Lessons from Laura Sloate

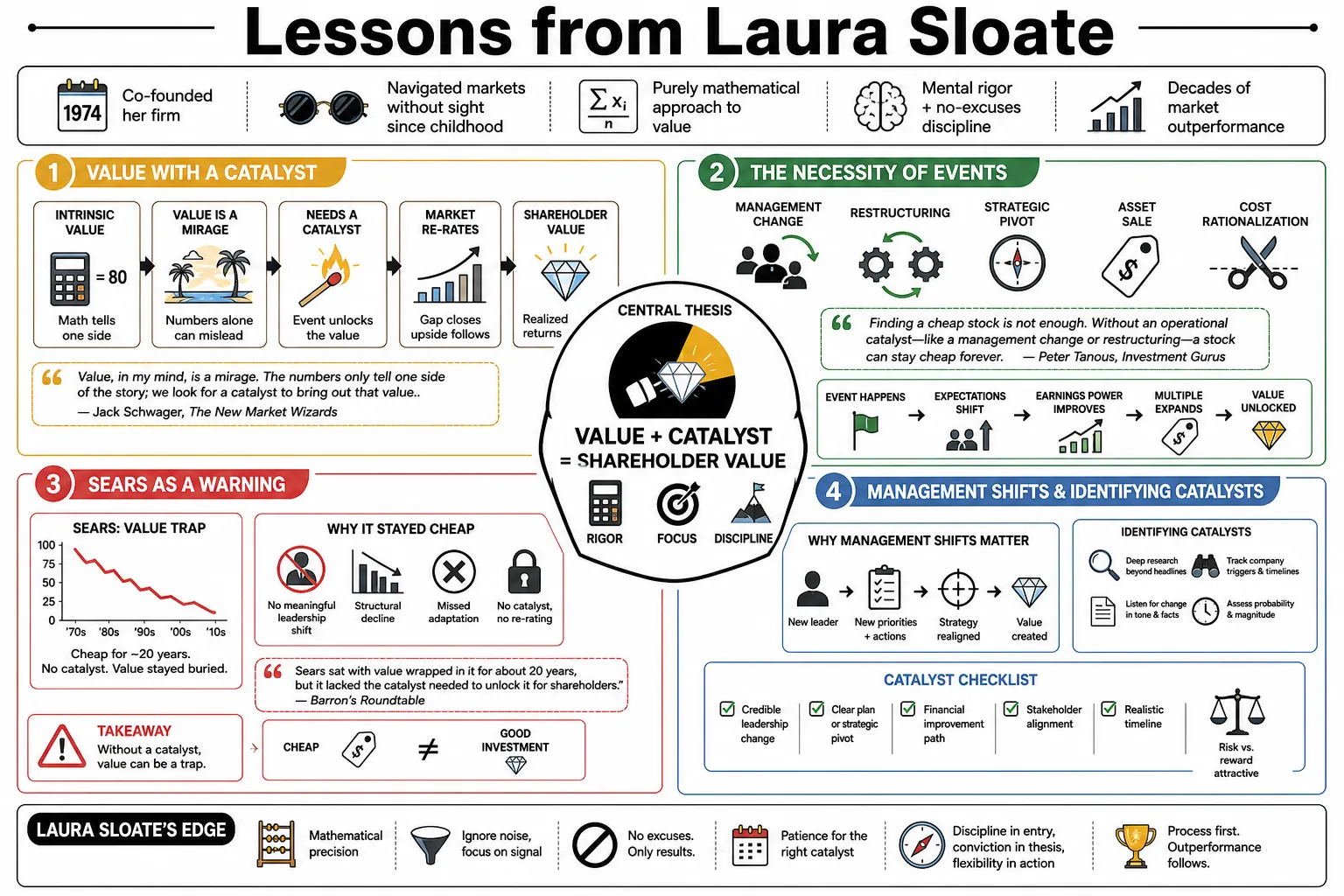

Laura Sloate co-founded her firm in 1974, building a career as a top Wall Street analyst while navigating the markets without sight since childhood. She traded visual charts and management stories for a purely mathematical approach to value. This profile examines the mental rigor and "no-excuses" discipline that fueled her decades of market outperformance.

