Lessons from André Perold

Finance researcher André Perold spent three decades teaching at Harvard Business School before co-founding HighVista Strategies to manage institutional assets. He is best known for inventing the "implementation shortfall," a mathematical framework that measures the hidden costs of trading. This profile details his findings on market mechanics and portfolio construction, showing how investment theory works in practice.

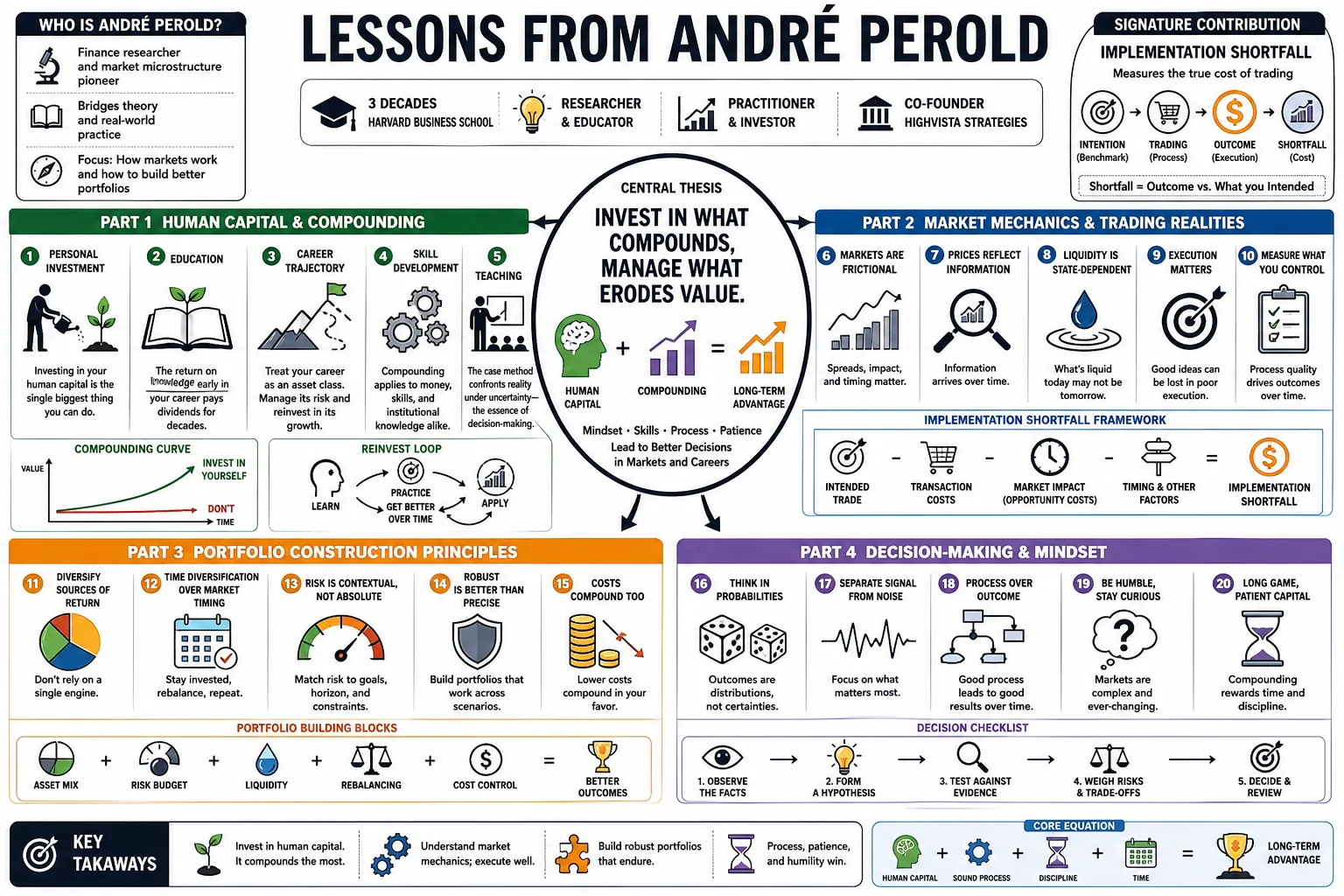

Part 1: Human Capital and Compounding

- On Personal Investment: "Investing in your human capital is the single biggest thing you can do. That is what compounds over time." — Source: Podcast Notes

- On Education: "The return on knowledge early in your career pays dividends for decades, far outstripping early financial investments." — Source: Art of Investing

- On Career Trajectory: "Treat your career as an asset class. Manage its risk and reinvest in its growth continuously." — Source: Family Inc.

- On Skill Development: "Compounding applies to money, skills, and institutional knowledge alike." — Source: Capital Allocators

- On Teaching: "The case method forces students to confront the reality of decision-making under uncertainty, which is the essence of finance." — Source: Harvard Business School

- On Life Choices: "Every major life decision is fundamentally a capital allocation problem." — Source: Family Inc.

