Lessons from Terry Smith

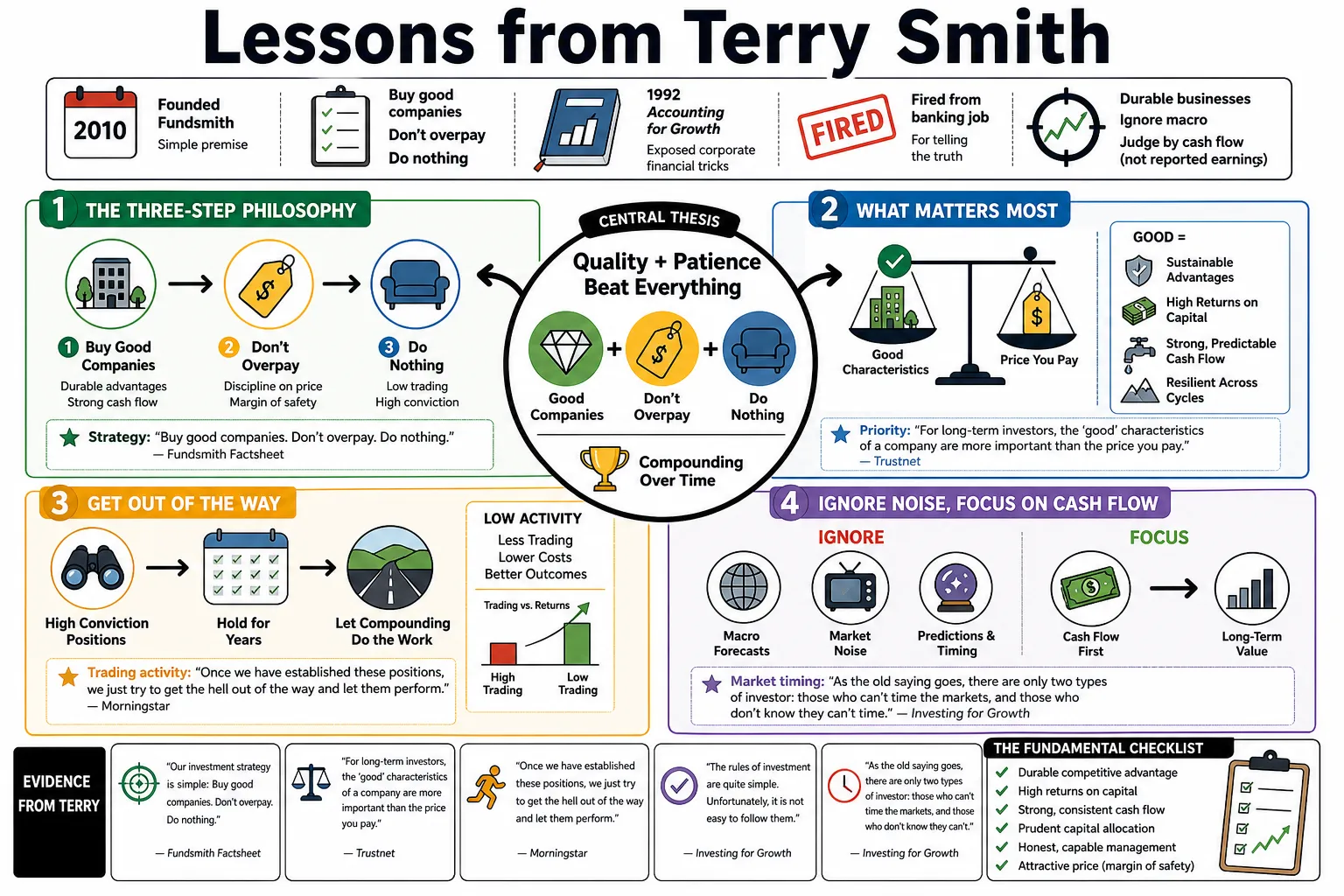

Terry Smith founded Fundsmith in 2010 on a simple premise: buy good companies, don't overpay, and do nothing. Long before that, he was fired from his banking job for exposing widespread corporate financial tricks in his 1992 book, Accounting for Growth. His approach relies entirely on identifying durable businesses, ignoring macroeconomic forecasts, and judging companies strictly by cash flow rather than reported earnings.

