Lessons from Amit Wadhwaney

Amit Wadhwaney co-founded Moerus Capital Management following a two-decade tenure at Third Avenue Management. He takes a strict, asset-based approach to deep value investing, favoring balance sheet strength and corporate survival over macroeconomic guesswork. This profile covers his strategies for valuing hard assets and buying out-of-favor companies in international markets.

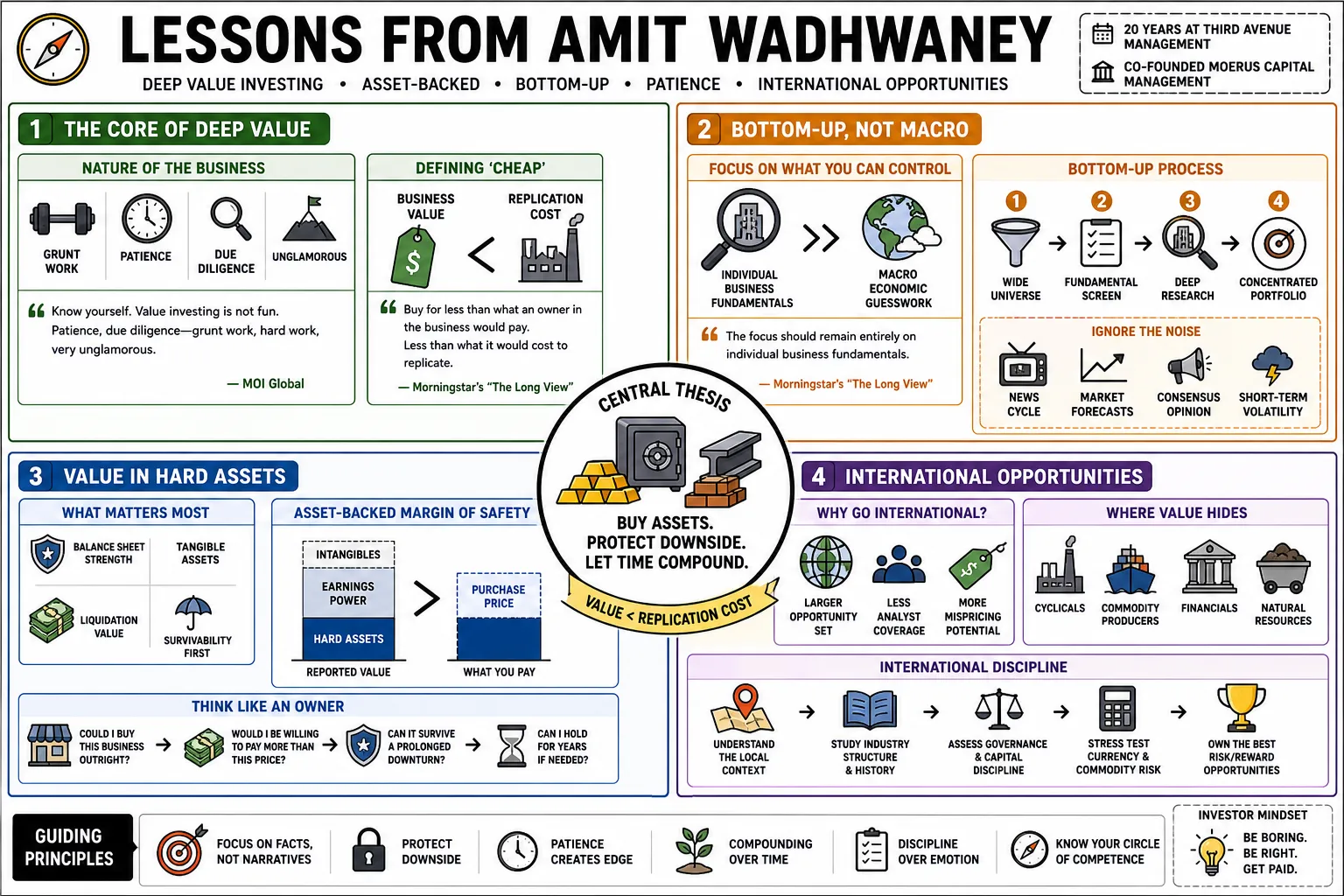

Part 1: The Core of Deep Value

- On the nature of the business: "It is important that anybody who goes down this path be aware of a few things. Know yourself. There's certain kinds of things that value investors do which are not fun. Fun in terms of patience, fun in terms of due diligence. This is grunt work, this is hard work, it's very unglamorous." — Source: MOI Global

