Lessons from Alan Waxman

As co-founder and CEO of the $130 billion investment firm Sixth Street, Alan Waxman is known for his flexible, "go-anywhere" mandate and for criticizing private credit's asset-gathering "factory model." This compilation collects his views on structural risk, sports investing, and how to build an unconstrained team.

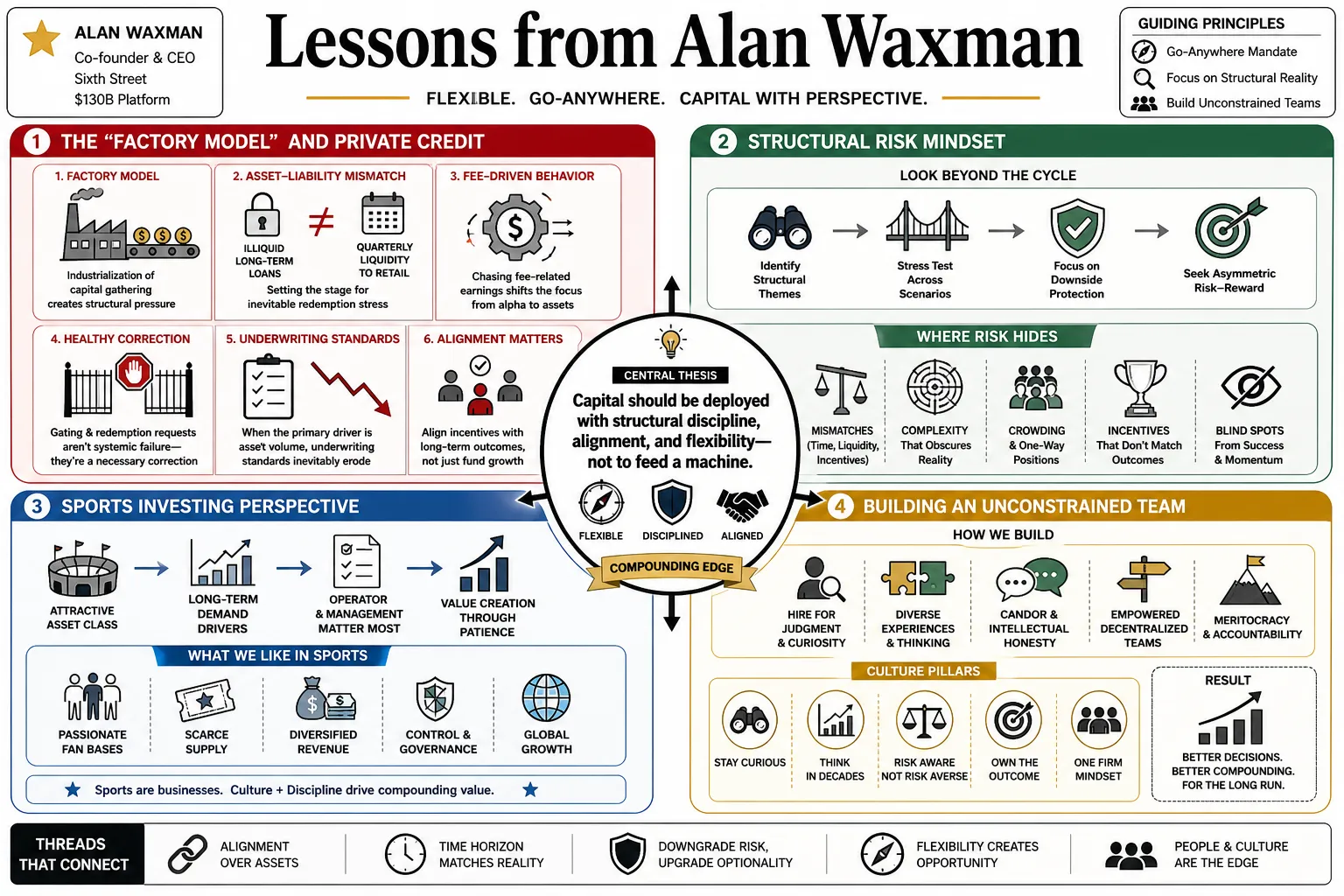

Part 1: The "Factory Model" and Private Credit

- On the factory model: "The industrialization of capital gathering inherently forces managers to deploy capital faster than the market might naturally support, creating structural pressure." — Source: [Invest Like the Best]

