Lessons from Andrew Lo

MIT Sloan economist Andrew Lo studies how biology and evolution drive investor behavior. He developed the Adaptive Markets Hypothesis to explain why standard economic models break down during market panics and booms. This profile covers his work on market ecosystems, his push to fund cancer research using financial engineering, and his views on AI in asset management.

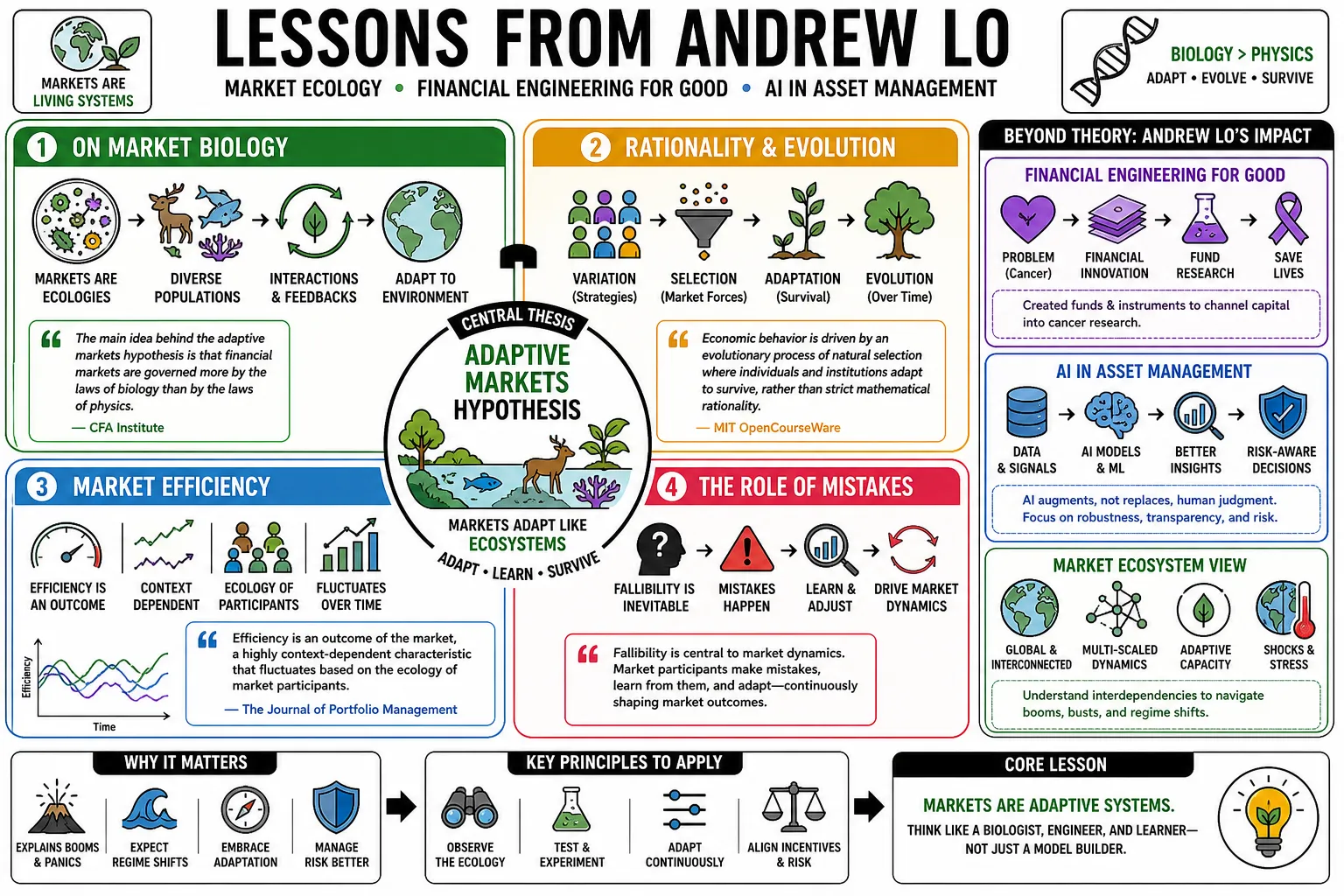

Part 1: The Adaptive Markets Hypothesis

- On Market Biology: "The main idea behind the adaptive markets hypothesis is that financial markets are governed more by the laws of biology than by the laws of physics." — Source: CFA Institute