- On defining 'cheap': "Buying cheap has a number of attractions to it... it's less than what somebody who is in the business would be willing to pay for that business. And that's quite important that you are buying a business less than for what you could replicate it for." — Source: Morningstar's "The Long View"

- On bottom-up investing: "The focus should remain entirely on individual business fundamentals rather than trying to construct a portfolio based on top-down macroeconomic predictions." — Source: Value Investing with Legends

- On market mishaps: "Mishaps at the level of a company, a good company slips on a banana peel. It happens... We wind up with companies that have amazing market positions and great businesses, and a bunch of things happen to them at one time." — Source: Morningstar's "The Long View"

- On boring environments: "Boring is good. As an investor, you don't necessarily want excitement; you want predictability and the opportunity to buy assets at a discount." — Source: MOI Global

- On being unconstrained: "An ocean-wide mandate allows an investor to look across developed, emerging, and frontier markets to find undervalued assets wherever they may be hiding." — Source: Moerus Capital Management

- On patience: "The investment process requires a willingness to wait for years for a thesis to play out, recognizing that the market timeline rarely aligns with the intrinsic value realization timeline." — Source: The Accent Podcast

- On identifying discounts: "True deep value is found when the market price reflects a structural failure, but the reality is merely a temporary, fixable problem." — Source: Value Invest New York 2026

- On rejecting the glamor: "Value investing requires turning away from exciting, fast-growing industries in favor of overlooked or out-of-favor sectors where expectations are completely washed out." — Source: Moerus Capital Management Investor Memos

Part 2: Defining Risk and Survivability

- On survivability: "Ensuring a company has the financial strength to weather near-term challenges is the absolute core of the risk management process; if a company cannot survive, its long-term value is zero." — Source: Morningstar's "The Long View"

- On permanent loss of capital: "Risk is not short-term share price volatility, which is often an opportunity. True risk is the permanent destruction of capital." — Source: Moerus Worldwide Value Fund Reports

- On downside protection: "The goal is to seek opportunities where the potential for loss is strictly mitigated by the price paid relative to the hard tangible value of the business assets." — Source: Value Investing with Legends

- On balance sheet strength: "A strong balance sheet is the ultimate margin of safety, providing a company with the staying power needed to outlast cyclical downturns and operational missteps." — Source: MOI Global

- On market volatility: "Short-term market fluctuations should be viewed as a mechanism that misprices assets, providing the disciplined investor with entry points rather than reasons to panic." — Source: Moerus Capital Management Investor Memos

- On risk aversion: "Maintaining a highly risk-averse posture is essential. The investment process must constantly ask what can go wrong before considering how much can be made." — Source: The Accent Podcast

- On structural integrity: "When evaluating a distressed business, one must differentiate between a company facing a liquidity event and one facing outright insolvency." — Source: Value Invest New York 2026

- On conservative assumptions: "Stress-testing a company's financials under adverse scenarios is the only way to ensure its survivability during periods of extreme economic stress." — Source: bvc Direct Podcast

- On saying no: "The habit of saying no to the vast majority of investment ideas is an asset, acting as the primary filter against taking on unnecessary risk." — Source: Moerus Capital Management

Part 3: Asset-Based Valuation

- On the here and now: "Rather than relying on projections of future earnings or cash flows, which are inherently unpredictable, the focus should be on the company's value today." — Source: MOI Global

- On Net Asset Value: "The goal is to estimate a company's net asset value using conservative bedrock assumptions, aiming to buy businesses at a significant discount to what they might be worth if their assets were sold today." — Source: MOI Global

- On avoiding forecasts: "Cash flow projections inherently require predicting the future, a practice fraught with error. Tangible assets provide a much firmer foundation for valuation." — Source: Value Investing with Legends

- On hard assets: "Focusing on tangible assets like real estate and natural resources provides a concrete floor to valuation that intangibles cannot offer." — Source: Moerus Capital Management Investor Memos

- On replacement cost: "It is essential to determine what it would cost a competitor to replicate a business from scratch, as buying below this cost offers a profound margin of safety." — Source: Morningstar's "The Long View"

- On earnings quality: "Current earnings can be manipulated or distorted by cyclical factors, whereas a rigorously analyzed balance sheet reveals the true economic reality of the enterprise." — Source: MOI Global

- On bedrock assumptions: "Valuation models must be built on the most conservative possible assumptions about asset realizability, ensuring that any surprises are positive ones." — Source: Moerus Capital Management