Part 1: The Three-Step Philosophy

- On strategy: "Our investment strategy is simple: Buy good companies. Don’t overpay. Do nothing." — Source: Fundsmith Factsheet

- On priority: "For long-term investors, the 'good' characteristics of a company are more important than the price you pay." — Source: Trustnet

- On trading activity: "Once we have established these positions, we just try to get the hell out of the way and let them perform." — Source: Morningstar

- On simplicity: "The rules of investment are quite simple. Unfortunately, it is not easy to follow them." — Source: Investing for Growth

- On market timing: "As the old saying goes, there are only two types of investor: those who can't time the markets, and those who don't know they can't time the markets." — Source: The Economic Times

- On patience: "The most challenging part of an investment strategy is to have the patience of sitting and doing nothing when the investment climate is not conducive for trading." — Source: The Economic Times

- On business ownership: "We seek to buy and hold shares in good companies... we want to hold them forever." — Source: Fundsmith Owner's Manual

- On complex strategies: "If you need a computer model to tell you if a business is a good investment, it's probably not." — Source: Interactive Investor

- On long-term focus: "Investment is a test of the endurance of investors and the winners are the ones who find a good strategy or fund and stick with it." — Source: The Economic Times

- On judging performance: "To assess an investment strategy or a fund, you need to see its results across a full economic cycle with both bull and bear markets." — Source: The Economic Times

Part 2: Defining a Good Company

- On value creation: "Good companies create value by consistently earning returns on capital that exceed their cost of capital." — Source: Substack

- On high returns: "Over the long term, it’s hard for a stock to earn a much better return than the business which underlies it earns." — Source: ShareScope

- On mathematical certainty: "If the business earns 6% on capital over 40 years... you’re not going to make much different than a 6% return. If a business earns 18%... you’ll end up with a fine result." — Source: ShareScope

- On intangibles: "The best defenses against competition are intangible assets: brands, patents, licenses, and installed bases of equipment." — Source: Fundsmith Owner's Manual

- On capital destruction: "Bad companies destroy value by earning returns on capital that are lower than their cost of capital." — Source: Substack

- On predictability: "Rather than seeking superior portfolio performance by chasing high-risk stocks, investors should seek out 'boring' quality companies, which have predictable returns." — Source: Business Insider

- On consumer staples: "Companies that make everyday, small-ticket, repeat-purchase items are generally far more predictable and resilient than those making large, one-off purchases." — Source: Financial Times

- On innovation vs distribution: "It is much easier to sell a new product through an existing, dominant distribution network than it is to build a new distribution network for a novel product." — Source: Fundsmith Annual Letter 2018

- On gross margins: "Gross margin is a good protection against inflation... companies with high returns and gross margins require less capital to maintain their operations." — Source: Medium

- On leverage: "We avoid companies that require significant borrowing to generate their returns. Debt introduces an element of fragility that we do not want." — Source: Fundsmith Owner's Manual

Part 3: Valuation and Price

- On the Greater Fool theory: "You can't play 'greater fool theory', in which you knowingly overpay for the shares, hoping that a greater fool will buy them off you at an even more egregious valuation." — Source: Business Insider

- On valuation metrics: "Price-to-earnings ratios are often misleading because earnings are highly manipulable. We prefer to look at free cash flow yields." — Source: Investing for Growth

- On fair prices: "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price." — Source: Trustnet

- On overpaying: "We don't seek to overpay but it's a much less important characteristic than a company being 'good'." — Source: Trustnet

