Lessons from Abigail Wattley

Abigail Wattley manages the $4.5 billion Williams College endowment, which funds most of the school's operating budget. Since starting as an analyst in 2007, she has built a strategy that ignores arbitrary asset-allocation targets in favor of meeting concrete spending needs and choosing patience over market timing. This profile outlines her practical approach to institutional investing, from evaluating outside managers to running an internal team.

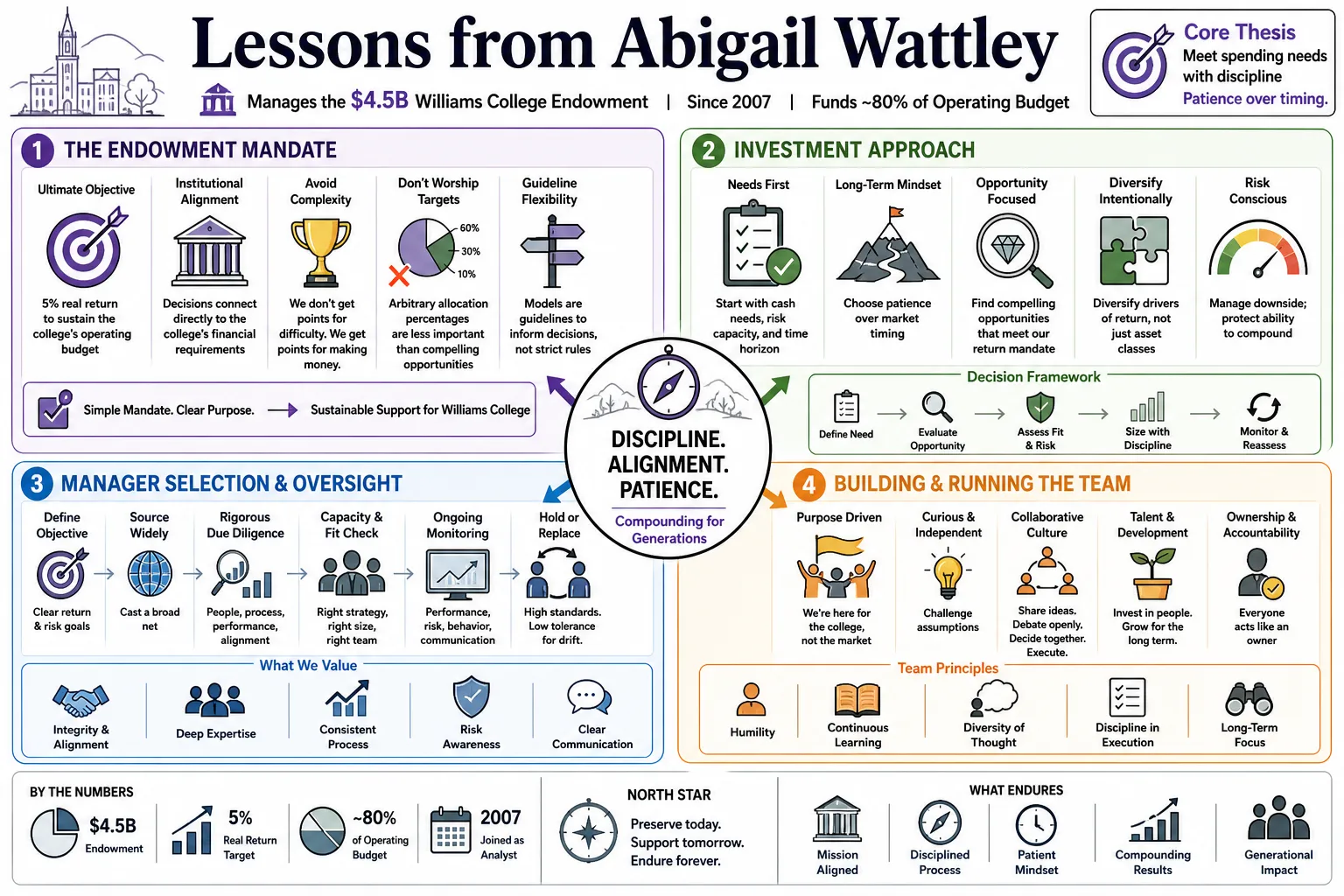

Part 1: The Endowment Mandate

- On ultimate objectives: "The sole purpose of the portfolio is to generate a five percent real return to sustain the college's operating budget." — Source: [Capital Allocators]