- On hidden value: "Often, real estate or other long-held assets are carried on the balance sheet at historical cost, masking their true current market value from superficial screening tools." — Source: Value Invest New York 2026

- On liquidation value: "While not necessarily predicting a liquidation, understanding what the company would fetch in a theoretical wind-down anchors the downside risk assessment." — Source: The Accent Podcast

- On balance sheet primacy: "The balance sheet is the most important financial statement for a deep value investor, as it dictates the company's ability to endure and adapt." — Source: Value Investing with Legends

Part 4: Macro Awareness vs. Macro Forecasting

- On being macro myopic: "Macro myopic, but macro aware. Avoid using macroeconomic forecasts to drive investment decisions, but understand how macro factors impact fundamental operations." — Source: MOI Global

- On the failure of forecasting: "Macroeconomic forecasting often fails investors because it layers one set of unpredictable variables on top of another." — Source: Morningstar's "The Long View"

- On macro as a disqualifier: "Macroeconomic conditions should be viewed as potential disqualifiers (reasons not to invest in a specific country or sector) rather than reasons to buy." — Source: Value Investing with Legends

- On day-to-day operations: "The focus must remain on how macro factors affect the day-to-day reality of a business, such as input costs and currency exposure, rather than predicting GDP growth." — Source: MOI Global

- On bottom-up primacy: "If a business is cheap enough and strong enough on a bottom-up basis, it should be able to withstand various macroeconomic environments." — Source: Moerus Worldwide Value Fund Reports

- On inflation protection: "Buying tangible assets at a discount is one of the most effective ways to protect capital against the eroding effects of inflation without having to explicitly forecast inflation rates." — Source: Moerus Capital Management Investor Memos

- On interest rates: "While interest rates affect the cost of capital, buying companies with strong balance sheets minimizes reliance on debt markets and insulates them from rate shocks." — Source: The Accent Podcast

- On geopolitical risk: "Geopolitical events often create the dislocations that allow for the purchase of assets at a discount, provided the specific business is not directly threatened with expropriation." — Source: bvc Direct Podcast

- On ignoring the noise: "Investors spend too much time worrying about the Federal Reserve and not enough time reading annual reports and understanding the assets they own." — Source: Value Investing with Legends

Part 5: Navigating Global and Emerging Markets

- On global heterogeneity: "Asia is not one big ball of wax. It's a very heterogeneous collection of countries and markets." — Source: MOI Global

- On Japanese equities: "Japan is making its own tottering attempts at a comeback and deep down I am mildly optimistic. I think some degree of shock therapy has been administered." — Source: MOI Global

- On the promise of India: "India's got a lot of promise, a lot of traction... For the first time in a number of years, actually decades, there seems to be hope for a change." — Source: MOI Global

- On unconstrained mandates: "Looking outside of domestic markets is essential because the cheapest assets are rarely found in the most popular or heavily trafficked geographies." — Source: Moerus Capital Management

- On emerging market volatility: "The inherent volatility in emerging markets frequently causes stock prices to decouple entirely from underlying asset values, creating prime opportunities." — Source: bvc Direct Podcast

- On local partnerships: "Understanding local laws and the motivations of controlling families is essential before investing abroad." — Source: Value Invest New York 2026

- On currency risk: "While currency fluctuations are a reality of global investing, buying assets at a sufficiently large discount can provide a buffer against adverse foreign exchange movements." — Source: The Accent Podcast

- On frontier markets: "Frontier markets often feature completely ignored companies with dominant local market shares, trading at valuations unseen in developed economies." — Source: Moerus Worldwide Value Fund Reports

- On cross-border comparisons: "A truly global approach allows an investor to compare a cement company in Colombia with one in Indonesia, selecting the absolute cheapest and safest option available worldwide." — Source: Value Investing with Legends

- On geographic bias: "Investors must actively fight their home-country bias, recognizing that excellent businesses exist everywhere, often at much more attractive valuations than domestic counterparts." — Source: Morningstar's "The Long View"

Part 6: Finding Opportunity in Trouble

- On crises: "In other words, to us, Trouble is Opportunity." — Source: Moerus Capital Management Investor Memos

- On the 'Problem' thesis: "The most attractive investments are often those that are cheap for a reason. These companies face temporary, fixable challenges rather than structural failures." — Source: Value Invest New York 2026

- On corporate restructuring: "Companies undergoing massive internal restructuring or distressed assets often present the best entry points, as the market abhors uncertainty." — Source: Value Invest New York 2026

