Lessons from Antti Ilmanen

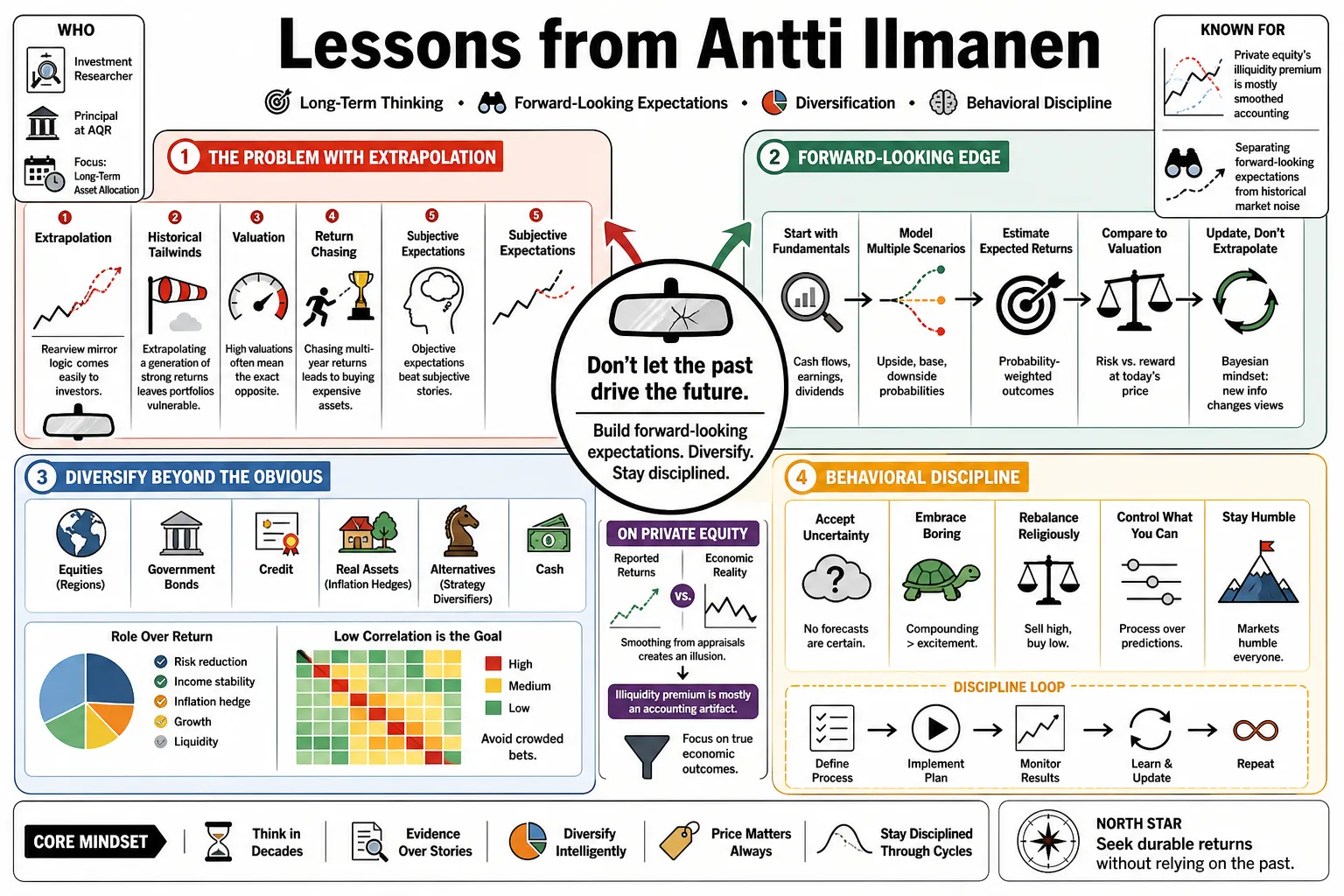

Antti Ilmanen is an investment researcher and Principal at AQR Capital Management focused on long-term asset allocation. He is known for showing that private equity's illiquidity premium is mostly a result of smoothed accounting, and for separating forward-looking expectations from historical market noise. This profile outlines his practical approach to diversifying portfolios and maintaining behavioral discipline when traditional assets offer low yields.

Part 1: The Problem with Extrapolation

- On Extrapolation: "Rearview mirror logic comes easily to investors, making them prone to extrapolate past successes into the future." — Source: [Bogle Center for Financial Literacy]

- On Historical Tailwinds: "Extrapolating a generation of strong realized returns leaves portfolios vulnerable when historical tailwinds shift to headwinds." — Source: [AQR Insights]

- On Valuation: "Investors frequently conflate high past returns with high future returns, when high valuations often mean the exact opposite." — Source: [The Meb Faber Show]

- On Return Chasing: "The human tendency to chase multi-year returns forces investors to buy expensive assets just before they revert to the mean." — Source: [Rational Reminder]

- On Subjective Expectations: "Objective expectations based on yields clash constantly with subjective expectations driven by recent market momentum." — Source: [Bogle Center for Financial Literacy]

- On Changing Environments: "A changing market environment requires abandoning the simple heuristics that worked during the previous decade." — Source: [AQR Capital Management]

- On Market Pricing: "Market pricing mechanisms mask the underlying shift in expected returns, making extrapolation feel safe until it fails." — Source: [Flirting with Models]

- On Behavioral Errors: "Relying on the recent past to predict the distant future is the most common behavioral error in long-term asset allocation." — Source: [The Meb Faber Show]