- On institutional alignment: "Every investment decision must connect directly to the college's financial requirements, not to external benchmarks." — Source: [Williams College]

- On avoiding complexity: "We don't get points for difficulty. We get points for making money." — Source: [Capital Allocators]

- On asset allocation targets: "Arbitrary allocation percentages are less important than finding compelling opportunities that serve our return mandate." — Source: [Capital Allocators]

- On guideline flexibility: "Investment models should function as guidelines to inform decisions, rather than strict mandates that force our hand." — Source: [Capital Allocators]

- On spending reliance: "When an endowment funds sixty percent of an operating budget, the tolerance for permanent capital impairment drops to zero." — Source: [Capital Allocators]

- On peer comparison: "Chasing the returns of other institutions distracts from the specific liability stream and risk profile of our own college." — Source: [Williams College]

- On real returns: "Factoring in inflation is non-negotiable; nominal returns offer a false sense of security when institutional costs are rising." — Source: [Capital Allocators]

- On long-term focus: "The time horizon of a college is perpetual, which allows us to underwrite strategies that might take a decade to materialize." — Source: [Williams College]

- On mission integration: "The investment office is not an island; it exists entirely to enable the academic and operational goals of the faculty and students." — Source: [Capital Allocators]

Part 2: Manager Selection

- On manager underwriting: "The craft of underwriting is often learned best in asset classes that are out of favor or generally avoided by others." — Source: [Capital Allocators]

- On reviewing materials: "You can often identify the core problems in a manager's portfolio simply by applying deep scrutiny to their standard reporting materials." — Source: [Capital Allocators]

- On manager alignment: "We look for partners who treat their own capital with the same care and caution that we apply to the college's funds." — Source: [Williams College]

- On organizational stability: "A brilliant investor inside a dysfunctional firm is rarely a durable source of long-term returns." — Source: [Capital Allocators]

- On past performance: "Historical track records tell us what a manager did in a specific environment, not necessarily what they will do in the next one." — Source: [Capital Allocators]

- On strategy drift: "When managers drift from their core competency, it usually signals a desire to grow assets rather than compound capital." — Source: [Williams College]

- On concentration: "We prefer managers who are willing to concentrate their portfolios in their absolute best ideas." — Source: [Capital Allocators]

- On relationship building: "The best manager relationships are built during periods of underperformance, where communication and transparency matter most." — Source: [Capital Allocators]

- On portfolio fit: "A great manager doesn't always make a great addition to the portfolio if their exposure overlaps heavily with our existing book." — Source: [Williams College]

- On sizing allocations: "An allocation must be large enough to move the needle on our overall performance, or it isn't worth the administrative burden." — Source: [Capital Allocators]

Part 3: Team Development

- On making mistakes: "Giving team members a long leash to make mistakes is essential for teaching them what not to do." — Source: [Capital Allocators]

- On mentorship: "Institutional knowledge is best transferred through direct mentorship and shared repetitions in due diligence meetings." — Source: [Capital Allocators]

- On internal promotions: "A homegrown career path ensures that the leadership deeply understands the specific history and culture of the institution." — Source: [Williams College]

- On delegating authority: "You have to allow younger analysts to take ownership of ideas, even if their approach differs slightly from yours." — Source: [Capital Allocators]

- On handling complexity: "Assigning junior staff to opaque or complex asset classes forces them to develop original analytical frameworks." — Source: [Capital Allocators]

