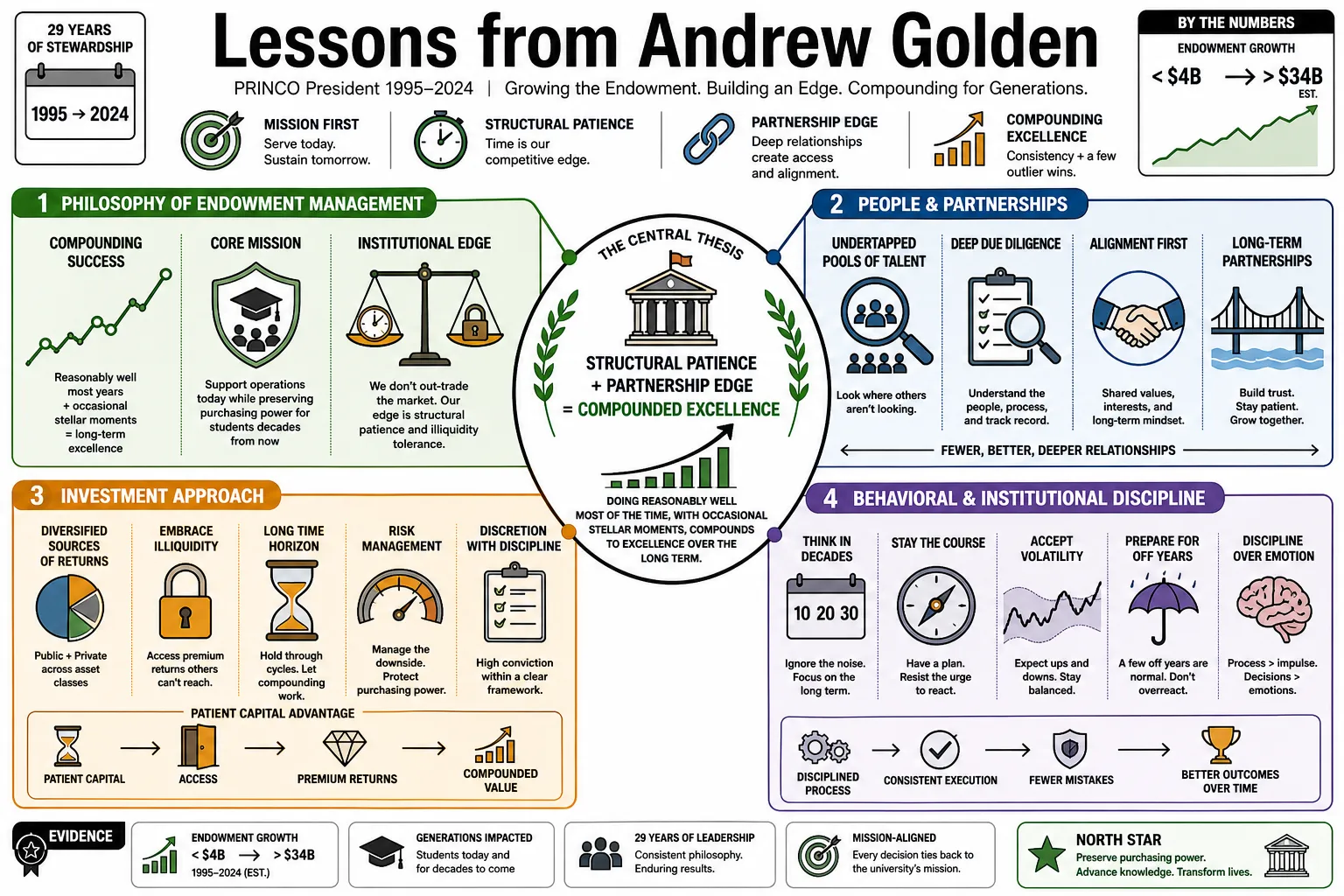

Andrew Golden served as the president of the Princeton University Investment Company (PRINCO) from 1995 to 2024, guiding the university's endowment from under $4 billion to more than $34 billion. He is known for building a distinct investment culture focused on finding "undertapped pools of talent" and cultivating deep, long-term partnerships with outside managers. This profile collects his approaches to manager selection, institutional discipline, and the behavioral realities of capital allocation.

