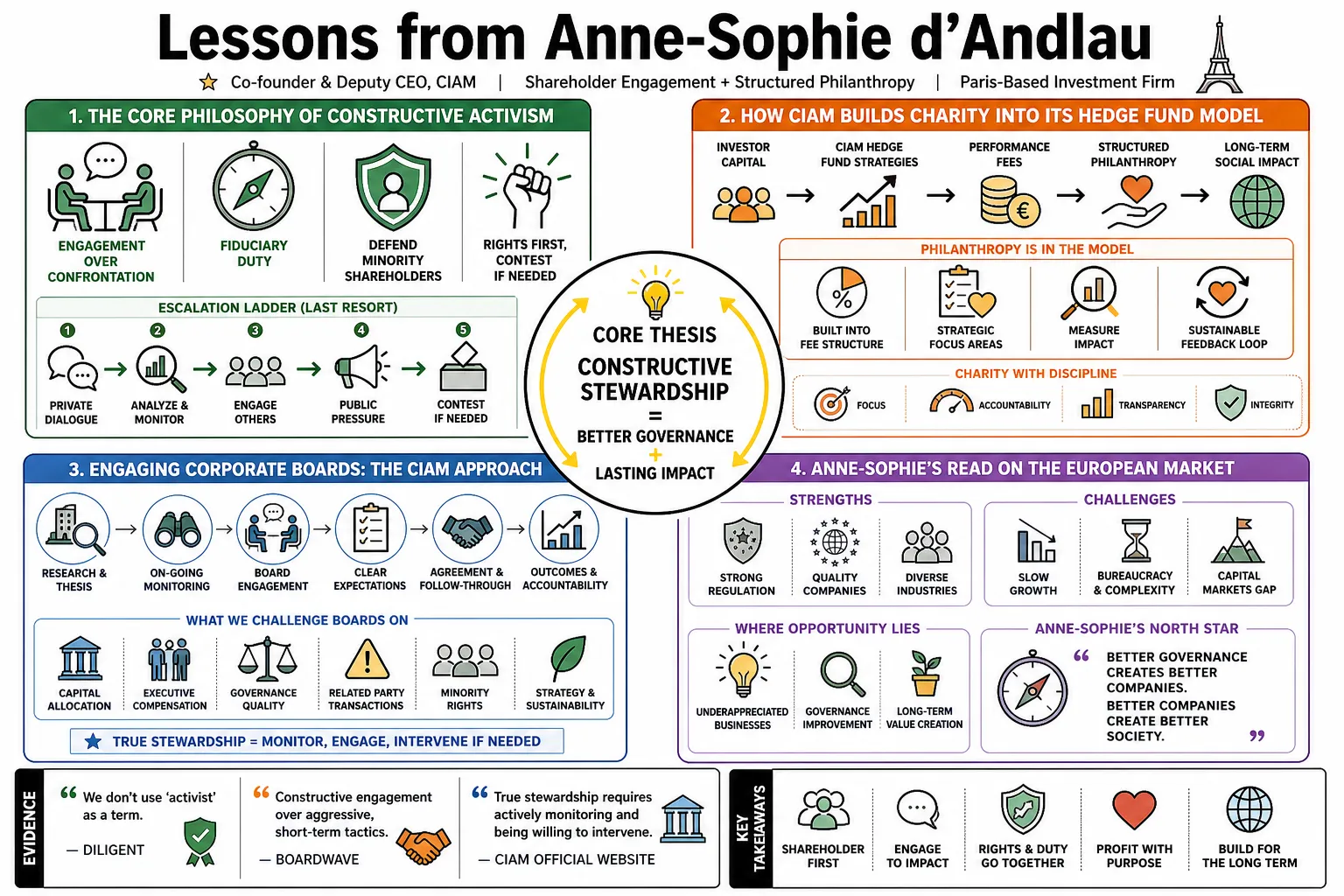

Lessons from Anne-Sophie d'Andlau

Anne-Sophie d'Andlau is the co-founder and Deputy CEO of CIAM, a Paris-based investment firm that pairs shareholder engagement with structured philanthropy. She regularly challenges the boards of major European corporations to defend minority shareholders and demand strict governance. This profile covers her approach to engaging with corporate boards, how CIAM builds charity into its hedge fund model, and her read on the European market.

