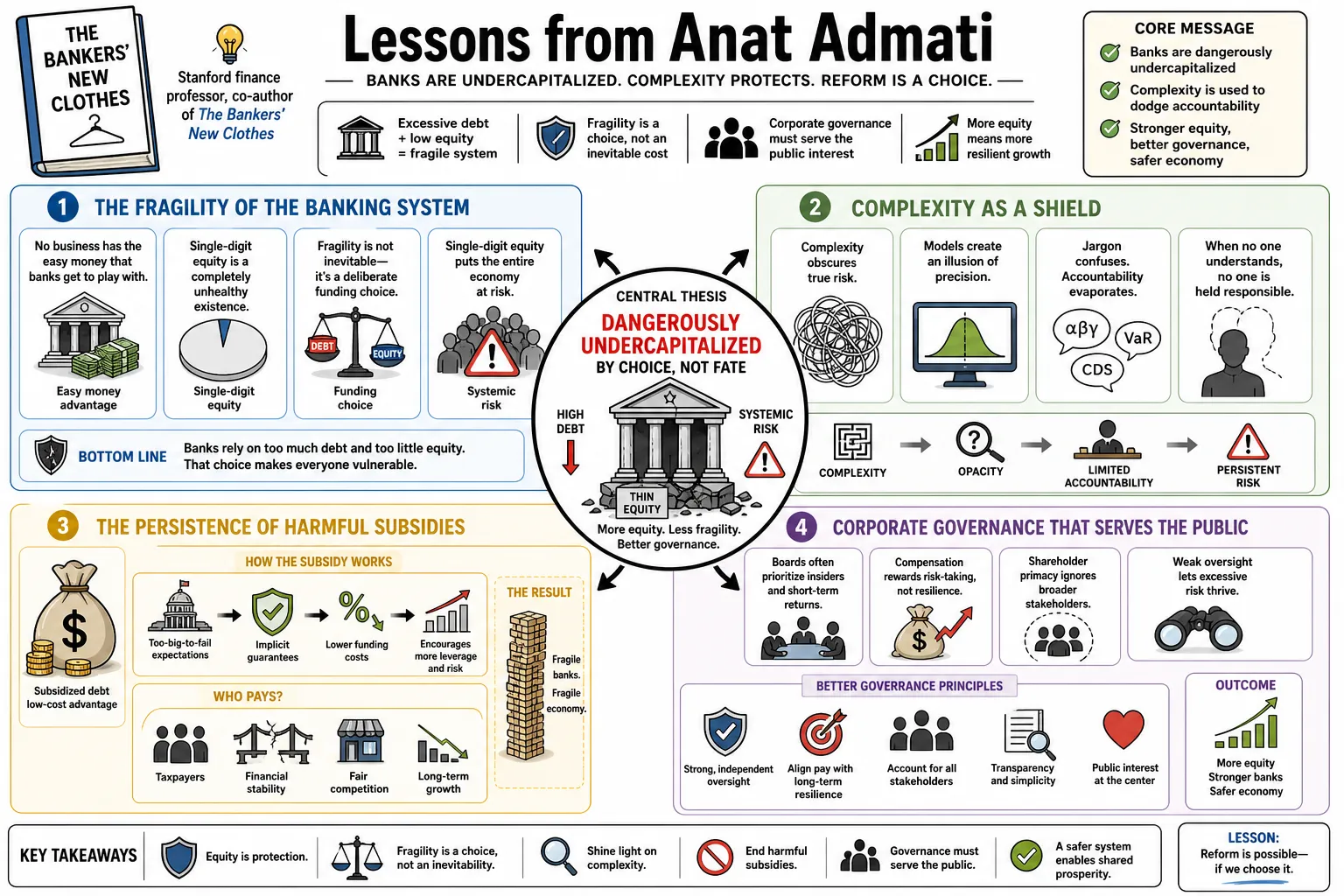

Lessons from Anat Admati

Stanford finance professor Anat Admati, co-author of The Bankers' New Clothes, argues that banks are dangerously undercapitalized. She has consistently dismantled industry claims that requiring banks to fund themselves with more equity would harm the economy. This collection gathers her insights on how the financial sector uses complexity to dodge accountability, why harmful debt subsidies persist, and how corporate governance fails the public.