Part 1: Value with a Catalyst

- On the Value Mirage: "Value, in my mind, is a mirage. The numbers only tell one side of the story; we look for a catalyst to bring out that value." — Source: Jack Schwager's The New Market Wizards

- On the Necessity of Events: "Finding a cheap stock is not enough. Without an operational catalyst—like a management change or restructuring—a stock can stay cheap forever." — Source: Peter Tanous's Investment Gurus

- On Sears as a Warning: "Sears sat with value wrapped in it for about 20 years, but it lacked the catalyst needed to unlock it for shareholders." — Source: Barron’s Roundtable

- On Management Shifts: "A change in leadership is often the most reliable signal that a company is ready to pivot from value-trap to value-creator." — Source: The Wall Street Transcript

- On Identifying Catalysts: "We look for events like spin-offs, asset sales, or new product cycles that the market hasn't yet priced into the equity." — Source: Neuberger Berman Insights

- On Institutional Inertia: "Companies often need a crisis or a new CEO to break the inertia that keeps their assets undervalued." — Source: Cannon Financial Group

- On the 'Story' vs. the Reality: "We don't buy stories. We buy specific, measurable events that will change the cash flow of a business." — Source: Jack Schwager's The New Market Wizards

- On Corporate Restructuring: "A restructuring is only valuable if it actually lowers the cost of capital or increases the return on assets." — Source: Peter Tanous's Investment Gurus

- On Real Estate Assets: "Value hidden in real estate is useless if management has no plan to sell it or monetize it." — Source: Barron’s Roundtable

- On the Catalyst Checklist: "Before buying, ask: what exactly is going to happen in the next 12 to 18 months to make other people want to own this?" — Source: The New York Times

Part 2: The Discipline of Risk and Selling

- On the 15% Rule: "If a stock drops 15% from your purchase price, sell it. It’s gone. You can always buy it back later if you were right." — Source: Jack Schwager's The New Market Wizards

- On Cutting Losses: "The biggest mistake investors make is hanging on to a loser because they don't want to admit they were wrong." — Source: Peter Tanous's Investment Gurus

- On Sun America (Broad): "My 15% rule was born from a loss in Sun America; I watched it go from $11 to $4 because I didn't have a stop-loss discipline." — Source: Barron’s Roundtable

- On Thesis Violation: "The moment the reason you bought the stock is no longer true, the stock must be sold immediately." — Source: The Wall Street Transcript

- On Avoiding Meltdowns: "Individual portfolios are ruined by one or two meltdowns. If you cut your losses early, you never have a meltdown." — Source: Peter Tanous's Investment Gurus

- On Emotional Selling: "Selling at a loss is a mechanical act, not an emotional one. It is a cost of doing business." — Source: Neuberger Berman Insights

- On Position Sizing: "If you can't sleep at night because of a position, it's too big. Size your risk so your judgment stays clear." — Source: Jack Schwager's The New Market Wizards

- On the 'Hope' Trap: "Hope is not an investment strategy. If you're hoping a stock comes back to even, you've already lost." — Source: Cannon Financial Group

- On Market Volatility: "In a volatile market, your discipline is the only thing that keeps you from becoming part of the noise." — Source: The New York Times

- On Re-evaluating After a Sale: "Once you sell a stock because it hit your stop, wait. Don't rush back in until the fundamentals have actually stabilized." — Source: Barron’s Roundtable

Part 3: Mastery through Mental Models and Focus

- On the Back-of-an-Envelope Test: "If you give me a reliable estimate of a company's earnings power, I can value it in my head in seconds." — Source: Jack Schwager's The New Market Wizards

- On Staying in Your Circle: "Stay with what you know. Improve what you know, but don't wander into sectors where you have no edge." — Source: Peter Tanous's Investment Gurus

- On Avoiding Tech Widgets: "We don't buy tech stocks because we don't know who is going to come out with a better widget tomorrow and kill our thesis." — Source: Barron’s Roundtable

