Lessons from Angela Aldrich

Angela Aldrich is the founder and CIO of Bayberry Capital Partners, a New York-based long/short equity fund. A former managing director at Blue Ridge Capital, she grounds her global equity investments in primary research and fundamental analysis. This collection outlines her approach to portfolio construction, short selling, and spotting structural market shifts.

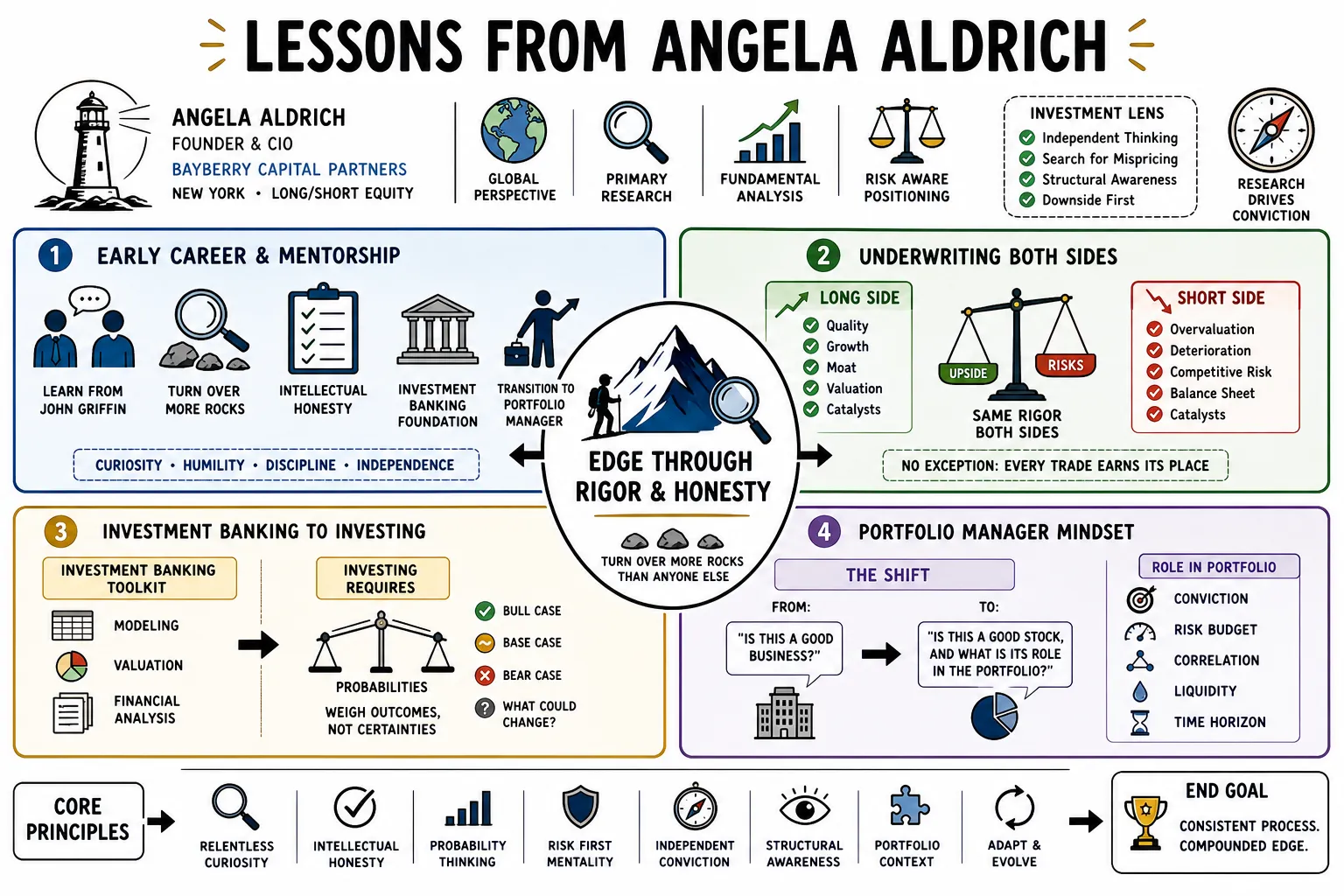

Part 1: Early Career and Mentorship

- On learning from John Griffin: "The most important lesson was that an investment edge comes from turning over more rocks than anyone else." — Source: [Value Investing with Legends Podcast]

