Lessons from Ali Afridi

Ali Afridi is a venture capitalist and former Equal Ventures principal focused on digitizing legacy industries like insurance and manufacturing. He built SandHill.io to aggregate investment theses for founders and investors tracking market opportunities. This profile collects his perspectives on startup ideation, market cycles, and system-of-record software for the industrial economy.

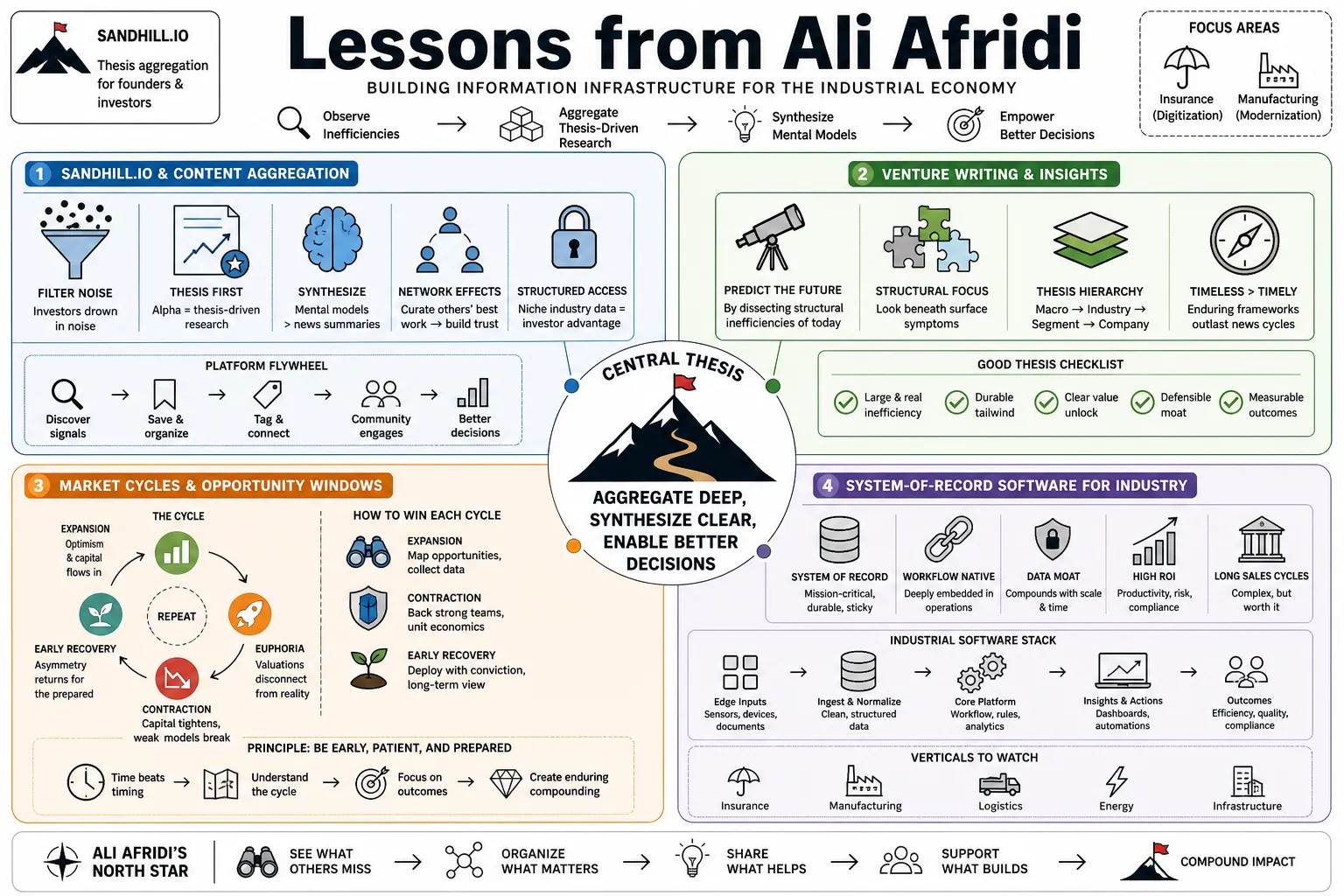

Part 1: SandHill.io and Content Aggregation

- On content curation: "Investors drown in noise; the real alpha lies in aggregating thesis-driven research rather than chasing daily funding announcements." — Source: [SandHill.io]

