Lessons from Ana Marshall

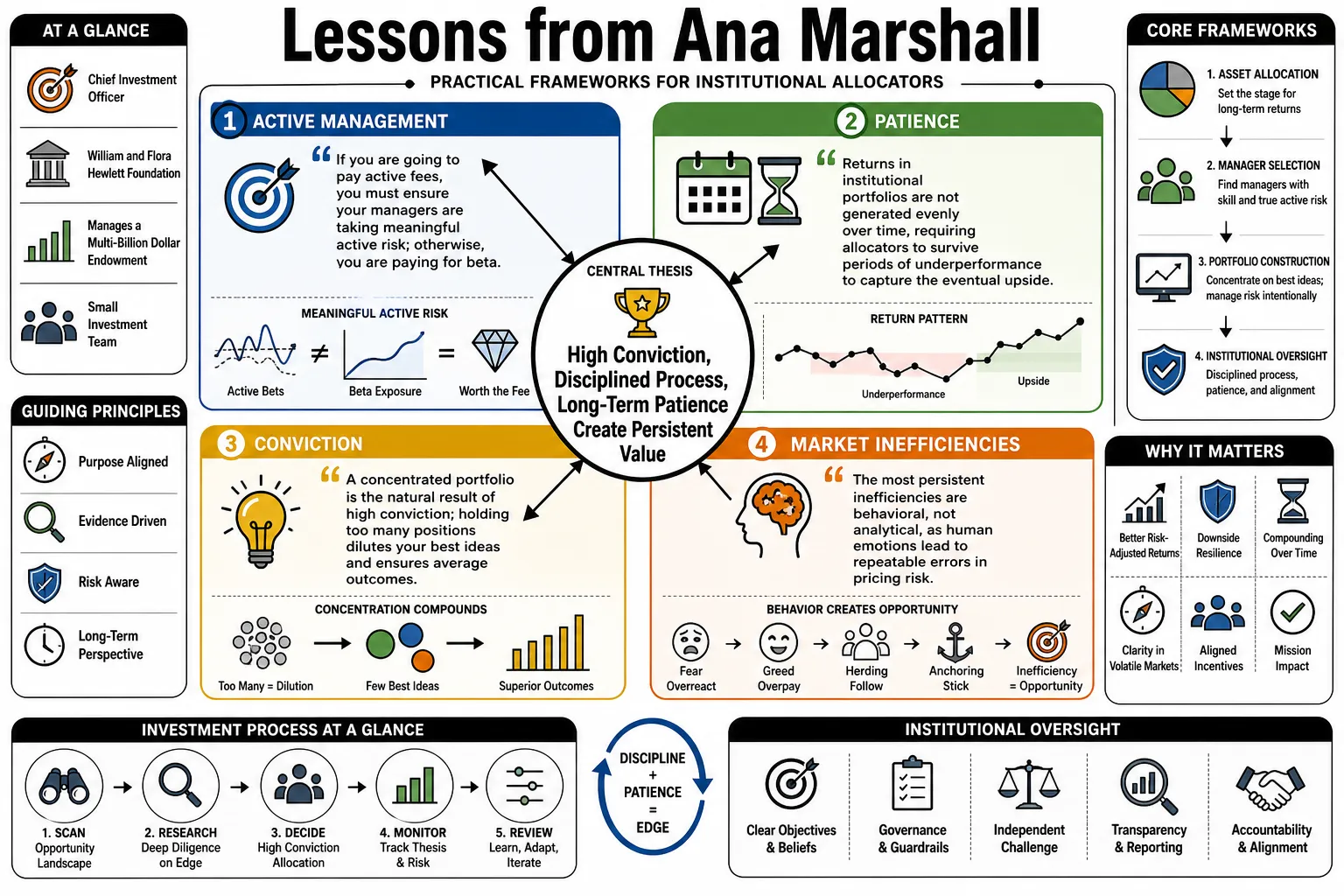

Ana Marshall is the Chief Investment Officer of the William and Flora Hewlett Foundation, where she has managed its multi-billion dollar endowment since 2011. She is known for her disciplined approach to concentrated portfolios and her preference for a small investment team. This profile details her practical frameworks for asset allocation, manager selection, and institutional oversight to explain why her methods matter to modern allocators.

