Lessons from Mario Gabelli

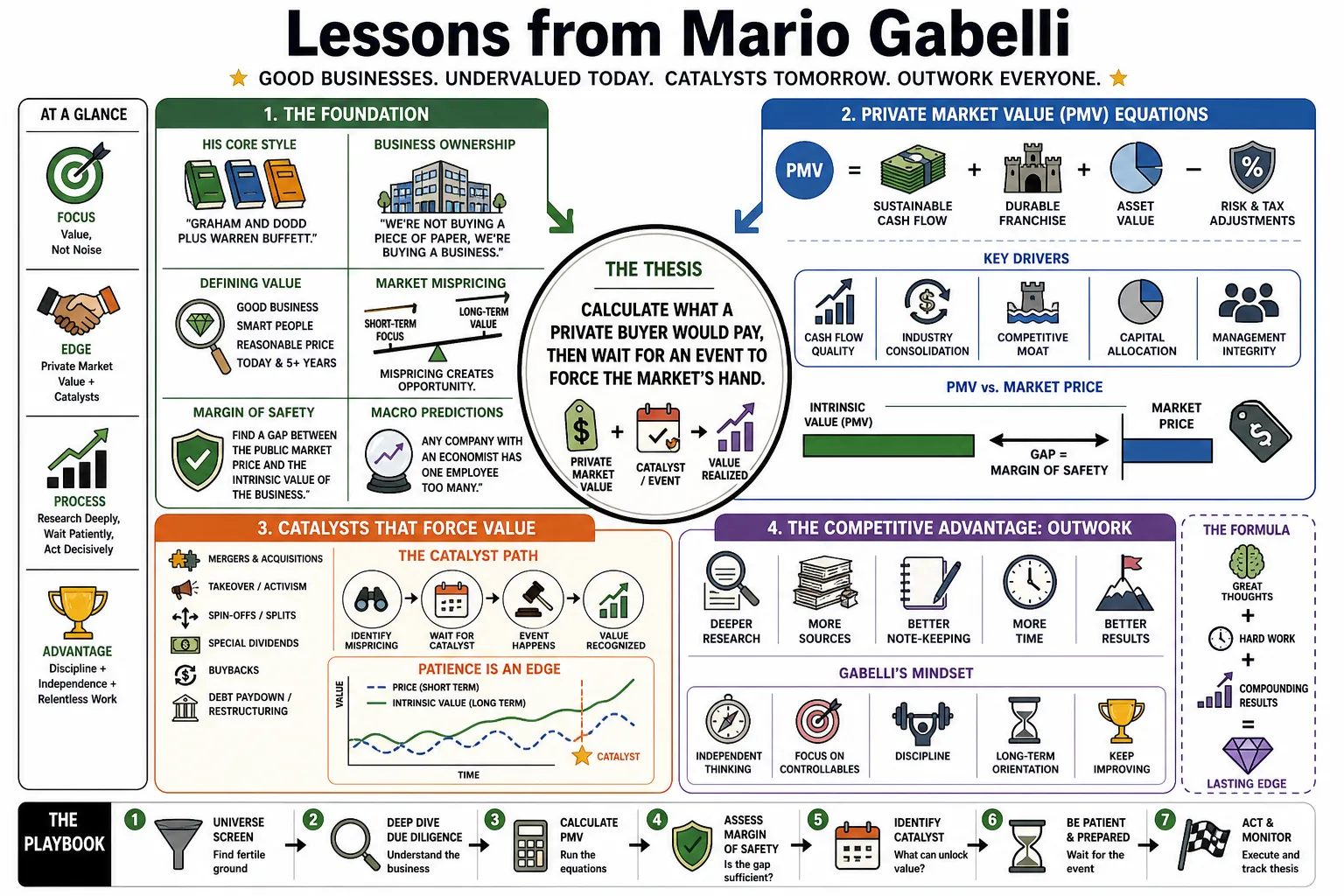

Mario Gabelli built GAMCO Investors on a straightforward premise: calculate what a private buyer would pay for a public company, then wait for an event to force the market's hand. He pushed value investing past basic asset discounts by zeroing in on cash flow, durable franchises, and industry consolidation. This collection outlines his Private Market Value equations and his insistence on simply outworking the competition.

Part 1: The Foundations of Value Investing

- On His Core Style: "Graham and Dodd plus Warren Buffett." — Source: [GuruFocus]

- On Business Ownership: "We're not buying a piece of paper, we're buying a business." — Source: [QuotesWise]

- On Defining Value: "Value investing, the way I define it, is finding a good business run by smart people, at a reasonably good price relative to its values today and five or more years from now." — Source: [QuotesWise]

- On Market Mispricing: "The market misprices assets because it focuses on the short term, creating opportunities for value buyers." — Source: [Columbia Business School]

- On Margin of Safety: "Find a gap between the public market price and the intrinsic value of the business." — Source: [GAMCO Investors]

- On Macro Predictions: "Any company with an economist has one employee too many." — Source: [GAMCO Investors]

