Lessons from Joel Greenblatt

Joel Greenblatt is a value investor, hedge fund manager, and adjunct professor at Columbia Business School. He built Gotham Capital's track record by systematically finding mispriced companies, a strategy he later distilled into the "Magic Formula." This collection covers his practical advice on special situations, valuation, patience, and why individual investors have a structural edge over large institutions.

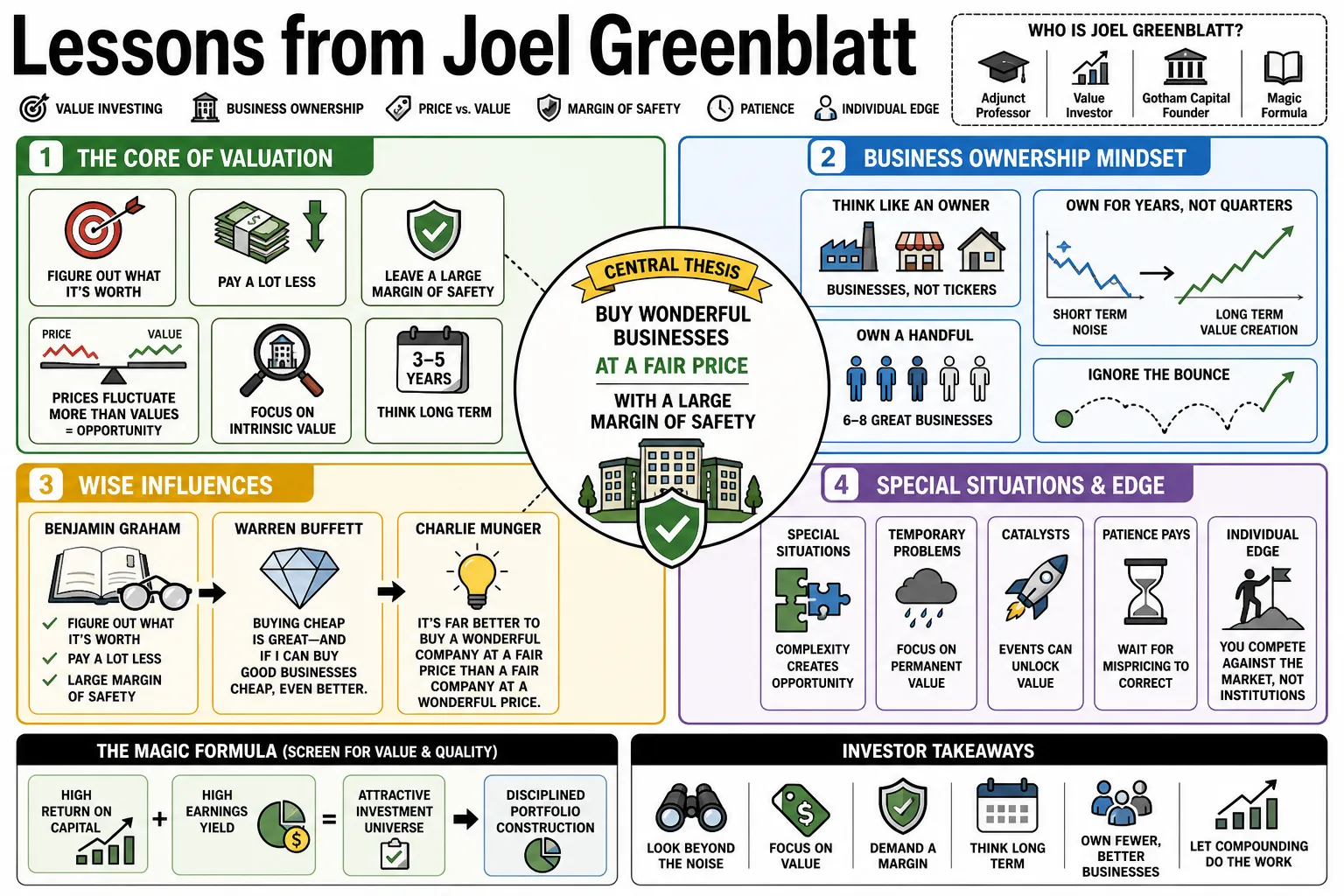

Part 1: The Core of Valuation

- On Value Investing: "Figure out what something is worth and pay a lot less." — Source: [Novel Investor]