- On debate culture: "The investment committee room must be a place where junior analysts feel comfortable challenging the assumptions of the CIO." — Source: [Williams College]

- On retaining talent: "Keeping great investors at an endowment requires offering them intellectual autonomy and a clear path for professional growth." — Source: [Capital Allocators]

- On hiring criteria: "We screen for intellectual curiosity and humility, as arrogance is fatal in long-term investing." — Source: [Williams College]

- On succession planning: "A healthy investment office builds its bench strength years before a senior departure actually occurs." — Source: [Capital Allocators]

- On shared conviction: "When the entire team has a hand in underwriting a manager, the institution is much more likely to hold the line during a drawdown." — Source: [Capital Allocators]

Part 4: Portfolio Construction

- On strategic patience: "The Williams playbook is built on strategic patience rather than the frequent execution of tactical pivots." — Source: [Capital Allocators]

- On rebalancing: "Mechanical rebalancing forces you to trim your winners and add to your losers, which instills discipline in emotional markets." — Source: [Williams College]

- On diversification: "True diversification means holding assets that will behave differently during a severe liquidity crisis." — Source: [Capital Allocators]

- On liquidity management: "You cannot spend illiquid assets; managing the pacing of capital calls and distributions is just as important as the investments themselves." — Source: [Capital Allocators]

- On thematic investing: "Top-down thematic investing often looks brilliant in hindsight but is difficult to execute consistently in real time." — Source: [Williams College]

- On private markets: "The illiquidity premium in private markets is only worth capturing if the absolute return clears our hurdle rate by a wide margin." — Source: [Capital Allocators]

- On asset class silos: "Looking at investments strictly through the lens of asset classes can blind you to the underlying economic risk factors they share." — Source: [Capital Allocators]

- On benchmark constraints: "If you optimize a portfolio to beat a standard benchmark, you will inevitably end up owning a standard portfolio." — Source: [Williams College]

- On sizing constraints: "We would rather have a concentrated portfolio of our highest conviction ideas than a diluted book of average ones." — Source: [Capital Allocators]

Part 5: Navigating Market Cycles

- On interest rates: "Exiting investment-grade bonds in 2019 was a probability calculation based on the likelihood of rising rates, not an attempt to time the macro cycle." — Source: [Capital Allocators]

- On macro forecasting: "We do not build the portfolio around macro predictions because the variables are too complex to forecast with edge." — Source: [Capital Allocators]

- On zero-interest rate periods: "The zero-interest rate environment rewarded risk-taking indiscriminately, masking flaws in otherwise mediocre investment strategies." — Source: [Williams College]

- On market panics: "Volatility is only dangerous if you are forced to sell; for a perpetual endowment, it is primarily a mechanism for buying assets cheaply." — Source: [Capital Allocators]

- On regime changes: "When the cost of capital changes fundamentally, you have to reassess every assumption embedded in your illiquid book." — Source: [Capital Allocators]

- On cash reserves: "Holding enough cash to cover the college's short-term needs is what gives us the psychological freedom to stay invested during a crash." — Source: [Williams College]

- On defensive posturing: "You cannot build a defensive portfolio after the storm has already arrived; the preparation has to happen years in advance." — Source: [Capital Allocators]

- On chasing trends: "By the time a new asset class becomes universally popular among institutions, the excess returns have typically been arbitraged away." — Source: [Capital Allocators]

- On inflation protection: "Real assets only provide genuine inflation protection if they possess pricing power that can keep pace with rising input costs." — Source: [Williams College]

Part 6: Due Diligence and Underwriting

- On finding flaws: "Deep scrutiny of a manager's standard reporting often reveals the structural weaknesses they are trying to obscure." — Source: [Capital Allocators]

- On investment intuition: "Diligence instincts are honed by looking at hundreds of pitches and learning to spot the subtle inconsistencies in a manager's narrative." — Source: [Capital Allocators]

