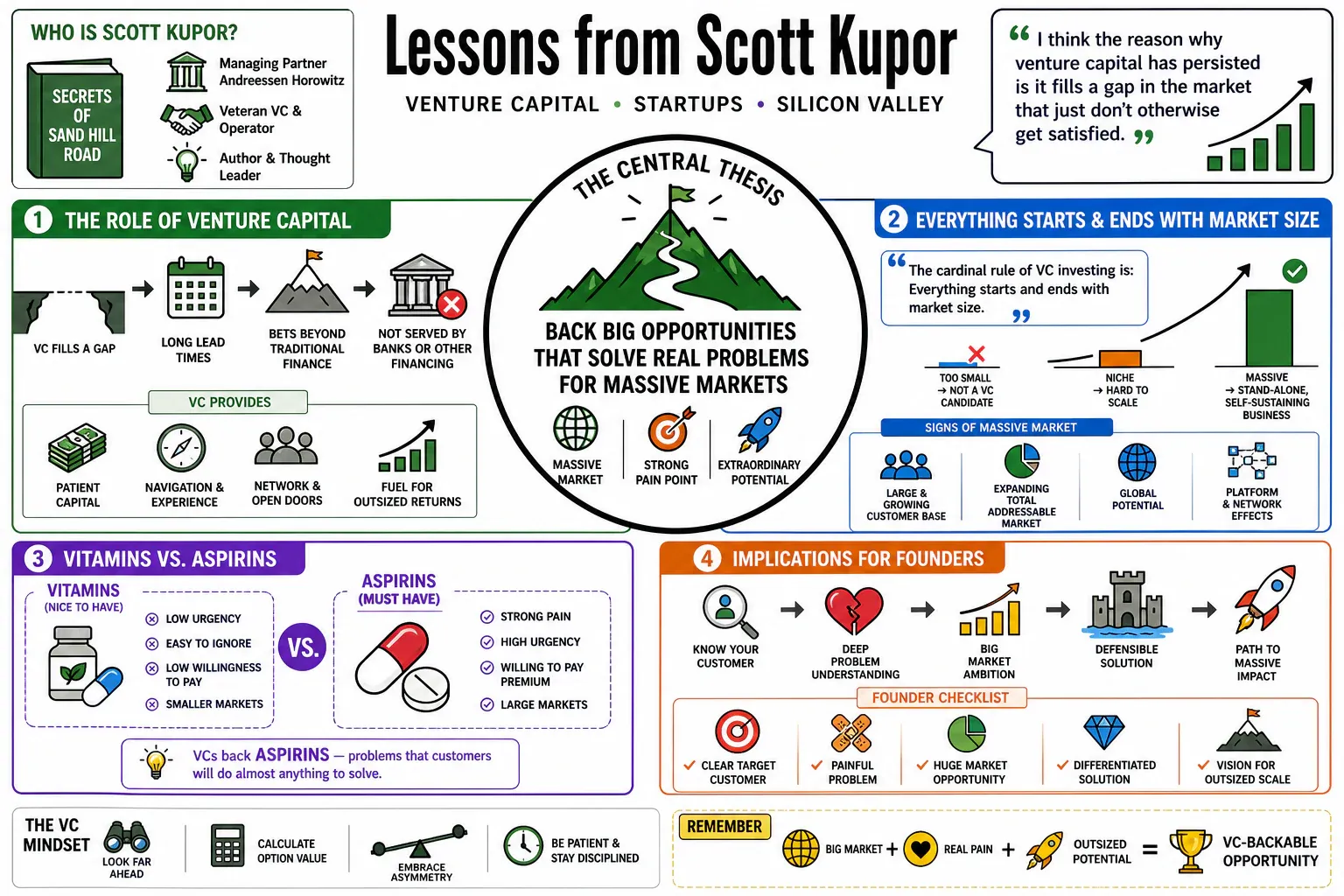

Scott Kupor, a managing partner at Andreessen Horowitz and author of "Secrets of Sand Hill Road," has shared a wealth of knowledge over the years on venture capital, startups, and the dynamics of Silicon Valley.

