Lessons from Tom Russo

Value investor Tom Russo spent decades at Gardner Russo & Quinn buying family-controlled, global consumer brands. He is best known for the "capacity to suffer," arguing that great businesses must endure short-term financial hits to fund long-term growth. His track record is a study in extreme patience, showing how ignoring quarterly earnings and focusing on tax-deferred compounding creates lasting wealth.

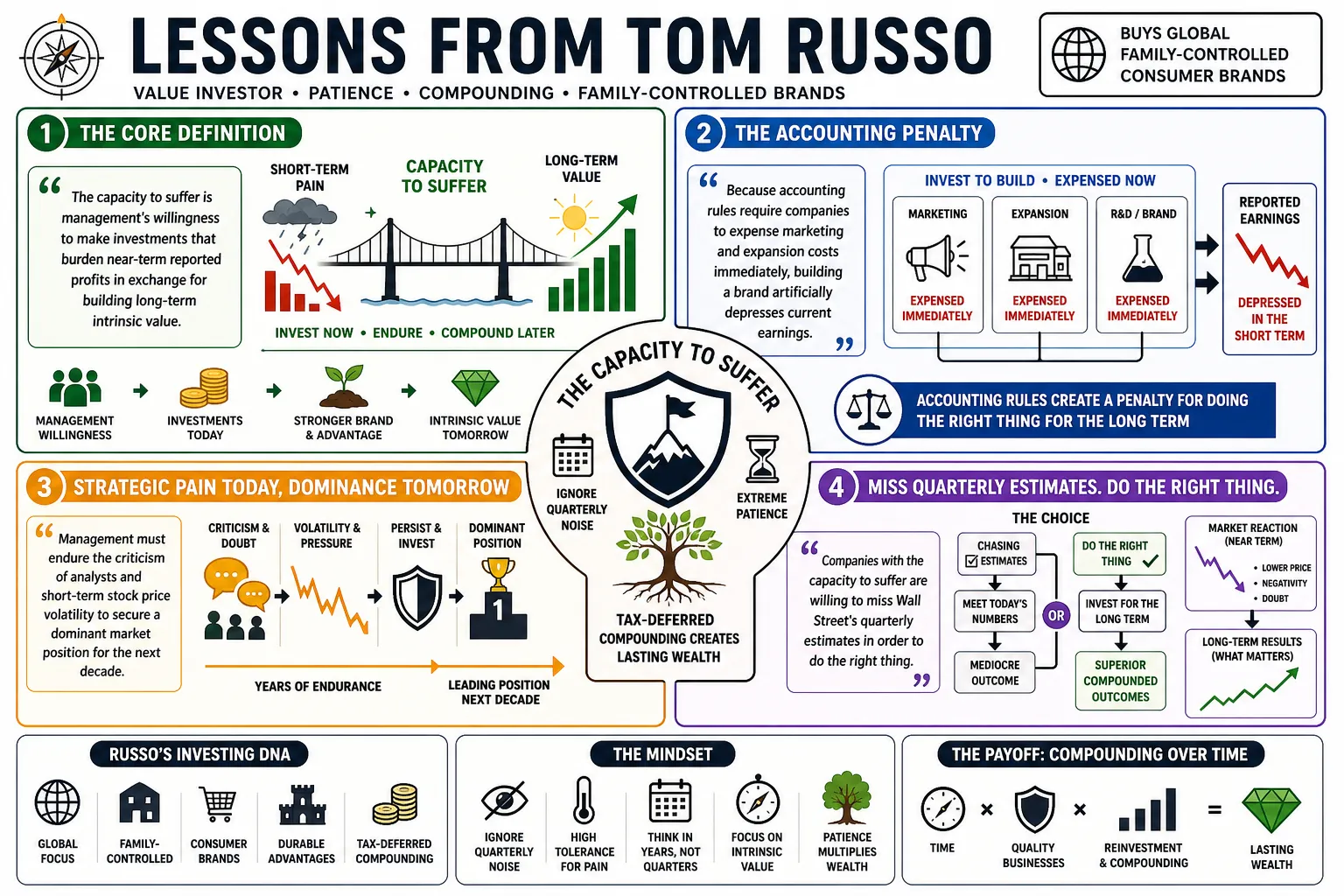

Part 1: The Capacity to Suffer (Corporate Leadership)