- On the Power of Memory: "Because I can't see charts, I have to remember the numbers. That forces a deeper level of concentration on the data." — Source: Time Magazine

- On Identifying 'Vision': "I look for 'vision'—an insight into an asset or a trend that goes beyond what is printed in the morning paper." — Source: Peter Tanous's Investment Gurus

- On Comsat and Assets: "We saw Comsat not as an earnings story, but as an asset redeployment story involving satellite consortiums." — Source: Peter Tanous's Investment Gurus

- On Mental Math Efficiency: "Mental math isn't just a trick; it’s a way to filter out the garbage quickly so you can focus on the real opportunities." — Source: Jack Schwager's The New Market Wizards

- On Historical Context: "Following an industry for 30 years gives you a perspective that a spreadsheet from a young analyst can't replicate." — Source: The Wall Street Transcript

- On the Importance of 'No': "Sometimes your best investments are the ones you don't make." — Source: Cannon Financial Group

- On Focus over Breadth: "It is better to be an expert on 60 companies than to have a vague opinion on 600." — Source: Jack Schwager's The New Market Wizards

Part 4: Analytical Rigor and EVA

- On Economic Value Added (EVA): "We use EVA to see if management is actually creating value or just spending shareholder capital." — Source: Peter Tanous's Investment Gurus

- On the Cost of Capital: "If the return on capital isn't higher than the cost of that capital, the company is effectively melting away." — Source: Barron’s Roundtable

- On Earnings Power vs. Book Value: "Book value today is often an illusion. Focus on the sustainable earnings power of the assets instead." — Source: The Wall Street Transcript

- On Cash Flow Quality: "Reported earnings are for the public; cash flow is for the owners. Always look at the cash." — Source: Neuberger Berman Insights

- On Debt as a Call Option: "A company with huge debt and slim equity acts like a call option on the business if operations improve slightly." — Source: Jack Schwager's The New Market Wizards

- On Hilton Hotels and Gaming: "We predicted a Hilton earnings miss by tracking the baccarat win-rates long before the company admitted the shortfall." — Source: Barron’s Roundtable

- On Management's Capital Allocation: "Watch how management spends their last dollar of profit. That tells you more than their annual report." — Source: Peter Tanous's Investment Gurus

- On Industrial Turnarounds: "In manufacturing, look for the 'hidden' asset—it's usually the efficiency that can be squeezed out by new management." — Source: The Wall Street Transcript

- On Valuation Discipline: "Never pay for growth that hasn't happened yet. Pay for the value that is there, and take the growth as a bonus." — Source: Cannon Financial Group

- On SEC Filings: "The footnotes are where the real story lives. Most people read the glossy front; we read the dry back." — Source: Jack Schwager's The New Market Wizards

Part 5: Breaking Barriers and Professional Resilience

- On Early Discrimination: "In 1968, they told me I had three strikes: I was a woman, I was blind, and I was inexperienced." — Source: Time Magazine

- On Ignoring Excuses: "I don't believe in handicaps. You either do the work or you don't." — Source: The New York Times

- On Starting Her Own Firm: "I started Sloate, Weisman, Murray & Co. because I wanted to be judged solely on my numbers, not my appearance." — Source: Vogue

- On Professional Competition: "The market doesn't care who you are. It only cares if you are right." — Source: Jack Schwager's The New Market Wizards

- On Resilience in Bear Markets: "We made money in 1973-74 because we weren't afraid to go against the prevailing gloom of the street." — Source: Peter Tanous's Investment Gurus

- On Female Leadership: "Being one of the first women to lead a firm meant I had to be twice as prepared as everyone else in the room." — Source: Barnard College Profile

- On the 'Blind Broker' Moniker: "I don't mind what they call me as long as my clients see the returns in their accounts." — Source: Time Magazine

- On Career Longevity: "The only way to stay in this business for 50 years is to keep your ego out of your portfolio." — Source: The Wall Street Transcript

- On Overcoming Rejection: "Every 'no' I received early in my career just made me a more aggressive researcher." — Source: Neuberger Berman Biography

