: "We want to invest in founders who have scaled the mountain once and now understand the terrain well enough to build something even bigger." — Source: [Invest Like the Best]

- On Intellectual Honesty: "The best founders possess the intellectual honesty to admit when a strategy fails and the willingness to change direction without ego." — Source: [Frederik Journals]

- On Pattern Recognition: "An 'Act II' founder has already developed the pattern recognition to avoid early-stage scaling mistakes, allowing them to allocate capital much more efficiently." — Source: [25iq]

- On Team Building: "Experienced founders attract better talent. They know what a high-performing executive team looks like because they have built one before." — Source: [Value Investing with Legends]

- On Managing Transitions: "An essential phase for any growth company is the transition from a founder-led startup to a professionally managed enterprise. 'Act II' leaders navigate this seamlessly." — Source: [Invest Like the Best]

- On Long-Term Relationships: "We track talented people for years. Often, our best investments are backing a founder in their subsequent venture after building a relationship during their first." — Source: [Compound]

- On Ambition: "When a successful founder starts a second company, they aren't doing it for a quick payout. They are doing it to leave a lasting legacy, which perfectly aligns with our ten-year horizon." — Source: [Frederik Journals]

- On Founder-Market Fit: "We look for founders who are deeply obsessed with their specific industry. Their domain expertise usually gives them a proprietary view of the market's future." — Source: [Durable Capital Partners]

Part 4: The False Dichotomy of Public and Private Markets

- On Market Structure: "The traditional separation between private and public market investing is a false dichotomy. Great companies don't change their fundamental nature just because their stock trades on an exchange." — Source: [Value Investing with Legends]

- On Lifecycle Investing: "By following a company from its late private stage into the public markets, you build a depth of knowledge that most public-only investors can never replicate." — Source: [Invest Like the Best]

- On Information Arbitrage: "Our edge comes from seeing the private market innovation pipeline, which directly informs our public market investments." — Source: [Frederik Journals]

- On the IPO Process: "The IPO serves as a financing event along a company's timeline rather than an exit. We prefer to partner with companies that view going public as a stepping stone." — Source: [Compound]

- On Public Market Discipline: "Public markets impose a necessary discipline on companies. The requirement for transparent, quarterly feedback can actually force a business to tighten its operations." — Source: [25iq]

- On Crossover Strategy: "A crossover strategy allows us to be flexible capital partners. We can support a founder when they need private growth capital and continue that support through market volatility post-IPO." — Source: [Value Investing with Legends]

- On Valuation Realities: "Private markets can sometimes mask underlying issues by delaying mark-to-market valuations. We use our public market lens to accurately underwrite private deals." — Source: [Invest Like the Best]

- On Sourcing: "Being a known long-term holder in public equities makes us an attractive partner for late-stage private companies looking for stable capital." — Source: [Durable Capital Partners]

- On Capital Allocation: "Whether a company is public or private, the core question remains the same: how effectively is management deploying capital to generate future cash flows?" — Source: [Frederik Journals]

Part 5: Assessing Business Health and Biology

- On Biological Systems: "Companies are like biological organisms. They are either fundamentally healthy or out of balance. If they are in balance with employees, customers, and shareholders, they can grow and thrive." — Source: [Frederik Journals]

- On Corporate Homeostasis: "A healthy business naturally regulates itself. When one area grows too fast without the supporting infrastructure, the organism becomes stressed and risks failure." — Source: [Compound]

- On Employee Alignment: "You cannot have a structurally sound company if the employees are not aligned with the mission. High turnover is often the first symptom of a biological imbalance." — Source: [Invest Like the Best]

- On Customer Health: "A balanced company delivers surplus value to its customers. If you extract too much value in the short term, the relationship degrades and the ecosystem collapses." — Source: [25iq]

- On Shareholder Returns: "Shareholder returns are the byproduct of a healthy ecosystem, not the input. You generate returns by keeping the employees and customers in equilibrium." — Source: [Value Investing with Legends]

- On Cultural DNA: "The fundamental culture of a company is set early on. It becomes highly difficult to alter once an organization scales past a few hundred people." — Source: [Invest Like the Best]

- On Recognizing Disease: "We look for early warning signs of cultural decay, such as when management starts optimizing for short-term metrics over long-term customer satisfaction." — Source: [Frederik Journals]

- On Adaptation: "The best companies act like evolutionary organisms; they adapt to changes in their environment, iterating their products to survive new competitive threats." — Source: [Compound]

- On Organizational Debt: "Just like technical debt, companies accumulate organizational debt. If you don't periodically restructure and clarify roles, the organism slows down." — Source: [Durable Capital Partners]

Part 6: Building an Investment Culture

- On Humility: "We never look at a problem and assume we're right and the other person's wrong. We actually look at things and assume the other person's really smart. And what can we go learn from them?" — Source: [Invest Like the Best]

- On the Writing Culture: "Writing forces clarity. We require deep, well-researched investment memos because it prevents lazy thinking and maintains accountability." — Source: [Compound]