Part 1: Investment Philosophy

- On Active Management: "If you are going to pay active fees, you must ensure your managers are taking meaningful active risk; otherwise, you are paying for beta." — Source: [Capital Allocators Episode 360]

- On Patience: "Returns in institutional portfolios are not generated evenly over time, requiring allocators to survive periods of underperformance to capture the eventual upside." — Source: [The Climb to Investment Excellence]

- On Conviction: "A concentrated portfolio is the natural result of high conviction; holding too many positions dilutes your best ideas and ensures average outcomes." — Source: [Hewlett Foundation CIO Profile]

- On Market Inefficiencies: "The most persistent inefficiencies are behavioral, not analytical, as human emotions lead to repeatable errors in pricing risk." — Source: [Institutional Investor Profile]

- On Complexity: "Adding complexity to a portfolio rarely adds return, but it consistently adds cost and opacity." — Source: [The Climb to Investment Excellence]

- On Time Horizons: "An endowment’s primary advantage is its perpetual time horizon, which allows the portfolio to absorb illiquidity and volatility that others cannot tolerate." — Source: [Capital Allocators Episode 360]

- On Decision Making: "Good investment decisions require stripping away noise and focusing on the three or four variables that actually drive an asset's outcome." — Source: [CFA Society Chicago]

- On Absolute Returns: "While benchmarks matter for context, foundations spend absolute dollars, meaning the portfolio must ultimately generate real purchasing power." — Source: [The Climb to Investment Excellence]

- On Structural Advantages: "Identifying whether your edge is analytical, informational, or behavioral is a prerequisite before committing capital to a specific strategy." — Source: [Hewlett Foundation CIO Profile]

Part 2: Team Building and Culture

- On Team Size: "A small investment team forces clear communication, limits bureaucracy, and ensures that everyone understands the entire portfolio rather than a single silo." — Source: [Institutional Investor Profile]

- On Hiring: "We look for individuals with high intellectual curiosity and low ego, because markets will eventually humble anyone who lacks either." — Source: [Capital Allocators Episode 360]

- On Debate: "An effective investment culture requires constructive conflict, where junior team members feel obligated to challenge the assumptions of the CIO." — Source: [The Climb to Investment Excellence]

- On Generalists: "Operating as a team of generalists prevents turf wars over capital allocation and keeps the focus on the best returns across the entire portfolio." — Source: [CFA Society Chicago]

- On Compensation: "Incentives must be aligned with long-term fund performance rather than short-term individual asset class benchmarks." — Source: [Hewlett Foundation CIO Profile]

- On Mentorship: "Training the next generation of investors involves giving them real capital to allocate and the freedom to make reversible mistakes." — Source: [The Climb to Investment Excellence]

- On Retention: "People stay in demanding investment roles when they feel a strong connection to the foundation's mission and see a clear path for intellectual growth." — Source: [Capital Allocators Episode 360]

- On Decision Fatigue: "Protecting the team's time from low-probability manager pitches is necessary to maintain focus on existing relationships and high-conviction ideas." — Source: [Institutional Investor Profile]

- On Diversity of Thought: "Building a team with different professional backgrounds and life experiences prevents groupthink during market extremes." — Source: [CFA Society Chicago]

- On Accountability: "Post-mortems on investment decisions should focus on the quality of the process rather than the luck of the outcome." — Source: [The Climb to Investment Excellence]

Part 3: Portfolio Construction

- On Asset Allocation: "Asset allocation is a blunt instrument; its primary purpose is to ensure you survive severe market drawdowns with enough capital to rebalance." — Source: [Capital Allocators Episode 360]

- On Liquidity: "Illiquidity is a budget that must be spent carefully, as being forced to sell private assets in a downturn destroys long-term compounding." — Source: [The Climb to Investment Excellence]

- On Correlation: "During a true financial panic, correlations across most asset classes converge to one, making liquidity the only reliable diversifier." — Source: [Institutional Investor Profile]

- On Rebalancing: "Mechanical rebalancing is painful because it forces you to sell what has done well and buy what feels terrible, which is exactly why it works." — Source: [Hewlett Foundation CIO Profile]

- On Alternatives: "Private equity and venture capital only make sense if the manager can consistently deliver a premium that compensates for the multi-year lockup of capital." — Source: [CFA Society Chicago]

- On Position Sizing: "If an investment is not large enough to impact the overall portfolio return, it is not worth the monitoring cost." — Source: [The Climb to Investment Excellence]

