Nick Train is the co-founder of Lindsell Train and a British fund manager known for an extreme buy-and-hold approach to consumer staples and data franchises. He built his strategy on the belief that holding highly concentrated positions in durable, long-standing brands over decades is the most reliable way to generate returns. This profile catalogs his specific views on extreme patience, the value of un-replicable data, and the discipline required to endure periods of severe market underperformance.

Part 1: The Psychology of Patience and Optimism

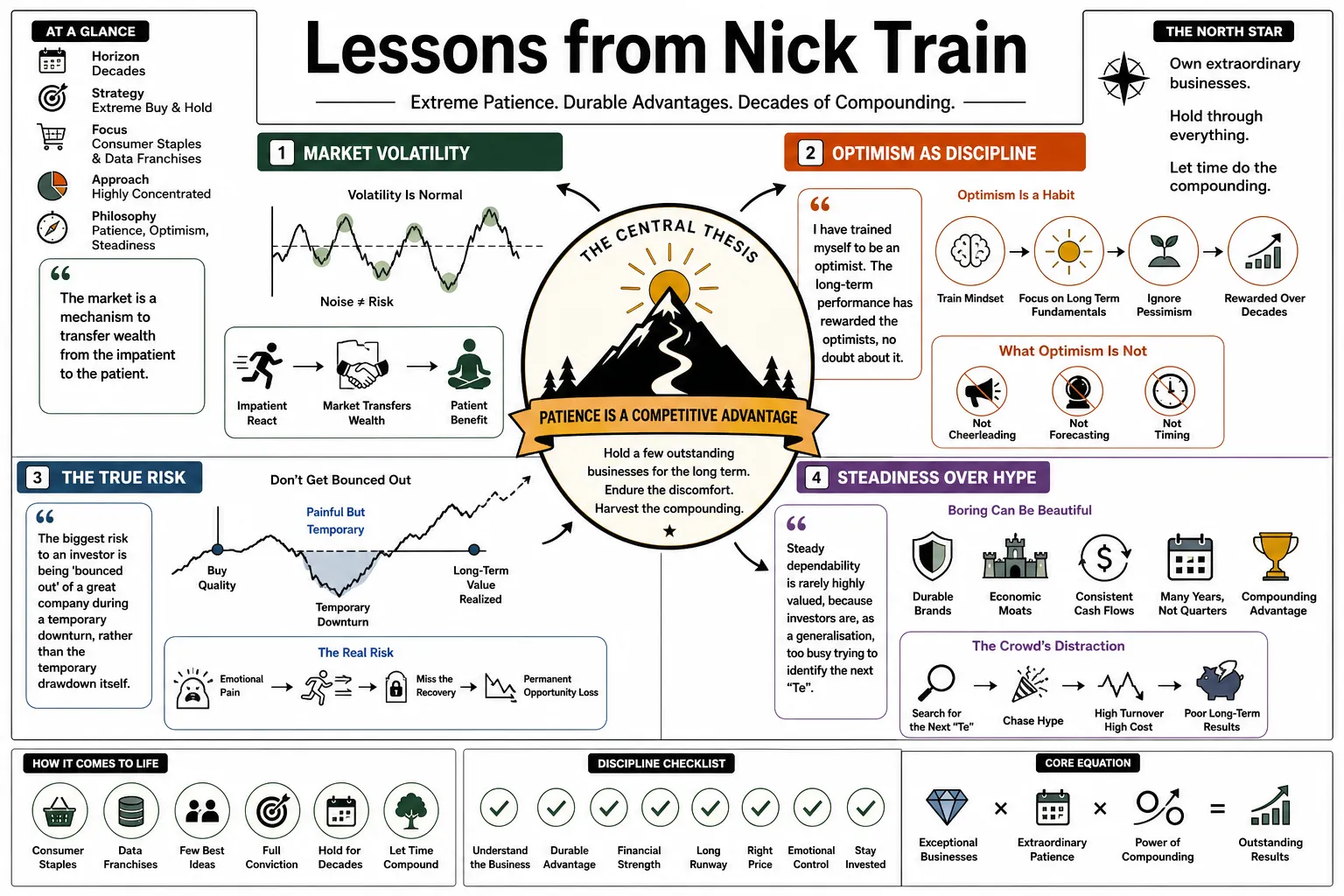

- On Market Volatility: "The market is a mechanism to transfer wealth from the impatient to the patient. We've always wanted to be on the right side of that trade." — Source: [Morningstar]