- On platform growth: "A newsletter scales when it moves from summarizing news to synthesizing mental models that founders can apply immediately." — Source: [Substack]

- On venture writing: "The best venture writing predicts the future by dissecting the structural inefficiencies of the present." — Source: [SandHill.io]

- On information asymmetry: "Capital is a commodity. The modern competitive advantage for early-stage investors is structured access to niche industry data." — Source: [Kauffman Fellows]

- On network effects in media: "Curating other people's high-quality work builds trust faster than publishing original, mediocre takes." — Source: [SandHill.io]

- On reading habits: "Founders who read deeply about tangential industries often discover the most durable business models." — Source: [Recess Labs]

- On thesis development: "A strong investment thesis requires publicly testing assumptions and iterating based on the friction you encounter in the market." — Source: [Equal Ventures]

- On community building: "An audience reads your content, but a community actively shares frameworks and challenges your underlying assumptions." — Source: [SandHill.io]

- On the creator economy for investors: "Venture capitalists must operate as niche media companies to attract the specific type of founder their fund requires." — Source: [Substack]

- On attention metrics: "High open rates matter less than the specific titles of the people forwarding the emails to their internal teams." — Source: [SandHill.io]

Part 2: Venture Capital Market Cycles

- On downturns: "Venture capital has been quietly outgrowing traditional definitions, making historical comparisons of market contractions less reliable." — Source: [Credistick]

- On cyclical behavior: "When public markets compress, early-stage investors retreat to perceived safe harbors, artificially inflating valuations in a few crowded sectors." — Source: [Equal Ventures]

- On capital deployment: "The most lucrative vintages are deployed when the broader institutional community questions the viability of the asset class." — Source: [Kauffman Fellows]

- On founder priorities: "During bull runs, founders optimize for valuation. In bear markets, the focus abruptly shifts to board composition and operating experience." — Source: [SandHill.io]

- On market corrections: "A reset in venture valuations forces companies to trade hyper-growth for unit economics, often saving the underlying business from itself." — Source: [Credistick]

- On liquidity events: "Extended periods of low IPO activity create secondary market pressure, forcing funds to engineer alternative exits to return capital." — Source: [SandHill.io]

- On dry powder: "Record levels of uncalled capital distort early-stage pacing, as funds feel obligated to deploy regardless of the macro environment." — Source: [Kauffman Fellows]

- On valuation metrics: "Revenue multiples expand and contract, but the underlying cost of customer acquisition remains the true constraint on scaling." — Source: [Equal Ventures]

- On category creation: "Market peaks fund multiple competitors in established categories; troughs fund the monopolists of completely new ones." — Source: [SandHill.io]

- On resilience: "Startups built with scarcity as a core principle outlast those heavily reliant on continuous, cheap venture rounds." — Source: [Credistick]

Part 3: InsurTech and Digital Transformation

- On structural catalysts: "2020 acted as a defining year for the InsurTech ecosystem, forcing legacy carriers to adopt digital distribution channels overnight." — Source: [Equal Ventures]

- On insurance value chains: "Digital transformation in insurance is shifting from front-end customer acquisition to overhauling backend underwriting systems." — Source: [Equal Ventures]

- On embedded insurance: "The future of the policy involves attaching coverage directly to the point of sale for high-value items, bypassing the traditional broker." — Source: [SandHill.io]

- On legacy infrastructure: "Incumbent insurers operate on old mainframes, creating a massive opportunity for startups to act as the modern API layer." — Source: [Equal Ventures]

- On data underwriting: "Traditional risk models rely on historical demographics; modern InsurTech uses real-time behavioral data to price policies dynamically." — Source: [Equal Ventures]