- On the core definition: "The capacity to suffer is management's willingness to make investments that burden near-term reported profits in exchange for building long-term intrinsic value." — Source: [YouTube]

- On the accounting penalty: "Because accounting rules require companies to expense marketing and expansion costs immediately, building a brand artificially depresses current earnings." — Source: [Morningstar]

- On strategic pain: "Management must endure the criticism of analysts and short-term stock price volatility to secure a dominant market position for the next decade." — Source: [Scuttlebutt Investor]

- On missing estimates: "Companies with the capacity to suffer are willing to miss Wall Street's quarterly estimates in order to do the right thing for the business long-term." — Source: [MOI Global]

- On Nestlé's global push: "Nestlé demonstrated a profound capacity to suffer by spending heavily for decades to build distribution networks in emerging markets." — Source: [Morningstar]

- On transitioning business models: "Philip Morris International suffered by deploying billions of dollars to pivot away from combustible cigarettes toward reduced-risk products." — Source: [HeyGotrade]

- On the rarity of endurance: "Most public company managers are incentivized by annual bonuses, making them financially unwilling to tolerate the suffering required for generational growth." — Source: [MOI Global]

- On avoiding bad acquisitions: "The capacity to suffer also means enduring the pressure to 'do something' and refusing to overpay for acquisitions just to show top-line growth." — Source: [Medium]

- On the origin of the term: "I credit the phrase to Jean-Marie Eveillard, who originally used it to describe the pain an analyst feels when they are early and out of favor." — Source: [Morningstar]

- On long-term optics: "A willingness to tolerate ugly financial optics is often the absolute prerequisite for compounding real corporate wealth." — Source: [Apple Podcasts]

Part 2: The Capacity to Suffer (The Investor's Burden)

- On investor endurance: "A good money manager must have the emotional and financial ability to endure periods of underperformance while the market catches up to the company's growing value." — Source: [Morningstar]

- On the dot-com bubble: "During the late 1990s, I had to suffer through holding boring consumer brands like Unilever while the tech bubble soared without us." — Source: [Morningstar]

- On standing firm: "There is no better time to invest than when the markets are in chaos. Whenever you have a market catastrophe, stay the course." — Source: [Ivey Business School]

- On delayed gratification: "We tend to benefit in life when we sacrifice something today to gain something tomorrow. That is true for individuals just as it is for companies." — Source: [YouTube]

- On client alignment: "An investment strategy requiring patience will fail if your clients lack the capacity to suffer alongside you during periods of relative underperformance." — Source: [Scuttlebutt Investor]

- On periods of being wrong: "You have to accept that looking foolish in the short term is the price of admission for being right over the span of decades." — Source: [MOI Global]

- On avoiding panic: "If you stand firm during a catastrophe, you'll be OK; the real danger is reacting to the market's temporary suffering by selling your best assets." — Source: [Ivey Business School]

- On absolute conviction: "You can only suffer through a prolonged downturn if you deeply understand the intrinsic cash-generating power of the businesses you own." — Source: [Novel Investor]

- On the reward of patience: "The suffering eventually ends when the cash flows from those long-term investments finally mature and become undeniable to the broader market." — Source: [Medium]

Part 3: The Capacity to Reinvest

- On the twin engines of compounding: "The capacity to suffer must be paired with the capacity to reinvest—the ability to deploy large amounts of capital at high rates of return." — Source: [Apple Podcasts]

- On addressable markets: "I look for businesses that have a vast runway to put capital back into the business, because 95 percent of the world's population lives outside the United States." — Source: [Morningstar]

- On the ultimate management test: "As an investor in businesses which generate enormous cash flows, my single most important issue to get right is what management will do with cash flow through reinvestment." — Source: [YouTube]

- On mature cash flows: "The ideal model is a company that takes the massive free cash flow generated in mature markets and reinvests it into new geographies." — Source: [YouTube]

- On avoiding stagnation: "A cheap but stagnant business is a poor investment because its value is slowly eroded; you need growing dollar bills driven by internal reinvestment." — Source: [YouTube]

- On brand scalability: "Trusted global brands possess the rare ability to take a product successful in one market and reinvest capital to scale it across fifty others." — Source: [MOI Global]