- On Reputation: "In an industry built on trust, your integrity is a non-depreciating asset that must be protected." — Source: Art of Investing

- On Early Mistakes: "Making errors early with small stakes is a necessary part of building the human capital required to manage large stakes later." — Source: Capital Allocators

- On Continuous Learning: "The markets evolve constantly, meaning your human capital depreciates if you are not actively updating your mental models." — Source: Private Capital Podcast

- On Mentorship: "Transferring knowledge through apprenticeship is how the best investment firms compound their organizational intelligence." — Source: Harvard Business School

Part 2: Implementation Shortfall and Trading Costs

- On Paper vs. Reality: "There is a massive gap between the returns of a theoretical portfolio on paper and what can actually be captured in the market." — Source: Journal of Portfolio Management

- On the Decision Price: "The true cost of a trade must be measured against the price of the asset at the exact moment the investment decision is made." — Source: Quantitative Brokers

- On Hidden Friction: "Commissions are only the most visible part of trading costs. Market impact and delay often consume far more alpha." — Source: Ryan O'Connell Finance

- On Opportunity Cost: "The shares you fail to buy because the price ran away from you represent a very real, measurable drag on performance." — Source: UPenn Research

- On Market Impact: "Large trades move the market against the trader. If you do not measure this movement, you are ignoring your biggest expense." — Source: BS Capital Markets

- On Execution Speed: "The time elapsed between a decision and its execution is a window where expected returns can easily vanish." — Source: QuestDB

- On Portfolio Drag: "A positive implementation shortfall means the frictions of reality have actively eroded your intended investment edge." — Source: Ryan O'Connell Finance

- On Trading Analytics: "Without a strict framework to measure execution costs, active managers cannot know if their stock-picking adds actual value." — Source: Harvard Business School

- On Performance Measurement: "Measuring performance against execution price alone artificially flatters the trader and obscures the true cost to the fund." — Source: Journal of Portfolio Management

- On Slippage: "Slippage is a structural cost of accessing liquidity that must be modeled into expected returns." — Source: Quantitative Brokers

Part 3: Market Efficiency and Inefficiencies

- On Zero-Sum Games: "Public market investing is largely a zero-sum game. For every winner, there must be a loser on the other side of the trade." — Source: HBS Club Houston

- On Structural Inefficiency: "Investors should seek out beautiful inefficiencies, which are pockets of the market where informational or structural barriers prevent perfect pricing." — Source: Private Capital Podcast

- On Human Behavior: "Markets act less like math equations and more like complex puzzles driven by human behavior and asymmetric information." — Source: Capital Allocators

- On Edge: "You only have an edge if you understand exactly why the person selling to you is willing to part with the asset at that price." — Source: Art of Investing

- On Market Niches: "The most attractive returns are often found in niche markets that are too small or complex for mega-funds to efficiently deploy capital." — Source: HighVista Strategies

- On Complexity: "Complexity scares away average capital, which leaves a premium for those willing to do the intensive underwriting." — Source: Private Capital Podcast

- On Arbitrage Limits: "Even when mispricings are obvious, funding constraints can prevent them from closing quickly." — Source: Harvard Business School

- On Information Flow: "In public markets, information is priced in instantly. In private markets, information travels slowly and creates actionable discrepancies." — Source: HighVista Strategies

- On Competition: "To generate alpha consistently, you must operate in arenas where the competition is systematically disadvantaged." — Source: Capital Allocators

- On Liquidity Illusions: "The illusion of liquidity in public markets often leads investors to underestimate the true risk of crowded trades." — Source: Private Capital Podcast

Part 4: The Endowment Model and Multi-Asset Investing

- On Asset Allocation: "The endowment model works because it relies on profound diversification across fundamentally different drivers of return." — Source: Harvard Business School

- On Time Horizons: "Institutions with infinite time horizons have a distinct advantage. They can harvest the illiquidity premium that others cannot afford." — Source: Capital Allocators

- On Flexibility: "A successful multi-asset strategy requires the flexibility to shift capital dynamically as different asset classes become cheap or expensive." — Source: HighVista Strategies

- On Uncorrelated Returns: "True diversification requires holding assets whose underlying cash flows are completely unlinked." — Source: HBS Club Houston

- On Opportunism: "Endowment-style investing requires the patience to sit on your hands and the opportunism to strike when dislocations occur." — Source: Art of Investing

- On Institutional Constraints: "Many funds fail because their governance structures prevent them from making the contrarian bets required for long-term success." — Source: Harvard Business School

- On Alternative Assets: "Alternatives function best as essential tools for smoothing the overall variance of the portfolio, rather than acting as a separate bucket." — Source: HighVista Strategies

- On Manager Selection: "In private markets, the dispersion between top and bottom quartile managers is so wide that manager selection matters more than asset allocation." — Source: Capital Allocators

- On Patience: "Capital that cannot wait will inevitably be transferred to capital that can wait." — Source: Art of Investing

Part 5: Private Equity and Venture Capital

- On the Lower Middle Market: "The lower middle market in private equity remains fertile ground because it relies on operational improvements rather than financial engineering." — Source: HighVista Strategies

- On Alignment of Interests: "The best private investments are those where the operator's net worth is inextricably tied to the specific outcome of the asset." — Source: Private Capital Podcast