- On Business Ownership: "If you think of them as stocks and pieces of paper that bounce around... as opposed to taking a three or five-year horizon in owning those six or eight different businesses." — Source: [The Investors Podcast]

- On Price vs. Value: "Prices fluctuate more than values—so therein lies opportunity." — Source: [Scribd]

- On Benjamin Graham's Philosophy: "Figure out what it’s worth, pay a lot less, and leave a large margin of safety." — Source: [25iq]

- On Warren Buffett's Twist: "Buying cheap is great—and if I can buy good businesses cheap, even better." — Source: [Goodreads]

- On Charlie Munger's Influence: "It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price." — Source: [25iq]

- On the Definition of Value: "All successful investing comes from getting more value than you pay for." — Source: [Goodreads]

- On Blind Speculation: "If we invest without understanding the value of what we’re buying, we’ll have little chance of making an intelligent investment." — Source: [Medium]

- On Simplicity: "A good investment idea can be explained in 2 minutes." — Source: [Columbia Business School]

- On Recognizing Quality: "If you just stick to buying good companies... and to buying those companies only at bargain prices... you can end up systematically buying many of the good companies that crazy Mr. Market has decided to literally give away." — Source: [Goodreads]

Part 2: The Magic Formula

- On the Secret to Wealth: "Buying good businesses at bargain prices is the secret to making lots of money." — Source: [Bookey]

- On Systematizing Common Sense: "The magic formula isn't magic. It just makes sense." — Source: [Goodreads]

- On Earnings Yield: "The formula focuses on earnings yield to determine how much a business earns relative to the price of the entire business, finding companies that are fundamentally cheap." — Source: [Medium]

- On Return on Capital: "Return on capital measures how effectively a company uses its assets to generate profit, separating the good businesses from the bad." — Source: [Phillip Capital]

- On Universal Application: "If the magic formula worked all the time, everyone would probably use it. If it worked every month and every year, it would be bid up and the opportunity would be gone." — Source: [Bookey]

- On Long-Term Strategy: "The book will take readers on a step-by-step journey so that they can learn the principles of value investing in a way that will provide them with a long-term strategy that they can understand and stick with through both good and bad periods." — Source: [TraderLion]

- On Emotional Discipline: "The market's very emotional, but over time, doing something logical and systematic does work." — Source: [Profit Quotes]

- On Business Quality: "Buffett realized that a good business with high returns on capital is worth more over time than a cheap but poor business, forming the quality half of the Magic Formula." — Source: [Stock Spinoff Investing]

- On Measuring Performance: "Enterprise Value to EBIT is preferred over P/E ratios because it accounts for debt and provides a clearer picture of pre-tax earnings yield." — Source: [Columbia Business School]

Part 3: Special Situations & Spinoffs

- On Spinoff Inefficiencies: "The spin-off process itself is a fundamentally inefficient method of distributing stock to the wrong people." — Source: [Medium]

- On Immediate Selling: "Once the spinoff's shares are distributed to the parent company's shareholders, they are typically sold immediately without regard to price or fundamental value." — Source: [Jackson Zhu]

- On Institutional Blind Spots: "Most professional investors don't even think about individual spinoff situations... Just doing a little of your own thinking about each spinoff opportunity can give you a very large edge." — Source: [Bookey]

- On Finding Opportunities: "In the stock market, knowing where to 'bang' is the secret to your fortune." — Source: [Bookey]

- On Unconventional Paths: "Edge comes from taking your knowledge and applying it in places off the beaten path." — Source: [Medium]

- On Insider Incentives: "A theme common to many attractive investment situations is that management and employees have been incentivized to act like owners." — Source: [Medium]

- On Leveraging Motives: "By focusing on the motives of management and other insiders, you can turn this advantage for insiders into an advantage for yourself." — Source: [Medium]

