Lessons from Jean-Marie Eveillard

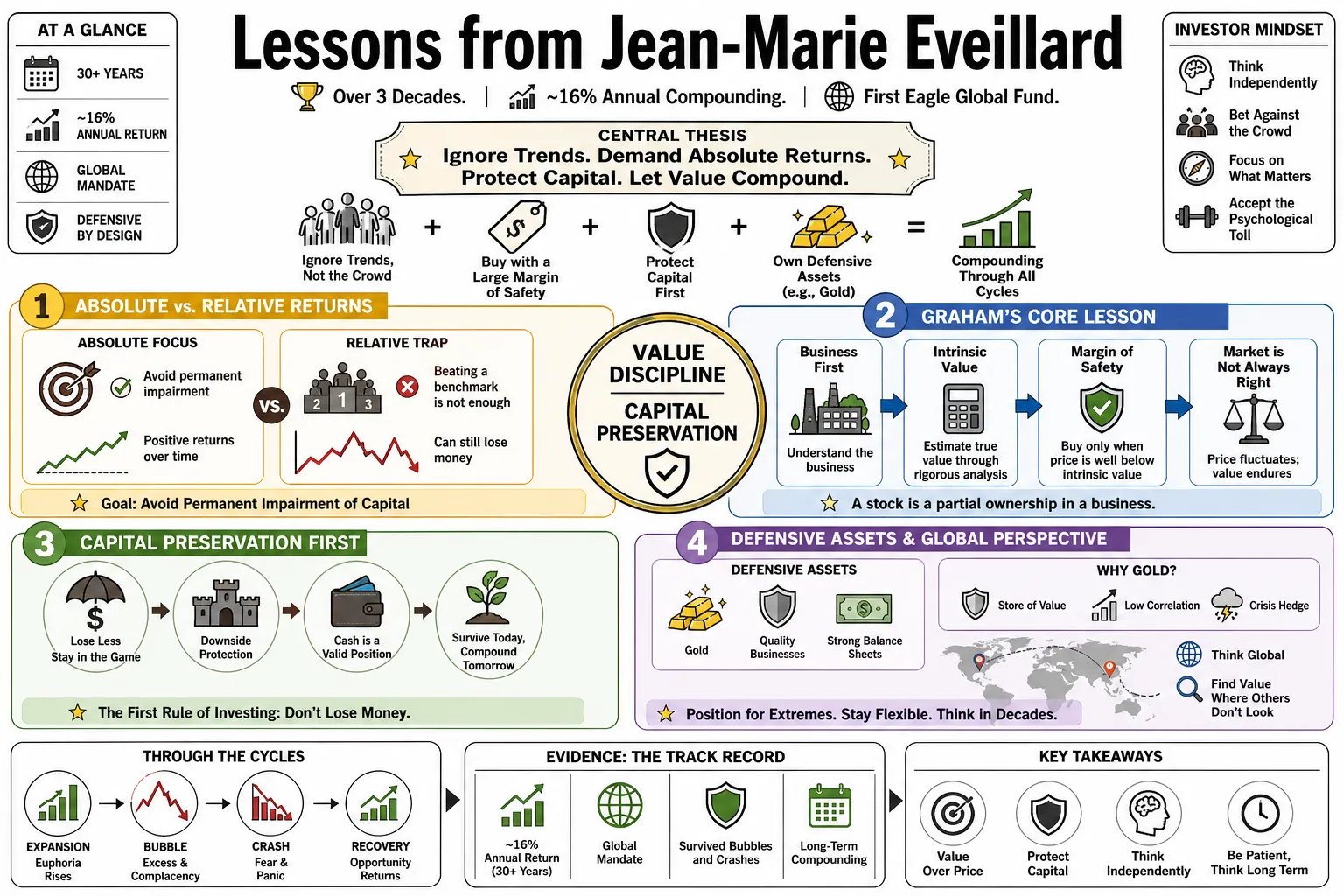

For over three decades at the First Eagle Global Fund, Jean-Marie Eveillard compounded capital at nearly 16% annually by ignoring trends and demanding absolute returns. He took Benjamin Graham's strict price discipline global, holding defensive assets like gold to weather market extremes. His track record details how to survive bubbles and crashes by accepting the psychological toll of betting against the crowd.