- On asking questions: "The most revealing moments in a manager meeting occur when you ask a basic question and receive an overly complicated answer." — Source: [Williams College]

- On reference checks: "Back-channel references are exponentially more valuable than the curated list of contacts a manager provides in their pitch deck." — Source: [Capital Allocators]

- On operational diligence: "A brilliant investment strategy will ultimately fail if the back-office infrastructure cannot support it." — Source: [Capital Allocators]

- On peer networks: "Sharing diligence notes with other endowments helps uncover blind spots that a single institution might miss on its own." — Source: [Williams College]

- On continuous underwriting: "Diligence does not end when the capital is deployed; we re-underwrite our conviction in every manager constantly." — Source: [Capital Allocators]

- On red flags: "High turnover among a manager's junior investment staff is usually a leading indicator of cultural decay at the firm." — Source: [Williams College]

- On conviction building: "True conviction is built slowly through repeated interactions, observing how a manager behaves in both favorable and hostile environments." — Source: [Capital Allocators]

Part 7: Real Assets and Fixed Income

- On fixed income utility: "Fixed income must serve a clear purpose in the portfolio, whether that is deflation protection, liquidity provision, or reliable income." — Source: [Capital Allocators]

- On ignoring consensus: "Managing the asset classes that others actively avoid is often where the most mispriced opportunities reside." — Source: [Capital Allocators]

- On real estate: "In real assets, the quality of the local operating partner is just as important as the macro thesis behind the geographic market." — Source: [Williams College]

- On energy investments: "The transition in energy markets requires underwriting managers who understand both the regulatory environment and the physical constraints of infrastructure." — Source: [Capital Allocators]

- On yield chasing: "Reaching for yield in lower-quality credit instruments is a reliable way to turn a safe allocation into a correlated equity risk." — Source: [Williams College]

- On fixed income constraints: "When starting yields are near zero, the mathematical reality is that traditional bonds can no longer fulfill their historical role in a portfolio." — Source: [Capital Allocators]

- On asset class evolution: "You have to be willing to structurally abandon a traditional asset class if the prospective forward returns no longer justify the capital lock-up." — Source: [Capital Allocators]

- On real asset illiquidity: "The illiquidity of physical assets is a feature, not a bug, provided it prevents the investment committee from selling at the bottom of a cycle." — Source: [Williams College]

- On resource scarcity: "Investing in real assets ultimately comes down to identifying areas where physical constraints limit future supply in the face of inelastic demand." — Source: [Capital Allocators]

Part 8: Institutional Knowledge and Career Growth

- On institutional memory: "An investment office's most valuable asset is the collective memory of how the portfolio responded to past crises." — Source: [Williams College]

- On the CIO transition: "Stepping into the CIO role requires shifting your perspective from finding the best individual investments to managing the aggregate risk of the institution." — Source: [Capital Allocators]

- On early career lessons: "Starting as an analyst teaches you the unglamorous mechanics of how cash actually moves and how returns are practically generated." — Source: [Capital Allocators]

- On honoring predecessors: "Inheriting a successful portfolio means respecting the architecture built by the founding CIO while gradually adapting it to new realities." — Source: [Williams College]

- On continuous learning: "The financial markets are a humbling mechanism; the moment you assume you have mastered them, you are preparing to lose money." — Source: [Capital Allocators]

- On committee management: "A successful CIO must translate complex portfolio mechanics into a language that a diverse board of trustees can easily understand and support." — Source: [Williams College]

- On legacy: "The ultimate measure of our work will be determined decades from now by the scholarships and facilities we were able to quietly fund." — Source: [Capital Allocators]

- On intellectual honesty: "You have to be willing to look at an investment that has lost money and admit whether your original thesis was wrong or simply early." — Source: [Capital Allocators]

- On the privilege of the role: "Managing a college endowment is fundamentally about stewarding the future of an institution, which makes the pressure entirely worthwhile." — Source: [Williams College]