Tom Gayner is the CEO of Markel Group, a financial holding company often compared to Berkshire Hathaway for its disciplined approach to capital allocation. Over his decades-long career, he has built a reputation as a thoughtful value investor who prioritizes long-term compounding, high-integrity management, and acquiring private businesses with a promise to never sell them. This collection catalogs his practical insights on evaluating companies, managing temperament, and the structural advantages of patience.

Part 1: The Four Pillars of Investing

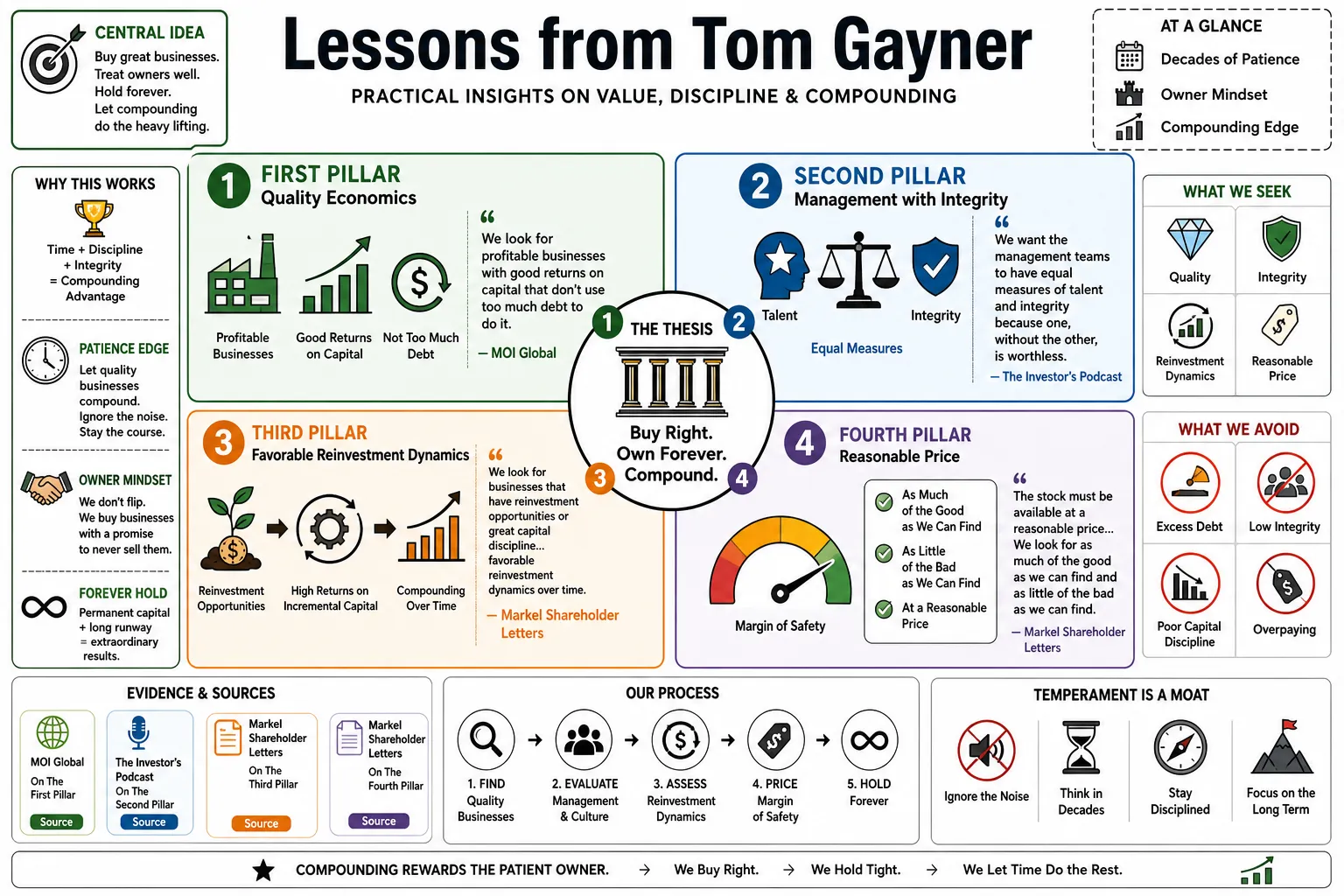

- On The First Pillar: "We look for profitable businesses with good returns on capital that don’t use too much debt to do it." — Source: MOI Global

