Lessons from Walter Schloss

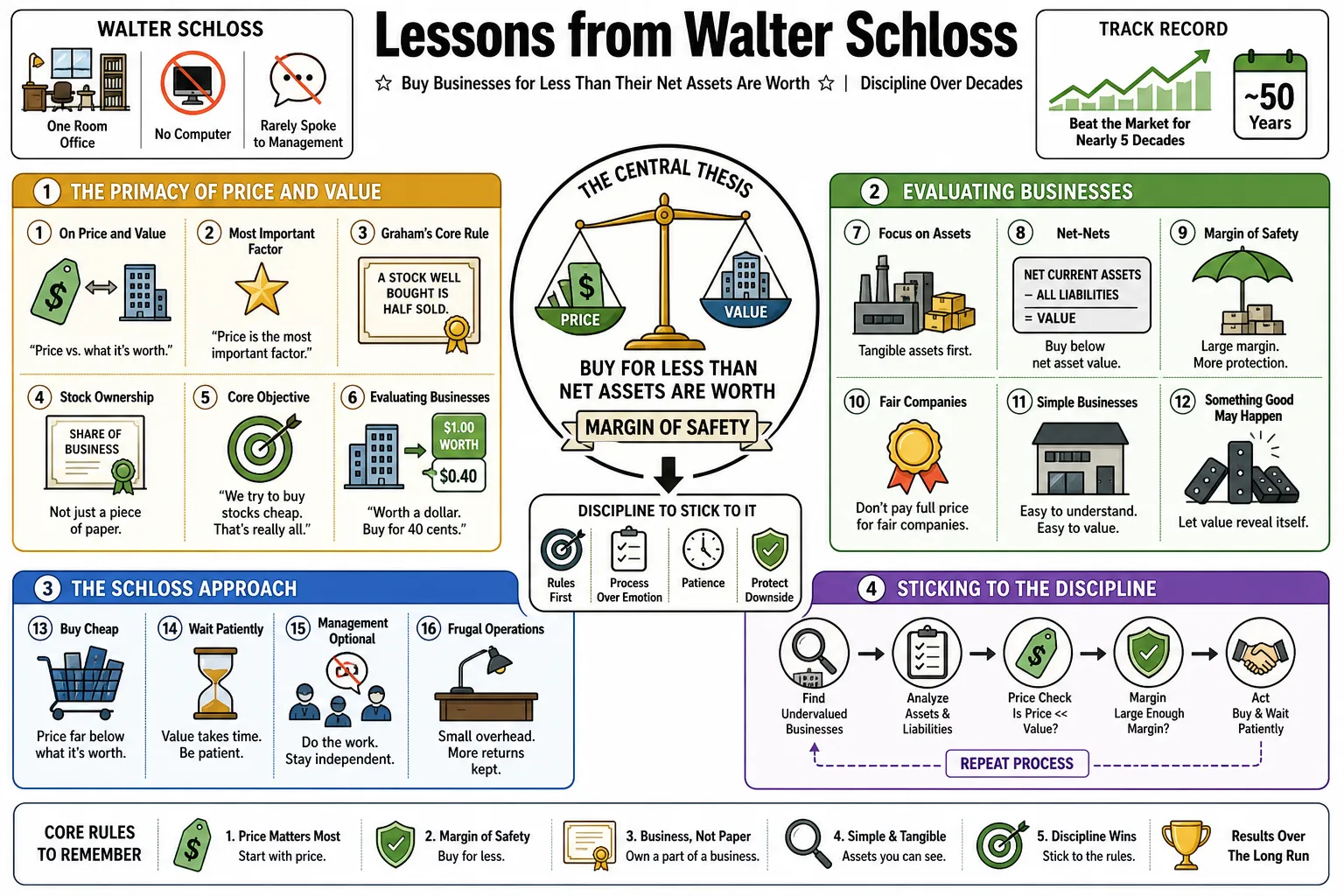

Walter Schloss worked out of a single room, refused to use a computer, and rarely spoke to management. By rigidly applying Benjamin Graham's method of buying businesses for less than their net assets were worth, he beat the market for nearly five decades. This collection covers his frugal, asset-based approach and the discipline required to actually stick to it.

Part 1: The Primacy of Price and Value

- On Price and Value: "Basically, we try to buy value expressed in the differential between its price and what we think it's worth." — Source: [Barron's]

- On the Most Important Factor: "Price is the most important factor to use in relation to value." — Source: [Walter J. Schloss Archives]

- On Graham's Core Rule: "A stock well bought is half sold." — Source: [GuruFocus]

- On Stock Ownership: "Remember that a share of stock represents a part of a business and is not just a piece of paper." — Source: [Walter J. Schloss Archives]

- On the Core Objective: "We try to buy stocks cheap. That’s really all." — Source: [Outstanding Investor Digest]

- On Evaluating Businesses: "If a business is worth a dollar and I can buy it for 40 cents, something good may happen to me." — Source: [Columbia Business School]