Part 1: The Fragility of the Banking System

- On banking fragility vs business norms: "No business in the economy has the easy money that banks get to play with.... The existence of banks with single-digit amounts of equity is a completely unhealthy existence." — Source: [Notable Quotes]

- On systemic risk: The fragility of banks is not an unavoidable cost of doing business, but a deliberate choice driven by how they choose to fund themselves. — Source: [The Bankers' New Clothes]

- On risk management: Operating with single-digit equity percentages is a highly dangerous approach to managing bank capital that puts the entire economy at risk. — Source: [The Big Picture]

- On the danger of current structures: Despite the widespread narrative that post-2008 reforms fixed the system, banks remain dangerously fragile today. — Source: [Stanford GSB News]

- On the burden of bailouts: The current system allows bankers to capture the upside while forcing the public to bear the burden of bailouts and economic instability when crises hit. — Source: [The Bankers' New Clothes]

- On bank un-specialness: "Politicians are always saying that banks have always been friends. No. The entire problem in banking is bad governance." — Source: [City, University of London]

- On coddled banks: Banks are treated differently primarily because of the unique privileges they are afforded by the government; they are coddled to the point that they don't even recognize the extent of their subsidies. — Source: [City, University of London]

- On recurring failures: The sudden collapse of banks like Silicon Valley Bank proves that the underlying systemic issues regarding capital and risk have remained unresolved. — Source: [Capitalisn't Podcast]

- On societal costs: By prioritizing extreme debt over sufficient equity, banks maximize their own profitability but create an asymmetric and unacceptable level of risk for society. — Source: [The Big Picture]

- On artificial fragility: Subsidizing banks to borrow excessively makes as much sense as subsidizing the chemical industry to intentionally pollute rivers when clean alternatives are readily available. — Source: [Notable Quotes]

Part 2: Debunking Capital Requirements and "Expensive Equity"

- On the definition of capital: "Capital requirements do not require banks to hold anything; they only concern the source of funding banks use and the extent to which investments are funded by equity." — Source: [UK Parliament Evidence]

- On confusing capital with reserves: "In fact, bank capital is not a cash reserve, and capital requirements must not be confused with minimum reserve requirements." — Source: [FDIC Guest Lecture]

- On the purpose of capital rules: Capital requirements simply dictate the mix of debt and equity that banks must use to fund their operations and assets. — Source: [FDIC Guest Lecture]

- On the fallacy of expensive equity: "We examine the pervasive view that 'equity is expensive'... We find that arguments made to support this view are either fallacious, irrelevant, or very weak." — Source: [Paris School of Economics]

- On the social benefits of equity: "Setting equity requirements significantly higher than the levels currently proposed would entail large social benefits and minimal, if any, social costs." — Source: [RePEc Archive]

- On industry rhetoric regarding lending: The frequent claim that increasing equity requirements will automatically make lending too expensive or stall economic growth is fundamentally flawed. — Source: [EconTalk]

- On the "capital sits idle" myth: The banking industry's claim that every dollar of capital is one less dollar working in the economy relies on the false premise that capital is set aside rather than actively deployed. — Source: [The Bankers' New Clothes]

- On who holds the capital: Corporations do not "hold" their own funding; rather, investors hold claims, such as common shares, that are paid from the cash flows the firm generates. — Source: [UK Parliament Evidence]

- On industry fear-mongering: No matter what regulatory changes are proposed, the banking industry predictably claims that the new rules will restrict credit and harm the economy. — Source: [Institute for New Economic Thinking]

Part 3: Too Big to Fail and Regulatory Failure

- On TBTF as a symptom: "‘Too big to fail’ is a symptom of regulatory failure." — Source: [UK Parliament Evidence]

- On the license for recklessness: "Too Big to Fail is a license for recklessness. These institutions defy notions of fairness, accountability, and responsibility." — Source: [Institute for New Economic Thinking]

- On the scale of the problem: Megabanks are the largest, most complex, and most heavily indebted corporations in the entire economy. — Source: [Institute for New Economic Thinking]

- On the danger of immense institutions: "Institutions considered too big to fail are particularly dangerous because they have an incentive to, and can, become inefficiently large, complex, and opaque." — Source: [ProMarket]

- On the impossibility of management: It has become nearly impossible for executives to manage, and for regulators to effectively oversee, financial institutions of this size and opacity. — Source: [ProMarket]

- On the illusion of reform: Even when politicians claim bipartisan agreement to end Too Big to Fail, simple and effective proposals like a strict 15% equity requirement are quietly sidelined. — Source: [EconTalk]