- On underwriting rigor: "I learned how to structurally underwrite both sides of a trade, ensuring every long had the same rigor as every short." — Source: [Business Insider Profile]

- On investment banking skills: "Investment banking provided the raw financial modeling toolkit, but investing required learning how to weigh probabilities." — Source: [Financial Times Feature]

- On intellectual honesty: "Being part of that ecosystem teaches you that intellectual honesty is the only way to survive market cycles." — Source: [Worth Magazine]

- On the transition to portfolio manager: "It shifts from asking 'is this a good business?' to 'is this a good stock, and what is its role in the portfolio?'" — Source: [Value Investing with Legends Podcast]

- On working with family businesses: "Working closely with family-owned businesses taught me the value of long-term capital compounding." — Source: [Hedge Fund Journal]

- On evaluating risk early: "You learn quickly that avoiding catastrophic loss is just as vital as finding the multi-bagger." — Source: [Columbia Business School Event]

- On seeking mentors: "The best investors are often the most generous with their time, provided you come prepared with deep, specific questions." — Source: [Value Investing with Legends Podcast]

- On building a foundation: "An economics background at Duke and an MBA at Stanford gave me the macro context for micro decision-making." — Source: [Business Insider Profile]

Part 2: The Foundation of Bayberry Capital

- On launching her own fund: "The decision to launch Bayberry was driven by a desire to apply a rigorous framework in a more nimble, concentrated way." — Source: [Business Insider Profile]

- On naming the firm: "The name reflects a desire to build something enduring and resilient, much like the plant itself." — Source: [Financial Times Feature]

- On being a female founder: "The numbers are still small, but the focus must remain on generating alpha; performance is the ultimate equalizer." — Source: [Worth Magazine]

- On hiring analysts: "I look for analysts who have an insatiable curiosity and an unwillingness to accept management's narrative at face value." — Source: [Hedge Fund Journal]

- On Bayberry's global mandate: "We operate as a global long/short fund because restricting yourself geographically often means missing the best relative value." — Source: [Insider Monkey Q&A]

- On first-year challenges: "You are suddenly managing a business as well as a portfolio, which requires a ruthless prioritization of time." — Source: [Financial Times Feature]

- On cultivating team culture: "An investment team must have psychological safety to pitch a controversial idea and defend it vigorously." — Source: [Value Investing with Legends Podcast]

- On investor alignment: "Finding LPs who understand your timeframe and your tolerance for volatility is critical to surviving drawdowns." — Source: [Worth Magazine]

- On operational excellence: "Alpha generation can easily be offset by operational friction; running a tight ship is non-negotiable." — Source: [Business Insider Profile]

Part 3: Fundamental and Primary Research

- On going beyond filings: "We don't just read the filings; we map out the entire value chain and speak to suppliers, competitors, and former employees." — Source: [Columbia Business School Event]

- On variants of perception: "If you have the exact same inputs as the market, you will get the exact same outputs. You have to look where others aren't." — Source: [Value Investing with Legends Podcast]

- On assessing management: "A great management team can navigate a mediocre industry, but assessing their capital allocation history is essential." — Source: [Hedge Fund Journal]

- On piecing together data: "Primary research is about piecing together a mosaic of qualitative data that quantitative models can't capture." — Source: [Robin Hood Investors Conference]

- On conducting channel checks: "A channel check is useless if it just confirms your bias; you must actively search for disconfirming evidence." — Source: [Value Investing with Legends Podcast]

- On sell-side research: "We use sell-side reports to understand the consensus view, not to generate our own ideas." — Source: [Business Insider Profile]

