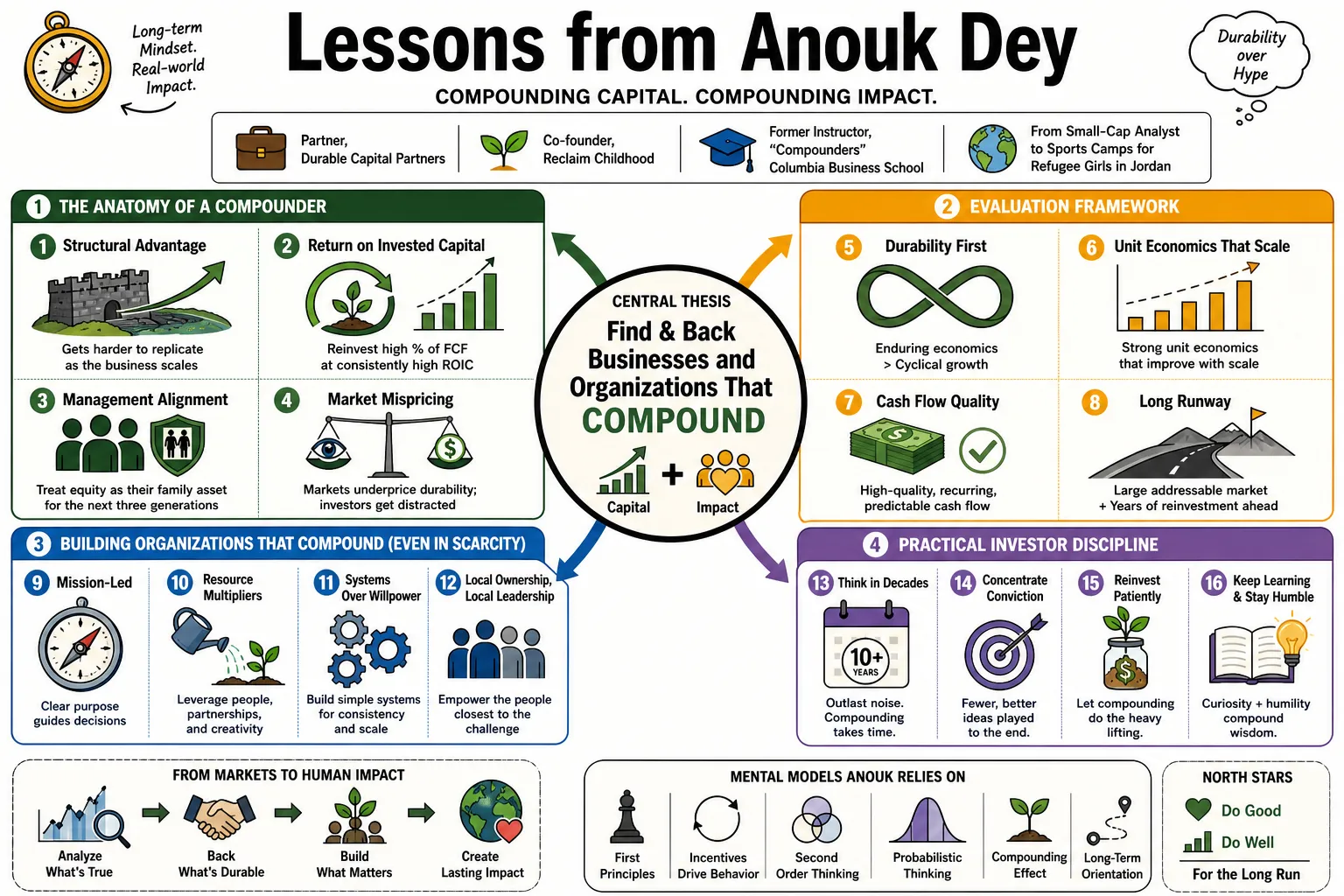

Anouk Dey is a partner at Durable Capital Partners, co-founder of the non-profit Reclaim Childhood, and a former instructor of the "Compounders" course at Columbia Business School. Her background spans analyzing small-cap growth stocks at T. Rowe Price to operating sports camps for refugee girls in Jordan. This outline covers her methodology for evaluating long-term equities and her approach to building sustainable organizations in resource-constrained environments.