- On cyclical troughs: "The optimal time to buy resource-intensive businesses is when commodity prices have collapsed and the sector is universally despised." — Source: Moerus Capital Management Investor Memos

- On reputational damage: "A company suffering from temporary reputational damage often sees its stock price punished far in excess of the actual long-term impairment to its business." — Source: MOI Global

- On forced selling: "Market panics or institutional mandates often lead to forced selling, allowing prepared investors to step in and provide liquidity at heavily discounted prices." — Source: Morningstar's "The Long View"

- On contrarianism: "If everyone is comfortable with an investment thesis, it is likely already priced in. True bargains are found where others are afraid to look." — Source: The Accent Podcast

- On complexity: "Complex corporate structures or convoluted balance sheets frequently scare off lazy analysts, leaving mispriced assets for those willing to do the intensive work to untangle them." — Source: Value Investing with Legends

- On fixing the fixable: "Differentiating between a broken business model and a fundamentally sound business burdened by bad management or too much debt is the key to distressed investing." — Source: bvc Direct Podcast

Part 7: Patience and the Psychology of Investing

- On the requirement of patience: "Deep value investing is an exercise in extreme patience; one must be willing to sit on an undervalued asset for years before the market recognizes its worth." — Source: MOI Global

- On ignoring the crowd: "The investment business is full of people trying to chase the next big trend. The value investor must actively tune out this noise and stick to the discipline." — Source: MOI Global

- On emotional discipline: "The ability to remain calm and unemotional when a holding declines in price is a rare but necessary trait, provided the thesis remains intact." — Source: The Accent Podcast

- On the glamor of growth: "Acknowledging that growth investing is more glamorous helps set expectations; deep value is about grinding through documents, not predicting the future." — Source: MOI Global

- On conviction: "True conviction is not stubbornness. It is the confidence derived from exhaustive fundamental analysis that allows an investor to hold firm during drawdowns." — Source: Morningstar's "The Long View"

- On the fear of missing out: "Avoiding the temptation to participate in speculative bubbles requires a rigid adherence to one's valuation framework, even when looking foolish in the short term." — Source: Value Investing with Legends

- On mental models: "An investor must develop a framework that automatically defaults to seeking a margin of safety rather than seeking maximum upside." — Source: bvc Direct Podcast

- On continuous learning: "The markets are constantly evolving, and an investor must maintain the humility to learn from mistakes and adapt their application of core principles to new environments." — Source: MOI Global

- On holding cash: "Cash is not a drag on performance. It is a call option on future opportunity and the natural byproduct of a disciplined refusal to overpay." — Source: Moerus Worldwide Value Fund Reports

- On independent thinking: "It is essential to arrive at conclusions independently, relying on primary documents like annual reports rather than Wall Street research notes." — Source: Moerus Capital Management Investor Memos

Part 8: Contrarian Independence and Portfolio Construction

- On benchmark hugging: "A portfolio should look nothing like the popular market indices. True value requires building a highly idiosyncratic collection of assets." — Source: Moerus Capital Management Investor Memos

- On concentration: "While diversification is necessary, an over-diversified portfolio simply mimics the market. Capital should be concentrated in the absolute best ideas where the margin of safety is widest." — Source: The Accent Podcast

- On position sizing: "Position sizes must be dictated not by potential upside, but by the degree of downside protection and the overall quality of the underlying assets." — Source: Value Investing with Legends

- On index correlation: "Seeking assets that are entirely uncorrelated with popular technology indices is essential for true portfolio diversification." — Source: Moerus Capital Management Investor Memos

- On selling: "The decision to sell should be triggered by the price approaching intrinsic value or a fundamental deterioration in the asset base, not by macroeconomic fears or market sentiment." — Source: Morningstar's "The Long View"

- On institutional imperatives: "The pressure to deliver smooth quarterly returns is the enemy of deep value investing. True long-term performance requires a structure that allows for lumpy returns." — Source: MOI Global

- On ignoring peer pressure: "A successful contrarian must be comfortable looking completely wrong for extended periods while the broader market pursues expensive fads." — Source: Value Invest New York 2026

- On capital preservation first: "The entire portfolio construction process must be geared toward the avoidance of permanent capital loss as the absolute highest priority." — Source: Moerus Worldwide Value Fund Reports

- On the aggressive conservative approach: "The goal is to be a distinguished aggressive conservative investor: aggressive in where one looks for value, but intensely conservative in the price paid and the assumptions used." — Source: Mutual Fund Observer