- On Rationality and Evolution: "Economic behavior is driven by an evolutionary process of natural selection where individuals and institutions adapt to survive, rather than strict mathematical rationality." — Source: MIT OpenCourseWare

- On Market Efficiency: "Efficiency is an outcome of the market, a highly context-dependent characteristic that fluctuates based on the ecology of market participants." — Source: The Journal of Portfolio Management

- On the Role of Mistakes: "Fallibility is central to market dynamics. Market participants make mistakes, learn from them, and innovate through trial and error." — Source: EDHEC Business School

- On Shifting Environments: "Strategies that perform well in one market environment may fail entirely when the ecology changes, requiring continuous adaptation." — Source: Financial Times

- On Reconciling Theories: "The Adaptive Markets Hypothesis bridges the gap between the Efficient Markets Hypothesis and behavioral finance by placing both within an evolutionary framework." — Source: Knowledge at Wharton

- On the Speed of Change: "Financial evolution now occurs at the speed of thought, meaning biological principles operate on highly accelerated timescales in modern markets." — Source: MIT Sloan

- On Self-Interest: "While participants act in their own self-interest, this drive is biological and survival-oriented." — Source: CFA Institute

- On Economic Modeling: "Traditional static economic models fail because they assume equilibrium, whereas markets are continuously adapting ecosystems." — Source: Medium

- On Market Ecology: "Different market players, like retail investors and market makers, interact as distinct species competing for limited resources." — Source: Financial Times

Part 2: Human Behavior and Evolution in Markets

- On Fear and Survival: "Strong emotions like fear are an immediate call-to-arms to survive, selected by evolution over millions of generations of life in hostile environments." — Source: Goodreads

- On Heuristics: "The mental shortcuts that humans use to make financial decisions are evolutionary adaptations that worked well in the past but misfire in modern markets." — Source: MIT Sloan

- On Intelligence and Emotion: "Emotion is the physiological mechanism that focuses human attention on imminent threats, operating alongside rational thought." — Source: CFA Institute

- On Risk Perception: "Human risk preferences shift dynamically in response to stress and environmental feedback." — Source: The Journal of Portfolio Management

- On Herding Behavior: "Following the crowd is a deeply ingrained survival mechanism that translates directly into financial bubbles and panics." — Source: Knowledge at Wharton

- On Trust: "The willingness to engage in complex financial transactions relies on biological trust mechanisms that break down rapidly during a panic." — Source: MIT OpenCourseWare

- On Neuroeconomics: "Understanding financial decision-making requires mapping the neurological responses of traders under high-stress conditions." — Source: EDHEC Business School

- On Loss Aversion: "The psychological pain of losing capital is tied to ancestral survival instincts, making it difficult for investors to cut losses rationally." — Source: Medium

- On Adaptation Limitations: "Evolution optimizes for immediate survival, meaning human brains are poorly adapted for long-term compounding and retirement planning." — Source: MIT Sloan

- On Animal Spirits: "The spontaneous optimism or pessimism described by Keynes is driven by actual neurochemical responses to market stimuli." — Source: Goodreads

Part 3: Healthcare Finance and Megafunds

- On Financial Engineering for Good: "If deployed in megafunds by teams of savvy money managers and scientists, the securitization of intellectual property related to biomedical research could yield lucrative returns." — Source: Institutional Investor

- On the Valley of Death: "Large-scale portfolio theory can bridge the funding gap for early-stage biomedical research, where individual drug projects are deemed too risky for traditional capital." — Source: Healthcare Finance

- On Diversifying Risk: "By combining many highly risky, uncorrelated drug development projects into a single massive entity, the overall risk profile becomes attractive to bond markets." — Source: MIT News

- On Personal Motivation: "Friends and family were dealing with various kinds of cancer, and I felt pretty useless. I decided that if I was going to really be useful to my friends and family, I needed to learn more about how drug development works." — Source: Pharmaphorum

- On the Funding Contradiction: "Scientists and clinicians are making breakthroughs all the time with regard to drug developments, but the amount of funding that is going into biomedicine is declining." — Source: Institutional Investor