- On Optimism as Discipline: "I have trained myself to be an optimist. The long-term performance has rewarded the optimists, no doubt about it." — Source: [YouTube]

- On the True Risk: "The biggest risk to an investor is being 'bounced out' of a great company during a temporary downturn, rather than the temporary drawdown itself." — Source: [Trustnet]

- On Steadiness: "Steady dependability is rarely highly valued, because investors are, as a generalisation, too busy trying to identify the next Tesla or trying to time the next gyration of the economic cycle." — Source: [Interactive Investor]

- On Holding Periods: "Our favorite holding period is forever." — Source: [Behind the Balance Sheet]

- On Looking Forward: "Direct your feet to the sunny side of the street." — Source: [YouTube]

- On Market Predictions: "I will not make flippant or complacent predictions about prospects for Lindsell Train Limited, as we experience arguably the worst period of relative investment performance in our history." — Source: [Trustnet]

- On Frivolous Trading: "We will not take frivolous risks or indulge in long-term losing behaviour." — Source: [Trustnet]

- On the Compounding Effect: "At least part of your portfolio should be populated by these enduring assets. I promise you, there are times when that enduring value will protect your wealth." — Source: [Morningstar]

Part 2: Concentration and Portfolio Strategy

- On Wealth Creation: "In order to create wealth, you need to concentrate your portfolio. In order to protect wealth, you should diversify." — Source: [Morningstar]

- On Conviction: "We’ve chosen to concentrate the portfolio to try and maximize the returns, holding maybe 20 positions where the top 10 account for over 80% of assets." — Source: [Morningstar]

- On Taking Profits: "It can be very wrong to take a profit if by doing so you permanently reduce your interest in a great long-term investment. Share prices of the best companies double, then double again and again over time." — Source: [Trustnet]

- On Differentiation: "If you want different investment performance, you must invest differently." — Source: [Trustnet]

- On Active Management: "Active managers have to take some risk. The risk we’ve chosen to take is portfolio concentration. But if we do our job well, concentration on high-quality businesses." — Source: [Portfolio Adviser]

- On Turnover: "Every sale is, in my mind, a confession of error." — Source: [Morningstar]

- On the Goal of Equities: "We remain disciplined and serious in our efforts to invest in assets with the potential of protecting or enhancing the real, after-tax purchasing power of your savings." — Source: [Trustnet]

- On Doing Less: "We’d rather stick with Thomas Burberry’s invention of gabardine 130 years ago than try to guess the next major tech innovation." — Source: [Apple Podcasts]

- On Sticking to Your Circle: "We are envious of the people who make fortunes investing in tech. It’s just that we know we don’t have the critical ability to distinguish what’s going to last." — Source: [Apple Podcasts]

Part 3: The Power of "Immortal" Brands

- On Enduring Franchises: "Our focus is primarily on companies possessed of durable, preferably immortal, business franchises." — Source: [Morningstar]

- On Pricing Power: "If it tastes good, buy the shares." — Source: [Apple Podcasts]

- On Consumer Staples: "Investments in businesses that can compound steadily, like Heineken or Mondelez, remain valid and valuable portfolio constituents." — Source: [Trustnet]

- On Heritage Brands: "The consumer preference for a pint of Guinness and nothing else is an intangible asset that provides immense pricing power and resilience." — Source: [Portfolio Adviser]

- On Shifting Preferences: "That multi-decade shift in consumer preference away from higher calorie, less differentiated beer to premium spirits looks set to continue." — Source: [Portfolio Adviser]

- On Equities as Gilts: "We view these equities not as trading chips, but as irredeemable gilts with a variable coupon that grows over time." — Source: [Trustnet]

