Lessons from Michael Steinhardt

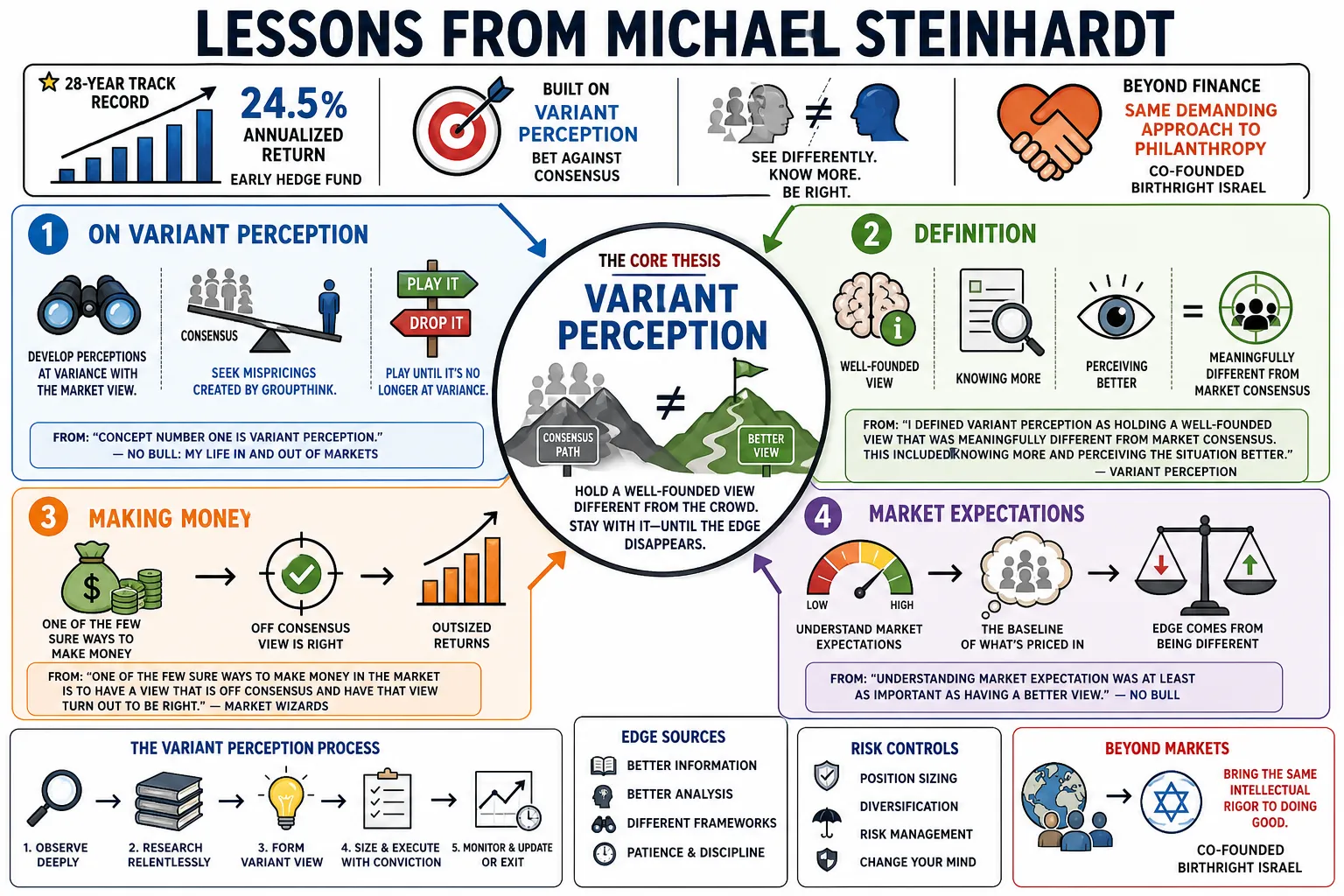

Michael Steinhardt ran an early hedge fund that posted a 24.5% annualized return over 28 years. His track record was built on "variant perception," a strategy of betting against the market consensus using superior information. After leaving finance, he brought that same demanding approach to his philanthropic work, co-founding Birthright Israel.