On Venture Capital and Investment Philosophy

- On the role of venture capital: "I think the reason why venture capital has persisted is it fills a gap in the market that just don't otherwise get satisfied...for things where you have long lead times, you have people really trying to take on a risk that is just well beyond what a bank or other financing source can do."[1][2]

- The importance of market size: “The cardinal rule of VC investing is: Everything starts and ends with market size. No matter how interesting or intellectually stimulating your business, if the ultimate size of the opportunity isn't big enough to create a stand-alone, self-sustaining business of sufficient scale, it may not be a candidate for venture financing.”[3]

- Vitamins vs. Aspirins: VCs are looking for startups that solve a strong pain point. As Kupor, referencing his partner Ben Horowitz, puts it, "Vitamins are nice to have...If you have a headache, though, you'll do just about anything to get an aspirin! They solve your problem and they are fast acting. Similarly, products that often have massive advantages over the status quo are aspirins; VCs want to fund aspirins.”[3][4]

- The power of software: Echoing the Andreessen Horowitz mantra, Kupor emphasizes the pervasive impact of software across industries. "We've been investing on this theme called 'Software is eating the world' for a long time," he says, noting its influence on entertainment, music, financial services, and potentially healthcare and education.[5][6]

- Focus on the magnitude of wins: In venture capital, success isn't about the percentage of successful investments. "Everything here is about the magnitude of the winners."[1][2]

- The changing landscape of VC: Kupor notes that access to capital is no longer a differentiator for VC firms. "Money is free flowing, so it is definitely a commodity and no longer a scarce resource."[7] This has led firms like Andreessen Horowitz to offer more services to portfolio companies.[6]

- Companies are staying private longer: "Historically, companies would go public about five to six years after they were founded. However, Kupor said this pattern has changed in recent decades. 'The trend we see today, which I think is a long-term structural change, is companies staying private for 10 or 12 years.'"[5]

- The democratization of capital: Kupor predicts a future where venture capital is more geographically distributed. "In general, the spoils of venture capital have not been well distributed geographically...I actually think if we're sitting here 10 or 20 years from now — I would be shocked if we don't see better democratization of access to capital."[5]

Advice for Founders: Pitching and Fundraising

- Don't tell VCs what you think they want to hear: "I think the biggest mistake that we see when people pitch to us is they tell us what they think we want to hear."[8] Instead, demonstrate a deep understanding of your industry.

- Have strong opinions, weakly held: VCs appreciate founders with conviction, but also the ability to adapt. "We prefer people with ideas that are strongly imagined but weakly held...your ability to incorporate feedback reasonably over time with more data points is a really important part of what makes entrepreneurs successful."[3][6]

- Focus on the big vision, not the exit: A red flag for Kupor is when founders immediately talk about potential acquirers. "They say that sometimes because they think we want to hear that, because they think we want to de-risk the opportunity...we are risk-taking people."[6]

- The "Idea Maze": VCs will rigorously test a founder's idea. "This is where entrepreneurs are quizzed about the genesis of their idea, why they believe it will translate into a successful product, and the insights and market data that have shaped their ideation process."[9]

- Be resourceful with your intro: A warm introduction to a VC is more effective than a cold outreach. "A good way to demonstrate that skill set is by being resourceful and figuring out a way to get a warm intro to a VC rather than reaching out cold."[10]

- Five pitch essentials: As outlined in his book, the key elements of a pitch are: market size, the team, the product, the go-to-market strategy, and the financing plan.[10]

- Raise enough money to make progress: When raising a round, secure enough capital to significantly de-risk the business for the next set of investors. "Your B round investor will pay you for your success in the form of higher valuation."[11]

- Be honest about struggles: If you're having trouble raising, "be honest with yourself and the VC in order to have a real conversation on why the business may not be working."[10]

- Understand VC fund cycles: "If you get an investment from the fund in its early days, the VC will be under a lot less pressure to return capital to its Limited Partners (LPs). If you are getting funded in the later part of that fund's lifecycle, then the pressure for a near-term exit for the VCs will be immense."[11]

- Avoid a high valuation with little runway: "The worst mistake you can make as an entrepreneur is to take a small amount of money at a very high valuation. This ultimately sets an unrealistically high marker without giving yourself the runway needed to clear that hurdle."[10]