- On Executive Distance: "While we build strong relationships with founders, we must maintain enough executive distance to evaluate their decisions objectively and sell if the thesis breaks." — Source: [Invest Like the Best]

- On Liberal Arts Thinking: "A liberal arts background trains you to synthesize historical patterns with human psychology to better understand business cycles." — Source: [Value Investing with Legends]

- On Data and Judgment: "Data is essential for understanding the past, but human judgment is required to underwrite the future. We combine rigorous metrics with independent human intuition." — Source: [Frederik Journals]

- On Independent Thinking: "You cannot generate alpha by agreeing with the consensus. You have to cultivate an environment where dissenting opinions are expected and actively encouraged." — Source: [25iq]

- On Continuous Learning: "The market is a constantly evolving puzzle. The moment you think you have it completely figured out is the moment you are about to underperform." — Source: [Invest Like the Best]

- On Process Over Outcomes: "We judge our analysts on the intellectual rigor and fidelity of their research process rather than whether a stock went up or down in a given quarter." — Source: [Durable Capital Partners]

- On Partnership: "A successful investment firm operates as a true partnership, where incentives are aligned for the long term rather than maximizing short-term bonus pools." — Source: [Compound]

- On AI and Tooling: "We use technology to handle the processing of vast amounts of information, freeing up our human capital to focus entirely on high-level judgment and relationship building." — Source: [Cambridge Associates: Unseen Upside]

Part 7: Patience, Time Arbitrage, and Holding Winners

- On Letting Winners Run: "The biggest mathematical error in growth investing is trimming a true outlier too early. You have to let compounding do its work over years, not months." — Source: [Frederik Journals]

- On Time Arbitrage: "In a market obsessed with next quarter's earnings, our primary edge is simply our willingness to look five to ten years into the future." — Source: [A Wealth of Common Sense]

- On Volatility: "You have to accept that a stock can draw down thirty percent and still be a massive compounder over a decade. Volatility is the price of admission for high returns." — Source: [Invest Like the Best]

- On Inaction: "Often, the best investment decision you can make is to do absolutely nothing and let a great management team continue to execute." — Source: [25iq]

- On Conviction: "True conviction isn't how you feel when a stock is up; it is your willingness to buy more when the market turns against a fundamentally intact thesis." — Source: [Compound]

- On Ignoring the Noise: "We actively try to tune out the daily macroeconomic chatter. If you own the right businesses, they will compound through multiple economic cycles." — Source: [Value Investing with Legends]

- On the Pain of Holding: "Holding a massive winner is psychologically difficult. You constantly feel the urge to lock in profits. You have to train yourself to resist that urge." — Source: [Invest Like the Best]

- On Asymmetric Returns: "Because a stock can only go down completely but can rise infinitely, the math demands that you hold your biggest winners to offset your inevitable losers." — Source: [Frederik Journals]

- On Thesis Drift: "While patience is required, you must remain strictly honest about thesis drift. If the structural reasons you bought the company change, you have to sell." — Source: [Durable Capital Partners]

- On Market Myopia: "The public market systematically underprices durability. If a company can grow rapidly for twice as long as the market expects, it will be chronically undervalued." — Source: [Compound]

Part 8: Navigating Changing Market Regimes

- On Regime Change: "Investors must be careful not to hold onto imposters that only thrived under specific, temporary market conditions like an era of zero interest rates." — Source: [A Wealth of Common Sense]

- On the Cost of Capital: "When money is no longer free, the market violently reprices companies that require constant external funding to sustain their growth." — Source: [Invest Like the Best]

- On Self-Sufficiency: "In a higher rate environment, a company's ability to self-fund its operations becomes its most valuable competitive advantage." — Source: [Frederik Journals]

- On Recognizing Shifts: "You have to be a student of financial history to recognize when the underlying tectonic plates of the market are shifting beneath you." — Source: [Value Investing with Legends]

- On Adaptability: "The best companies use market downturns to play offense, acquiring weaker competitors and investing in research while others are cutting back." — Source: [25iq]

- On False Comfort: "A bull market provides a lot of false comfort. It masks poor unit economics and bad management decisions that are instantly exposed when the tide goes out." — Source: [Compound]

- On Capital Allocation in Downturns: "Management teams are truly tested during regime changes. How they allocate capital when it is scarce defines the future trajectory of the business." — Source: [Durable Capital Partners]

- On Valuation Discipline: "You cannot rely on multiple expansion to drive returns. In the long run, your return will closely mirror the underlying earnings growth of the business." — Source: [Invest Like the Best]

- On the Persistence of Innovation: "Regardless of the macroeconomic environment, technological innovation continues. The key is finding the companies that can monetize that innovation profitably." — Source: [Cambridge Associates: Unseen Upside]

- On Staying Grounded: "Market cycles will inevitably test your discipline. The only defense is to stay grounded in deep, fundamental research and a long-term horizon." — Source: [Frederik Journals]