Part 1: The Foundations of Value

- On Absolute vs. Relative Returns: "Eveillard’s primary goal is the avoidance of the permanent impairment of capital, focusing on absolute return rather than trying to beat a benchmark." — Source: Graham and Doddsville

- On the Core Principle: "A stock is not just a ticker symbol; it is a partial ownership of a business with an underlying value that can be estimated through rigorous analysis." — Source: MOI Global

- On Graham's Core Lesson: "Eveillard adopted Graham's principle of intrinsic value, ensuring that the market price is sufficiently below what the business is actually worth." — Source: Value Investing Makes Sense

- On Capital Preservation: "Becoming a value investor allowed me to acknowledge the fact that I am uncertain about the future, so my priority is to avoid losing money, rather than to generate big returns." — Source: MOI Global

- On Intrinsic Value Calculations: "I focused mainly on stocks that were trading at 30 to 40 percent below my intrinsic value calculations." — Source: Economic Times

- On the Voting vs Weighing Machine: "In the short run, the market is a voting machine, but in the long run it is a weighing machine." — Source: QuotesWise

- On Being Wrong: "Successful investing is not about being right about the future, but about being prepared to be wrong." — Source: Novel Investor

- On Simplifying Analysis: "Identify the five or six key strengths and weaknesses that truly drive the business, rather than over-complicating analysis." — Source: Ivey Business School

- On Public Information: "To value investors, investing begins and sometimes ends with analysis of public information. If the analysis is not satisfactory, then the documents go into the waste basket." — Source: Novel Investor

Part 2: Margin of Safety and Humility

- On Humility: "You need humility because you know you can be wrong, and when you admit that, you stress caution by assigning a margin of safety to your investments so that you don't overpay for them." — Source: 25iq

- On the Unknowable Future: "The future is uncertain. Wall Street's obsession with precise forecasts is nonsense." — Source: WealthTrack

- On Cushioning Errors: "Because the future is unknowable, you must insist on a cushion or discount to intrinsic value to protect against errors." — Source: Graham and Doddsville

- On Forecasting Folly: "On Wall Street, you have all sorts of people who tell you on October 8, 2013, the Dow Jones will be at 18,225. You're lucky if they don't give you the decimals. Of course this is nonsense, nobody knows." — Source: MOI Global

- On Unprecedented Times: "It’s true that the future is unknowable. But it’s even more unknowable than usual because the fiscal and monetary steps are unprecedented." — Source: WealthTrack

- On Black Swans: "You're deluding yourself if you think you can forecast. On the contrary, you have to be aware of how many unknowns there are as well as fat tails and black swans." — Source: MOI Global

- On the Importance of Doubt: "The very humble idea that the future is uncertain—it made sense to me." — Source: MOI Global

- On Avoiding Leverage: "He avoids leverage at the portfolio level and is wary of companies with excessive debt, believing that leverage reduces the staying power of the investor." — Source: Economic Times

- On the Source of the Margin: "With the Graham approach, the margin of safety is in the discount to the intrinsic value. With the Buffett approach, it lies as much in the perceived quality of the moat." — Source: Novel Investor

- On Protecting Capital: "A margin of safety is a psychological necessity born from humility, protecting capital from the investor's own errors in judgment." — Source: 25iq

Part 3: Psychology and the Pain of Investing

- On Swimming Upstream: "Eveillard is known for his willingness to swim upstream and look foolish in the short term to be right in the long term." — Source: Value Investing Makes Sense

- On Lagging the Herd: "If you are a value investor, you have to accept in advance that you are not trying to keep up with the benchmark. Occasionally you will lag, and to lag is to suffer." — Source: Ivey Business School

- On the Pain of Value Investing: "Most people aren't cut out for value investing, because human nature shrinks from pain." — Source: Scribd

- On Sticking to Guns: "I think the secret of success of most value investors is that when times became difficult, they stuck to their guns and did not capitulate." — Source: 25iq