- On Understanding the Present: "Whether the in-laws can or cannot predict the future is beside the point; they don't have to—they already know how to profit from studying the present." — Source: [Reddit]

- On Messy Situations: "Look for complicated, messy, and obscure situations like spinoffs and restructurings, because opportunities are best when you understand why others are missing them." — Source: [Columbia Business School]

Part 4: Risk and Capital Preservation

- On Capital Protection: "One way to create an attractive risk/reward situation is to limit downside risk severely by investing in situations that have a large margin of safety." — Source: [Goodreads]

- On the Downside: "Look down, not up, when making your initial investment decision. If you don't lose money, most of the remaining alternatives are good ones." — Source: [Goodreads]

- On Risk vs. Reward: "Comparing the risk of loss in an investment to the potential gain is what investing is all about." — Source: [Bookey]

- On Quantifying Risk: "Your job remains to quantify, by some measure, a stock's upside and downside. This is such an imprecise and difficult task, though, that a proxy of your own may well be in order." — Source: [Goodreads]

- On Over-Diversification: "Don't screw up a perfectly good stock-market strategy by diversifying your way into mediocre returns." — Source: [Reddit]

- On Concentration: "The strategy of putting all your eggs in one basket and watching that basket is less risky than you might think." — Source: [Goodreads]

- On Statistical Risk Reduction: "Statistics say that owning just two stocks eliminates 46% of the nonmarket risk of owning just one stock... [this risk is reduced] by 81% with eight stocks." — Source: [Reddit]

- On Position Sizing: "Position sizing is the most important thing... being too timid on the few good ideas that come your way is like the biggest mistake people make." — Source: [The Knowledge Project]

- On Asymmetric Bets: "I size my positions not based on the upside potential, but on the downside risk." — Source: [The Investors Podcast]

- On Margin of Safety: "Margin of Safety: the difference between price and value. A larger difference means a larger margin of safety that protects investors from big losses." — Source: [Novel Investor]

Part 5: Market Psychology & Mr. Market

- On Market Volatility: "Imagine that you are partners in a business with a crazy guy named Mr. Market. Every day, he offers to buy your interest or sell you his. The catch is that Mr. Market is a very emotional fellow." — Source: [Goodreads]

- On Long-Term Rationality: "Although over the short term Mr. Market may price stocks based on emotion, over the long term Mr. Market prices stocks based on their value." — Source: [Goodreads]

- On Ignoring the Noise: "The truth is that I don't really have to know why people are willing to buy and sell shares of most companies at wildly different prices over very short periods of time. I just have to know that they do!" — Source: [The Investors Podcast]

- On Contrarian Temperament: "The greatest investors tend to have 'a screw loose'." — Source: [The Investors Podcast]

- On Avoiding Speculation: "Choosing individual stocks without any idea of what you're looking for is like running through a dynamite factory with a burning match. You may live, but you're still an idiot." — Source: [QuoteFancy]

- On Playing the Game: "Speculating without knowing what you're doing is not a great idea." — Source: [Masters in Business]

- On the Cost of Ignorance: "If you don’t know what you’re doing, it’s an expensive place to find out." — Source: [Masters in Business]

- On Asset Allocation: "Almost everyone should have a significant portion of their assets in stocks. But here it comes—few people should put ALL their money in stocks." — Source: [25iq]

- On Handling Pain: "Whether you choose to place 90% of your assets or 40% of your assets in stocks should be based largely on how much pain you can take on the downside." — Source: [25iq]

Part 6: Patience and Time Horizons

- On the Biggest Edge: "The secret to being successful is patience. The big secret that no one bought... is really just having a longer time horizon than most people." — Source: [Masters in Business]

- On Short Horizons: "Most people just won't wait that long. Their investment time horizon is too short." — Source: [Bookey]

- On the Necessity of Underperformance: "Value investing doesn't always work... and that is a very good thing. The fact that our value approach doesn't work over periods of time is precisely the reason why it continues to work over the long term." — Source: [AZ Quotes]