- On finding an edge: "Our edge usually comes from a longer time horizon and a willingness to underwrite complexity." — Source: [Financial Times Feature]

- On reading financial statements: "The income statement tells you the story management wants you to hear; the cash flow statement tells you the truth." — Source: [Columbia Business School Event]

- On industry structure: "We prefer industries that are consolidating rationally over those that are fragmenting aggressively." — Source: [Insider Monkey Q&A]

- On building conviction: "Conviction is built one phone call, one document, and one debate at a time." — Source: [Value Investing with Legends Podcast]

Part 4: Developing a Differentiated View

- On consensus thinking: "The moment a thesis feels too comfortable is the moment you need to re-underwrite the entire position." — Source: [Value Investing with Legends Podcast]

- On defining value: "Value isn't just a low multiple; it's a mispricing of a company's future cash generation capabilities." — Source: [Columbia Business School Event]

- On thematic investing: "Themes are helpful for sourcing ideas, but every investment must stand on its own bottom-up merits." — Source: [Hedge Fund Journal]

- On tracking market sentiment: "Understanding who is on the other side of your trade is as important as understanding the company itself." — Source: [Business Insider Profile]

- On time horizons: "The market is incredibly efficient over three months, but highly inefficient over three years." — Source: [Value Investing with Legends Podcast]

- On contrarianism: "Being contrarian just for the sake of it is a quick way to lose money. You must be contrarian and right." — Source: [Robin Hood Investors Conference]

- On idea generation: "The best ideas often come from looking at companies going through unglamorous transitions." — Source: [Financial Times Feature]

- On behavioral biases: "We actively monitor our own portfolios for endowment bias, constantly asking if we would buy this stock at today's price." — Source: [Insider Monkey Q&A]

- On spotting inflection points: "We look for businesses undergoing a fundamental change in unit economics that the market hasn't extrapolated yet." — Source: [Columbia Business School Event]

- On maintaining flexibility: "When the facts change, you must have the intellectual honesty to change your mind quickly." — Source: [Value Investing with Legends Podcast]

Part 5: The Art of Short Selling

- On shorting Treasury Wine Estates: "We saw a structural shift in millennial preferences away from wine toward spirits, paired with an oversaturated distribution model." — Source: [Sohn Investment Conference]

- On catalysts for shorts: "Valuation alone is never a short thesis; you need a defined catalyst that will force the market to re-rate the stock." — Source: [Sohn Hearts & Minds]

- On asymmetrical risk: "Shorting is inherently difficult because your upside is capped at 100%, but your downside is mathematically infinite." — Source: [Value Investing with Legends Podcast]

- On identifying short candidates: "We look for businesses facing technological obsolescence, accounting irregularities, or severe capital misallocation." — Source: [Business Insider Profile]

- On shorting consumer fads: "Consumer fads are excellent short candidates once growth decelerates, as the fixed cost deleverage is brutal." — Source: [Sohn Investment Conference]

- On position management: "Shorts require significantly more active trading and risk management than longs due to the inherent volatility." — Source: [Hedge Fund Journal]

- On borrow costs: "A great fundamental short can be ruined by prohibitive borrow costs; the math always has to work." — Source: [Sohn Hearts & Minds]

- On surviving short squeezes: "You must size short positions such that you can survive irrational exuberance without being forced to cover at the top." — Source: [Financial Times Feature]

- On the purpose of the short book: "Our short book isn't just a market hedge; it is designed to be an independent profit center." — Source: [Value Investing with Legends Podcast]

Part 6: Portfolio Construction and Sizing

- On position sizing: "We size positions based on the asymmetry of the risk-reward profile and the depth of our conviction." — Source: [Columbia Business School Event]

- On portfolio concentration: "A highly concentrated portfolio allows us to focus our research efforts on our absolute best ideas." — Source: [Value Investing with Legends Podcast]

- On managing drawdowns: "Portfolio construction is about ensuring that a single idiosyncratic event doesn't permanently impair capital." — Source: [Business Insider Profile]