Part 1: The Anatomy of a Compounder

- On structural advantages: "A true compounder relies on a structural advantage that becomes harder to replicate as the business scales, rather than a temporary edge in pricing or marketing." — Source: [Columbia Business School]

- On return on invested capital: "The math of long-term wealth creation requires companies that can reinvest a large portion of their free cash flow back into the business at consistently high rates of return." — Source: [Columbia Business School]

- On management alignment: "You want to find management teams who treat the company's equity as if it were their sole family asset for the next three generations." — Source: [Value Investing with Legends Podcast]

- On market mispricing: "Public markets frequently underprice durability. Investors are easily distracted by quarter-to-quarter variance and miss the mathematical power of a business growing steadily over a decade." — Source: [Value Investing with Legends Podcast]

- On qualitative moats: "The most protective moats are often cultural or behavioral. They do not appear on a balance sheet but manifest in customer loyalty and employee retention." — Source: [Columbia Business School]

- On patience: "Holding a compounding asset through market cycles is psychologically demanding. The instinct to act is strong, but the correct action is often to do nothing." — Source: [Value Investing with Legends Podcast]

- On capital intensity: "Businesses that can grow without requiring massive, continuous capital expenditures have a natural defense against inflationary environments." — Source: [Durable Capital Partners]

- On identifying the runway: "A high reinvestment rate only matters if the total addressable market is large enough to absorb that capital without diminishing returns." — Source: [Columbia Business School]

- On disruption risk: "A compounder must be adaptable. A static moat eventually dries up if the underlying technology or consumer preference shifts fundamentally." — Source: [Value Investing with Legends Podcast]

- On portfolio concentration: "If you identify a rare business capable of sustained high returns, the logical response is to size the position meaningfully rather than dilute your returns with mediocre ideas." — Source: [Columbia Business School]

Part 2: Value Investing in the Modern Era

- On defining value: "Value investing is not strictly about buying statistically cheap stocks. It is about acquiring an asset for less than the present value of its future cash flows, regardless of the P/E ratio." — Source: [Value Investing with Legends Podcast]

- On intangible assets: "Modern accounting rules heavily penalize companies that invest in software and research, often masking the true economic earning power of digital-first businesses." — Source: [Value Investing with Legends Podcast]

- On the shift from manufacturing: "We have transitioned from an economy constrained by physical capital to one constrained by human capital and network effects. Investment frameworks must adjust accordingly." — Source: [Value Investing with Legends Podcast]

- On margin expansion: "A low-margin business scaling rapidly can be a classic value investment if the unit economics dictate that margins will expand once customer acquisition costs stabilize." — Source: [Value Investing with Legends Podcast]

- On evaluating tech monopolies: "Network effects create winner-take-most markets. The value investor's job is to identify these dynamics early before the dominance is fully priced in." — Source: [Durable Capital Partners]

- On the danger of value traps: "A statistically cheap company in secular decline is a liability, not a bargain. Mean reversion is not a law of physics in business." — Source: [Value Investing with Legends Podcast]

- On forecasting growth: "Growth is simply a component of the value equation. The mistake is treating growth and value as opposing investment styles rather than parts of the same calculation." — Source: [Value Investing with Legends Podcast]

- On market efficiency: "Information is more widely distributed than ever, but investor time horizons have shortened. The remaining inefficiency in the market is time arbitrage." — Source: [Value Investing with Legends Podcast]

- On regulatory risk: "As digital platforms reach utility-like status, the primary risk shifts from competition to regulation. Valuations must incorporate the cost of future compliance." — Source: [Durable Capital Partners]

- On adapting frameworks: "Graham and Dodd principles are foundational, but rigidly applying twentieth-century metrics to modern businesses will yield flawed conclusions." — Source: [Value Investing with Legends Podcast]

Part 3: Small-Cap and Growth Strategy

- On finding emerging leaders: "Small-cap investing requires identifying businesses that have already solved their product-market fit but have not yet scaled their distribution." — Source: [T. Rowe Price]

- On execution risk: "In a large cap, the system runs the company. In a small cap, the founder runs the company. Evaluating the individual is non-negotiable." — Source: [T. Rowe Price]

- On surviving downturns: "Small companies with weak balance sheets do not survive recessions. Cash flow generation early in the lifecycle is a strong indicator of durability." — Source: [T. Rowe Price]

- On market obscurity: "The lack of analyst coverage in the small-cap space provides an opportunity to build deep fundamental conviction before the broader market recognizes the asset." — Source: [T. Rowe Price]

- On scaling operations: "Many companies can sell a great product to early adopters. The true test of a growth company is whether it can build a sales force to reach the mainstream." — Source: [Durable Capital Partners]