- On The Durability of Value: "Value investing will never go out of style. Who doesn't want value?" — Source: [GAMCO Investors]

- On Research Methodologies: "In the course, we dug into companies' annual reports and 10-Ks. It was that analytical work that made me say, 'This is what I want to do.'" — Source: [Columbia Business School]

- On Adapting Tradition: "We evolved the traditional Graham and Dodd asset-based valuation to focus on modern cash-flowing businesses." — Source: [Forbes]

- On Growth vs. Value: "Just as growth-stock investors will pay a higher price-to-earnings ratio for higher earnings growth, private-market-value investors will pay a higher multiple of cash flow for faster cash-flow growth." — Source: [QuotesWise]

Part 2: Private Market Value (PMV) Explained

- On Defining PMV: "Private Market Value is the price an informed industrialist would pay for the entire company." — Source: [GuruFocus]

- On The Takeover Premium: "Private market value includes its intrinsic value and the takeover premium that would be paid by an acquirer." — Source: [Observer]

- On The Core Question: "If you were an informed industrialist or a very wealthy person, what would you pay for the entire company?" — Source: [Observer]

- On Valuing the Future: "Ask what that company will be worth in five, ten or 15 years." — Source: [Observer]

- On Enterprise Value: "You must add net debt to the equity capitalization to understand the true cost a private buyer would face." — Source: [Forbes]

- On The Informed Buyer: "Buyers in the same industry see synergies and structural advantages that public markets often ignore." — Source: [The AIC]

- On Ignoring the Ticker: "Focus on what a strategic buyer would pay in a negotiated transaction, not the daily market fluctuations." — Source: [The AIC]

- On Franchise Assets: "PMV evolved from hunting for simple asset discounts to identifying franchise value and reliable cash generation." — Source: [Behind the Balance Sheet]

- On The Pricing Gap: "The core strategy is buying public stock when it trades at a significant, verifiable discount to its PMV." — Source: [Forbes]

- On Realizing Value: "A discount to private market value only matters if there is a realistic mechanism to close that gap." — Source: [Traders Log]

Part 3: The Power of the Catalyst

- On The Ideal Stock: "The ideal stock comes with a catalyst – something that will bring the public to it." — Source: [QuotesWise]

- On The Purpose of a Catalyst: "We focus on a catalyst, or event that will help surface the value in the company." — Source: [Reddit Value Investing]

- On Types of Events: "A catalyst may take many forms and can be an industry or company-specific event." — Source: [25iq]

- On Specific Triggers: "Catalysts can be a regulatory change, industry consolidation, a repurchase of shares, a sale or spin-off of a division, or a change in management." — Source: [Reddit Value Investing]

- On Timeline Uncertainty: "You don't always know exactly when the catalyst will happen, but you must identify its probability." — Source: [GAMCO Investors]

- On Management Changes: "A shift in executive leadership is often the fastest way to unlock trapped corporate value." — Source: [GAMCO Investors]

- On Regulatory Shifts: "Changes in government rules frequently serve as the primary catalyst for major industry restructuring." — Source: [Traders Log]

- On Financial Engineering: "Companies restructuring their balance sheets or repurchasing shares act as their own internal catalysts." — Source: [Futu]

- On Industry Consolidation: "External forces often push fragmented industries to consolidate, forcing the market to recognize private market values." — Source: [Futu]

- On Avoiding Value Traps: "Value without a catalyst can remain cheap indefinitely; you need an event to force the market's hand." — Source: [25iq]

Part 4: Analyzing Businesses and Cash Flow

- On Free Cash Flow: "The best barometer of a company's true value is EBITDA minus maintenance capital expenditures." — Source: [Behind the Balance Sheet]

- On Accounting Profits: "You have to look past reported accounting earnings to understand the actual cash a business generates." — Source: [Behind the Balance Sheet]

- On Inflation Protection: "Seek out companies with inflation-indexed earnings—businesses that can raise prices to match or exceed rising costs." — Source: [GAMCO Investors]

- On Interest Rates: "A business must be fundamentally structured to operate well within a higher interest-rate environment." — Source: [GAMCO Investors]

- On Cash Burn: "It becomes very difficult to justify high multiples for companies burning cash when interest rates are rising." — Source: [GAMCO Investors]

- On The Supply Chain: "Do bottom-up research—read the 10-Ks, visit competitors, and understand the total supply chain." — Source: [Musixmatch Podcasts]

- On Capital Allocation: "Smart management teams know how to deploy free cash flow efficiently to build long-term shareholder wealth." — Source: [Columbia Business School]

- On Irreplaceable Assets: "Look for franchise assets that are functionally impossible or prohibitively expensive for a competitor to replicate." — Source: [Observer]

- On Corporate Debt: "Avoid companies with excessive leverage that cannot use their free cash flow to pay down debt quickly." — Source: [GAMCO Investors]

Part 5: Macroeconomics and Market Psychology

- On Contrarianism: "The ignored is where we love." — Source: [QuotesWise]