Part 1: The Philosophy of Endowment Management

- On Compounding Success: "Doing reasonably well more often than not, with occasional stellar moments, even if with a few, but not many, off years, compounds to excellence over the long term." — Source: Princeton University Communications

- On the Core Mission: "The primary directive is to support the university's operations today while preserving the purchasing power of the endowment for students who won't arrive for decades." — Source: Finance Simplified Podcast

- On Institutional Edge: "We aren't going to out-trade the market. Our advantage comes from structural patience and the ability to tolerate illiquidity longer than most." — Source: Capital Allocators Podcast

- On Complexity: "Just because a strategy is difficult to understand doesn't mean it holds superior returns. Often, the best ideas are structurally simple but psychologically hard to execute." — Source: Princeton Alumni Weekly

- On Active Management: "It only makes sense to pay active fees in areas where inefficiency is high enough that true skill can actually surface above the costs." — Source: Institutional Investor

- On Portfolio Construction: "You don't build a portfolio by collecting a bunch of great individual investments; you build it by combining assets that behave differently under varying conditions." — Source: 3 Takeaways Podcast

- On Measuring Performance: "We evaluate ourselves against our own policy portfolio, because beating a generic market index doesn't matter if we fail to meet the specific financial needs of the university." — Source: Princeton University Investment Company

- On Liquidity: "Endowments can afford to lock up capital, but you have to be compensated for that illiquidity. If the premium isn't there, we prefer the flexibility of cash." — Source: Financial Times

- On Policy Portfolios: "The policy portfolio is the baseline. Any deviation from it requires a high degree of conviction that we are being paid to take that specific tracking risk." — Source: Capital Allocators Podcast

- On the Endowment Model: "The so-called endowment model isn't a static mix of assets. It is a philosophy of adapting to where capital is scarce and applying rigorous manager selection." — Source: Finance Simplified Podcast

Part 2: Finding Talent and Avoiding the Herd

- On Manager Selection: "We spend far more time evaluating the character and cognitive flexibility of a manager than we do analyzing their past track record." — Source: 3 Takeaways Podcast

- On Undertapped Pools of Talent: "If you want alpha, you have to look where others aren't. That naturally leads you to undertapped pools of talent, including firms owned by women and minorities." — Source: Princeton University Communications

- On Emerging Managers: "First-time funds often have the highest hunger and the clearest alignment of interests, even if they lack the polished infrastructure of legacy firms." — Source: Institutional Investor

- On the Consensus Problem: "If everybody agrees a specific asset class is a great opportunity, the price has likely already adjusted to reflect that enthusiasm." — Source: Capital Allocators Podcast

- On Intellectual Honesty: "The best managers are the ones who can articulate their mistakes clearly and explain what they learned without getting defensive." — Source: Princeton Alumni Weekly

- On Pedigree: "A degree from a famous school might get you a first meeting, but it tells us nothing about your ability to generate independent investment insights." — Source: 3 Takeaways Podcast

- On Size Constraints: "Asset growth is the enemy of performance. We prefer managers who explicitly cap their fund sizes to protect their returns rather than maximizing their management fees." — Source: Finance Simplified Podcast

- On Capacity: "Finding a great manager is only half the battle. The other half is ensuring they have the discipline to turn away capital when opportunities are scarce." — Source: Institutional Investor

- On Due Diligence: "You learn more about a manager by talking to the people they fired or the companies they didn't invest in than by reading their marketing materials." — Source: Capital Allocators Podcast

Part 3: The Meaning of True Partnership

- On the Pursuit of Partnership: "I think the hallmark of PRINCO, one of the things that distinguishes us, is that pursuit of partnership." — Source: Institutional Investor

- On Client Dynamics: "We don't view ourselves as customers buying a product. We are partners in a joint enterprise, and that requires mutual transparency." — Source: Princeton Alumni Weekly

- On Trust: "You can't write a contract that covers every possible edge case in a ten-year lockup. Ultimately, you are underwriting the integrity of the people." — Source: 3 Takeaways Podcast

- On Communication: "A true partnership means we want to be the first call when something goes wrong, not the last to find out when the quarterly letter arrives." — Source: Capital Allocators Podcast

- On Alignment of Interests: "We look closely at how a manager structures their own compensation and how much of their net worth is invested alongside ours." — Source: Finance Simplified Podcast

- On Patience: "We promise long-term partnership, which means we don't fire a manager just because their specific style happens to be out of favor for a few years." — Source: Institutional Investor

