Lessons from Allison Fisch

Allison Fisch is President and Portfolio Manager at Pzena Investment Management, where she has spent over two decades as a deep value investor in global and emerging markets. Her approach hinges on a single distinction: telling a temporary setback from a terminal decline. This profile collects her insights on market psychology and the mechanics of contrarian investing.

Part 1: Value Investing Philosophy

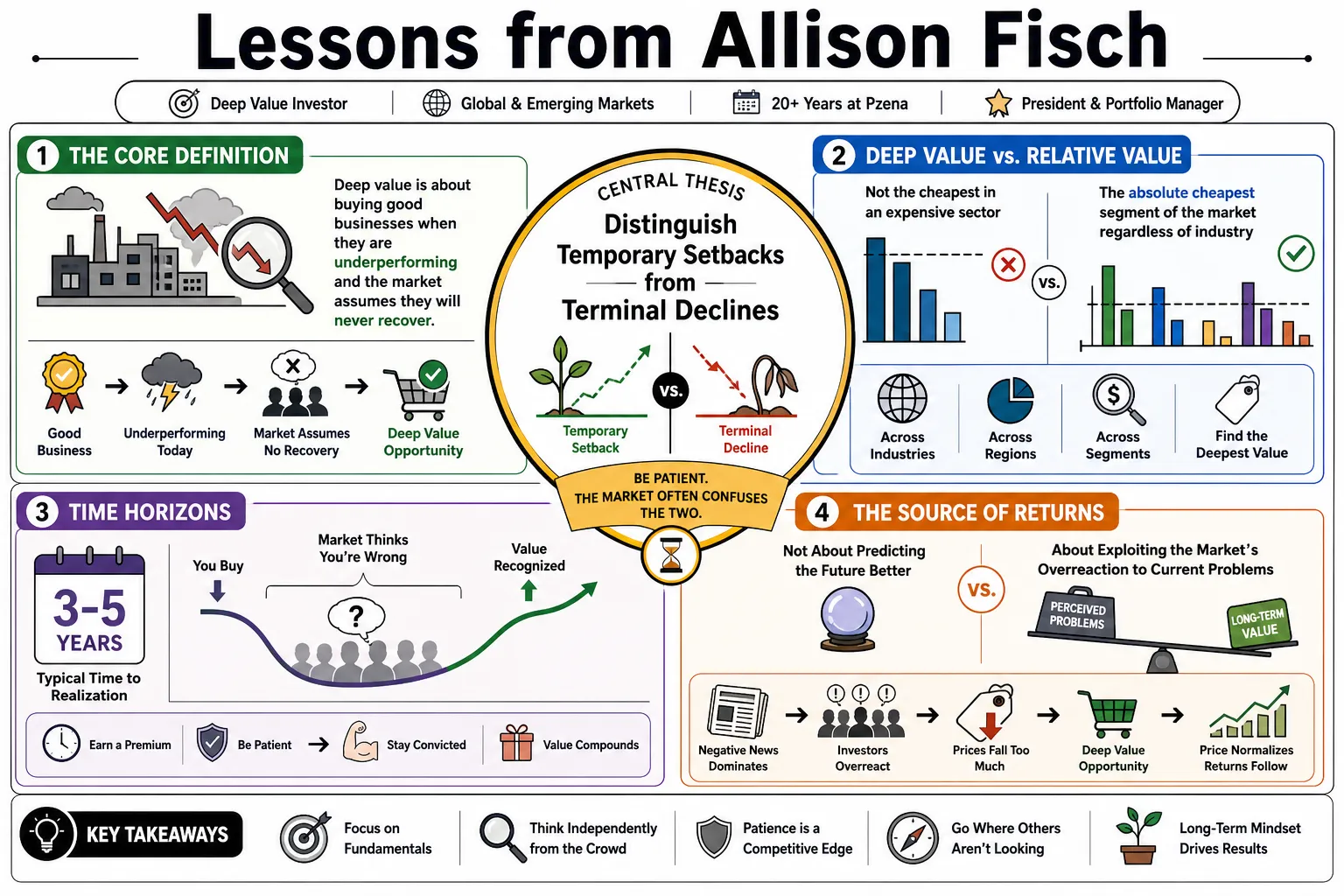

- On The Core Definition: "Deep value is about buying good businesses when they are underperforming and the market assumes they will never recover." — Source: Value Investing with Legends