Part 1: The Core Philosophy of Variant Perception

- On Variant Perception: "Concept number one is variant perception. I try to develop perceptions that I believe are at variance with the general market view. I will play those variant perceptions until I feel they are no longer so." — Source: No Bull: My Life In and Out of Markets

- On Definition: "I defined variant perception as holding a well-founded view that was meaningfully different from market consensus. This included knowing more and perceiving the situation better than others did." — Source: Variant Perception

- On Making Money: "One of the few sure ways to make money in the market is to have a view that is off consensus and have that view turn out to be right." — Source: Market Wizards

- On Market Expectations: "Understanding market expectation was at least as important as, and often different from, fundamental knowledge." — Source: No Bull: My Life In and Out of Markets

- On Priced-In Views: "If your view is the same as everyone else's, it is already priced in. The only trades worth making are the ones where your analysis leads you to a conclusion the market has not yet reached." — Source: Quantified Strategies

- On Timing: "Variant perception is the art of knowing what others do not yet know and acting on it before they do." — Source: DayTrading.com

- On Recognizing Flaws: "The goal is to understand what the market expectation is and then have a well-founded reason to believe that expectation is wrong." — Source: MicroCapClub

- On Being Right: "Being different is not enough; you must be right. Being different and wrong is a recipe for disaster." — Source: Financhill

- On Consensus Thinking: "You must understand why the consensus believes what it does, and then find the specific data or insight that proves that consensus is flawed." — Source: Trade The Pool

- On Catalysts: "Always look for a trigger event that will force the market to realize its error and shift toward your variant view." — Source: Investing Caffeine

Part 2: Contrarianism and Market Extremes

- On Courage: "The hardest thing over the years has been having the courage to go against the dominant wisdom of the time, to have a view that is at variance with the present consensus and bet that view." — Source: AZQuotes

- On Discomfort: "When your views are truly contrarian, they are inevitably uncomfortable. Courage and the ability to withstand pain are required." — Source: Gracious Quotes

- On Euphoria and Fear: "Just as outright euphoria is often a sign of a market top, fear is for sure a sign of a market bottom." — Source: QuoteFancy

- On Emotional Extremes: "Time and time again... the extremes of emotion always appear, even among experienced investors." — Source: MicroCapClub

- On Identifying Bottoms: "When the world wants to buy only treasury bills, you can almost close your eyes and get long stocks." — Source: AZQuotes

- On Betting Against the Crowd: "The most important thing is to have a good sense of the consensus and then be willing to bet against it when you think it's wrong. But you better be sure." — Source: Investoquotia

- On Institutional Favorites: "Shorting institutional favorites—stocks with high valuations and universal praise—is profitable if you are willing to wait for the consensus to crack." — Source: MicroCapClub

- On Market Reality: "In an immediate emotional sense the market is always right so if you take a variant point of view you will always be bombarded for some time by conventional wisdom as expressed by the market." — Source: Market Wizards

- On Adaptation: "The markets are always changing, and the successful trader needs to adapt to these changes." — Source: QuoteFancy

Part 3: The Psychology of Trading and Mistakes

- On the Required Traits: "A good trader has to have three things: a chronic inability to accept things at face value, to feel continuously unsettled, and to have humility." — Source: Hedge Fund Alpha

- On Flexibility: "Good investing is a peculiar balance between the conviction to follow your ideas and the flexibility to recognize when you have made a mistake." — Source: AZQuotes

- On Early Lessons: "Make all your mistakes early in life. The more tough lessons early on, the fewer errors you make later." — Source: No Bull: My Life In and Out of Markets

- On Getting Smarter: "Smart investors get smarter with each passing mistake. Once a mistake has been committed and the losses incurred, the investor will resist the trap to the same mistake again." — Source: Hedge Fund Alpha

- On Opposing Traders: "I try to assume that the guy on the other side of a trade knows at least as much as I do. Always ask yourself: Why does he want to sell? What does he know that I don't?" — Source: Quantified Strategies

- On Confidence and Humility: "The balance between confidence and humility is best learned through extensive experience and mistakes." — Source: QuoteFancy

- On the Value of Errors: "One of the advantages of trading the way I do... is that I have made so many decisions and mistakes that it has made me wise beyond my years as an investor." — Source: No Bull: My Life In and Out of Markets

- On Truth Seeking: "You have to be intellectually honest with yourself and others. In my judgment, all great investors are seekers of truth." — Source: Gracious Quotes