- On digital networks: "Companies like Mastercard and Alphabet fit the reinvestment profile beautifully because their digital dominance allows them to deploy capital globally at exceptionally high returns." — Source: [HeyGotrade]

- On evaluating capital allocation: "Do they care about the owner, or do they care about themselves? The answer is revealed by the quality and discipline of their reinvestment decisions." — Source: [YouTube]

- On avoiding early dividends: "If a company has a massive global runway, paying out large dividends early on destroys value that could have been compounded internally." — Source: [Latticework]

- On long-term compounding: "The math of wealth creation requires a business that can internalize its own compounding, shielding the investor from the friction of finding new ideas." — Source: [Gainify]

Part 4: Family-Controlled Businesses and Governance

- On the family advantage: "Family-controlled companies are uniquely positioned to possess the capacity to suffer because they think in generations rather than quarterly earnings cycles." — Source: [Ivey Business School]

- On shielding management: "When a founding family holds significant control, it provides a buffer against activist investors or analysts demanding immediate cost-cutting." — Source: [Gainify]

- On aligning interests: "Family control reduces agency costs; the family’s wealth is tied directly to the long-term health of the enterprise rather than next year's bonus." — Source: [Latticework]

- On dual-class structures: "While corporate governance experts often hate dual-class voting shares, I love them if they protect a visionary family from Wall Street's short-term demands." — Source: [MOI Global]

- On Heineken's structure: "The Heineken family’s control allowed the company to consistently prioritize long-term brand equity over short-term financial engineering." — Source: [GuruFocus]

- On Richemont: "Compagnie Financière Richemont, controlled by the Rupert family, can patiently build luxury assets like Cartier without rushing the delicate process of brand building." — Source: [HeyGotrade]

- On enduring culture: "I look for companies that resemble an ancient Japanese temple—the outside is old, the inside is refreshed, but there must be an enduring, family-like culture." — Source: [Udemy]

- On the Berkshire model: "Berkshire Hathaway is the ultimate example of a company with a family-office mindset, utilizing permanent capital to suffer for long-term gain." — Source: [YouTube]

- On surviving downturns: "During economic crises, family-controlled businesses are less likely to lay off key talent or slash marketing, allowing them to capture market share when competitors retreat." — Source: [Latticework]

Part 5: Wall Street's Short-Termism

- On misaligned incentives: "Sadly, on Wall Street, rewards for acting with self-interest and to disadvantage public shareholders often prove to be too tempting." — Source: [Novel Investor]

- On the hunting mentality: "I think most people on Wall Street are hunters. They like to fell big beasts, constantly chasing the next immediate catalyst." — Source: [Value Investing World]

- On the pressure to act: "The financial industry demands constant motion and trading, but investors should think more and trade less to truly build wealth." — Source: [Udemy]

- On quarterly capitalism: "The obsession with smoothing out quarterly earnings prevents public companies from making the very investments that would secure their future." — Source: [Morningstar]

- On new eras: "I believe pronouncements of a new era will prove to be as misplaced going forward as they have been in the past." — Source: [Novel Investor]

- On the danger of bonuses: "When management is compensated based on annual stock performance, they will predictably underinvest in the long-term health of the brand." — Source: [MOI Global]

- On activist investors: "Activist investors often force companies to strip away the exact investments in marketing and distribution that generate long-term defensive moats." — Source: [Gainify]

- On institutional impatience: "Institutional capital frequently lacks the capacity to suffer, forcing portfolio managers to sell great businesses just as they are planting seeds for the next decade." — Source: [Scuttlebutt Investor]

- On Wall Street's blind spot: "Wall Street struggles to model companies that expense heavy investments today for a payoff five years out, creating the mispricing we try to exploit." — Source: [YouTube]

Part 6: Brands, Moats, and Pricing Power

- On pricing power: "The true test of a consumer brand is whether it can raise prices without losing market share, providing a natural hedge against inflation." — Source: [Ivey Business School]

- On indispensable products: "I target indispensable consumer products like food, beverage, and tobacco that people buy reliably regardless of the macroeconomic environment." — Source: [HeyGotrade]

- On brand trust: "A brand is essentially a promise to the consumer; when that promise is delivered consistently over decades, it creates a lasting moat." — Source: [Udemy]