- On Deep Value vs. Relative Value: "We avoid simply looking for the cheapest company in an expensive sector; we look for the absolute cheapest segment of the market regardless of industry." — Source: Pzena Investment Management

- On Time Horizons: "If you want to earn a premium, you must be willing to wait out the period where the market thinks you are wrong, which often spans three to five years." — Source: i3 Podcast

- On The Source of Returns: "Outperformance comes from exploiting the market's overreaction to current problems rather than predicting the future better than others." — Source: Livewire Interview

- On Market Behavior: "The strategy works because human emotion forces the average investor to sell when the news is worst." — Source: Value Investing with Legends

- On Mean Reversion: "Corporate profitability tends to revert to historical averages over time, driven by competitive forces and management interventions." — Source: PzenaPerspectives

- On Staying the Course: "The hardest part of investing is doing nothing when prices are falling but fundamentals remain intact." — Source: Pzena Investment Management

- On Process Over Outcomes: "A sound investment decision can still result in a short-term loss; the key is judging the decision by the research process rather than the immediate stock price." — Source: i3 Podcast

- On Patience: "You cannot force the market to recognize value on your schedule." — Source: Livewire Interview

- On Growth vs. Value: "Paying a high multiple for assumed future growth leaves little room for error if the business stumbles." — Source: Value Investing with Legends

Part 2: Emerging Markets Strategy

- On Emerging Market Volatility: "Volatility in developing economies creates steeper mispricings because capital flees faster during periods of stress." — Source: PzenaPerspectives

- On State-Owned Enterprises: "You have to carefully assess whether a government stakeholder aligns with minority shareholders or views the company as a public utility." — Source: Value Investing with Legends

- On Macro vs. Micro: "While macroeconomic trends matter in emerging markets, we focus entirely on how those trends affect the cash flows of specific businesses." — Source: i3 Podcast

- On Country Selection: "We do not allocate based on top-down country views; our geographic exposure is a byproduct of where we find the cheapest individual stocks." — Source: Pzena Investment Management

- On Currency Risk: "A weak local currency can sometimes benefit exporters, meaning currency depreciation is not uniformly bad for all equities in a country." — Source: Livewire Interview

- On Corporate Governance: "We demand a higher margin of safety when investing in jurisdictions with weaker shareholder protections." — Source: PzenaPerspectives

- On The EM Discount: "Emerging markets often trade at a persistent discount, so the goal is finding companies that will survive distress rather than waiting for the entire asset class to re-rate." — Source: Value Investing with Legends

- On Information Asymmetry: "Less analyst coverage in developing regions provides an advantage to investors willing to do primary fundamental research." — Source: i3 Podcast

- On China's Market Dynamics: "Regulatory shifts in China often cause indiscriminate selling, which can occasionally present opportunities to buy dominant franchises at distressed valuations." — Source: PzenaPerspectives

- On Diversification in EM: "Because political and economic risks are higher, we ensure our emerging market portfolios have broad exposure across different regions and sectors." — Source: Pzena Investment Management

Part 3: Identifying Sick vs. Terminal Companies

- On Temporary Disruption: "A sick company is one facing a fixable problem, like a cyclical downturn or a correctable management error." — Source: Value Investing with Legends

- On Structural Decline: "A terminal company suffers from permanent impairment, such as technological obsolescence or a permanent shift in consumer behavior." — Source: i3 Podcast

- On Balance Sheet Strength: "The primary difference between a sick business recovering and one going bankrupt is the liquidity available to survive the down cycle." — Source: Livewire Interview