- On Adding Value: "As a limited partner, our job is to be a sounding board for our managers without trying to backseat drive their specific investment decisions." — Source: Princeton University Communications

- On Manager Transitions: "The most fragile moment in any partnership is generational succession. We spend years discussing how a firm will hand over leadership before it actually happens." — Source: Capital Allocators Podcast

- On Loyalty: "Loyalty doesn't mean blindly funding bad decisions. It means giving a manager the benefit of the doubt when they face temporary headwinds." — Source: 3 Takeaways Podcast

Part 4: Managing Through Crises and Volatility

- On Market Panics: "Crises are when your structural advantages matter most. If you have the liquidity and the nerve, panic creates the best entry points." — Source: Capital Allocators Podcast

- On the 2008 Crisis: "The global financial crisis was a harsh stress test of liquidity assumptions. We learned that correlation goes to one when everyone is rushing for the exit." — Source: Institutional Investor

- On Rebalancing: "Rebalancing sounds easy in theory, but in practice, it means systematically buying the assets that have caused you the most pain recently." — Source: Princeton Alumni Weekly

- On Holding Cash: "Cash is a low-returning asset, but its option value during a severe market dislocation is nearly impossible to quantify." — Source: Finance Simplified Podcast

- On Institutional Nerve: "The hardest part of a crisis isn't the math; it's managing the anxieties of your board and ensuring everyone stays committed to the long-term plan." — Source: 3 Takeaways Podcast

- On Forecasting: "We spend zero time trying to predict macroeconomic variables like interest rates or GDP growth. We focus entirely on underwriting specific assets." — Source: Capital Allocators Podcast

- On Drawdowns: "You have to accept that drawdowns are a feature, not a bug, of owning risk assets. If you can't tolerate the downside, you can't earn the premium." — Source: Princeton University Communications

- On Market Timing: "Moving in and out of the market based on short-term news is a fool's errand. You have to be right twice: when to sell and when to buy back in." — Source: Institutional Investor

- On Volatility as Opportunity: "Volatility is only risk if you are forced to sell. If you are a buyer, volatility is the mechanism that creates mispricing." — Source: Financial Times

Part 5: Decision Making and Cognitive Bias

- On Groupthink: "The role of the investment committee is not to reach unanimous agreement quickly, but to ensure that dissenting views are fully explored." — Source: Capital Allocators Podcast

- On Overconfidence: "The most dangerous investors are the ones who have experienced an unbroken string of successes and believe their own press clippings." — Source: 3 Takeaways Podcast

- On Process over Outcome: "You can make a terrible decision and get lucky, or make a brilliant decision and lose money. We judge our team on the quality of the process." — Source: Finance Simplified Podcast

- On Cognitive Flexibility: "When the facts change, or when we discover our initial thesis was flawed, the ability to change our minds quickly is our best defense." — Source: Princeton Alumni Weekly

- On Sunk Costs: "The market doesn't care what price you paid for an asset. The only question that matters is whether it's a good investment at today's price." — Source: Institutional Investor

- On Confirmation Bias: "We explicitly assign people on our team to play devil's advocate and build the case for why a proposed investment will fail." — Source: Capital Allocators Podcast

- On Narrative Fallacy: "A compelling story is often a trap. We force ourselves to separate the narrative appeal of a company from the mathematical reality of its valuation." — Source: 3 Takeaways Podcast

- On Status Quo Bias: "Doing nothing is an active investment decision. Keeping an underperforming manager requires the same conviction as hiring a new one." — Source: Finance Simplified Podcast

- On Hindsight Bias: "We write down our thesis and expected outcomes before making an investment so we can't rewrite history to make ourselves look smarter later." — Source: Princeton University Communications

- On Complexity Bias: "There is a persistent bias in finance to believe that complicated models are more accurate than simple ones. They rarely are." — Source: Institutional Investor

Part 6: Building a Winning Culture

- On the Secret Sauce: "Our secret sauce is our ability to partner well with a promise of long-term partnership, and creating a culture that attracts people who want to work that way." — Source: Institutional Investor

- On Hiring: "We look for people who are intensely curious, deeply analytical, and completely lack a sense of entitlement." — Source: 3 Takeaways Podcast

- On Retention: "You keep good people by giving them real responsibility early and fostering an environment where their ideas are debated on merit, not seniority." — Source: Princeton Alumni Weekly