- On Currency Risk: "For a US-based foundation, unhedged foreign currency exposure introduces unnecessary volatility that rarely compensates the portfolio over the long term." — Source: [Capital Allocators Episode 360]

- On Fixed Income: "The role of high-quality fixed income is not to generate high returns, but to provide dry powder when equities decline." — Source: [Institutional Investor Profile]

- On Over-Diversification: "Holding fifty different equity managers is an expensive way to replicate an index fund." — Source: [The Climb to Investment Excellence]

- On Pacing: "Consistent deployment pacing in private markets is more effective than trying to time vintages based on macroeconomic forecasts." — Source: [Hewlett Foundation CIO Profile]

Part 4: Risk Management

- On Defining Risk: "Risk is not volatility; risk is the permanent impairment of capital and the failure to fund the foundation's grant-making." — Source: [Capital Allocators Episode 360]

- On Drawdowns: "Understanding how much pain a portfolio can endure requires stress-testing the psychological resilience of the board alongside the financial numbers." — Source: [The Climb to Investment Excellence]

- On Leverage: "Implicit leverage within underlying portfolio companies is often the hidden variable that turns a moderate economic slowdown into a severe capital loss." — Source: [CFA Society Chicago]

- On Tail Risks: "Preparing for low-probability events means building a margin of safety into asset valuation rather than relying on complex derivative hedges." — Source: [Institutional Investor Profile]

- On Concentration Risk: "Concentration requires a much deeper level of ongoing underwriting, as mistakes in a concentrated portfolio cannot be easily absorbed." — Source: [The Climb to Investment Excellence]

- On Liquidity Modeling: "Stress tests must assume that capital calls will accelerate and distributions will halt exactly when public markets are plunging." — Source: [Hewlett Foundation CIO Profile]

- On Valuation: "Relying on marked-to-model valuations in private markets during public market sell-offs creates a false sense of security." — Source: [Capital Allocators Episode 360]

- On Tracking Error: "Allocators must be willing to look wrong for extended periods, as low tracking error usually indicates a lack of active conviction." — Source: [CFA Society Chicago]

- On Operational Risk: "The most devastating losses often come from operational failures or fraud rather than poor investment strategy, making operational due diligence non-negotiable." — Source: [The Climb to Investment Excellence]

Part 5: Manager Selection and Partnerships

- On Sourcing: "The best investment managers rarely market themselves aggressively, meaning allocators must rely on deep networks to find true talent." — Source: [Institutional Investor Profile]

- On Alignment: "We look for managers who have the majority of their own liquid net worth invested alongside our capital." — Source: [Hewlett Foundation CIO Profile]

- On Capacity: "Asset growth is the enemy of performance; we prefer partners who explicitly constrain their fund sizes to maintain their edge." — Source: [Capital Allocators Episode 360]

- On Track Records: "Past performance is useful only as a forensic tool to understand how a manager behaves under pressure, not as a predictor of future returns." — Source: [The Climb to Investment Excellence]

- On Relationships: "A true partnership means having open conversations when performance is poor, without the manager fearing immediate redemption." — Source: [CFA Society Chicago]

- On Edge: "If a manager cannot clearly articulate why the market is offering them a mispriced asset, their edge is likely temporary or nonexistent." — Source: [Institutional Investor Profile]

- On Firm Culture: "High turnover at an investment firm is a red flag, as it usually indicates misaligned compensation or a toxic leadership structure." — Source: [The Climb to Investment Excellence]

- On Fees: "We are willing to pay for genuine alpha, but we aggressively negotiate structures that prevent managers from getting wealthy on management fees alone." — Source: [Capital Allocators Episode 360]

- On Terminations: "The decision to end a relationship should be based on a drift in strategy or a change in the team, rather than a short-term period of underperformance." — Source: [Hewlett Foundation CIO Profile]

- On Co-investments: "Co-investing is a way to deploy capital efficiently, but it requires the internal team to have the speed and expertise to underwrite specific deals." — Source: [The Climb to Investment Excellence]

Part 6: Governance and Institutional Alignment

- On Board Dynamics: "The CIO's most important job is managing the board, ensuring they understand the strategy well enough to stay the course during a crisis." — Source: [Institutional Investor Profile]

- On Mission: "Every basis point of return translates directly into grant dollars, grounding our daily work in a profound sense of institutional purpose." — Source: [Hewlett Foundation CIO Profile]