- On asset-liability mismatch: "When you pair illiquid, long-term loans with vehicles offering quarterly liquidity to retail investors, you are setting the stage for inevitable redemption stress." — Source: [Invest Like the Best]

- On fee-driven behavior: "Chasing fee-related earnings changes a firm's focus from generating pure alpha to simply feeding the asset-gathering machine." — Source: [Invest Like the Best]

- On private credit corrections: "The gating of funds and redemption requests in private credit aren't a systemic failure, but rather a healthy, necessary correction to an overheated model." — Source: [Invest Like the Best]

- On underwriting standards: "When the primary goal becomes scale and speed to satisfy the factory, the natural casualty is the rigor of your underwriting standards." — Source: [Invest Like the Best]

- On true private credit: "Real private credit is about bespoke, highly structured solutions for specific company needs, not mass-producing generic loans." — Source: [Invest Like the Best]

- On the retail wealth channel: "The aggressive push into retail wealth for private credit products requires a level of education and transparency regarding liquidity that the industry has not fully mastered." — Source: [Invest Like the Best]

- On market discipline: "Periods of stress are a gift because they flush out the tourists and force the industry back to the fundamentals of matching duration and risk." — Source: [Invest Like the Best]

- On scale versus alpha: "Growing AUM at all costs is the enemy of maintaining the flexibility required to actually generate differentiated returns." — Source: [Invest Like the Best]

- On structural fragility: "The factory model creates a fragility that is hidden during bull markets but becomes immediately apparent the moment capital flows reverse." — Source: [Invest Like the Best]

Part 2: Flexibility and "Go-Anywhere" Investing

- On investment mandates: "Having a completely flexible, go-anywhere mandate is the only way to ensure you aren't forced to invest in a specific asset class when it is fundamentally overvalued." — Source: [Goldman Sachs Exchanges]

- On cross-asset fluency: "You have to be able to evaluate a real estate deal, a software company, and a sports franchise through the same core lens of risk and return." — Source: [Goldman Sachs Exchanges]

- On unconstrained capital: "Unconstrained capital allows you to act as a liquidity provider when others are paralyzed by the strict definitions of their fund mandates." — Source: [Goldman Sachs Exchanges]

- On avoiding style boxes: "The moment you put your investment strategy into a rigid style box, you lose the ability to capture the best risk-adjusted returns in shifting markets." — Source: [Invest Like the Best]

- On capital as a solution: "We don't view capital just as money; we view it as a highly adaptable tool designed to solve a very specific problem for a management team." — Source: [Invest Like the Best]

- On market dislocations: "Flexibility is most valuable during market dislocations, because that is when traditional capital sources retreat to their most conservative silos." — Source: [Goldman Sachs Exchanges]

- On structural creativity: "You have to be willing to invent the security that a company needs, rather than forcing them to issue a security that already exists." — Source: [Invest Like the Best]

- On thematic investing: "We don't rely on macro predictions; we rely on micro-level flexibility to adapt to whatever macro environment actually materializes." — Source: [Goldman Sachs Exchanges]

- On being a partner: "A flexible mandate means we can sit across from a founder and ask 'What do you actually need?' instead of 'Here is what we sell.'" — Source: [Invest Like the Best]

Part 3: The Architecture of Sixth Street

- On firm independence: "Building Sixth Street meant creating an architecture where the investment team was entirely insulated from the pressures of asset gathering." — Source: [Invest Like the Best]

- On institutional DNA: "You cannot bolt on a flexible, cross-asset capability to a traditional private equity firm; it has to be the foundational DNA from day one." — Source: [Invest Like the Best]

- On the 'one-team' model: "Silos destroy information flow. We built a firm where compensation and culture strictly enforce a single, integrated team." — Source: [Goldman Sachs Exchanges]

- On shared information: "The most valuable asset in an investment firm isn't the capital, it's the speed and fidelity with which information moves across different sector teams." — Source: [Goldman Sachs Exchanges]

- On scaling a culture: "As you grow from a handful of partners to hundreds of employees, the challenge shifts from making good investments to systematizing how you make good decisions." — Source: [Invest Like the Best]

- On data-enabled investing: "We built our infrastructure to ensure that every investment decision is grounded in proprietary data, not just market consensus." — Source: [Sixth Street]

- On permanent capital: "Structuring our own capital base to be long-term and stable is what allows us to be patient when the rest of the market is panicking." — Source: [Invest Like the Best]