On Building a Company

- The importance of a strong team: "Success in the startup world is not just about the idea; it's about execution. Kupor stresses the importance of assembling a strong and complementary team."[12]

- Founder-market fit: VCs are trying to answer a fundamental question: "Why back this founder against this problem set versus waiting to see who else may come along with a better organic understanding of the problem?"[4]

- The value of the startup experience: "There's no substitute for understanding the company building process...One is the pure learning of what it is like to raise money, to go through hypergrowth, and in some cases hypercontraction."[6]

- The "Live to fight another day" mantra: This is a crucial mindset for startups navigating the inevitable challenges.[4]

- The delusional nature of entrepreneurship: "You have to be partly delusional to start a company given the prospects of success and the need to keep pushing forward in the wake of the constant stream of doubters."[4]

- Stock vesting is key: This is a critical tool to align the incentives of founders and early employees with the long-term success of the company.[11]

On the Relationship Between Founders and VCs

- It's a long-term marriage: "That means sharing equity ownership with a VC, sharing board control and governance, and ultimately entering into a marriage that is likely to last for about the same time as the average 'real' marriage (8–12 years)."[3]

- Good VCs provide more than money: "Good VCs help entrepreneurs achieve their business goals by providing guidance, support, a network of relationships, and coaching."[9]

- The value of a VC's network: Entrepreneurs should "leverage the expertise and networks of their investors to accelerate the growth of their startups."[12]

- Alignment of incentives is crucial: "Key factors in determining if venture capital is appropriate for your business include, alignment from an incentives perspective with the capital that your considering taking to the company."[10]

- Transparency builds trust: "Venture capital thrives on clear communication between founders and investors."[13]

On the Broader Tech and Economic Landscape

- Waves of technological innovation: "Every 10 to 15 years we tend to have some major technological innovation that basically drives the large...accretion of...investment opportunity."[14]

- The global nature of venture capital: "US venture dollars used to be 90% of global dollars. Today that's about 50%."[6]

- The impact of AI: Kupor sees AI as a critical future component of both the private and public sectors.[15]

- Billion-dollar companies are the new benchmark: "I hate to say it, but billion-dollar companies are kind of table stakes at this point in time."[1]

From his Time in Government (as former OPM Director)

- Creating a high-performance culture: Kupor aimed to "attract and retain the best and the brightest" and ensure "real accountability for outcomes" in the federal workforce.[16]

- The importance of operational efficiency: "A lot of the problems...we have with government in my mind stem from the fact that you know kind of often times we really think about headcount as the logical solution to many problems."[16]

- Culture is what happens when the leader isn't there: Quoting Ben Horowitz, Kupor emphasized the need for a strong organizational culture.[13]

- Incentives drive organizations: "Organizations are made up of people. And people respond to incentives."[15]

Other Notable Learnings

- On the importance of storytelling: "The most compelling pitches that we see are those individuals who can really create a vision and distill that vision and tell it in a way that will cause people...to do maybe even irrational things.”[3]

- The process of navigating the "idea maze" is a better predictor of success than the idea itself.[4]

- VCs are not looking to de-risk investments at the individual company level; they manage risk at the portfolio level.[8]

- The entrepreneur is in a more privileged position today in terms of capital raising than 15 years ago.[14]

- Good VCs know their limits and avoid giving advice on topics outside their expertise.[4]

- Ultimately, entrepreneurs and employees build iconic companies, with VCs playing a supportive role.[4]

- A company should probably be able to sustain at least a couple billion-dollar market capitalization before going public.[6]

- It's cheaper than ever to start a company, but more expensive than ever to scale one.[7]

- VCs are looking for founders with a sense of vision, purpose, and a willingness to "walk through walls."[10]

- Narrative and brand building are important for both entrepreneurs and VCs.[12]

- When things go wrong, a founder's ability to be resourceful is a key indicator of their potential.[10]

- The decision to take VC money means playing by a specific set of rules regarding growth and exit expectations.[3]

- VCs look for teams that are uniquely equipped to solve a particular problem.[4]

Sources