Part 6: Information Processing and the Edge of Blindness

- On Filtering Noise: "My blindness is an advantage because it filters out the visual noise of the tape and the charts." — Source: Jack Schwager's The New Market Wizards

- On Information Intake: "I have readers who go through annual reports with me for hours every day. I listen for the things others overlook." — Source: Time Magazine

- On Listening to Management: "You can hear the hesitation or confidence in a CEO's voice during an earnings call. That's data you can't see on a chart." — Source: Peter Tanous's Investment Gurus

- On Technology as an Equalizer: "The computer and voice-synthesis technology have leveled the playing field for information access." — Source: The New York Times

- On Synthesizing Data: "I process data in my head as I hear it. It creates a mental map of the company that is very difficult to distract." — Source: Vogue

- On the Absence of Visual Bias: "I don't care what the CEO looks like or how nice the headquarters is. I only care about the balance sheet." — Source: Jack Schwager's The New Market Wizards

- On the Intensity of Concentration: "When you can't see, your other senses—especially your memory and logic—become much sharper tools." — Source: Time Magazine

- On Staying Updated: "I use technology to 'read' the news as it breaks, but I wait for the numbers before I react." — Source: Neuberger Berman Insights

- On the Discipline of Reading: "We read everything. If a company is in our portfolio, we know every footnote in their 10-K." — Source: Peter Tanous's Investment Gurus

Part 7: Portfolio Management and Concentration

- On the 60-Stock Rule: "We manage 60 to 70 stocks. If you can't beat the market with 60 well-researched names, you're doing something wrong." — Source: Jack Schwager's The New Market Wizards

- On Closet Indexing: "Most large funds are just closet indexers. We want to make specific bets where we have an information edge." — Source: Peter Tanous's Investment Gurus

- On Portfolio Concentration: "Concentration is where the alpha is. Diversification is for people who don't know what they are doing." — Source: Barron’s Roundtable

- On Mid-Cap Opportunities: "We find the most value in mid-to-large cap companies that are going through a transition the market hasn't noticed." — Source: The Wall Street Transcript

- On Sector Avoidance: "We avoid sectors where the variables are out of our control, like fashion or high-stakes R&D biotech." — Source: Neuberger Berman Insights

- On Market Capture: "Our goal is to capture 100% of the upside and only 70% of the downside. That’s how you win over decades." — Source: Cannon Financial Group

- On Position Turnover: "We aren't traders. We are owners of businesses, but we aren't afraid to sell if the price is wrong." — Source: Jack Schwager's The New Market Wizards

- On Managing Other People's Money: "When you manage money, you are a steward of someone else's future. That requires a sober mind." — Source: The Wall Street Transcript

- On the Futility of Macro Timing: "We don't time the market. We time the individual catalysts in our 60 stocks." — Source: Peter Tanous's Investment Gurus

Part 8: Character, Routine, and Longevity

- On the 4:00 AM Routine: "I wake up at 4:00 AM every day to start my research. By the time the market opens, I’ve already done my thinking." — Source: The New York Times

- On Friday Research Lunches: "Every Friday, we have a lunch where we only talk about our mistakes. You learn nothing from your winners." — Source: Peter Tanous's Investment Gurus

- On Her Mother's Influence: "My mother told me I could do anything anyone else could, just a little differently. I believed her." — Source: Time Magazine

- On Philanthropy and the Arts: "Investing is a science, but opera and art are the things that keep your mind creative and open." — Source: New York Philharmonic Trustee Profile

- On the Ethics of Wall Street: "Integrity is the only asset you can't buy back once you've sold it. Keep your reputation clean." — Source: Neuberger Berman Insights

- On Intellectual Honesty: "If you lie to yourself about why a stock is down, you will eventually go broke." — Source: Jack Schwager's The New Market Wizards

- On Constant Learning: "The day you think you’ve figured out the market is the day you should retire. It is a game of constant learning." — Source: Cannon Financial Group

- On Personal Legacy: "I want to be remembered as a great investor who happened to be blind, not a blind woman who happened to invest." — Source: Vogue