- On The Second Pillar: "We want the management teams to have equal measures of talent and integrity because one, without the other, is worthless." — Source: The Investor's Podcast

- On The Third Pillar: "We look for businesses that have reinvestment opportunities or great capital discipline... favorable reinvestment dynamics over time." — Source: Markel Shareholder Letters

- On The Fourth Pillar: "The stock must be available at a reasonable price... We look for as much of the good as we can find and weigh that against what we have to pay for it." — Source: Invest Like the Best

- On Paying a Fair Price: "The long term returns should be similar to the underlying growth in intrinsic value of the company itself... We are willing to pay a 'fair' price for a great business." — Source: GuruFocus

- On Profit Predictability: "Deciding if a business will produce profits over time is much easier than predicting when it will produce profits." — Source: Substack

- On Capital Discipline: "If a business lacks internal reinvestment opportunities, look for capital discipline—the ability to smartly allocate cash through dividends or share repurchases." — Source: Hedge Fund Alpha

- On Avoiding Leverage: "A business achieving good returns on capital must do so without heavy debt, as excessive leverage drastically reduces the margin of error." — Source: Novel Investor

- On Evolution of Style: "Moving from strict quantitative cigar-butt investing toward quality and durability is necessary because time is the friend of the wonderful business." — Source: Boyar Value Group

Part 2: Capital Allocation and Strategy

- On The Three Engines: "Markel operates as a financial holding company powered by insurance underwriting, public equity investments, and controlling interests in private businesses." — Source: Hedge Fund Alpha

- On Organic Growth First: "Reinvesting in existing, proven businesses within the portfolio is always the first priority for deploying capital." — Source: In Practise

- On Markel Ventures: "Markel can offer cash, a quick closing, and a permanent home for the business." — Source: Substack

- On Competing with Private Equity: "Private equity firms are often willing to pay more... They're using other people's money, lots of debt, and have to either deploy their money and earn a fee or give it back." — Source: Substack

- On Berkshire Hathaway as a Benchmark: "Berkshire is considered the new S&P 500 and serves as the ultimate yardstick for Markel's structure and performance." — Source: In Practise

- On The Charlie Munger Question: "Before buying a new stock, always ask if the opportunity is better than what you already own; if not, simply add to existing positions." — Source: The Business Brew

- On Low Turnover: "An equity portfolio turnover rate of around 1% reflects a buy and hold forever mindset that minimizes taxes and trading friction." — Source: Boyar Value Group

- On Selling as Failure: "If I’ve made one mistake in the course of managing investments it was selling really good companies too soon. Because generally, if you’ve made good investments, they will last for a long time." — Source: Novel Investor

- On The 360-Degree View of Capital: "We can invest in the businesses that are proven winners. We can buy new businesses... The way we dynamically triage these opportunities is by putting capital to its best and highest use." — Source: Markel.com

Part 3: Patience and The Eternal Horizon

- On The Eternal Mindset: "With those pennies of underwriting profit, we’re willing to invest that money with an eternal forever mindset." — Source: Markel.com

- On The Redwood Tree Analogy: "Redwood trees symbolize enduring growth. If you ever cut down a redwood tree, you will see a ring marking each year... Some rings would be thin and some would be thick." — Source: Dokumen

- On Buying to Never Sell: "In general, we hope to be able to buy a stock and never sell it. I think that if you limit your buying to things you will be able to own for a long time, you will put more thought into whether to buy it or not." — Source: Fool.com

- On Time as an Advantage: "Having a long time horizon is an epic advantage." — Source: Apprise Wealth

- On Bull vs. Bear Markets: "An old saying is that in a bull market, your time horizons grow longer and longer. In a bear market, they grow shorter and shorter." — Source: Novel Investor