- On niche dominance: "A small-cap company that dominates a narrow, unglamorous niche often produces better shareholder returns than a company fighting for a sliver of a massive market." — Source: [Durable Capital Partners]

- On capital raises: "Dilution is a reality in small-cap growth. The question is whether the capital being raised is funding accretive projects or merely covering operational burn." — Source: [T. Rowe Price]

- On transitioning to mid-cap: "The skills required to manage a small company are different from those needed for a mid-sized one. Management upgrades are often a necessary friction." — Source: [T. Rowe Price]

- On early-stage volatility: "Price swings in small caps are severe and often disconnected from fundamentals. You must underwrite the business, not the daily quote." — Source: [T. Rowe Price]

Part 4: Capital Allocation and Leadership

- On evaluating capital allocators: "A CEO's primary job is capital allocation, yet most are promoted for their operational skills. The mismatch requires investors to scrutinize every acquisition and buyback." — Source: [Columbia Business School]

- On dividend policy: "Dividends are a promise. If a company cannot sustain them without starving its core business of investment, the capital structure is flawed." — Source: [Columbia Business School]

- On share repurchases: "Buybacks create value only when the stock is trading below intrinsic value. Systematic buybacks regardless of price often destroy shareholder wealth." — Source: [Value Investing with Legends Podcast]

- On programmatic M&A: "Companies that grow through small, frequent, and adjacent acquisitions tend to outperform those that rely on large, transformative megadeals." — Source: [Columbia Business School]

- On founder-led firms: "Founders possess a moral authority within their organizations that professional managers struggle to replicate. This allows them to make unpopular, long-term decisions." — Source: [Durable Capital Partners]

- On tracking track records: "When assessing a management team, look at what they did during the last industry downturn. Capital allocation errors are made in the boom and revealed in the bust." — Source: [Columbia Business School]

- On organizational debt: "Rapid growth often masks organizational debt: poor processes, redundant layers, and technical compromises that eventually drag down margins." — Source: [Columbia Business School]

- On aligning incentives: "Compensation structures should reward long-term cash flow generation and return on equity, avoiding short-term revenue targets or absolute stock price levels." — Source: [Columbia Business School]

- On strategic patience: "Sometimes the best capital allocation decision a CEO can make is to let cash build on the balance sheet until a mispriced opportunity presents itself." — Source: [Value Investing with Legends Podcast]

Part 5: Navigating Global Affairs and Policy

- On geopolitical risk: "Investors frequently underestimate geopolitical risk because it is difficult to model. However, shifts in trade policy or sanctions can permanently alter a company's supply chain." — Source: [OpenCanada]

- On international norms: "The stability of global markets depends on adherence to international norms. When those norms erode, the risk premium on cross-border investments must increase." — Source: [University of Oxford]

- On emerging markets: "Growth in emerging markets is not linear. It is frequently interrupted by currency devaluations and political instability, requiring a different margin of safety." — Source: [University of Oxford]

- On public policy impact: "A single regulatory shift can instantly change the competitive environment. Understanding the political climate is as necessary as understanding a balance sheet." — Source: [OpenCanada]

- On information ecosystems: "The fragmentation of media and the rise of digital echo chambers have complicated how societies reach consensus on foundational issues." — Source: [OpenCanada]

- On global supply chains: "Efficiency has been prioritized over resilience for decades. The future will require companies to build redundancy into their sourcing, even if it hurts short-term margins." — Source: [OpenCanada]

- On local context: "You cannot evaluate an international business without understanding the specific political economy and cultural nuances of its domestic market." — Source: [University of Oxford]

- On diplomatic constraints: "State actions are often constrained by domestic political realities rather than grand strategic logic. Policy analysis must start at the local level." — Source: [OpenCanada]

- On soft power: "The cultural export of ideas and norms often paves the way for commercial expansion. Soft power has tangible economic value." — Source: [OpenCanada]

Part 6: Reclaiming Childhood Through Sport

- On the right to play: "For children displaced by conflict, the simple act of playing on a team provides a baseline of normalcy that is necessary for trauma recovery." — Source: [Reclaim Childhood]

- On safe spaces: "Creating physical safety is the first step. Girls in refugee communities need designated spaces where they can simply exist without fear." — Source: [Reclaim Childhood]

- On leadership development: "Sports force rapid decision-making, communication, and conflict resolution. It is a real-time laboratory for building leadership skills." — Source: [Reclaim Childhood]