- On His Academic Role: "I'm not qualified to manage any of these vehicles. I'm hoping to play the role of glorified wedding planner. I'll bring the bride and groom together; they should know what to do after the wedding." — Source: Institutional Investor

- On the Cost of Capital: "Reducing the cost of capital for biotech firms through structural finance is equal in importance to discovering the underlying science itself." — Source: National Institutes of Health

- On Uncomfortable Conversations: "For the first few years, I really felt extremely uncomfortable talking with oncologists about investing. It actually seemed offensive and obscene." — Source: Pharmaphorum

- On the Scale Requirement: "A biomedical megafund requires billions of dollars to hold enough parallel projects for the law of large numbers to successfully mitigate clinical trial failure rates." — Source: American Economic Association

- On Debt Markets: "Equity alone cannot solve the biotech funding crisis. The industry must access the much larger global debt markets through credit-enhancing structures." — Source: MIT Sloan

Part 4: Financial Crises and Systemic Risk

- On Financial Energy: "Global financial markets contain enormous financial energy, and when detonated in an uncontrolled and irresponsible manner, you get bubbles, crashes, and years of nuclear fallout." — Source: Goodreads

- On Crisis Utility: "A crisis is a terrible thing to waste; we must take advantage of the window of opportunity for new legislation before its memory fades completely." — Source: Bookey

- On Inevitability: "Financial panics cannot be legislated out of existence because they are an unavoidable byproduct of human nature interacting with modern capitalism." — Source: IDEAS/RePEc

- On Systemic Contagion: "Like an epidemiologist studying the spread of a contagious disease from its point of origin, we should identify the potential linkages through which a financial crisis may travel." — Source: Goodreads

- On the Illusion of Science: "Many of us like to think of financial economics as a science, but complex events like the financial crisis suggest that this conceit may be more wishful thinking than reality." — Source: ResearchGate

- On Network Theory: "Mapping systemic risk requires visualizing the financial system as a highly connected network graph, rather than looking at individual balance sheets in isolation." — Source: MIT Sloan

- On the Cause of Crises: "Crises occur when financial engineering outpaces the understanding of the market participants and regulators attempting to oversee it." — Source: CFA Institute

- On Liquidity Droughts: "Systemic risk often materializes as a sudden, catastrophic evaporation of liquidity driven by mutual distrust rather than a simple drop in asset prices." — Source: Financial Times

- On Measuring Risk: "The inability to accurately quantify systemic risk before a crash occurs remains a primary vulnerability for global banking." — Source: IDEAS/RePEc

Part 5: Rethinking Regulation

- On Regulatory Flexibility: "If regulations don't bend, they'll break. Financial regulation should be adaptive, not reactive." — Source: Risk.net

- On Regulatory Efficacy: "Financial markets do not need more regulation; they need smarter and more effective regulation." — Source: IDEAS/RePEc

- On Software Paradigms: "Could the principles of good software design be used to improve the way we write financial regulations?" — Source: Goodreads

- On Counter-Cyclical Measures: "Regulators must implement borrowing limits that tighten during booms and loosen during busts to dampen natural market extremes." — Source: IDEAS/RePEc

- On Deliberate Policymaking: "Policymakers frequently react to crises with hasty, emotionally driven rules rather than deliberating carefully to build durable frameworks." — Source: MIT Sloan

- On Financial Literacy for Regulators: "The complexity of modern markets demands that regulators possess the same level of mathematical and technological sophistication as quantitative traders." — Source: CFA Institute

- On Transparency: "Market oversight fails when regulators cannot clearly see the aggregate exposures hidden within shadow banking and derivatives markets." — Source: MIT News

- On Evolutionary Regulation: "Because market participants adapt to new rules, regulation itself must be a continuous, iterative process rather than a static legal code." — Source: Behavioral Economics

- On Professional Certification: "Financial institution leadership should require rigorous professional certification similar to medicine or law, given the systemic damage they can cause." — Source: IDEAS/RePEc

Part 6: Quantitative Finance and Portfolio Management

- On Theory vs. Reality: "A strong quantitative model must incorporate real-world frictions like illiquidity and execution costs, or it is useless in practice." — Source: MIT OpenCourseWare

- On the Limits of Math: "Financial modeling is a tool for structuring thought, not a crystal ball for forecasting the future with exact certainty." — Source: Yale University