- On initial yield: "The dividend yield at the time of purchase is largely irrelevant if the company cannot grow its cash flow over time." — Source: Fundsmith Annual Letter 2016

- On mean reversion: "Cheap, low-quality companies may revert to the mean, but high-quality companies with durable moats can defy mean reversion for decades." — Source: Financial Times

- On deep value investing: "Buying a bad business because it looks cheap is like picking up a cigar butt off the street for one last puff—it might be free, but it's deeply unpleasant." — Source: The Telegraph

- On buying opportunities: "The best time to buy shares in good companies is when they are facing temporary, solvable problems that the market has mistaken for permanent impairment." — Source: Interactive Investor

- On growth vs value: "The distinction between value and growth is false. Growth is simply a component of value—usually a positive one, but sometimes negative if the return on capital is poor." — Source: Fundsmith Annual Letter 2019

- On long-term compounding: "If you pay an expensive-looking price for a business that earns 18% on capital over 30 years, you will still end up with a very satisfactory result." — Source: ShareScope

Part 4: The Virtues of Inactivity

- On the urge to act: "In investing, doing nothing is often the hardest action to take, but it is frequently the most profitable." — Source: Morningstar

- On portfolio turnover: "High portfolio turnover is the enemy of the investor. It incurs transaction costs and taxes, and it usually means the manager has no conviction." — Source: Fundsmith Owner's Manual

- On transaction costs: "The more you trade, the more you pay the brokers and the taxman, and the less you keep for yourself." — Source: The Telegraph

- On boredom: "If you find investing exciting, you are probably doing it wrong. Good investing should be boring." — Source: Business Insider

- On rebalancing: "We do not automatically rebalance the portfolio. Selling your winners to buy more of your losers is like cutting the flowers to water the weeds." — Source: Fundsmith Annual Letter 2014

- On checking stock prices: "Watching your portfolio daily is a recipe for anxiety and bad decision-making. Check it rarely." — Source: Financial Times

- On news flow: "Most financial news is noise designed to make you act. Ignoring it is a competitive advantage." — Source: Investing for Growth

- On the difficulty of holding: "Everyone wants to know what to buy and what to sell. Almost no one asks what they should just hold." — Source: Interactive Investor

- On compounding: "To benefit from the magic of compounding, you must first survive, and then you must not interrupt the process unnecessarily." — Source: Fundsmith Annual Letter 2020

Part 5: Accounting and Cash Flow

- On accounting rules: Comparing British and US accounting rules in 1992, he noted: "Better yes, good no." — Source: The Guardian

- On earnings vs cash: "Earnings are an opinion, but cash is a fact." — Source: Accounting for Growth

- On paying bills: "Cash is the only thing you can pay the bills with." — Source: The Investors Podcast

- On creative accounting: "Many companies struggle with cash flow rather than profitability and, in some cases, use deliberately misleading accounting techniques." — Source: MarketScreener

- On cash conversion: "We seek to buy companies which deliver high returns on capital in cash." — Source: The Investors Podcast

- On share buybacks: "Share buybacks only create value if the shares are undervalued and there is no better use for the cash which would generate a higher return." — Source: Business Insider

- On depreciation: "Depreciation is a real cost. Anyone who tells you to look at EBITDA is either trying to fool you or fooling themselves." — Source: Fundsmith Annual Letter 2017

- On capital expenditure: "Companies that have to constantly reinvest heavily just to stand still are poor investments, no matter what their stated earnings are." — Source: Investing for Growth

- On financial camouflage: "The main purpose of a company's annual report often seems to be to conceal the true economic reality of the business from its owners." — Source: Accounting for Growth

Part 6: Inflation and Resilience

- On macroeconomic forecasts: "Macro views and developments have no bearing on our strategy." — Source: The Investors Podcast

- On controlling the controllable: "I waste little or no time trying to guess what will happen to factors I cannot control or predict and deploy most of my time and effort on things I can control." — Source: The Investors Podcast