- On regulatory willful blindness: Policymakers frequently succumb to the influence of the banking lobby, resulting in the design and perpetuation of unnecessarily complex rules that fail to address core risks. — Source: [Stanford GSB News]

- On "too big to jail": The systemic protection afforded to large banks means that "too big to fail" has effectively morphed into "too big to jail" for the individuals running them. — Source: [Boardroom Governance Podcast]

- On protecting the status quo: Powerful actors in finance actively construct and maintain complicated narratives specifically to justify a failing system that benefits them. — Source: [The Bankers' New Clothes]

Part 4: Corporate Governance vs. Democracy

- On the definition of good governance: "In the title [of our paper, Why 'Good' Corporate Governance is Not Always Good], the first good is in quotation marks – because it's not good." — Source: [Corporate Crime Reporter]

- On the limits of corporate law: Corporate law ignores the fact that many of society's most pressing problems cannot be solved in the boardroom; they must be solved at the level of democracy. — Source: [Corporate Crime Reporter]

- On democratic enforcement: "That's where the government creates and enforces rules. If we did that, we wouldn't need to beg CEOs to do it." — Source: [Corporate Crime Reporter]

- On misaligned incentives: "The corporations consider good governance as aligning the interests of the shareholders with the interests of the managers... That can actually undermine external enforcement." — Source: [Corporate Crime Reporter]

- On external vs internal governance: Academics spend entirely too much time obsessing over manager-shareholder alignment while ignoring the severe failures in public law enforcement and democratic oversight. — Source: [ECGI]

- On the market test fallacy: "Economists often assume any economic activity that passes the market test is beneficial for society and don't seriously consider the possibility that corporations can find it profitable to cause harm." — Source: [Stanford GSB Insights]

- On threats to institutions: The sheer size and unchecked dominance of the financial industry pose direct threats to the integrity of democratic institutions. — Source: [King's College London]

- On corporate rights without responsibility: Treating corporations as "legal persons" affords them extensive constitutional rights while offering them limited liability when they cause profound societal harm. — Source: [Berkeley Law Symposium]

- On false choices: "The stark choices we are often presented within the political discourse — between 'free market capitalism' and 'big government socialism' — are simplistic and misleading." — Source: [Stanford GSB Insights]

Part 5: The Problem with Debt and Leverage

- On the addiction to borrowing: "Borrowing can be addictive, especially if the borrower benefits from guarantees." — Source: [Notable Quotes]

- On the subsidization of debt: The current tax code and implicit government guarantees create a system inherently structured to favor borrowing over raising equity. — Source: [The Bankers' New Clothes]

- On magnified losses: Debt mechanically magnifies both returns and losses, rendering any institution operating with minimal equity exceptionally vulnerable to slight downturns in asset values. — Source: [EconTalk]

- On perverse incentives: Allowing banks to fund themselves almost entirely with borrowed money creates a heads-I-win, tails-you-lose dynamic for executives. — Source: [Capitalisn't Podcast]

- On crony capitalism: A system that guarantees private gains for bank executives while socializing their extreme losses is the definition of crony capitalism. — Source: [Minneapolis Fed]

- On the systemic risk of debt: The entire global economy remains highly vulnerable to contagion simply because the financial sector is permitted to operate with unsafe levels of leverage. — Source: [Odd Lots Podcast]

- On the failure of current regulation: Complex regulatory frameworks, like the Basel accords, obscure the simple reality that banks still operate with far too much debt. — Source: [Macro Musings Podcast]

- On the reality of bank funding: High leverage is not an economic necessity for banking; it is a strategic choice made to maximize return on equity for insiders. — Source: [The Bankers' New Clothes]

- On shadow banking: The same fundamental issues of dangerous leverage and inadequate loss-absorbing capital that plague traditional banks are simply replicated in shadow banking. — Source: [Capitalisn't Podcast]

- On the crypto market: Unregulated digital asset markets often recreate the exact systemic vulnerabilities and extreme leverage profiles that make traditional finance dangerous. — Source: [Capitalisn't Podcast]

Part 6: The Banking Industry's Political Influence and Lobbying

- On the power of the banking lobby: "Banks are the most powerful lobby in Washington." — Source: [City, University of London]

- On the political nature of finance: "Banking is political. You do not understand outcomes in banking without understanding the politics." — Source: [City, University of London]