- On Objective Measures: "The hard part is that the investor must measure himself not by his own perceptions of his performance, but by the objective measure of the market. The market has its own reality." — Source: Market Wizards

- On Capital Preservation: "When my fund suffered massive losses, I realized I had failed in the most fundamental tenet of money management: capital preservation." — Source: No Bull: My Life In and Out of Markets

Part 4: Information, Research, and Intuition

- On Information Gathering: "Be intellectually competitive. The key to research is to assimilate as much data as possible in order to be the first to sense a major change." — Source: AZQuotes

- On Incomplete Data: "Make good decisions even with incomplete information. You will never have all the information you need. What matters is what you do with the information you have." — Source: Gracious Quotes

- On Trusting Your Gut: "Always trust your intuition, which resembles a hidden supercomputer in the mind. It can help you do the right thing at the right time if you give it a chance." — Source: Investoquotia

- On the Nature of Intuition: "Intuition acts as a hidden computer that processes years of experience into a split-second feeling." — Source: No Bull: My Life In and Out of Markets

- On Macro Shifts: "Plow through the data so as to be able to sense a major change coming in the macro situation." — Source: Price Action Ninja

- On Pitching Ideas: "Analysts pitching an idea must state the idea, explain the consensus view, describe the variant perception, and identify the trigger event." — Source: Quantified Strategies

- On Trading as Discovery: "I do an enormous amount of trading, not necessarily just for profit, but also because it opens up other opportunities. I get a chance to smell many things. Trading is a catalyst." — Source: AZQuotes

- On Avoiding Comfort: "Comfort is the absolute enemy of returns. Maintain an environment of pressure to forge sharper decision-making." — Source: YouTube Interview Excerpt

- On Exiting Trades: "When the market begins to reflect your view, the variant edge is gone, and it is time to exit the trade." — Source: Trade The Pool

- On Depth of Knowledge: "Variant perception is the effort to become sufficiently knowledgeable about whatever the subject is, that at a time to be at variance from consensus." — Source: Grokipedia

Part 5: Navigating Risk and Market Danger

- On Danger: "My attitude has always been that to make money in the markets, you have to be willing to get in the way of danger." — Source: No Bull: My Life In and Out of Markets

- On Sizing: "Do not make small investments. If you are going to put money at risk, make sure the reward is high enough to justify the time and effort you put into the investment decision." — Source: Gracious Quotes

- On Pre-set Rules: "I don't have any rules about stops or objectives. I simply don't think in those terms." — Source: Market Wizards

- On Holding Periods: "Warren Buffett has said, 'If you are not willing to own a stock for 10 years, do not even think about owning it for 10 minutes.' The truth of the matter is, I have never owned a stock for 10 years, but I have had the unique and profitable experience of owning some very good companies for 10 minutes." — Source: MicroCapClub

- On Concentration: "If you have a real edge, scale it heavily. Small positions waste time and energy; if a concept is worth the risk, it’s worth a concentrated bet." — Source: Wharton Undergraduate Address

- On Pragmatism: "It is better to be liquid and enviably wealthy than to be stubbornly right and broke." — Source: MicroCapClub

- On Re-evaluating the Portfolio: "I tried to view the portfolio fresh every day... Irregularly, I would decide I did not like the portfolio writ large... I concluded we would be better off with a clean slate." — Source: No Bull: My Life In and Out of Markets

- On the Circle of Competence: "Stepping outside your circle of competence, such as moving from familiar U.S. equities into complex foreign bonds, often leads to failure." — Source: YouTube Interview Excerpt

- On Daily Discipline: "Maintain a savage focus on daily performance; down days in the market are no excuse for losing money." — Source: Varchev Finance

Part 6: Hedge Fund Management and Leadership

- On Becoming a Trader: "When I first got into this business in the late 1960s, I only had an analytical background... As our business grew, trading became more important. I became the trader from the firm, having had very little trading background." — Source: Market Wizards

- On Industry Purpose: "I thought there must be something more virtuous, more ennobling to do with one's life than make rich people richer." — Source: Hedge Fund Alpha

- On Fees and Pressure: "Now people are charging much fancier fees, and they do not make the same demands on themselves. I was always anxious that my fees were egregious and that I had to have the best performance in the world to justify them." — Source: Quantified Strategies

- On Industry Evolution: "In the 1950s and 1960s, the heroes were the long-term investors; today the heroes are the wise guys." — Source: Investing Caffeine