- On the barrier to entry: "The billions of dollars and decades of suffering required to build a global distribution network serve as a massive barrier to entry for upstarts." — Source: [Morningstar]

- On local tastes, global scale: "The best global companies, like Nestlé, operate with local autonomy to match local tastes, backed by the sheer scale of a global balance sheet." — Source: [Morningstar]

- On luxury goods: "In the luxury sector, heritage cannot be fabricated quickly; time itself is the moat that protects a brand like Cartier." — Source: [HeyGotrade]

- On industry transformation: "With every company I own, there is always the question of sustainability—that a transformation in its industry will leave it behind." — Source: [Ivey Business School]

- On mindshare: "You are investing in a sliver of the consumer's mindshare; once a brand is entrenched there, it requires extraordinary effort by a competitor to dislodge it." — Source: [MOI Global]

- On digital moats: "Payment networks like Visa and Mastercard enjoy incredible pricing power because they operate as the fundamental toll roads of the global digital economy." — Source: [HeyGotrade]

Part 7: Tax-Efficient Compounding

- On the ultimate advantage: "The only real break an investor gets from the government is the non-taxation of unrealized capital gains; you must exploit this by holding winners." — Source: [Columbia Business School]

- On the friction of trading: "Every time you sell a position to buy another, you pay taxes and friction costs, significantly interrupting the magic of compound interest." — Source: [Udemy]

- On fifty-cent dollars: "A fifty-cent dollar only creates massive wealth if it is a growing business; a static cheap asset will eventually be eroded by inflation and taxes." — Source: [YouTube]

- On portfolio concentration: "When you find a business capable of compounding internally for decades, you should concentrate your capital there rather than diluting it with lesser ideas." — Source: [Hedge Fund Alpha]

- On long holding periods: "My strategy relies on holding companies for twenty or thirty years, allowing the underlying business growth to compound entirely tax-deferred." — Source: [YouTube]

- On letting winners run: "It is a mathematical necessity to let your best businesses become a massive portion of your portfolio if you want to generate generational wealth." — Source: [Hedge Fund Alpha]

- On avoiding the hunt: "By finding a few great businesses that reinvest their own cash flows, I am spared the tax-inducing labor of constantly hunting for new investments." — Source: [Value Investing World]

- On absolute returns: "Tax efficiency is more than an accounting trick; over decades, the deferred tax liability acts as an interest-free loan from the government to compound your money." — Source: [Columbia Business School]

- On the cost of mistakes: "The math of selling a great company means your next idea must be vastly better simply to cover the tax bill you incur by trading." — Source: [YouTube]

Part 8: The Psychology of the Farmer

- On defining the mindset: "I consider myself to be a farmer, not a hunter. I'm very comfortable planting a few rows and just tending to them carefully over the years." — Source: [YouTube]

- On ignoring noise: "The farmer does not dig up the seed every day to see if it has sprouted; similarly, investors must ignore daily market noise to let their capital grow." — Source: [Value Investing World]

- On the influence of Buffett: "Meeting Warren Buffett in 1982 shifted my mindset away from buying liquidating cigar butts toward owning high-quality global franchises." — Source: [YouTube]

- On being right once: "If you find a business with a vast global runway and honest management, you only need to make the decision to buy it once." — Source: [Latticework]

- On continuous learning: "The evolution from deep value to global quality requires an investor to continually study consumer behavior and global demographics." — Source: [Udemy]

- On the comfort of boredom: "A truly great investment portfolio should look incredibly boring from day to day, operating quietly in the background like a well-tended field." — Source: [Value Invest]

- On resisting action bias: "The hardest psychological hurdle in investing is resisting the urge to do something when doing nothing is the mathematically superior choice." — Source: [Ivey Business School]

- On trusting management: "You have to deeply trust the operators of the business; if you are constantly second-guessing their capital allocation, you cannot maintain the farmer's patience." — Source: [YouTube]

- On outperforming in tough times: "I look for trusted companies that have proven to outperform in tough times, providing the psychological comfort needed to hold them." — Source: [Udemy]

- On the ultimate goal: "The purpose of investing is not to be proven right on a quarterly basis, but to quietly accumulate capital by partnering with businesses that do the heavy lifting for you." — Source: [Scuttlebutt Investor]