- On Market Sentiment: "What we like to do is to buy, buy, buy when everyone doesn't want it." — Source: [QuotesWise]

- On Valuation Stability: "Businesses don't change in value as quickly as the market." — Source: [QuotesWise]

- On Assessing Extremes: "As always, when we think about the economy and each investment we ask: How bad is bad? How good is good?" — Source: [GAMCO Investors]

- On Market Multiples: "The multiple is a function of interest rates, which is a function of debt and deficit." — Source: [Columbia Business School]

- On GDP Drivers: "Productivity and population growth are the ultimate keys to driving global economic expansion." — Source: [Columbia Business School]

- On National Debt: "Growth is needed to improve the standard of living and reduce the nation's debt-to-GDP ratio." — Source: [Columbia Business School]

- On Artificial Intelligence: "AI is a powerful productivity tool, but it might accelerate the problem of income inequality." — Source: [Columbia Business School]

- On Market Corrections: "Higher inflation and higher 10-year Treasury yields act as major wild cards that can trigger swift market repricing." — Source: [GAMCO Investors]

Part 6: Work Ethic and the "PHD" Mindset

- On Who To Hire: "Look for people who are a 'PHD': Poor, Hungry, and Driven." — Source: [Columbia Business School]

- On Outworking Competitors: "If everybody you're going to compete with wants to work from nine to five, you work from five to nine." — Source: [Columbia Business School]

- On Passion vs. Work: "This is not a job. This is my passion." — Source: [QuotesWise]

- On The Fear of Failure: "The risk of failure is an important driver... that's why you get up at four or five in the morning." — Source: [GAMCO Investors]

- On Warren Buffett's Success: "Warren did better at investing because he really worked at it. He had unmatched mechanics and intense focus." — Source: [Observer]

- On Staying Grounded: "If somebody looks at me today and says 'You made a lot of money,' it wasn't always that way. I still ride subways!" — Source: [Musixmatch Podcasts]

- On Practicality: "I'm just practical. A survivor." — Source: [GAMCO Investors]

- On His Upbringing: "If you grew up in the Bronx, they clearly assumed you were a farmer." — Source: [Forbes]

- On Early Hustle: "I learned about stocks by hitchhiking from the Bronx to caddy for Wall Street specialists, listening to their conversations on the golf course." — Source: [Forbes]

Part 7: Media, Telecom, and Industry Consolidation

- On Content Value: "In a streaming world, live news and sports are the most valuable and resilient assets." — Source: [YouTube]

- On Consolidation Dynamics: "There are always winners, and there are always those who exit during industry contractions." — Source: [Futu]

- On Sports Franchises: "Sports teams are the ultimate scarcity assets, acting as classic PMV plays with extreme barriers to entry." — Source: [GAMCO Investors]

- On M&A Environments: "The M&A landscape is increasingly driven by financial engineering and shifting regulatory views on monopolies." — Source: [Futu]

- On Telecom Predictability: "Subscription models in telecom and cable provide the recurring, predictable cash flow that private buyers crave." — Source: [GAMCO Investors]

- On Hidden Media Assets: "Legacy media companies frequently hold real estate or local stations that the broader market completely ignores." — Source: [GAMCO Investors]

- On Content Demand: "The underlying human demand for entertainment grows consistently, even as the mechanisms for delivery undergo massive disruption." — Source: [YouTube]

- On Tech Obsession: "You can often find massive value in traditional broadcasting precisely because the market is entirely obsessed with technology." — Source: [GAMCO Investors]

- On The Streaming Wars: "Financial engineering will dictate the next wave of legacy media restructuring as companies fight for scale." — Source: [YouTube]

Part 8: Long-Term Thinking and Compounding

- On Decadal Returns: "The Dow will be the equivalent of 1 million in 40 years, and it was under 1,000 40 years ago. So, invest long term." — Source: [Morningstar]

- On Patience: "Let the gap between the public stock price and the private market value close over time." — Source: [GAMCO Investors]

- On Historical Perspective: "Looking back 40 years provides the exact mental perspective required to look forward 40 years." — Source: [Morningstar]

- On Filtering Noise: "Filter out the daily market fluctuations to focus strictly on the five- and ten-year structural outcomes." — Source: [GAMCO Investors]

- On Industry Tailwinds: "Allocate capital toward industries with multi-decade growth trajectories rather than chasing short-term fads." — Source: [Columbia Business School]

- On Compounding: "The ultimate goal of disciplined value investing is to allow your capital to compound uninterrupted." — Source: [GAMCO Investors]

- On Passing The Torch: "Sponsoring value investing education is essential to pass the Graham and Dodd framework to the next generation." — Source: [Columbia Business School]

- On The Persistence of Value: "The core principles of Graham and Dodd, appropriately adapted for modern markets, will always work." — Source: [GuruFocus]

- On The Long Game: "True wealth is built by combining a sound analytical framework with the patience to let business fundamentals play out." — Source: [GAMCO Investors]