- On Waiting for Alignment: "We are patient. We build relationships with people; sometimes the timing doesn't work, but if the relationship is there, time is your friend." — Source: The Science of Hitting

- On Quarterly Expectations: "Cutting that into quarterly time frames and setting expectations that are tied to that, that just seems like a bad idea." — Source: The Investor's Podcast

- On Nurturing Patience: "Nurture your patience; it will save you from trouble and open up doors to wonderful opportunities." — Source: Sicart Associates

- On Continuous Service: "We think about our customers as once you’re a customer of ours... we want to be doing a good enough job for you indefinitely." — Source: Markel.com

- On Intrinsic Value Drivers: "What publicly-traded companies are worth is roughly 90% dominated by the cash flows they produce over time and 10% by what the market will pay for these types of companies at any given time." — Source: Novel Investor

Part 4: Management and Integrity

- On The Non-Negotiable Factor: "The one area where I will not compromise is in the area of integrity... Even if you get everything else right, the integrity factor can kill you." — Source: MOI Global

- On The Bad Person Rule: "My father used to tell me that, 'you can’t do a good deal with a bad person.' And he was right." — Source: MOI Global

- On The Slipperiness of Success: "Sometimes people can build great careers and enjoy great successes for a period of time through bluster and bullying... but that always comes unraveled. Always." — Source: MOI Global

- On Trust as a Compounder: "Trust compounds like capital." — Source: Circles Studio

- On Identifying High Quality: "Integrity is a huge part of quality. So if that management team has demonstrated the fact to you through consistent performance that they have been conservative, they are indeed demonstrating a pretty strong marker." — Source: Behind the Balance Sheet

- On Behavioral Values: "Values only work if they show up in behavior." — Source: Circles Studio

- On Reciprocity: "One needs to find good people in life and business... If one invests with good intentions then odds are that it is going to come back to him in a compounded return kind of fashion." — Source: Medium

- On The CEO of CEOs: "As the CEO of a diverse financial holding company with decentralized management, I liken my role to being a 'CEO of CEOs.'" — Source: Fool.com

- On Treating Money as Their Own: "We need to trust the people running the businesses. We look for leaders who treat the company's money as their own." — Source: Req.no

Part 5: Assessing Business Quality

- On The Win-Win-Win Architecture: "We define a great company as one with a culture and system of Win-Win-Win for our employees, our customers, and our shareholders." — Source: Good Investing

- On Customer Delight: "We want to be doing a good enough job for customers and delivering enough value and delighting them in such a way that they want to keep doing business with us." — Source: Dokumen

- On Doing Things For Customers: "You want companies that are doing things for their customers rather than to their customers." — Source: MOI Global

- On Solving Problems: "The more a business serves others, and the more problems they solve, the more profitable they will be and the more an investor in those enterprises should make." — Source: MOI Global

- On Market Leadership: "Each of these companies are really market leaders in what they do... they're established businesses that have long histories of taking care of their customers." — Source: Substack

- On Business as Human Organization: "Business to me is the form and organization by which people creatively apply their skills and talents to solving problems or serving other people." — Source: Economic Times

- On Service as a Flywheel: "Serving others works forever. The mindset of service drives a durable flywheel that attracts people, capital, and businesses." — Source: Markel.com

- On Endurance: "When asked to describe the essence of Markel in one word, Gayner replied: Endurance." — Source: Dokumen

- On Embracing Compromise: "Perfection doesn't exist in this world. All of my choices involve various degrees of compromise and tradeoffs." — Source: Fool.com

Part 6: Risk, Leverage, and Mistakes

- On Mistakes of Omission: "If I look at the mistakes that I’ve made, the ones that have been most costly have been those of omission." — Source: Novel Investor

- On Overconfidence: "I think some of the great mistakes are made by people who think they’re smarter than they really are." — Source: Economic Times

- On Excessive Leverage: "I’ve made so many mistakes over the years that I struggle to isolate just one as the biggest... Among the choices though I think excessive leverage has been the most personally painful." — Source: Novel Investor