- On Un-replicable Assets: "The most valuable assets are often hard-to-replicate digital and brand-based franchises." — Source: [Morningstar]

- On Management: "There is almost no company we are invested in where I think we are qualified to tell current management how to run the business better." — Source: [Portfolio Adviser]

- On Brand Loyalty: "The best companies build a deep emotional connection with their customers, creating a moat that competitors struggle to cross." — Source: [Interactive Investor]

- On Long-Term Value: "At least part of your portfolio should be populated by these enduring assets." — Source: [Morningstar]

Part 4: Dealing with Underperformance and Mistakes

- On Accountability: "The underperformance is mortifying for me and my colleagues. My recent record was terrible." — Source: [Morningstar]

- On Apologies: "I sort of feel I’m running out of ways to say sorry." — Source: [Morningstar]

- On Staying the Course: "We acknowledge the strategy has not been working for too long a time. However, we believe that dismantling the portfolio and selling out of companies of the calibre we own at this juncture would not be in the best interest of investors." — Source: [Portfolio Adviser]

- On Missing Rallies: "It is so galling that in a year when the UK stock market has made some tangible returns I have been unable to participate." — Source: [Portfolio Adviser]

- On Disappointing Investors: "Investors will be bitterly disappointed by recent performance, but the portfolio strategy remains the same." — Source: [Morningstar]

- On Sector Avoidance: "I think I can say categorically, at least as long as I am responsible, we won't own anything in the oil sector, even though BP and Shell have been very strong performers." — Source: [Morningstar]

- On When to Sell: "We only sell if the investment thesis is broken, rather than due to short-term price volatility." — Source: [Investors Chronicle]

- On Committing to Strategy: "I can't offer anything more than blood, sweat, and tears." — Source: [Morningstar]

- On Selling Great Companies: "Dismantling the portfolio at this juncture would not be in the best interest of investors." — Source: [Portfolio Adviser]

Part 5: The Value of Data and Artificial Intelligence

- On the Power of Data: "Constantly replenishing, proprietary business data at scale is right at the heart of the competitive advantages of the companies we have chosen to invest in." — Source: [Portfolio Adviser]

- On Tech Winners: "We absolutely know that if we are to meet our clients' expectations in coming years, we will need to participate in more tech winners, existing and new holdings." — Source: [Trustnet]

- On Tech Valuations: "We also know that some tech stocks will never justify their current market capitalisations." — Source: [Trustnet]

- On AI Beneficiaries: "Artificial Intelligence is a massive opportunity for older companies with proprietary data, such as the London Stock Exchange Group and Sage, allowing them to become more valuable to their customers." — Source: [Trustnet]

- On the True Moat in AI: "While AI models are powerful, they require high-quality data to be effective. Companies that own exclusive, proprietary data hold the ultimate competitive advantage." — Source: [Interactive Investor]

- On AI Enhancers: "Because our companies own the raw material, they are better positioned to build their own AI tools than a generic AI startup is to recreate their data sets." — Source: [Morningstar]

- On Generational Opportunities: "Companies owning massive, proprietary data sets have a generational opportunity to accelerate growth by applying AI tools." — Source: [Trustnet]

- On Experian's Moat: "Experian updates its data a billion times a month, creating a barrier to entry that is nearly impossible for a new competitor to match." — Source: [Trustnet]

- On Avoiding the SaaSpocalypse: "The indiscriminate sell-off of these data owners is a once-in-a-decade opportunity to buy world-class assets at the wrong price." — Source: [Morningstar]

Part 6: The UK Market Opportunity

- On UK Valuation: "Even I’m finding things that are getting harder to resist. At some point this is going to have been extraordinary value creating." — Source: [YouTube]

- On the Value Gap: "We have been pointing out for months that there was a deep value gap between UK and US growth stocks." — Source: [Portfolio Adviser]

- On UK AI Potential: "How many global asset allocators would think to look at the UK for AI? I’m going to guess not many, but I do wonder whether those sorts of companies have a credible proposition." — Source: [YouTube]