- On the Late 1990s Bubble: "During the late-1990s tech bubble, he refused to buy into the mania, enduring significant underperformance and client redemptions before the bubble burst." — Source: Graham and Doddsville

- On Client Money: "I would rather lose half of our clients than half of our clients' money." — Source: Graham and Doddsville

- On Temperament: "He argues that successful investing requires the temperament to withstand the pain of being out of step with the crowd." — Source: WealthTrack

- On Market Psychology: "If you are a long-term investor, you don't have to worry about market psychology." — Source: Graham and Doddsville

- On Perseverance: "It takes perseverance to be a successful investor over the long term." — Source: Ivey Business School

Part 4: Global and Eclectic Investing

- On Global Mandates: "Eveillard was an early global value investor, not restricting himself to U.S. equities." — Source: Graham and Doddsville

- On Eclecticism: "His portfolios often included small-cap stocks, distressed debt, and mundane businesses that others ignored." — Source: Graham and Doddsville

- On Macro Awareness: "While primarily a bottom-up stock picker, he pays attention to the macroeconomic environment to identify systemic risks." — Source: Graham and Doddsville

- On Benchmark Agnosticism: "The willingness to hold cash or gold when value is scarce is a hallmark of his benchmark-agnostic approach." — Source: Novel Investor

- On Going Anywhere: "His eclectic approach meant searching for bargains in any geography or asset class where a margin of safety could be found." — Source: MOI Global

- On Legal Activism: "Outraged by a low buyout offer from the Bank for International Settlements, Eveillard sued in the International Court of Justice, resulting in a payout 3x the market price." — Source: Novel Investor

- On "Net-Net" Asset Plays: "The BIS case is a classic example of an activist asset play, trading at a 50% discount to its Net Asset Value while holding massive amounts of unreflected gold bullion." — Source: Novel Investor

- On Floating Between Styles: "He floated between the Graham and Buffett styles, starting with Graham's quantitative approach and moving toward Buffett's qualitative style as markets became more competitive." — Source: MOI Global

- On Opportunity Sets: "The advantage of a global mandate is that if there is nothing to buy in the U.S., you can look at Europe, Japan, or emerging markets." — Source: GuruFocus

Part 5: Gold, Cash, and Defense

- On Gold as Insurance: "Gold provides protection against extreme outcomes... insurance against an extreme outcome, given that the system of fiat money is fraying at the edges." — Source: Forbes

- On Real Money: "Gold is cash, but not cash in the fiat currency; it is cash in real money." — Source: MOI Global

- On Inflation and Deflation: "Inflation and deflation are two faces of the same coin. Gold is the only major asset to offer some protection against both." — Source: MOI Global

- On Sizing the Gold Position: "A stake below 5% is irrelevant and anything more than 12% becomes more than insurance." — Source: Forbes

- On Unprintable Cash: "If one looks at gold as a substitute currency, then one should look at it as cash, except that cash is in a currency that cannot be printed." — Source: WealthTrack

- On Cash as Deferred Purchasing Power: "Investors should have large cash reserves only if they're holding that cash as a reserve for future opportunities—not as a long-term strategy." — Source: Validea

- On Cash Being a Residual: "Cash is a residual. We don't decide from the top down to be in cash; it's what's left when we can't find anything to buy at a reasonable price." — Source: MOI Global

- On Staying Power: "If stock markets go down and investors have cash, they can buy without having to sell something else... borrowing reduces your staying power." — Source: Economic Times

- On Defensive Tactics: "He views gold not as an investment for profit, but as a potential hedge against extreme market outcomes or a failure of the financial system." — Source: Graham and Doddsville

- On Non-Productive Assets: "Unlike many value investors who avoid non-productive assets, Eveillard famously held significant gold positions as insurance." — Source: Forbes

Part 6: Graham vs. Buffett Approaches

- On the Big Tent: "Value investing is a big tent that accommodates many different people. At one end of the tent there is Ben Graham, and at the other end there is Warren Buffett." — Source: 25iq

- On Graham's End: "At one end is the quantitative, balance-sheet focused, cigar butt investing taught by Graham." — Source: MOI Global