- On Return Smoothing: "Investors must heavily scrutinize private and illiquid assets. Their reported low volatility is often a statistical artifact rather than actual risk reduction." — Source: MIT Sloan

- On Technical Analysis: "When viewed through an adaptive lens, technical analysis captures the behavioral footprints of market participants responding to changing environments." — Source: Google Scholar

- On Risk Management: "True risk management requires preparing for structural breaks and regime changes, bypassing reliance on historical volatility distributions." — Source: CFA Institute

- On Portfolio Construction: "The goal is building portfolios durable enough to survive evolutionary shifts in market structure, rather than simply achieving mathematical optimization." — Source: Princeton University

- On Tail Risks: "Standard normal distributions fail in finance because human behavior causes rare, extreme events to cluster during periods of high stress." — Source: IPE

- On Data Quality: "The output of any quantitative strategy is entirely dependent on the cleanliness and context of the input data." — Source: Euromoney

- On the Perfect Portfolio: Lo frames the search for a perfect portfolio as a never-ending journey: investors can learn from the pioneers who shaped portfolio thinking, but the right portfolio remains personal, adaptive, and revisited over time. — Reference: In Pursuit of the Perfect Portfolio page on Lo and the perfect portfolio as a never-ending journey

Part 7: Machine Learning and AI in Finance

- On the AI Revolution: "I believe that within the next five years we're going to see a revolution in how humans interact with AI." — Source: InvestmentNews

- On AI as a Fiduciary: "With the right guardrails, artificial intelligence could be trusted to meet the high bar of fiduciary advice." — Source: InvestmentNews

- On Democratizing Finance: "Machine learning has the capacity to lower the cost of financial planning, bringing sophisticated advice to everyday consumers who find investing scary." — Source: Open Matters

- On Adaptive Algorithms: "Machine learning is uniquely suited for financial markets because algorithms can organically update as the market ecology evolves." — Source: Santa Fe Institute

- On Autonomous Agents: "AI in finance is shifting from being a pure data-analysis tool to an autonomous agent capable of executing high-level strategic decisions." — Source: MIT CSAIL

- On Technology Risks: "Finance can be tremendously powerful when used properly, but it can be a dangerous weapon if incorrectly applied." — Source: Stern Strategy Group

- On Analyzing Behavior: "Large language models and AI can now parse qualitative human behavior and sentiment, adding a new dimension to quantitative forecasting." — Source: University of Pennsylvania

- On Technological Literacy: "The future of asset management belongs to those who can fluently bridge advanced computer science with fundamental economic intuition." — Source: InvestmentNews

- On the Speed of Processing: "AI accelerates the adaptive cycle of markets by processing information and discovering inefficiencies faster than humanly possible." — Source: Scribd

Part 8: Hedge Funds and the Ecology of Finance

- On Market Evolution: "Hedge funds serve as the Galápagos Islands of finance because they are the isolated environments where financial innovation occurs most rapidly." — Source: Financial Times

- On Survival of the Fittest: "The high attrition rate among hedge funds is a direct demonstration of natural selection culling maladaptive strategies." — Source: MIT Sloan

- On Strategy Decay: "Alpha is a finite resource. As successful hedge fund strategies attract capital and imitators, the advantage is competed away." — Source: CFA Institute

- On Illiquidity Premiums: "Much of the outperformance generated by certain hedge funds is simply compensation for bearing the risk of being unable to exit positions during a panic." — Source: MIT News

- On Innovation and Regulation: "Hedge funds often test the boundaries of financial engineering, intentionally operating in the gray areas before regulation catches up." — Source: Yale University

- On Systemic Importance: "Despite their private nature, the interconnectedness of large hedge funds with prime brokers makes their risk management a public concern." — Source: IDEAS/RePEc

- On Interdisciplinary Teams: "The most successful quantitative funds operate like scientific research labs, employing physicists and computer scientists rather than traditional bankers." — Source: Euromoney

- On Alpha vs. Beta: "The line between pure manager skill and passive factor exposure is constantly moving as markets evolve and computation improves." — Source: IPE

- On Market Ecology Roles: "Hedge funds play a specific ecological role as predators of inefficiency, keeping the overall market ecosystem healthy and prices accurate." — Source: Financial Times