- On the nature of inflation: "Trying to light a bonfire with gasoline... you can go from no fire to a loud 'Whoosh!' and find that you have also set fire to the garden fence." — Source: The Investors Podcast

- On corporate profit: "The initial impact of inflation is not on consumer prices, but on company profits." — Source: The Investors Podcast

- On pricing power: "The defining characteristic of a great company is the ability to raise prices without losing customers to competitors." — Source: Fundsmith Annual Letter 2022

- On input costs: "If you own shares in companies during a period of inflation, it is better to own those with high returns and gross margins." — Source: Medium

- On capital light models: "In inflationary times, asset-heavy businesses suffer because the cost of replacing their equipment rises. Asset-light businesses are largely insulated." — Source: Financial Times

- On interest rates: "We don't buy banks because they are too highly leveraged and too reliant on forecasting interest rates, which no one can do consistently." — Source: Fundsmith Annual Letter 2011

- On market panics: "Volatility is not risk. A permanent loss of capital is risk. Volatility is simply the price of admission for long-term equity returns." — Source: Trustnet

Part 7: Indexing and the Fund Industry

- On passive investing dynamics: "Essentially, index investing is nothing more than momentum investing, which means you invest in companies that are performing very well at the time." — Source: Interactive Investor

- On market distortions: "The increasing proportion of equities held by index funds are invested without any regard to the quality or valuation of the shares bought, which produces dangerous distortions." — Source: The Motley Fool

- On systemic risk: "The shift into index funds is laying the foundations of a major investment disaster." — Source: The Motley Fool

- On the passive paradox: "The best equity investment for most investors most of the time is an index fund because of its low cost and outperformance of most active fund managers." — Source: The Motley Fool

- On active manager fees: "The fund management industry is the only industry where you get paid regardless of whether you deliver the service you promised." — Source: The Telegraph

- On closet indexing: "If a fund has 100 or more stocks in it, it is a closet index tracker charging active management fees." — Source: Fundsmith Owner's Manual

- On benchmark hugging: "We do not manage our portfolio with reference to any index weightings. If we don't like a sector, we simply won't own it." — Source: Fundsmith Annual Letter 2015

- On performance fees: "Performance fees are an asymmetrical option. The manager takes a cut of the upside but doesn't write a cheque to the investors when the fund falls." — Source: Investing for Growth

- On feedback loops: "Index investing is a self-reinforcing feedback loop which will operate until it doesn't." — Source: The Motley Fool

Part 8: Technology and Disruption

- On the AI boom: He recently described the AI boom as the largest speculative craze in history, warning about unverified capital expenditure. — Source: Financial Times

- On defining tech: "I don't think people think, 'oh technology'... what drives those companies is not technology, it's employment in payroll, or business in accounting... social media and digital advertising." — Source: The Investors Podcast

- On hyperscalers: "It is far from clear whether the massive capital expenditure by hyperscalers on AI infrastructure will yield the expected returns on capital." — Source: Fundsmith Annual Letter 2024

- On tech cyclicality: "Large technology companies have in a sense become victims of their own success... they have become inevitably more cyclical." — Source: Trustnet

- On tech disruption: "We generally avoid companies engaged in rapid technological innovation, as the ultimate winners are almost impossible to predict at the outset." — Source: Fundsmith Owner's Manual

- On software as a service: "The best software businesses are essentially subscription models where the customer is locked in by high switching costs and the mission-critical nature of the product." — Source: Fundsmith Annual Letter 2020

- On established networks: "Dominant platforms benefit from powerful network effects, where the value of the service increases for everyone as more users join." — Source: Investing for Growth

- On Meta and Alphabet: "While classified as tech, their actual business model is simply selling advertising, which makes them highly sensitive to the broader economic cycle." — Source: Trustnet

- On investing in innovation: "It is rarely the pioneer who captures the economic value of an innovation; it is usually the company that standardizes and scales it." — Source: Fundsmith Annual Letter 2019