- On Market Brutality: "The market does not care about your feelings or your excuses. Success is purely a function of your ability to process information faster and more accurately than the person on the other side of the trade." — Source: No Bull: My Life In and Out of Markets

- On Trading Style: "Think like a long-term investor by analyzing fundamentals and macro trends, but execute like a short-term strategic trader." — Source: Varchev Finance

- On Agility: "Being a global macro pioneer requires shifting seamlessly between equities, bonds, currencies, and options based on where you see the greatest opportunity." — Source: Price Action Ninja

- On Winning: "The attraction to the hedge fund industry is fundamentally tied to an identity built on winning, making periods of loss deeply traumatic." — Source: YouTube Interview Excerpt

- On Walking Away: "The soul-crushing agony of losing creates permanent psychological scar tissue, a heavy price for playing at such a high level." — Source: YouTube Interview Excerpt

Part 7: Philanthropy and Jewish Identity

- On Birthright Israel: "I started Birthright to try to instill in the next generation of non-Orthodox Jews a sense of their Jewish heritage... The idea is to create, at this last moment in youth, a sense of Jewish identity." — Source: eJewish Philanthropy

- On True Threats: "In North America, the greatest threat to the Jewish people is not the external force of antisemitism, but the internal forces of apathy, inertia and ignorance of our own heritage." — Source: AZQuotes

- On Philanthropic Risk: "Most affluent Jews do not put innovation as the primary objective in their philanthropic world. They're comfortable with being honored and having their name on galas... but to experiment, to take risks... they don't do it so much in their Jewish philanthropy." — Source: Steinhardt Foundation

- On the Future: "I feel that there is a nobility in thinking about the Jewish future that I don't find in very many other places." — Source: Steinhardt Foundation

- On Education: "Our philanthropy must contend with Jewish pride and orient itself to a newly understood landscape... it is time to invest more seriously in educational endeavors that reinforce it and build upon it." — Source: Steinhardt Foundation

- On Secular Achievement: "Jews have accomplished so much, so inexplicably out of proportion to their numbers, in these 300 years, and it's one of the great failures of Jewish education that that's not focused on at all." — Source: ACJNA

- On Pride vs. Ritual: "Jewish pride is not about laying tefillin. In fact, it has nothing to do with Jewish spiritual devotion... most Jews are ambivalent about ritual, but they are passionate about accomplishment." — Source: Steinhardt Foundation

- On Israel: "Israel has become, for me, the substitute for religion... The modern state of Israel is the Jewish miracle of the 20th century, but it's the secular part of Israel that's the miracle." — Source: ACJNA

- On the Diaspora: "We are not Israel's saviors—if anything, we should think about what Israel can do to save us. Diaspora Jews are in a crisis, and Israel has a role to play in solving it." — Source: Substack

Part 8: Success, Failure, and The Meaning of Work

- On Career Choice: "Always make your living doing something you enjoy." — Source: No Bull: My Life In and Out of Markets

- On the Process: "I was happier when pursuing success than I was when savoring its fruits; the attraction, perhaps the addiction, was in the process, as much as in its end." — Source: Bookey App

- On Diversification: "Art is a form of asset. Hedge-fund managers who have made money fast should diversify into other areas." — Source: Hedge Fund Alpha

- On Personal Failure: "When your entire identity is built on winning, a severe market drawdown is not just a financial loss, but a deep personal failure." — Source: YouTube Interview Excerpt

- On Intensity: "Success requires an intensity that is impossible to sustain if you don't love the process." — Source: Wharton Undergraduate Address

- On Legacy: "As I wind down my philanthropic work, I am hopeful that others will carry the torch: a torch of Jewish pride, of peoplehood, of a deep connection between Israel and American Jewry, of learning and action." — Source: Gracious Quotes

- On Discipline: "Success requires the brutal discipline to maintain a variant perception and the stamina to endure extreme discomfort." — Source: YouTube Interview Excerpt

- On Arrogance: "Failure often stems from arrogance—stepping outside one's expertise—and the psychological exhaustion that comes from a life defined solely by the need to win." — Source: YouTube Interview Excerpt

- On Higher Purpose: "Transitioning away from finance is necessary when you recognize the need for a higher purpose beyond sheer accumulation." — Source: Hedge Fund Alpha