- On Fair Companies: "I don't like to buy good companies at what I think they're worth. I have no problem buying a good company, but I want to buy it at a discount." — Source: [GuruFocus]

- On Avoiding Quick Profits: "Don't buy on tips or for a quick move. Let the professionals do that, if they can." — Source: [Walter J. Schloss Archives]

- On Groceries vs. Perfume: "You buy stocks like you buy groceries, not the way you buy perfume." — Source: [Barron's]

- On Patience: "Have patience. Stocks don't go up immediately." — Source: [Walter J. Schloss Archives]

Part 2: Assets Over Earnings

- On the Core Principle: "Try to buy assets at a discount than to buy earnings." — Source: [GuruFocus]

- On Earnings Volatility: "Earnings can change dramatically in a short time. Usually assets change slowly." — Source: [GuruFocus]

- On Knowledge Requirements: "One has to know much more about a company if one buys earnings." — Source: [GuruFocus]

- On Starting Valuation: "Use book value as a starting point to try and establish the value of the enterprise." — Source: [Walter J. Schloss Archives]

- On Downside Protection: "I like to buy stocks selling below book value. It gives me a certain amount of protection." — Source: [GuruFocus]

- On Forecasting: "So many investors today focus on earnings, but I focus on assets and don't try to predict next months' earnings, which is a much more difficult approach to investing." — Source: [GuruFocus]

- On What Really Matters: "Most people say, 'What is it going to earn next year?' I do not care much about earnings as long as they are reasonable; I focus on assets." — Source: [Business Insider]

- On the Value of Low Debt: "If you don't have a lot of debt, it's worth something." — Source: [Business Insider]

- On Working Capital: "We basically followed the idea of buying companies selling below working capital—at two-thirds of working capital." — Source: [GuruFocus]

- On Predictability: "Assets seem to change less than earnings." — Source: [Outstanding Investor Digest]

Part 3: Emotional Discipline and Psychology

- On Market Emotions: "The market is a very emotional place that appeals to fear and greed." — Source: [GuruFocus]

- On the Worst Emotions: "Fear and greed are probably the worst emotions to have in connection with the purchase and sale of stocks." — Source: [Walter J. Schloss Archives]

- On Self-Awareness: "When it comes to investing, my suggestion is to first understand your strengths and weaknesses, and then devise a simple strategy so that you can sleep at night!" — Source: [GuruFocus]

- On the Art of Investing: "I think investing is an art, and we tried to be as logical and unemotional as possible." — Source: [Walter J. Schloss Archives]

- On Independent Thinking: "Don't be afraid to be a loner but be sure that you are correct in your judgment." — Source: [Walter J. Schloss Archives]

- On Self-Doubt: "You can't be 100% certain but try to look for weaknesses in your thinking." — Source: [Walter J. Schloss Archives]

- On Conviction: "Have the courage of your convictions once you have made a decision." — Source: [Walter J. Schloss Archives]

- On Panic Selling: "Do not sell on bad news." — Source: [Walter J. Schloss Archives]

- On Dealing with Declines: "Don't sell because the price goes down. If the fundamentals are sound, buy more." — Source: [Walter J. Schloss Archives]

- On Experience and Timidity: "Timidity prompted by past failures causes investors to miss the most important bull markets." — Source: [GuruFocus]

Part 4: The Mechanics of Buying and Selling

- On Scaling In and Out: "Buy on a scale down and sell on a scale up." — Source: [Walter J. Schloss Archives]

- On Price Drops: "We like to buy stocks which we feel are undervalued, and then we have to have the guts to buy more when they go down." — Source: [Hedge Fund Alpha]

- On the Hardest Decision: "Sell is tough. It's the worst, it's the most difficult thing of all." — Source: [Barron's]

- On Patience When Selling: "Don't be in too much of a hurry to sell. If the stock reaches a price that you think is a fair one, then you can sell." — Source: [Walter J. Schloss Archives]

- On Re-evaluating: "Before selling, try to re-evaluate the company again and see where the stock sells in relation to its book value." — Source: [GuruFocus]

- On Leaving Money on the Table: "It is better to sell too soon than to overstay your welcome and get caught in a severe downturn." — Source: [Barron's]

- On True Knowledge: "You never really know a stock until you own it." — Source: [Hedge Fund Alpha]

- On Identifying Lows: "Buy near the low of the past few years to increase your margin of safety." — Source: [Walter J. Schloss Archives]

- On Target Returns: "If a stock goes up 50%, don't sell it just because it went up. Wait until it reaches its fair value." — Source: [Walter J. Schloss Archives]

Part 5: Risk Management and Capital Preservation

- On the Primary Rule: "Remember this: I don't like to lose money." — Source: [GuruFocus]

- On Protecting the Downside: "I try to buy stocks that are protected on the downside, and then the upside sort of takes care of itself." — Source: [GuruFocus]

- On Debt Limits: "Ensure that debt does not exceed 100% of the equity (capital and surplus for the common stock)." — Source: [Walter J. Schloss Archives]