- On Policy Portfolios: "The policy benchmark should reflect the foundation's risk tolerance and spending needs, not a generic peer average." — Source: [The Climb to Investment Excellence]

- On Communication: "Translating complex investment strategies into clear language builds trust with stakeholders who are not finance professionals." — Source: [CFA Society Chicago]

- On Delegation: "An effective investment committee focuses on policy and asset allocation, leaving individual manager selection to the professional staff." — Source: [Capital Allocators Episode 360]

- On Spending Policy: "The spending rule must smooth out market volatility so that the foundation can maintain steady grant-making even when the endowment value drops." — Source: [The Climb to Investment Excellence]

- On Peer Comparisons: "Chasing the returns of peer endowments often leads to adopting inappropriate risk profiles and buying into overvalued asset classes late in the cycle." — Source: [Institutional Investor Profile]

- On Transparency: "Surprises are toxic to board relationships; bad news must be communicated immediately and with full context." — Source: [Hewlett Foundation CIO Profile]

- On Crisis Management: "Governance structures are tested not when markets are up twenty percent, but when they fall thirty percent and the board feels pressure to act." — Source: [The Climb to Investment Excellence]

Part 7: Market Volatility and Cycles

- On Market History: "Studying financial history provides a framework for understanding that panic and euphoria are permanent features of human markets." — Source: [Capital Allocators Episode 360]

- On Timing: "Consistently timing the market is impossible; survival depends on structuring the portfolio to weather the cycle regardless of its exact timing." — Source: [CFA Society Chicago]

- On Inflation: "Inflation silently erodes purchasing power, requiring real assets and equities to protect the long-term value of the endowment." — Source: [The Climb to Investment Excellence]

- On Interest Rates: "Decades of declining rates artificially boosted asset returns, making forward-looking assumptions heavily reliant on finding organic growth." — Source: [Institutional Investor Profile]

- On Contrarianism: "Being a contrarian requires a strong stomach, as you will look foolish for a long time before you are proven right." — Source: [Hewlett Foundation CIO Profile]

- On Geopolitics: "Geopolitical events create short-term noise, but rarely alter the long-term compounding fundamentals of high-quality businesses." — Source: [The Climb to Investment Excellence]

- On Tech Cycles: "Technological disruption creates clear winners and losers, requiring allocators to avoid value traps while being cautious of extreme growth valuations." — Source: [Capital Allocators Episode 360]

- On Credit Cycles: "Distressed debt opportunities only emerge when credit dries up, meaning the portfolio must have liquidity available exactly when others are forced to sell." — Source: [CFA Society Chicago]

- On Market Narratives: "Investors often construct elaborate narratives to justify extreme valuations, and recognizing those narratives is key to avoiding late-cycle mistakes." — Source: [The Climb to Investment Excellence]

Part 8: Leadership and The Climb to Excellence

- On The Mountain Metaphor: "Building an institutional portfolio is like climbing a high-altitude mountain; it requires meticulous preparation, adaptation to changing conditions, and endurance." — Source: [Capital Allocators Episode 360]

- On Ego: "The market is a ruthless evaluator; acknowledging what you do not know is a prerequisite for long-term survival." — Source: [The Climb to Investment Excellence]

- On Adaptability: "A strategy that worked brilliantly in the past decade may fail in the next, requiring a willingness to evolve without abandoning core principles." — Source: [Institutional Investor Profile]

- On Resilience: "Endurance in investing comes from an emotional equilibrium that prevents overreacting to both exceptional gains and severe losses." — Source: [CFA Society Chicago]

- On Focus: "Success requires ignoring the daily financial news cycle and maintaining a relentless focus on multi-year outcomes." — Source: [Hewlett Foundation CIO Profile]

- On Mentoring: "Building diverse teams is an intentional process that requires active sponsorship, not simply passive recruitment." — Source: [The Climb to Investment Excellence]

- On Legacy: "The ultimate measure of a CIO is the health of the portfolio and the strength of the team left behind for the next generation." — Source: [Capital Allocators Episode 360]

- On Continuous Learning: "The financial markets are a continuous puzzle; the moment you stop learning is the moment your performance begins to decay." — Source: [CFA Society Chicago]

- On The Final Goal: "Excellence is not a static summit you reach and defend, but a continuous process of discipline, execution, and renewal." — Source: [The Climb to Investment Excellence]