- On regulatory hurdles: "Navigating state-by-state compliance often serves as a larger moat for early-stage insurance startups than the core technology itself." — Source: [SandHill.io]

- On claims processing: "Automating the claims process reduces operational overhead and turns a typically adversarial customer interaction into a retention tool." — Source: [Equal Ventures]

- On commercial lines: "While consumer InsurTech receives the media attention, the commercial sector suffers from deeper inefficiencies and commands higher margins." — Source: [Equal Ventures]

- On the broker's role: "Technology will augment rather than replace the commercial broker, equipping them with software to handle complex, bespoke risks." — Source: [SandHill.io]

- On reinsurance: "Venture returns in insurance eventually require tackling the reinsurance layer, where the actual capital constraints of the industry reside." — Source: [Equal Ventures]

Part 4: Startup Ideation Models

- On systematic thinking: "Presenting mental models systematically helps investors dig into markets and identify opportunities more effectively than waiting for warm introductions." — Source: [Substack]

- On solving personal pain: "The best products often begin as internal tools built because the founders could not tolerate the existing market alternatives." — Source: [Recess Labs]

- On unbundling: "Taking a single feature from a massive enterprise software suite and building a specialized, superior product remains a viable path to product-market fit." — Source: [SandHill.io]

- On arbitrage: "Many successful business models simply take a pricing structure or distribution channel that works in one industry and apply it to a stagnant one." — Source: [Kauffman Fellows]

- On regulatory changes: "New legislation consistently creates temporary market confusion, opening a window for startups to sell compliance as a service." — Source: [SandHill.io]

- On technology transitions: "The shift from on-premise to cloud created a decade of opportunities; the current shift toward edge computing will follow a similar pattern." — Source: [Substack]

- On fragmented markets: "Industries with thousands of independent operators and no dominant player are primed for software platforms that aggregate supply." — Source: [Recess Labs]

- On demographic shifts: "Changing consumer habits among younger demographics often render existing legacy brands obsolete, leaving room for new entrants with native distribution." — Source: [SandHill.io]

- On simplicity: "If an idea sounds exhausting to explain to a potential customer, it will likely be impossible to sell at scale." — Source: [Substack]

Part 5: Digitizing the Industrial Economy

- On legacy sectors: "The industrial economy, including manufacturing and energy, remains largely underserved by modern software despite representing a massive portion of GDP." — Source: [Equal Ventures]

- On supply chain visibility: "The pandemic exposed how fragile global logistics networks are, accelerating the demand for software that tracks inventory in real time." — Source: [SandHill.io]

- On factory floor tech: "Selling software to a factory manager requires proving immediate ROI on the production line, bypassing traditional top-down IT procurement." — Source: [Equal Ventures]

- On predictive maintenance: "Replacing scheduled repairs with sensor-driven predictive maintenance saves heavy industries billions in unplanned downtime." — Source: [SandHill.io]

- On labor shortages: "Automation in manufacturing is driven less by the desire to cut costs and more by the physical inability to staff third-shift warehouse roles." — Source: [Equal Ventures]

- On energy transition: "Decarbonizing heavy industry requires both new hardware breakthroughs and the software layers to manage distributed, intermittent power sources." — Source: [SandHill.io]

- On construction tech: "Construction operates on paper and whiteboards. Software that simply connects the field worker to the back office creates immense immediate value." — Source: [Equal Ventures]

- On industrial APIs: "The next wave of industrial startups will build the middleware that allows proprietary machinery to communicate with modern cloud databases." — Source: [SandHill.io]

- On B2B marketplaces: "Procurement in heavy industry still happens via fax and phone; digital marketplaces for raw materials reduce friction and increase price transparency." — Source: [Equal Ventures]

Part 6: Systems of Record in Legacy Markets

- On core databases: "We are exploring new ideas for systems of record in sectors that have historically relied on Excel and institutional memory." — Source: [Substack]

- On data moats: "Once a startup becomes the system of record for a legacy business, the switching costs become prohibitive, creating a near-monopoly on that customer." — Source: [Equal Ventures]