- On assessing correlation: "We stress-test the portfolio to ensure we aren't taking the same underlying macroeconomic bet across ten different names." — Source: [Hedge Fund Journal]

- On scaling into positions: "We rarely buy a full position on day one; we prefer to average in as our thesis is validated." — Source: [Insider Monkey Q&A]

- On cutting losses: "The hardest discipline in investing is admitting you were wrong and moving on before a small loss becomes a massive one." — Source: [Value Investing with Legends Podcast]

- On letting winners run: "You can't generate outsized returns if you trim your winners too early just to manage volatility." — Source: [Financial Times Feature]

- On cash as a position: "Cash is a residual of the opportunity set, not a macroeconomic call on market direction." — Source: [Robin Hood Investors Conference]

- On dynamic beta exposure: "We manage our net exposure dynamically based on the bottom-up attractiveness of the long versus short opportunity set." — Source: [Columbia Business School Event]

Part 7: Finding Growth and Value in Transition

- On Sensient Technologies: "The market underappreciates the shift toward natural food colorants and the sticky nature of these B2B relationships." — Source: [Robin Hood Investors Conference]

- On ESG frameworks: "We don't view ESG as a constraint; we view it as a framework for identifying companies positioned for sustainable growth." — Source: [Worth Magazine]

- On structural tailwinds: "Investing in companies riding multi-year structural tailwinds provides a margin of safety against execution missteps." — Source: [Hedge Fund Journal]

- On assessing pricing power: "In an inflationary environment, the true test of a business model is whether it can raise prices without sacrificing volume." — Source: [Columbia Business School Event]

- On uncovering hidden assets: "Often, the best investments are those where a valuable subsidiary is masked by a struggling core business." — Source: [Value Investing with Legends Podcast]

- On supply chain shifts: "The transition from globalized just-in-time supply chains to localized resilience creates massive pockets of mispriced capital." — Source: [Business Insider Profile]

- On capital cycles: "We study capital expenditure cycles closely; long periods of underinvestment usually precede substantial margin expansion." — Source: [Financial Times Feature]

- On shifting consumer behavior: "Consumer habits change slowly, but when they do, the shift in market share is often permanent." — Source: [Sohn Investment Conference]

- On regulatory moats: "Companies operating in highly regulated environments often possess deeper moats than the market assigns them credit for." — Source: [Insider Monkey Q&A]

- On technological disruption: "You don't always have to invest in the disruptor; sometimes it's more profitable to short the incumbent that refuses to adapt." — Source: [Value Investing with Legends Podcast]

Part 8: Navigating the Hedge Fund Landscape

- On the state of value investing: "Value investing isn't dead; it has just evolved beyond simple price-to-book metrics into a more nuanced assessment of business quality." — Source: [Columbia Business School Event]

- On market volatility: "Volatility is the price you pay for liquidity; for the prepared investor, it is a source of opportunity, not a threat." — Source: [Sohn Hearts & Minds]

- On the impact of passive investing: "The relentless flow into passive vehicles creates significant price distortions that active managers can exploit." — Source: [Business Insider Profile]

- On diversity in finance: "Diverse teams naturally possess broader variants of perception, which directly translates to better investment outcomes." — Source: [Worth Magazine]

- On continuous learning: "The market is a humbling mechanism; the day you think you have it all figured out is the day you start losing." — Source: [Value Investing with Legends Podcast]

- On filtering noise vs. signal: "90% of financial news is noise designed to provoke a reaction. We spend our time looking for the 10% that constitutes an actual signal." — Source: [Financial Times Feature]

- On capping firm growth: "We are intentional about capacity; managing too much capital is the fastest way to dilute your returns." — Source: [Insider Monkey Q&A]

- On macroeconomic awareness: "We are bottom-up stock pickers, but we must be aware of the macro environment to ensure we aren't fighting a systemic headwind." — Source: [Hedge Fund Journal]

- On long-term objectives: "Our objective is to deliver compounding returns over a decade, which requires patience, discipline, and an unwavering commitment to our process." — Source: [Robin Hood Investors Conference]