- On Buffett's End: "At the other end is the qualitative approach focused on moats, management quality, and long-term compounding popularized by Buffett and Munger." — Source: MOI Global

- On Transitioning Styles: "He began buying Lindt shares in 1992 when they were trading at roughly 9x earnings, starting as a Graham stock bought cheap." — Source: MOI Global

- On Evolving with Lindt: "He held Lindt for decades as it transformed into a Buffett stock held for its compounding quality and powerful brand moat." — Source: Novel Investor

- On Adapting to Markets: "He moved toward Buffett's qualitative style as markets became more competitive and pure Graham net-nets became scarcer." — Source: MOI Global

- On the Source of Moats: "With the Buffett approach, the margin of safety lies as much in the perceived quality of the moat as it does in the discount to intrinsic value." — Source: Novel Investor

- On Graham's Enduring Relevance: "Eveillard adopted Graham's principles of humility, caution, and order, applying them on a global scale throughout his 50-year career." — Source: Value Investing Makes Sense

- On Blending the Two: "His philosophy is a blend of classic Benjamin Graham value principles and Warren Buffett’s focus on business quality, characterized by a deep-seated aversion to risk." — Source: Graham and Doddsville

Part 7: Analyzing Businesses and Management

- On the Illusion of Precision: "Detailed financial models projecting ten years out often lead to a false sense of security." — Source: Ivey Business School

- On Finding the Drivers: "Instead of trying to learn every minor detail, focus on identifying the five or six key variables that actually determine the company's fate." — Source: Ivey Business School

- On the Lindt Brand: "Eveillard recognized that Lindt was an excellent business because chocolate consumption grows with GDP, and competition in luxury chocolate is limited." — Source: MOI Global

- On Profitability: "He prized businesses like Lindt that enjoyed high operating margins and strong free cash flow generation." — Source: MOI Global

- On Management Assessment: "Assessing management is difficult from the outside, but their capital allocation decisions over time provide an objective scorecard." — Source: GuruFocus

- On Temporary Turmoil: "He bought Lindt when the company was facing temporary turmoil due to management turnover and negative press, exploiting short-term fear for long-term gain." — Source: MOI Global

- On Holding Periods: "By holding positions for 20+ years, he allowed the underlying economics of the business to drive the return, rather than short-term multiple expansion." — Source: Novel Investor

- On Mundane Businesses: "He did not restrict himself to glamorous industries, often finding the most durable moats in mundane businesses that others ignored." — Source: Graham and Doddsville

- On Fragility: "He is wary of companies with excessive debt, as it makes them fragile to the unknowable future." — Source: Economic Times

Part 8: The Industry and Wall Street Nonsense

- On Relative Return Obsession: "Unlike many managers who focus on relative return, Eveillard focuses on absolute return and capital preservation." — Source: Graham and Doddsville

- On Wall Street Time Horizons: "Wall Street's six-to-twelve month time horizon... if you are a value investor, you are a long-term investor." — Source: Graham and Doddsville

- On Groupthink: "I think there is a mindset among many professional investors that if I go down the drain, well it is o.k. as long as everyone else is going down the drain with me." — Source: Novel Investor

- On Value vs Price: "Whether you're investing in art or in securities, no one should confuse value and price." — Source: Novel Investor

- On Market Cycles: "I have a great belief that everything is cyclical in life, particularly in the investment world." — Source: Novel Investor

- On the Difficulty of Being Different: "To be a value investor, you have to be willing to suffer pain... human nature shrinks from pain." — Source: AZQuotes

- On the Dangers of Benchmarking: "If you try to keep up with the benchmark, you are forced to buy what is popular, which is the antithesis of value investing." — Source: Ivey Business School

- On the True Risk: "For Eveillard, risk is not the volatility of the stock price, but the probability of a permanent loss of capital." — Source: Value Investing Makes Sense

- On Career Risk vs Client Risk: "Most fund managers prioritize career risk—the fear of lagging peers and getting fired—over the risk of losing their clients' money." — Source: Graham and Doddsville

- On the Endurance of Value: "Value investing makes sense, it works over time, so how come there are so few of us? Because it requires a temperament most people simply do not possess." — Source: GuruFocus