- On flat hierarchies: "In a complex transaction, the best idea has to win, regardless of whether it comes from a first-year analyst or a founding partner." — Source: [Goldman Sachs Exchanges]

- On alignment of interest: "True alignment means the investment team feels the pain of a loss just as acutely, if not more so, than the limited partners." — Source: [Invest Like the Best]

- On leaving a legacy: "The goal was never just to build a successful fund; it was to build an institution that would outlast its founders by institutionalizing our investment process." — Source: [Invest Like the Best]

Part 4: Sports, Media, and Live Events

- On sports franchises as assets: "Sports teams are no longer just vanity assets for billionaires; they are highly complex, IP-rich media companies that require institutional capital." — Source: [Bloomberg The Deal]

- On women's sports: "Investing in Bay FC and the NWSL wasn't just a cultural play; we saw a massive, mispriced opportunity where the underlying demand vastly outstripped the capitalization." — Source: [Bloomberg The Deal]

- On media rights: "The unbundling of traditional sports media rights creates a vacuum where flexible capital can help leagues and teams bridge the gap to direct-to-consumer models." — Source: [Bloomberg The Deal]

- On stadium infrastructure: "Modern sports venues are year-round real estate ecosystems, and financing them requires a blend of real estate, corporate credit, and media expertise." — Source: [Bloomberg The Deal]

- On minority stakes: "Taking a minority position in a franchise like the Spurs allows us to provide strategic capital without disrupting the operational control of legacy ownership." — Source: [Bloomberg The Deal]

- On fan engagement: "The monetization of the fan experience is still in its infancy globally, particularly when you look at European football clubs compared to US franchises." — Source: [Bloomberg The Deal]

- On the ecosystem approach: "You can't just buy a team; you have to invest in the entire ecosystem surrounding it—from local real estate to regional broadcasting." — Source: [Bloomberg The Deal]

- On live events: "The premium on live, unscripted content is only going up as the rest of the media landscape becomes increasingly fragmented and on-demand." — Source: [CNBC]

- On European football: "The financial structures of many European clubs are antiquated, creating a massive opportunity to provide modern, structured capital solutions to stabilize their operations." — Source: [Bloomberg The Deal]

Part 5: Identifying Alpha and Unitizing Risk

- On unitizing risk: "You have to break down every potential investment into its absolute smallest components of risk and assign a specific required return to each one." — Source: [Invest Like the Best]

- On defining alpha: "Alpha isn't just about picking the right company; it's about structuring your entry point so that you are mathematically protected if your thesis is wrong." — Source: [Invest Like the Best]

- On relative value: "The essence of our strategy is constantly comparing the risk-adjusted return of a senior secured loan in a software company to an equity stake in a real estate portfolio." — Source: [Goldman Sachs Exchanges]

- On margin of safety: "You build your margin of safety not by hoping for a good outcome, but by structuring the downside so tightly that a bad outcome is survivable." — Source: [Invest Like the Best]

- On downside protection: "We spend 90% of our time obsessing over how we can lose money, and let the upside largely take care of itself." — Source: [Invest Like the Best]

- On asymmetric bets: "The goal is to construct a portfolio of investments where the upside is equity-like, but the structural protections are credit-like." — Source: [Goldman Sachs Exchanges]

- On complexity premium: "We are highly attracted to situations that are too complex for traditional lenders and too debt-heavy for traditional private equity, because that is where the premium lives." — Source: [Invest Like the Best]

- On pricing risk: "If you can accurately price the risk that everyone else is running away from, you have a structural advantage in any market environment." — Source: [Goldman Sachs Exchanges]

- On illiquidity: "We demand to be heavily compensated for locking up our capital; if the illiquidity premium isn't there, we simply will not do the deal." — Source: [Invest Like the Best]

Part 6: Navigating Crisis and Complex Deals

- On the Airbnb investment: "During the peak of COVID panic, Airbnb didn't need a standard loan; they needed a bespoke capital solution delivered with extreme speed and certainty." — Source: [Invest Like the Best]

- On the Spotify deal: "Our work with Spotify demonstrated that even the most successful growth companies occasionally require complex, non-dilutive capital structures that traditional markets can't provide." — Source: [Invest Like the Best]

- On acting during panics: "When a crisis hits, the firms that have pre-positioned their capital and maintained a flexible mandate are the ones that dictate terms." — Source: [Goldman Sachs Exchanges]