- On Intellectual Humility: "I still have a hard time taking myself very seriously. The moment you start believing you have all the answers is the moment the market humbles you." — Source: Institutional Investor

- On Team Dynamics: "A great investment team functions like a jazz ensemble. Everyone knows the underlying structure, but there is constant, fluid improvisation." — Source: Capital Allocators Podcast

- On Dissent: "If everyone in the room agrees on an investment, I get nervous. We need friction in the room to uncover the risks we might be missing." — Source: Finance Simplified Podcast

- On Training: "Mentorship isn't about telling junior staff what to do. It's about showing them how to think about ambiguity and risk." — Source: Princeton University Communications

- On Mistakes: "We celebrate well-reasoned mistakes because if you aren't making any mistakes, you aren't taking enough risk to generate excess returns." — Source: 3 Takeaways Podcast

- On Shared Mission: "The advantage of working for an endowment is that the ultimate beneficiary is education and research. That mission acts as a powerful aligning force for the team." — Source: Capital Allocators Podcast

Part 7: The David Swensen Influence

- On His Mentor: "Working at the Yale Investments Office under Dave was the equivalent of a medical internship and residency for me." — Source: Institutional Investor

- On Swensen's Legacy: "Every day I worked for him, every day since, and I suspect every day in the future, I had at least one debate with him, internal in my mind." — Source: Institutional Investor

- On the Internal Debate: "I always ask myself: 'What would Dave say about this investment opportunity, this organizational choice, this potential hire?'" — Source: Institutional Investor

- On Asset Allocation Principles: "David taught us that equity orientation and diversification are the twin pillars of institutional portfolio management." — Source: Capital Allocators Podcast

- On Pioneering Portfolio Management: "It remains the world's best and most forward-looking text on institutional investing, as relevant today as when he wrote it." — Source: Yale University Communications

- On Principal-Agent Problems: "Swensen hammered into us the necessity of understanding exactly how our managers are incentivized, because incentives drive all human behavior." — Source: Finance Simplified Podcast

- On Alternative Assets: "Yale showed the world that illiquid assets like private equity and venture capital could be structurally integrated into an institutional portfolio, provided you have the right manager access." — Source: 3 Takeaways Podcast

- On Institutional Courage: "David's greatest trait wasn't his math skills; it was his courage to stand completely apart from the crowd when he knew he was right." — Source: Princeton Alumni Weekly

- On Market Efficiency: "We learned early on that public equity markets are largely efficient, which means you have to go into less efficient, alternative markets to reliably find alpha." — Source: Capital Allocators Podcast

- On Continual Learning: "The most important thing I took from my time at Yale was a framework for thinking, a way to continuously update my priors as new information arrives." — Source: Princeton University Communications

Part 8: Long-Term Horizons and a Three-Decade Marathon

- On His Tenure: "It's been almost a three-decade marathon. My goal for the year ahead is to sprint through the tape." — Source: Princeton University Communications

- On Time Arbitrage: "Our longest duration asset is time. We can underwrite a ten-year business plan while the rest of the market is panicking over quarterly earnings." — Source: Capital Allocators Podcast

- On Generational Responsibility: "We are making decisions today that will fund financial aid for students who won't be born for another fifty years." — Source: Finance Simplified Podcast

- On Preparing for the Future: "My final job was to make sure that Princeton is positioned for success over the next 25 years, long after I have left the building." — Source: Institutional Investor

- On Structural Patience: "You can't manufacture patience. You have to build an governance structure—a board and a committee—that explicitly protects the team from short-term pressures." — Source: 3 Takeaways Podcast

- On the Evolution of Markets: "The markets today are vastly more competitive than they were in 1995. The easy inefficiencies have been arbitraged away, requiring us to dig much deeper." — Source: Financial Times

- On Private Equity Dynamics: "The private equity model has matured, and the liquidity environment is changing. LPs have to be much more discerning about which illiquid strategies they fund." — Source: Financial Times

- On Reading the Environment: "A long-term horizon doesn't mean ignoring the present. It means contextualizing the present so you don't overreact to it." — Source: Capital Allocators Podcast

- On Leaving a Legacy: "The true measure of my time here won't be the returns over the last thirty years, but whether the culture we built sustains the returns for the next thirty." — Source: Princeton Alumni Weekly