- On Venture Capital: "Early-stage venture is less about predicting the future and more about backing exceptional founders who can adapt to an unknown future." — Source: Capital Allocators

- On Co-Investments: "Co-investments allow LPs to concentrate capital in high-conviction ideas while driving down the blended fee rate of the portfolio." — Source: HighVista Strategies

- On Value Creation: "In public markets, you buy and hold. In private markets, you buy, fix, and sell. The difference is control." — Source: Harvard Business School

- On Life Sciences: "Investing in biotech requires specialized technical knowledge that inherently restricts the pool of capable capital." — Source: HighVista Strategies

- On Sourcing Deals: "In private markets, proprietary sourcing is an actual competitive advantage, whereas in public markets, proprietary information is often illegal." — Source: Private Capital Podcast

- On Exit Strategy: "A private equity investment is only as good as its liquidity event. Underwriting the exit is as important as underwriting the entry." — Source: Capital Allocators

- On Scale Constraints: "As private equity funds grow too large, they are forced into highly competitive, efficient large-cap auctions where returns compress." — Source: Harvard Business School

Part 6: Active versus Passive Management

- On the Active Debate: "Active management in large-cap public equities is extremely difficult because you are competing against the aggregate wisdom of the market." — Source: NBER

- On Indexing: "Cap-weighted indexing is essentially a momentum strategy. It automatically buys more of what has gone up and less of what has gone down." — Source: ResearchGate

- On Non-Cap-Weighted Indices: "Many supposed smart beta strategies are simply active management repackaged and sold as rules-based indexing." — Source: PRU FIDFA

- On Fee Drag: "The mathematical certainty of passive investing is that the average active investor must underperform the index by exactly the amount of their fees." — Source: Harvard Business School

- On Choosing Active: "You should only pay active fees in markets where information is scarce or highly technical." — Source: Capital Allocators

- On Market Function: "Passive investing relies on a healthy ecosystem of active managers to set prices. If everyone indexed, the market would break." — Source: Harvard Business School

- On Performance Persistence: "In highly efficient markets, past performance of active managers is virtually useless for predicting future returns." — Source: NBER

- On Active Share: "If an active manager holds a portfolio that closely mirrors the benchmark, they are just charging a premium for a commodity product." — Source: ResearchGate

- On Specialized Alpha: "Alpha is not dead, but it has migrated to the edges of the market where passive vehicles cannot easily go." — Source: HighVista Strategies

Part 7: Risk Management and Downside Protection

- On Tail Risk: "Investors consistently underestimate the probability and severity of tail events because recent history rarely reflects long-term market distributions." — Source: HighVista Strategies

- On Capital Preservation: "Recovering from a severe drawdown requires geometrically higher returns. Protecting capital in down markets is the essence of compounding." — Source: Art of Investing

- On Volatility: "Volatility is not the same as risk. True risk is the permanent impairment of capital." — Source: Harvard Business School

- On Correlation: "During a liquidity crisis, the correlation of almost all risk assets approaches one, defeating traditional diversification." — Source: Private Capital Podcast

- On Sizing Positions: "The size of an investment should be dictated by both its upside potential and the firmness of its floor." — Source: HighVista Strategies

- On Leverage: "Leverage does not create returns. It merely accelerates outcomes and narrows the margin for error." — Source: Capital Allocators

- On Liquidity Risk: "Being forced to sell illiquid assets to meet unexpected liabilities is how generational wealth is destroyed." — Source: Harvard Business School

- On Hedging: "A perfect hedge is often too expensive to maintain. The goal is cost-effective asymmetry." — Source: HighVista Strategies

- On Behavioral Risk: "The greatest risk to a portfolio is often the investor's own tendency to panic at the exact wrong moment." — Source: Art of Investing

Part 8: Academic Theory versus Practitioner Reality

- On the CAPM: "The Capital Asset Pricing Model is a beautiful theoretical framework that breaks down the moment it encounters the frictions of reality." — Source: Harvard Business School

- On Bridging the Gap: "Academia teaches us what markets should do in equilibrium. Practitioners make money by exploiting the path markets take to get there." — Source: Capital Allocators

- On Data Mining: "With enough computing power, you can torture historical financial data until it confesses to any pattern you want to see." — Source: NBER

- On Real-World Friction: "Theories assume frictionless trading, but in the real world, friction is the dominant variable in strategy execution." — Source: Journal of Portfolio Management

- On the Vanguard Board: "Serving on the board of Vanguard provided a front-row seat to the staggering power of scale and low costs in asset management." — Source: Vanguard

- On Teaching versus Doing: "Explaining a concept to a classroom of sharp students forces a level of clarity that immediately improves your own investment process." — Source: Art of Investing

- On Model Risk: "When a mathematical model fails, the market does not care how elegant the math was." — Source: Harvard Business School

- On Financial Innovation: "Most financial engineering is designed to hide risk and extract fees, rather than genuinely improving the efficiency of capital." — Source: Private Capital Podcast

- On the Purpose of Finance: "Ultimately, the role of finance is to efficiently allocate capital to its highest and best use in the real economy." — Source: Harvard Business School