- On Market Composition: "The London market lacks exposure to the wealth-creating themes like big tech driving the global economy." — Source: [Morningstar]

- On Speculative Mania: "UK growth stocks had not obviously been caught up in a speculative mania." — Source: [Portfolio Adviser]

- On Global Asset Allocation: "The UK market offers a once-in-a-generation opportunity to buy global growth businesses at a discount." — Source: [Interactive Investor]

- On Macro Worry: "Worrying about the big macro issues is a waste of time." — Source: [Apple Podcasts]

- On Youth Investing: "I wish young people would ditch sports betting in favor of having a flutter on the stock market, as equity investment is a more productive way to build long-term wealth." — Source: [Apple Podcasts]

- On Long-term UK Returns: "Over 24 years, Finsbury's net asset value total return has compounded at 9% per annum, and the FTSE All-Share Index has compounded at just over 5% per annum." — Source: [Morningstar]

- On Patience in the UK: "With a concentrated portfolio of wealth-creating businesses, we have very materially outperformed if you have had the patience." — Source: [Morningstar]

Part 7: On Specific Holdings (Diageo, RELX, Manchester United)

- On RELX's Potential: "If RELX can fulfil the promise of its investment in AI-enhanced tools, maybe RELX can become the biggest company in the UK stock market." — Source: [Behind the Balance Sheet]

- On RELX as a Multi-bagger: "RELX is a multi-bagger that proves the value of long-term patience, climbing from the bottom half of the FTSE 100 to the top 10." — Source: [Trustnet]

- On Manchester United: "Manchester United is a unique global content and entertainment franchise, making its intellectual property exceptionally valuable in the battle for live sports broadcasting rights." — Source: [Portfolio Adviser]

- On the United Buyout: "We were disappointed that a full buyout did not occur, as we had hoped to crystallize a big premium." — Source: [Portfolio Adviser]

- On Nintendo: "Nintendo is the Disney of Japan, owning some of the most sought-after entertainment content on the planet." — Source: [Interactive Investor]

- On Nintendo's Longevity: "I am confident gamers in 2040 will still be looking forward to the latest version of Mario Kart." — Source: [ShareScope]

- On Hardware Cycles: "We ignore the cyclical nature of console hardware launches, focusing instead on Nintendo's massive library of beloved intellectual property." — Source: [Interactive Investor]

- On Diageo: "The Americans have discovered Guinness!" — Source: [Trustnet]

- On Diageo's Brands: "Diageo’s portfolio represents exceptional global brands that are nearly impossible to replicate." — Source: [Investment Week]

- On Adding to Diageo: "The price dip is a once-in-a-generation opportunity to add to a high-quality business." — Source: [YouTube]

Part 8: Influences, Reading, and the Investment Profession

- On The Money Masters: "Reading John Train's book was a profound inflection point. Before that, I considered myself a gun-slinging trader who treated stocks like trading chips." — Source: [Trustnet]

- On Masterly Inactivity: "The book taught me masterly inactivity, the discipline to hold great companies for decades rather than trading frequently." — Source: [Trustnet]

- On Samuel Johnson: "Men more frequently require to be reminded than taught." — Source: [Trustnet]

- On the Wisdom of Equities: "Jeremy Siegel's 'Stocks for the Long Run' is required reading for our team because it provides the data-driven case for equities as the best long-term asset class." — Source: [Trustnet]

- On Sticking to Principles: "Successful investing is not about finding new secrets, but about having the discipline to stick to timeless principles found in classic books." — Source: [Trustnet]

- On Warren Buffett: "Buffett convinced me to stop trying to time the market and instead focus on eternal franchises with long-term compounding potential." — Source: [Trustnet]

- On the Profession: "We run a radically differentiated strategy in a world dominated by index huggers." — Source: [YouTube]

- On The Growth Trap: "Jeremy Siegel's 'The Future for Investors' shows why older, established companies often outperform new ones." — Source: [Trustnet]

- On Complexity: "Geoffrey West's 'Scale' provides a scientific look at the growth and survival of complex organisms and corporations, which applies directly to how we view enduring businesses." — Source: [Trustnet]