- On Leverage: "Be careful of leverage. It can go against you." — Source: [GuruFocus]

- On Keeping Profits: "It is harder to keep money than to make it; once you lose it, it's hard to get back." — Source: [Walter J. Schloss Archives]

- On Asset Classes: "Prefer stocks over bonds. Bonds limit your gains, and inflation reduces your purchasing power over time." — Source: [Walter J. Schloss Archives]

- On Margin of Safety: "Buying near multi-year lows offers the best margin of safety because expectations are already washed out." — Source: [Walter J. Schloss Archives]

- On Corporate Borrowing: "Avoid companies with excessive debt, because when things go wrong, the debt holders take the business." — Source: [Outstanding Investor Digest]

- On Compounding: "Remember the power of compounding. Understand the 'Rule of 72'." — Source: [Walter J. Schloss Archives]

Part 6: Portfolio Construction and Diversification

- On Diversification Volume: "I always held 50 to 100 stocks at any given time because it would have been very stressful if one particular stock had turned against me." — Source: [GuruFocus]

- On Personal Comfort: "I know my limitations, so I'd rather invest in the way I am most comfortable with." — Source: [GuruFocus]

- On Investment Horizons: "Our average holding period is four years." — Source: [Macro Ops]

- On Concentration vs. Diversification: "While some investors concentrate heavily to maximize returns, broad diversification protects against the risk of bankruptcy in deeply depressed businesses." — Source: [Outstanding Investor Digest]

- On Structuring the Portfolio: "We happen to run a partnership and each year we buy stocks and they go up, we sell them and then we try to buy something cheaper." — Source: [Novel Investor]

- On Sizing Positions: "Spread bets across many cheap stocks because it is impossible to know which specific beaten-down company will be the one to recover." — Source: [Outstanding Investor Digest]

- On the "Ick" Factor: "Invest broadly in out-of-favor companies—the ones that are currently unpalatable to institutional investors." — Source: [Macro Ops]

- On Managing Outside Capital: "Operate with a low profile and primarily manage money for people who genuinely need help preserving their wealth." — Source: [Barron's]

- On Alignment: "Perfectly align interests with investors by taking no management fee, accepting only a share of the final profits." — Source: [Hedge Fund Alpha]

Part 7: The "Cigar Butt" and Deep Value Strategy

- On the Core Target: "We try to buy things that are out of favor—stocks that others don’t want." — Source: [Good Investing]

- On Depressed Companies: "Look for stocks that are on the 52-week low list, as they often present the best starting point for a value thesis." — Source: [Outstanding Investor Digest]

- On Temporary Troubles: "Focus on companies facing temporary, solvable problems rather than terminal decline." — Source: [Outstanding Investor Digest]

- On Reading Financials: "I found that it was much better to look at the figures rather than people." — Source: [GuruFocus]

- On the Illusion of Growth: "Avoid paying a premium for expected growth, because growth is far less certain than the tangible assets currently on the balance sheet." — Source: [Outstanding Investor Digest]

- On "Pure" Graham Style: "Stick to buying fair companies at wonderful prices rather than trying to identify wonderful companies at fair prices." — Source: [Kingswell]

- On Ignoring the Story: "Do not get distracted by the nature of the business; if the numbers dictate a deep discount, the specific industry matters less." — Source: [Columbia Business School]

- On Surprising Outcomes: "Better to be rich than right; sometimes a cheap asset turns into a massive growth engine." — Source: [Fordham Gabelli Center]

- On Working the Numbers: "Rely on simple, publicly available data like Value Line reports rather than insider access or complex models." — Source: [Barron's]

Part 8: Simplicity and Independent Thinking

- On Having a Philosophy: "Have a philosophy of investment and try to follow it." — Source: [Walter J. Schloss Archives]

- On Acknowledging Genius: "Warren is brilliant... but we cannot be like him. You've got to satisfy yourself on what you want to do." — Source: [GuruFocus]

- On Seeking Input: "Listen to suggestions from people you respect. You don't have to accept them, but listen." — Source: [Walter J. Schloss Archives]

- On Keeping Overhead Low: "Run a lean operation to ensure that expenses don't eat into the compounding of your investors' capital." — Source: [Columbia Business School]

- On the Information Diet: "Stick to print newspapers and physical annual reports rather than chasing real-time ticker tape fluctuations." — Source: [Barron's]

- On Doing the Work: "Base your conviction entirely on your own research, not on the opinions of the crowd or market momentum." — Source: [Walter J. Schloss Archives]

- On Setting Realistic Goals: "Aim for steady, consistent base hits rather than attempting to hit home runs with speculative, high-flying stocks." — Source: [Outstanding Investor Digest]

- On Longevity in the Market: "True success in investing is measured over decades, requiring a strategy that is sustainable through multiple market cycles." — Source: [Ivey Business School]

- On Simplicity: "The most reliable path to market-beating returns does not require complex algorithms, but rather a simple, repeatable process executed with iron discipline." — Source: [Columbia Business School]