- On Mislabeling Risk: "Another huge mistake that I think people in general make is to mislabel risks. Specifically, people seem to think about risks in nominal rather than real terms." — Source: MOI Global

- On The Risk of Cash: "To have a lot of cash or government bonds has been a comforting thing... but I think it is a mistake to think that means you are not taking risks. The purchasing power of the currency continues to decline." — Source: MOI Global

- On The Danger of Being Right: "If you take yourself too seriously, that can easily slip over into thinking you’re right and if you think you’re right, you know, then you’re setting yourself up for a fall." — Source: The Investor's Podcast

- On Radical Moderation: "Aim to avoid anything so aggressive that you might risk getting knocked out of the game." — Source: The Investor's Podcast

- On Margin of Error: "He views the margin of safety not just as a price discount, but as a structural protection built by avoiding leverage and investing in high-quality people." — Source: The Investor's Podcast

- On Learning from Others: "I really believe it’s better to learn from other people’s mistakes as much as possible." — Source: Substack

- On Using Past Data for Future Risk: "You would be unwise and ignorant not to pay attention to what has happened in the past, but the risk you’re writing for is the future." — Source: Good Investing

Part 7: The Art of Continuous Learning

- On The Value of Information: "I've found no substitution for constant reading to immerse myself in the flow of information that eventually results in ideas." — Source: Good Investing

- On Congealed Intellectual Capital: "Equities are congealed intellectual capital, and that is what I want." — Source: MOI Global

- On Pushing the Circle of Competence: "One of the things you should always be doing with your circles of competence is see if you can push it a little bit more, because the world changes." — Source: Novel Investor

- On The Work of Reading: "It may appear that I am not doing very much, but I am actually reading, thinking, and talking to people all day." — Source: Behind the Balance Sheet

- On Diverse Inputs: "To keep your mind limber... is to have different forms of input coming into your thought process." — Source: Good Investing

- On The Power of Biographies: "Biographies like And There Was Light provide historical context that helps an investor understand human resilience and problem-solving." — Source: Behind the Balance Sheet

- On Recognizing Bubbles: "Reading classic financial literature helps investors understand the timeless nature of human greed and financial manias." — Source: Substack

- On Staying within Boundaries: "There might well be opportunities, but I have decided that they’re beyond my circle of competence to invest in them." — Source: Fool.com

- On The Sensation of Business: "Daily reading allows an investor to continuously get the sensation of how the macroeconomic environment and individual businesses are shifting." — Source: Behind the Balance Sheet

Part 8: Temperament and Life Philosophy

- On The Great Algorithm: "The great algorithm in life is 'do more of what’s working.'" — Source: Good Investing

- On Managing Temperament: "Successful investing requires the management of your own ego and temperament and usually that of your clients as well." — Source: Novel Investor

- On Leaning Against the Wind: "Part of being a value investor is being willing to lean against the wind and to do things that are unpopular... If it were always easy, that’s what everyone would do." — Source: Fool.com

- On The Necessity of Humor: "A sense of humor acts as a vital brake on taking oneself too seriously, helping avoid the ego-driven mistakes common in finance." — Source: The Investor's Podcast

- On The Plodder Mentality: "Gayner describes himself as a plodder—someone who values steady, incremental, and persistent progress over long periods." — Source: GuruGems

- On Leaving Slack in the System: "Leave a little slack in the system. Allow time and space, and muscle, and rest, and energy to create things that you couldn't have thought of beforehand." — Source: Dokumen

- On The Feeling of Mistakes: "It feels great! Because if it didn't feel good, you wouldn't do it. If the idea didn't seem brilliant at the time, you never would have acted on it." — Source: Dokumen

- On Low-Debt Philosophy: "We see our strong capital position and low-debt philosophy as necessary preconditions for long-term thinking." — Source: Substack

- On Indifference to the Path: "I'm indifferent to the path — whether I make zero in year one and 40 percent of it in year two... That pattern doesn't matter to me because I'm not trying to hit quarterly goals." — Source: Dokumen

- On The Illusion of "This Time Is Different": "Things are always getting better or worse, and it’s no different this time." — Source: Fool.com