- On speed as a differentiator: "In distressed situations, the ability to underwrite a billion-dollar check in a matter of days is a more significant competitive advantage than the cost of capital." — Source: [Invest Like the Best]

- On solving founder problems: "Founders in crisis don't care about your fund structure; they care about whether you can actually solve their immediate balance sheet problem without destroying their equity." — Source: [Invest Like the Best]

- On structural leverage: "We use structural protections—like seniority and covenants—rather than massive amounts of financial leverage to generate our returns in complex deals." — Source: [Invest Like the Best]

- On conviction: "You can't wait for the market to give you the 'all-clear' signal; by the time the consensus agrees an asset is safe, the alpha is already gone." — Source: [Goldman Sachs Exchanges]

- On managing distress: "Distressed investing isn't about buying cheap debt; it's about taking an active role in restructuring a fundamentally good business with a broken balance sheet." — Source: [Invest Like the Best]

- On the value of certainty: "In a highly volatile environment, capital certainty is the most valuable commodity we can offer a management team." — Source: [Invest Like the Best]

Part 7: Culture, Teamwork, and Leadership

- On culture as an antidote: "A strong, resilient culture is the only reliable antidote to the inevitable chaos of a rapidly changing business environment." — Source: [Goldman Sachs Exchanges]

- On winning as a team: "Individual brilliance is great, but over a long enough time horizon, a highly connected team will always beat a collection of brilliant individuals." — Source: [Goldman Sachs Exchanges]

- On Gregg Popovich's influence: "We drew heavy inspiration from Coach Popovich; the idea that 'the ball finds the open man' applies just as much to capital allocation as it does to basketball." — Source: [Goldman Sachs Exchanges]

- On connectedness: "The strength of a firm is measured not by its AUM, but by the density of connectedness and trust between its partners." — Source: [Goldman Sachs Exchanges]

- On hiring: "We look for people who are exceptionally smart but possess the low ego necessary to change their minds when the data proves them wrong." — Source: [Invest Like the Best]

- On intellectual honesty: "You have to foster an environment where admitting you were wrong about a thesis is celebrated as a vital part of the risk management process." — Source: [Invest Like the Best]

- On continuous improvement: "The moment a firm believes it has perfected its model is the exact moment it begins its decline." — Source: [Goldman Sachs Exchanges]

- On communication: "In times of stress, the volume and transparency of internal communication must increase exponentially to prevent silos from forming." — Source: [Goldman Sachs Exchanges]

- On defining success: "Financial returns are the output; the actual measure of success is the quality of the decisions being made by the team on a daily basis." — Source: [Invest Like the Best]

- On shared values: "You can teach the technical skills of investing, but you cannot teach the core values of integrity and extreme teamwork; you have to hire for them." — Source: [Goldman Sachs Exchanges]

Part 8: The Goldman Sachs Era and Career Lessons

- On early rejection: "Getting ghosted after 35 interviews, including four at Goldman Sachs, taught me that persistence and resilience are far more important than a linear resume." — Source: [Goldman Sachs Exchanges]

- On the Special Situations Group: "Running SSG at Goldman was the ultimate training ground; it was a pure meritocracy where we were forced to unearth value in the most complex corners of the market." — Source: [Invest Like the Best]

- On institutional training: "Goldman Sachs embedded a deep appreciation for risk management and the absolute necessity of rigorous, institutional-grade processes." — Source: [Goldman Sachs Exchanges]

- On non-linear paths: "The best investors rarely have a straight-line career; the detours and failures are what build the judgment required to price risk correctly." — Source: [Goldman Sachs Exchanges]

- On leaving a legacy platform: "Stepping away from the security of Goldman to build Sixth Street required a fundamental belief that our specific model of flexible capital could stand on its own." — Source: [Invest Like the Best]

- On organizational design: "The greatest lesson I took from my early career was observing how the structural design of a firm directly dictates the behavior of its investors." — Source: [Invest Like the Best]

- On managing one's career: "You have to be the primary architect of your own career; relying on an institution to passively manage your trajectory is a mistake." — Source: [Invest Like the Best]

- On personal organization: "Scaling yourself as a leader requires a rigid, almost obsessive personal organization system so that you can remain completely present in chaotic moments." — Source: [Invest Like the Best]

- On evaluating talent: "I learned early on to look past the pedigree and focus entirely on how a person processes complex information under pressure." — Source: [Goldman Sachs Exchanges]