- On Management in a Crisis: "We want to see executives acknowledging the core issue rather than blaming external factors." — Source: PzenaPerspectives

- On Assessing Moats: "A true competitive advantage becomes evident when a company maintains its market share despite severe industry headwinds." — Source: Pzena Investment Management

- On Earnings Power: "We model what the business will look like in five years assuming margins revert to their historical average." — Source: Value Investing with Legends

- On Industry Consolidation: "When an industry experiences a severe downturn, the strongest players usually acquire weaker rivals and emerge with better pricing power." — Source: i3 Podcast

- On Technology Risk: "We avoid cheap companies if their core product is actively being replaced by a superior, cheaper alternative." — Source: Livewire Interview

- On Catalysts: "We do not require an immediate catalyst to buy a stock; the cheap valuation itself is the margin of safety while we wait for fundamentals to improve." — Source: PzenaPerspectives

Part 4: Psychological Aspects of Investing

- On Human Emotion: "Fear and greed are constant, meaning the market will always misprice assets during periods of extreme stress." — Source: Value Investing with Legends

- On Herding Behavior: "It is professionally safer for an asset manager to fail doing what everyone else is doing than to fail standing alone." — Source: i3 Podcast

- On Comfort vs. Returns: "If a stock feels entirely comfortable to buy, the price likely reflects that safety and offers limited upside." — Source: Pzena Investment Management

- On Overreaction: "Markets consistently underestimate the ability of a good management team to cut costs and restructure a failing division." — Source: Livewire Interview

- On Institutional Imperative: "Many institutions are forced to sell underperforming assets due to strict risk limits, regardless of the underlying valuation." — Source: PzenaPerspectives

- On Anchoring Bias: "Investors often anchor to peak historical earnings, which can be dangerous if the industry structure has permanently worsened." — Source: Value Investing with Legends

- On Acknowledging Mistakes: "You must be willing to admit when your thesis is broken and sell, even if it means taking a substantial loss." — Source: i3 Podcast

- On Looking Foolish: "Value investors must accept looking out of touch during the final stages of a bull market." — Source: Livewire Interview

- On Maintaining Objectivity: "We rely on rigid screening processes to strip away the narrative and force us to look at the numbers objectively." — Source: Pzena Investment Management

Part 5: Risk Management and Portfolio Construction

- On Margin of Safety: "A low purchase price provides the necessary buffer for when our initial assumptions turn out to be overly optimistic." — Source: Value Investing with Legends

- On Position Sizing: "We size positions based on the range of potential outcomes, taking smaller bets on companies with binary regulatory risks." — Source: i3 Podcast

- On Sector Concentration: "Deep value investing often leads to concentrated sector bets because entire industries tend to fall out of favor at the same time." — Source: Pzena Investment Management

- On Downside Protection: "The best defense against permanent capital loss is avoiding companies with too much debt during a cyclical trough." — Source: Livewire Interview

- On Liquidity: "You have to match the liquidity of your portfolio to the time horizon of your capital base." — Source: PzenaPerspectives

- On Defining Risk: "Risk is the probability of a permanent loss of capital, whereas the market often incorrectly defines it as near-term price volatility." — Source: Value Investing with Legends

- On Portfolio Turnover: "Low turnover is a natural byproduct of our strategy, as it often takes years for an undervalued thesis to materialize." — Source: i3 Podcast

- On Scenario Analysis: "We spend more time evaluating the downside case than we do projecting the upside." — Source: Pzena Investment Management

- On Correlation in Crises: "During a severe panic, all correlations move to one; your only protection is owning assets that are already priced for distress." — Source: Livewire Interview

Part 6: Defining Normalized Earnings

- On Long-Term Averages: "Normalized earnings represent what a business can generate over a full economic cycle, ignoring peak booms and severe recessions." — Source: Value Investing with Legends

- On Adjusting for Cycles: "You cannot use trailing twelve-month earnings for a commodity producer; you must evaluate their profitability at mid-cycle prices." — Source: i3 Podcast