- On industry obstruction: Rational, simple reforms like higher equity requirements are consistently stalled by a lack of political will driven by intense industry lobbying. — Source: [Stanford GSB News]

- On willful misunderstanding: "It is difficult to get a man to understand something when his salary depends upon his not understanding it." — Source: [EconTalk]

- On the confusion tactic: The financial sector benefits heavily from public confusion, using technical jargon to shut down democratic debate over how they are regulated. — Source: [Blogspot / The Bankers' New Clothes]

- On resisting reform: When asked to alter their dangerous practices, the banking industry routinely complains about transition costs—a complaint that should not dictate public policy. — Source: [Notable Quotes]

- On the co-opting of regulators: The outsized influence of large financial institutions and their executives actively undermines both the regulatory apparatus and the rule of law. — Source: [ECGI]

- On the failure to act: Politicians routinely fail to protect the public interest because they are effectively captured by the very entities they are supposed to constrain. — Source: [Stanford CASI]

- On the persistence of bad rules: The persistence of distorted incentives and bad rules in banking is primarily a result of a highly successful, ongoing political lobbying effort. — Source: [City, University of London]

Part 7: Accountability, Liability, and the Rule of Law

- On corporate impunity: When large corporations cause massive societal harm, the legal structure often means that "there's kind of nobody home when you come for—you caused harm." — Source: [The Big Picture]

- On the enforcement gap: Basic principles of justice and law enforcement frequently and routinely fail when applied in the corporate context. — Source: [Stanford GSB Insights]

- On the need for external enforcement: True corporate accountability is impossible unless the justice system is willing to rigorously enforce the law against both the corporate entity and the specific executives involved. — Source: [Corporate Crime Reporter]

- On basic liability: The central issue missing from most financial regulation debates is basic liability; decision-makers must have a personal stake in the downside risks they create. — Source: [Minneapolis Fed]

- On the subversion of law: The legal protections and implicit guarantees afforded to major financial institutions create an environment where they are effectively above the law. — Source: [King's College London]

- On the necessity of stricter enforcement: Ensuring that the rule of law applies to powerful entities requires radical transparency, stricter auditing, and much stronger criminal enforcement mechanisms. — Source: [Financial Stability Board]

- On the impact of corporate dominance: The massive concentration of power and wealth within the banking sector directly undermines the equitable application of the justice system. — Source: [Stanford CASI]

- On holding executives responsible: Without credible threats of personal liability for the individuals actually running the corporations, all internal corporate governance is merely window dressing. — Source: [Corporate Crime Reporter]

- On transparency: Because of the opacity of modern financial systems, we require intense, enforced transparency so that both the public and regulators can recognize when laws are being broken. — Source: [The Bankers' New Clothes]

Part 8: Challenging Economics and Speaking Truth to Power

- On the responsibility of economists: "Beware of economists who hide assumptions." — Source: [Notable Quotes]

- On the difficulty of speaking out: "I persisted because I felt a strong sense of responsibility. But challenging people is difficult and no fun. I understand why people avoid it." — Source: [Stanford GSB News]

- On the intersection of disciplines: The spread of corporate disinformation intersects directly with financial risk, showing that bad data and false narratives threaten market stability. — Source: [Cambridge Disinformation Summit]

- On the role of academics: Academic economists have a civic duty to communicate complex financial realities to the public in clear, accessible language rather than hiding behind models. — Source: [Age of Economics]

- On technological narratives: Society must critically examine the narratives pushed by the tech industry regarding AI, applying the same skepticism required when evaluating banking regulations. — Source: [Power to Truth Web Series]

- On the definition of capitalism: Discussions about economic reform must address what capitalism actually means when massive private losses are routinely absorbed by the state. — Source: [Age of Economics]

- On the necessity of public understanding: Cutting through the dense jargon of finance is the only way for voters to understand the mechanics of banking and effectively demand necessary reforms. — Source: [The Bankers' New Clothes]

- On the danger of blind trust: There is profound systemic danger in placing blind trust in financial experts and their proprietary models to self-regulate. — Source: [TrustTalk Podcast]

- On the purpose of economic advice: There needs to be strict accountability for the economic advice provided to policymakers, which too often serves entrenched special interests rather than the public good. — Source: [Age of Economics]

- On intellectual courage: Unmasking the false narratives of the financial sector is not a one-time effort; it requires a sustained commitment to exposing hidden assumptions against intense industry pushback. — Source: [Stanford GSB News]