Part 1: The Core Philosophy of Constructive Activism

- On the "Activist" Label: "We don't use 'activist' as a term. We see ourselves as a shareholder, doing our fiduciary duty and if there is no dialogue, we will use our rights, speak to others and consider a contest if needed." — Source: Diligent

- On Engagement Over Confrontation: "The firm's approach is rooted in constructive engagement with businesses to make a tangible impact, rather than relying on aggressive, short-term tactics." — Source: Boardwave

- On Fiduciary Duty: "True stewardship requires actively monitoring portfolio companies and being willing to intervene when management strays from shareholders' best interests." — Source: CIAM Official Website

- On Dispelling the "Raider" Myth: "Activism in the modern European context is about improving governance and unlocking value, rather than indiscriminately stripping assets for immediate gain." — Source: Harvard Law School Forum on Corporate Governance

- On Building a Case: "Effective intervention requires rigorous, deep-dive due diligence before ever approaching a company’s board with demands." — Source: Hedgeweek

- On Escalation: "While dialogue is the preferred starting point, an engaged investor must be prepared to escalate to public campaigns and proxy contests if the board refuses to listen." — Source: Droit & Croissance

- On Constructive Dialogue: "The most successful outcomes often occur when boards are willing to engage privately and address governance flaws before a public dispute becomes necessary." — Source: Opalesque TV

- On Targeting Inefficiencies: "The strategy relies on identifying companies with sound underlying assets that are severely held back by poor management structures or strategic missteps." — Source: House of Beautiful Business

- On Long-Term Value: "The goal of intervention is establishing sustainable governance frameworks that protect value over the long haul, rather than seeking a temporary stock bump." — Source: CIAM Official Website

- On Accountability: "Active management means holding leadership accountable; passive investing often gives underperforming management teams a free pass." — Source: Boardwave

Part 2: Defending Minority Shareholder Rights

- On Protecting Market Integrity: "These three demergers on foreign markets will not close the discount. They represent an extreme case of where minority rights are being undermined... the implications of the demerger go beyond shareholder rights and threaten market integrity." — Source: Financial Times

- On Controlling Shareholders: "A recurring theme in our campaigns is pushing back against dominant or family shareholders who attempt to extract value at the expense of the broader investor base." — Source: The Hedge Fund Journal

- On Squeeze-Outs and Buyouts: "In cases like Club Med, we demonstrated that minority investors do not have to accept initial, inadequate buyout offers from controlling entities." — Source: Opalesque TV

- On Undervaluation: "When parent companies attempt to acquire subsidiaries on the cheap, activists must step in to demand fair asset valuation." — Source: Boardwave

- On Equal Treatment: "The foundational principle of public markets is that all shareholders, regardless of their size, deserve equal treatment and proportional voting power." — Source: Droit & Croissance

- On Legal Recourse: "When corporate structures are used to deliberately bypass minority approval, utilizing legal channels becomes a necessary tool for asset protection." — Source: Financial Times

- On Structural Discounts: "Conglomerate discounts often persist because management prioritizes empire-building over the financial realities faced by minority stakeholders." — Source: CIAM Official Website

- On Transparency: "Minority shareholders must relentlessly demand transparency in how related-party transactions and royalty fees are structured." — Source: The Hedge Fund Journal

- On Voting Power: "Exercising voting rights at annual general meetings is the most direct mechanism minority investors have to signal dissatisfaction with board decisions." — Source: Diligent

Part 3: The Intersection of Philanthropy and Finance

- On Purpose-Driven Finance: "The firm's name, Charity Investment Asset Management, was deliberately chosen to reflect a structural commitment to philanthropy from day one." — Source: CIAM Official Website

- On Donating Performance Fees: "By pledging 25% of our performance fees to charitable causes, we aligned our financial success directly with social impact." — Source: The Hedge Fund Journal

- On CIAM For Kids: "The firm channels its philanthropic efforts into supporting organizations focused on improving childhood health and education." — Source: Opalesque TV

- On Aligning Incentives: "Integrating a charitable mandate into the fund’s core structure provides the team with a deeper motivation beyond standard financial returns." — Source: House of Beautiful Business

- On Redefining the Hedge Fund Model: "The traditional view of activist funds as purely profit-driven entities is challenged by a model that actively redistributes wealth to vulnerable populations." — Source: Boardwave