- On breaking social barriers: "When you put a Syrian refugee, a Palestinian refugee, and a local Jordanian girl on the same basketball team, the geopolitical divisions dissolve into a shared goal." — Source: [Reclaim Childhood]

- On local coaching: "A program is only sustainable if it is run by the community. Training local women to become coaches ensures the knowledge remains long after initial funding." — Source: [Reclaim Childhood]

- On physical autonomy: "Teaching girls how to command their physical bodies through athletics translates directly into confidence in their social and academic lives." — Source: [Reclaim Childhood]

- On the compounding effect of intervention: "Reaching a girl at age ten changes the trajectory of her adolescence. The return on investment for early social intervention is staggeringly high." — Source: [UNHCR Nansen Refugee Award]

- On overcoming logistics: "Running a non-profit in a resource-constrained environment requires operating with the pragmatism of a startup. You figure out transportation, permits, and equipment through sheer persistence." — Source: [Reclaim Childhood]

- On defining impact: "Metrics are necessary for donors, but true impact is seen when a participant returns five years later asking to become a mentor." — Source: [Reclaim Childhood]

- On universal language: "You don't need to speak the same dialect to understand a pass or a goal. Sport bypasses linguistic and cultural friction." — Source: [UNHCR Nansen Refugee Award]

Part 7: The Competitive Athlete's Mindset

- On competitive discipline: "Ski racing demands an intense focus on mechanics and repetition. The margin between winning and losing is measured in fractions of a second, teaching you to respect the details." — Source: [Williams College Athletics]

- On processing failure: "In athletics, you lose far more often than you win. Learning to extract data from a loss without letting it damage your confidence is a transferable skill." — Source: [Williams College Athletics]

- On operating under pressure: "The physical response to a starting gate is the same as the physical response to a high-stakes meeting. The discipline is in controlling the adrenaline." — Source: [Williams College Athletics]

- On continuous feedback: "Athletes review tape constantly. In professional careers, we rarely seek that level of objective, unvarnished feedback on our daily performance." — Source: [FIS Ski]

- On the isolation of performance: "Even in team sports, individual execution is solitary. You have to take personal responsibility for your preparation before you can contribute to the group." — Source: [Williams College Athletics]

- On mental endurance: "Fatigue challenges focus. Building physical endurance is simply a prerequisite for maintaining mental clarity in the final stages of a competition." — Source: [FIS Ski]

- On managing variables: "In alpine skiing, the course conditions change with every competitor. You cannot control the environment, only your adaptation to it." — Source: [FIS Ski]

- On goal setting: "Amateur athletes focus on the outcome. Professional athletes focus on the process. If the process is correct, the outcome takes care of itself." — Source: [Williams College Athletics]

- On transition and identity: "Leaving competitive sports forces a complete rebuilding of identity. The drive remains, but it must be channeled into entirely new cognitive challenges." — Source: [Williams College Athletics]

Part 8: Academic Mentorship and Independent Study

- On the Socratic method: "Teaching investment principles forces you to clarify your own thinking. If you cannot explain a thesis to a bright student, you don't understand it well enough." — Source: [Columbia Business School]

- On case study limitations: "Historical case studies are neat and resolved. Real-world investing is messy and uncertain. Students need exposure to live, unresolved business problems." — Source: [Columbia Business School]

- On building intellectual honesty: "The most important trait to develop in students is the willingness to abandon a cherished hypothesis when the facts change." — Source: [Columbia Business School]

- On filtering noise: "Young analysts often build overly complex models to mask a lack of fundamental understanding. Mentorship involves stripping away the noise to find the core driver." — Source: [Columbia Business School]

- On structural thinking: "Education should prioritize frameworks over facts. Facts are easily acquired; the ability to structure a problem logically is rare." — Source: [Columbia Business School]

- On challenging consensus: "An independent study course is designed to push students away from the consensus view. The consensus is already priced in." — Source: [Columbia Business School]

- On empowering young women: "Representation in finance and leadership matters. Seeing women in capital allocation roles normalizes the ambition for the next generation." — Source: [Women's Executive Network]

- On practical application: "Theory detached from execution is useless. Students must learn how to size a position, manage risk, and endure volatility." — Source: [Columbia Business School]

- On lifelong learning: "The best investors view themselves as permanent students of business. The moment you think your framework is complete, the market will humble you." — Source: [Columbia Business School]