- On Profit Margins: "If a company's margins are currently half of their historical average, we investigate what specific structural changes would prevent them from recovering." — Source: Pzena Investment Management

- On Capital Allocation: "A management team's decision to reinvest in the business versus paying dividends heavily influences our view of future earnings power." — Source: Livewire Interview

- On Inflation Impacts: "Inflation distorts historical margins, forcing us to adjust our models to account for higher input costs and changing pricing power." — Source: PzenaPerspectives

- On Historical Precedents: "We look at how similar companies behaved in past industry downturns to estimate the duration of the current profit slump." — Source: Value Investing with Legends

- On Revenue Assumptions: "We generally assume flat or highly conservative revenue growth when calculating our normalized earnings estimates." — Source: i3 Podcast

- On Peer Comparisons: "Evaluating a company's cost structure relative to its direct competitors helps determine if their margin suppression is self-inflicted." — Source: Pzena Investment Management

- On Realistic Projections: "It is safer to assume a company will remain an average performer than to project a sudden operational miracle." — Source: Livewire Interview

Part 7: Contrarianism and Opportunity in Controversy

- On Embracing Controversy: "The best investments usually start with a headline that makes most people want to run the other way." — Source: Value Investing with Legends

- On the News Cycle: "The financial media amplifies short-term problems, creating the exact mispricings we seek to exploit." — Source: i3 Podcast

- On Market Consensus: "If everyone agrees a stock is a good idea, there is no one left to buy it and drive the price higher." — Source: Pzena Investment Management

- On Unloved Sectors: "Capital starvation in an unpopular sector eventually constrains supply, setting the stage for the next period of high profitability." — Source: Livewire Interview

- On Headline Risk: "You have to distinguish between a headline that damages short-term sentiment and one that indicates permanent economic impairment." — Source: PzenaPerspectives

- On the Price of Comfort: "Paying a premium for a stock with no immediate problems is often the most dangerous investment you can make." — Source: Value Investing with Legends

- On Independent Thinking: "You cannot rely on Wall Street research to find deep value; their models are typically built to extrapolate current trends." — Source: i3 Podcast

- On Panic Selling: "We view forced selling by distressed funds as an opportunity to provide liquidity at highly advantageous prices." — Source: Pzena Investment Management

- On Structural Skepticism: "Our default position is to question the market's assumption that a well-established business will suddenly disappear." — Source: Livewire Interview

- On the Value of Bad News: "Bad news is fully priced into a stock when the company reports terrible earnings and the share price goes up." — Source: PzenaPerspectives

Part 8: Career Journey and Perspectives

- On Consulting vs. Investing: "My background at McKinsey taught me how to break down complex business models, which transitioned perfectly into analyzing distressed companies." — Source: Value Investing with Legends

- On Team Dynamics: "A successful investment committee requires members who are willing to openly debate and challenge the primary analyst's assumptions." — Source: i3 Podcast

- On Mentorship: "Learning the nuances of value investing requires working alongside people who have successfully navigated multiple market cycles." — Source: Pzena Investment Management

- On Intellectual Honesty: "You have to separate your ego from your investment ideas and admit immediately when the facts change." — Source: Livewire Interview

- On Adapting to Markets: "The core philosophy of buying cheap assets never changes, but the metrics we use to evaluate businesses must evolve with the economy." — Source: PzenaPerspectives

- On Continuous Learning: "Every mistake is a permanent lesson in what to avoid during the next cycle." — Source: Value Investing with Legends

- On Firm Culture: "You need an institutional structure that protects portfolio managers from client pressure during periods of short-term underperformance." — Source: i3 Podcast

- On Long-Term Alignment: "Aligning employee compensation with long-term fund performance ensures that the team focuses on five-year outcomes rather than quarterly results." — Source: Pzena Investment Management

- On the Future of Value: "As long as human beings dictate market prices based on fear and greed, disciplined value investing will continue to work." — Source: Livewire Interview