- On Corporate Social Responsibility: "An investment firm cannot demand better ESG practices from its portfolio companies without first modeling responsible behavior in its own operations." — Source: CIAM Official Website

- On Global Impact: "The charitable donations span initiatives across Europe and internationally, reflecting a broad view of corporate citizenship." — Source: Opalesque TV

- On Giving Back: "The decision to incorporate charity into the business model was driven by a personal conviction that successful professionals have a duty to give back to society." — Source: Boardwave

- On Sustainable Philanthropy: "Tying donations to performance fees ensures that the firm's charitable contributions grow in tandem with its success in the market." — Source: The Hedge Fund Journal

Part 4: Corporate Governance and Board Accountability

- On Succession Planning: "Extended tenures by founders or long-serving chairmen can become a significant governance risk if clear, timely succession plans are not enforced." — Source: Hedgeweek

- On Poison Pills: "Defensive structures, such as the Dutch stichting foundation used by Ahold, are often utilized to entrench management and block legitimate shareholder initiatives." — Source: The Hedge Fund Journal

- On Board Independence: "A board cannot function effectively if it is overly deferential to a dominant CEO; true independence is required to provide necessary oversight." — Source: CIAM Official Website

- On Executive Compensation: "Pay packages must be rigorously tied to actual performance metrics, rather than rewarding executives during periods of market underperformance." — Source: Hedgeweek

- On the Separation of Powers: "Splitting the roles of Chairman and CEO is a fundamental governance practice that prevents the concentration of power in a single individual." — Source: Harvard Law School Forum on Corporate Governance

- On Challenging the Status Quo: "Boards in legacy companies often suffer from complacency; an outside perspective is frequently required to force necessary operational shifts." — Source: Boardwave

- On Director Accountability: "Individual directors must be held accountable when they fail to challenge management decisions that destroy shareholder value." — Source: Diligent

- On Transparent Reporting: "Governance requires clear, unambiguous communication from the board regarding strategy, risks, and capital allocation decisions." — Source: Droit & Croissance

- On Over-Boarding: "Directors who sit on too many boards lack the time and focus required to properly navigate complex corporate crises." — Source: CIAM Official Website

- On Evaluating Management: "The ultimate test of a board's effectiveness is its willingness to replace an underperforming management team." — Source: Hedgeweek

Part 5: M&A, Strategy, and Unlocking Value

- On Inadequate Buyout Premiums: "Initial buyout offers are often opportunistic attempts to acquire assets below their intrinsic value, requiring organized pushback from shareholders." — Source: Opalesque TV

- On Demerger Risks: "Breaking up a conglomerate only creates value if the resulting entities have clear strategic rationale and list in markets that protect investor rights." — Source: Financial Times

- On Assessing Synergies: "Proposed M&A synergies must be scrutinized heavily, as management teams frequently overstate them to justify expensive acquisitions." — Source: CIAM Official Website

- On the Veolia/Suez Battle: "High-profile corporate takeovers require vigilant shareholders to ensure that the final terms adequately compensate the target's investors." — Source: Wikipedia

- On Strategy Shifts: "When a company abruptly changes its core strategy without shareholder consultation, it is a clear trigger for activist intervention." — Source: Boardwave

- On Hidden Value: "The most lucrative activist campaigns involve identifying companies where real estate or subsidiary assets are not accurately reflected in the share price." — Source: The Hedge Fund Journal

- On Capital Allocation: "Hoarding cash or pursuing vanity projects destroys value; activists must push for prudent capital return programs like dividends or buybacks." — Source: Hedgeweek

- On Rejecting Lowball Offers: "Institutional investors must learn to reject the certainty of a lowball offer in favor of fighting for the true fair value of the business." — Source: Droit & Croissance

- On Market Discounts: "A persistent discount to net asset value is a symptom of market distrust in the current management's ability to execute." — Source: CIAM Official Website

Part 6: Integrating ESG into Activism

- On Governance as the Foundation: "Environmental and social initiatives cannot be effectively implemented if a company lacks the fundamental governance structures to oversee them." — Source: Boardwave

- On Holding Boards to ESG Targets: "It is insufficient for companies to publish sustainability reports; they must be held accountable by shareholders for missing environmental targets." — Source: CIAM Official Website

- On Responsible Stewardship: "Integrating ESG into the investment process is a core component of fiduciary duty, as climate and social risks directly impact long-term financial returns." — Source: Diligent