- On Sticking to the Process: "It wasn't because we were idiots in 1998 and geniuses in 2000; it's just that we followed a process and finally got paid." — Source: [YouTube]

- On Shrinking Horizons: "While technology allows people to check prices thirty times a second, time horizons are shrinking, giving a massive edge to anyone who can think in terms of three to five years." — Source: [YouTube]

- On Inevitable Convergence: "I promise [my students] if they do good valuation work, the market will agree with them. I just never tell them when." — Source: [The Investors Podcast]

- On System Reliability: "While the market is inefficient in the short term, it is reliable in the long term, and eventually, Mr. Market will pay you back." — Source: [Substack]

- On Loving the Puzzle: "Many successful managers are in it for the money, but the most successful long-term investors are those who enjoy solving puzzles and have the passion to stick through down years." — Source: [YouTube]

- On Following Concepts: "Being a successful investor requires following a few simple concepts, but most people won’t do it." — Source: [Novel Investor]

Part 7: The Individual Investor's Edge

- On Professional Limitations: "If you really want to 'beat the market,' most professionals and academics can't help you... That leaves only one real alternative: You must do it yourself." — Source: [Goodreads]

- On Wall Street Disadvantages: "The truth is, it isn't fair. The well-heeled Wall Street money managers and the hotshot MBAs don't have a chance against you and this book." — Source: [Bookey]

- On Career Risk: "Most mutual fund managers are effectively shut out from their best chances to beat the market." — Source: [Novel Investor]

- On Herding Behavior: "Institutional career risk forces managers to follow the herd, creating opportunities for patient individual investors who don't have to report quarterly earnings." — Source: [Novel Investor]

- On Indexing for the Masses: "Indexing is the right solution for most people, but for those who can value businesses, there are more opportunities now because so much money has moved to passive funds." — Source: [YouTube]

- On Independent Thinking: "You cannot be a good value investor without being an independent thinker, as you must see value where the market does not." — Source: [Gracious Quotes]

- On Choosing a Strategy: "The best investment strategy is the one that makes sense and that you can stick with." — Source: [Profit Quotes]

- On Size as an Anchor: "Buffett was forced to move away from Graham’s cigar butts and special situations because his capital base became too large to move the needle with small, cheap stocks, leaving those gems for individuals." — Source: [Stock Spinoff Investing]

- On Independent Research: "The central thesis of this approach is that individual investors have an advantage over professionals because they can afford to be patient with a simple, rules-based system." — Source: [Scribd]

Part 8: Teaching, Education, and Society

- On the Value of Teaching: "I think the exercise of trying to figure out how to simplify concepts has been incredibly helpful to me over the last 13 years of teaching and I hope my students have benefited from it." — Source: [Scribd]

- On Financial History: "My advice to young people, if they really want to be successful in this business, is to learn financial history... and you will not be in such awe of everything that's going on." — Source: [Columbia Business School]

- On Writing to Learn: "Writing is the process by which you learn that you don’t understand as much as you think you did." — Source: [The Knowledge Project]

- On Studying Mistakes: "I’d rather read their mistakes and make different ones." — Source: [The Knowledge Project]

- On Systemic Unfairness: "Right now, systematically, it's unfair — and the inequality starts from the beginning." — Source: [Business Insider]

- On Educational Inequality: "The U.S. education system is designed to be unequal from the start. Poor and minority students are systematically sent to the worst schools, often based on their zip code." — Source: [SoBrief]

- On Raising Expectations: "If a high-performing school could be opened in a low-income urban neighborhood and then successfully replicated... it would help show that—with the right supports—poor, low-income, and minority students could achieve at the highest levels." — Source: [SoBrief]

- On Alternative Credentials: "If it's true that, regardless of background, most of us 'can,' then considering alternative methods for job seekers to demonstrate accomplishment and job readiness should be on the table." — Source: [SoBrief]

- On Building an Economy for All: "The goal... is simple: establish an economy that works for all its citizens, not just the inherently advantaged." — Source: [Goodreads]

- On Business Ethics: "You don’t create long-term value by cheating your customers... treating your employees well... being a good member of the community." — Source: [The Knowledge Project]