- On wedge strategies: "You rarely sell a system of record directly. You sell a lightweight tool to solve an acute pain point, then slowly subsume the core database." — Source: [SandHill.io]

- On vertical orientation: "Vertical systems of record win by offering workflows tailored specifically to the quirks of a single industry, outcompeting generic horizontal tools." — Source: [Equal Ventures]

- On the API ecosystem: "A true system of record encourages third-party developers to build applications on top of it, transitioning from a product into a platform." — Source: [SandHill.io]

- On user adoption: "In legacy markets, the software must be intuitive enough for a workforce unaccustomed to technology, or the implementation will fail regardless of the feature set." — Source: [Equal Ventures]

- On embedded fintech: "After establishing the system of record, the natural expansion path involves capturing the payment flows and offering lending products to the user base." — Source: [Substack]

- On offline synchronization: "Software targeting field-heavy industries must function flawlessly offline and sync seamlessly when the worker returns to a service area." — Source: [SandHill.io]

- On customer success: "Deploying a system of record in a legacy market requires heavy, consultative onboarding to overcome deeply entrenched analog workflows." — Source: [Equal Ventures]

Part 7: Emerging Managers and Fund Dynamics

- On market positioning: "New fund managers must differentiate through specialized expertise or unique networks, as they cannot compete with established firms on capital alone." — Source: [Airstream Alpha]

- On fund sizing: "Raising too much capital in an early fund can destroy returns by forcing the manager to write larger checks into later, more competitive rounds." — Source: [Kauffman Fellows]

- On institutional investors: "Capital allocators look for emerging managers who can articulate a specific, repeatable mechanism for sourcing deals outside standard accelerator cohorts." — Source: [Cup of Zhou]

- On co-investing: "Building strong syndicates allows smaller funds to punch above their weight class and secures allocation in highly contested deals." — Source: [SandHill.io]

- On thesis drift: "The most common mistake for new managers is abandoning their core expertise to chase whatever consumer trend is currently dominating the tech press." — Source: [Airstream Alpha]

- On portfolio construction: "A concentrated portfolio requires extreme conviction and a high tolerance for failure, whereas a scattered approach dilutes both risk and potential upside." — Source: [Kauffman Fellows]

- On providing value: "Founders optimize for partners who can help recruit executive talent or secure initial enterprise pilot programs, discounting firms that only offer capital." — Source: [Cup of Zhou]

- On network building: "Formal scout programs push early-stage venture into the periphery, requiring managers to build relationships directly with operators rather than other investors." — Source: [SandHill.io]

- On reputation: "A venture firm's brand is entirely defined by the experiences of the founders in its portfolio, especially those whose companies failed." — Source: [Airstream Alpha]

Part 8: Founder Psychology and Team Building

- On product obsession: "The most successful founders possess an irrational fixation on a specific problem that borders on the unhealthy." — Source: [SandHill.io]

- On early hiring: "The first ten hires dictate the cultural DNA of the company; compromising on these roles to fill seats quickly is a fatal error." — Source: [Equal Ventures]

- On strategic pivoting: "Stubbornness is an asset until the market provides clear, repeated negative feedback. Knowing when to abandon the initial premise separates capable founders from failed ones." — Source: [Recess Labs]

- On self-awareness: "Great leaders understand their own operational deficits and aggressively hire executives who excel exactly where the founder struggles." — Source: [Kauffman Fellows]

- On handling rejection: "Fundraising requires processing hundreds of rejections without allowing the skepticism to erode the core vision of the product." — Source: [SandHill.io]

- On skill composition: "A founding team needs both the capability to build the product and the aggressive commercial instinct to force the market to care about it." — Source: [Equal Ventures]

- On scaling operations: "Culture transitions from implicit actions to explicit systems once a company crosses fifty employees; managing this transition requires deliberate internal communication." — Source: [Substack]

- On board dynamics: "Effective founders manage their board by providing bad news early and framing discussions around strategic roadblocks rather than routine operational updates." — Source: [Equal Ventures]

- On endurance: "Building a durable company is a decade-long exercise in managing personal burnout while maintaining the velocity expected by venture backers." — Source: [SandHill.io]