- On the PRI: "Active participation in organizations like the Principles for Responsible Investment helps standardize how activists can apply ESG pressure globally." — Source: House of Beautiful Business

- On Measuring Social Impact: "Just as financial returns are quantified, the social impact of corporate policies must be rigorously assessed." — Source: The Hedge Fund Journal

- On Sustainable Transitions: "Activists play a necessary role in pushing carbon-intensive businesses to adopt realistic, actionable transition plans rather than mere greenwashing." — Source: Droit & Croissance

- On Transparency in Reporting: "Companies must provide clear, standardized ESG data so that investors can make accurate comparisons across industries." — Source: CIAM Official Website

- On ESG as a Value Driver: "Improving a company's environmental and social footprint is a primary lever for expanding valuation multiples, moving beyond a simple compliance exercise." — Source: Boardwave

- On Board Diversity: "Pushing for gender and cognitive diversity at the board level is a vital part of the governance mandate, leading to better decision-making and risk management." — Source: Opalesque TV

Part 7: Navigating the European Market

- On the Evolution of French Activism: "The French market has historically been resistant to activist intervention, but the environment is shifting as institutional investors become more vocal." — Source: Harvard Law School Forum on Corporate Governance

- On Regulatory Environments: "European regulatory frameworks often provide unique tools and unique hurdles that require a tailored, localized approach compared to US-style activism." — Source: Droit & Croissance

- On Cultural Resistance: "Activists in Europe must navigate a business culture that traditionally views public confrontation as taboo, necessitating a more nuanced engagement strategy." — Source: Boardwave

- On M&A Dynamics in France: "The presence of the state and influential families in French corporations means that activists must build broad consensus to block or alter major transactions." — Source: Financial Times

- On Building Consensus: "Success in European activism relies heavily on quietly aligning with other institutional shareholders before going public with a campaign." — Source: Hedgeweek

- On Overcoming the Stigma: "The perception of activists as hostile raiders is slowly fading in Paris and London as they prove their ability to drive long-term strategic improvements." — Source: Diligent

- On Legal Frameworks: "Understanding the intricacies of European corporate law, such as the rights of minority shareholders in different jurisdictions, is essential for mounting a successful defense." — Source: The Hedge Fund Journal

- On Institutional Support: "The willingness of passive asset managers to support activist resolutions is the deciding factor in modern European proxy battles." — Source: CIAM Official Website

- On Cross-Border Complexity: "When engaging companies with listings or operations across multiple European countries, activists must account for conflicting regulatory regimes." — Source: Opalesque TV

Part 8: Resilience and Leadership in Finance

- On Overcoming Skepticism: "When people tell you that what you want to do is impossible, what do you do? Does it stop you or does it motivate you to continue and really do what you want to achieve?" — Source: Boardwave

- On Founding CIAM: "Launching an activist fund in 2010 required a potent combination of determination, extensive experience, and a willingness to embrace significant career risk." — Source: Opalesque TV

- On Being a Female Founder: "Navigating a deeply male-dominated industry required building a firm culture rooted in absolute meritocracy and resilience against institutional bias." — Source: House of Beautiful Business

- On The Drive to Succeed: "True leadership in finance demands a taste for facing formidable challenges and the tenacity to see multi-year campaigns through to the end." — Source: Boardwave

- On Pushing Back Against Giants: "Challenging corporate juggernauts requires a thick skin, as establishment entities will often utilize immense resources to discredit dissenting shareholders." — Source: Financial Times

- On Calculated Risks: "Activism is inherently risky; success depends on rigorous preparation so that when a public stance is taken, the underlying thesis is unassailable." — Source: CIAM Official Website

- On Partnership: "The partnership with co-founder Catherine Berjal demonstrates that aligned values and complementary skill sets are the foundation of a resilient firm." — Source: The Hedge Fund Journal

- On Building a Unique Culture: "Embedding philanthropy and a focus on minority rights into the firm's DNA has created a workplace culture distinct from traditional hedge funds." — Source: Diligent

- On Leaving a Legacy: "Success is ultimately measured by the permanent improvements made to corporate governance and the societal impact of the firm's charitable giving, rather than purely by returns generated." — Source: Opalesque TV

- On Continuous Motivation: "When faced with systemic resistance, the motivation to continue must stem from a deep-seated belief in the necessity of accountability and fairness in the markets." — Source: Boardwave