- On Structural Assumptions: "Investors must actively resist their own instinct to assume that a strategy’s recent success is a permanent structural feature." — Source: [Rational Reminder]

- On Data and Evidence: "Let ideas compete freely and let data be the judge, rather than relying on recent performance as the sole arbiter of truth." — Source: [Goodreads]

Part 2: Managing Expectations and Serenity

- On The Serenity Prayer: "God, grant me the serenity to accept the things I cannot change, the courage to change the things I can, and the wisdom to know the difference." — Source: [The Meb Faber Show]

- On Controllable Factors: "Investors cannot control random market shocks or baseline yields, but they can control their asset allocation, diversification, and fee structures." — Source: [Rational Reminder]

- On Accepting Reality: "Faced with low expected returns, one option is simply to accept the reality, lower spending plans, and increase savings rates." — Source: [AQR Insights]

- On Reaching for Yield: "Reaching for yield by blindly increasing risk exposure is a common, but dangerous, response to a low-return environment." — Source: [The Big Picture Blog]

- On Building Resilience: "The most viable path forward often involves building a better, more resilient portfolio rather than blindly accepting lower returns or taking uncompensated risk." — Source: [AQR Capital Management]

- On Acknowledging Limits: "Accepting the limitations of the current market environment is the first step in avoiding catastrophic allocation mistakes." — Source: [Rational Reminder]

- On Resisting Fads: "Serenity in investing means resisting the urge to fix a low expected return environment by chasing speculative fads." — Source: [The Meb Faber Show]

- On Tailwinds: "A low expected return environment does not mean negative returns are guaranteed, only that the tailwinds of the past are exhausted." — Source: [Flirting with Models]

- On Calibrating Expectations: "Investors must actively calibrate their expectations downward when initial yields and valuations are near historical extremes." — Source: [AQR Capital Management]

- On Courage: "Courage in the context of the serenity prayer means diversifying away from comfortable, home-country assets when they are overpriced." — Source: [Bogle Center for Financial Literacy]

Part 3: The Mechanics of Diversification

- On the 60/40 Portfolio: "Traditional 60/40 asset allocation is often highly concentrated in equity market direction, masking a lack of true diversification." — Source: [AQR Insights]

- On The Cube Framework: "Investors should view their portfolios through three dimensions: asset classes, strategy styles, and underlying macroeconomic risk factors." — Source: [Rational Reminder]

- On Bold Diversification: "Broad, bold diversification requires moving capital away from familiar equity indices into uncorrelated return streams." — Source: [The Meb Faber Show]

- On the Cost of Diversification: "True diversification means accepting that different parts of your portfolio will perform poorly at different times." — Source: [Bogle Center for Financial Literacy]

- On Narrow Framing: "Narrow framing causes investors to evaluate individual assets in isolation rather than focusing on their contribution to total portfolio risk." — Source: [AQR Capital Management]

- On Risk Exposures: "A portfolio should be thought of as a bundle of underlying risk exposures rather than a collection of tickers." — Source: [Rational Reminder]

- On Correlation: "Combining assets with low or negative correlation to one another is the most reliable way to improve risk-adjusted outcomes." — Source: [Flirting with Models]

- On Equity Beta: "Over-reliance on equity beta leaves portfolios exposed to specific economic regimes, requiring a structural shift to fix." — Source: [AQR Insights]

- On Source of Volatility: "Effective diversification looks beyond nominal capital allocation to measure where the actual volatility in a portfolio originates." — Source: [The Meb Faber Show]

- On Separating Return Sources: "The Cube framework forces allocators to separate market direction from the specific premiums generated by different investment styles." — Source: [AQR Capital Management]

Part 4: Harvesting Alternative Premia

- On Risk Premia: "Returns are best understood as bundles of risk premia, including broad market exposure and specific style factors." — Source: [AQR Insights]

- On Value: "Value investing relies on the fundamental tendency of cheap assets to mean-revert over a long enough time horizon." — Source: [Flirting with Models]

- On Momentum: "Cross-sectional momentum capitalizes on the persistent tendency of recent winners to keep winning and recent losers to keep losing." — Source: [Rational Reminder]

- On Carry: "Carry strategies exploit the reliable return generated by higher-yielding assets outperforming lower-yielding ones in stable environments." — Source: [The Meb Faber Show]

- On Defensiveness: "Defensive or high-quality assets historically deliver superior risk-adjusted returns by minimizing downside capture during volatile periods." — Source: [AQR Capital Management]

- On Structural Diversification: "Style premia offer structural diversification because their returns are driven by different behavioral and risk-based mechanisms than the broader equity market." — Source: [Bogle Center for Financial Literacy]

- On Factor Timing: "Factor timing is theoretically appealing but practically fraught with difficulty due to transaction costs and market friction." — Source: [AQR Insights]

- On Borrowed Capital: "Institutional investors can use borrowed capital prudently to harvest modest style premia without being forced into highly volatile, concentrated positions." — Source: [Rational Reminder]

- On Behavioral Biases: "Alternative premia provide a reliable source of returns because they exploit persistent human behavioral biases that are difficult to arbitrage away." — Source: [The Meb Faber Show]

Part 5: The Illiquidity Premium Debate

- On the Illiquidity Mirage: "The historical illiquidity premium in private equity is often negligible when properly compared to public market equivalents." — Source: [AQR Insights]

- On Return Smoothing: "Investors frequently overpay for private assets because they value the return-smoothing effect of infrequent mark-to-market pricing." — Source: [Rational Reminder]

- On Artificial Volatility: "Private markets exhibit lower reported volatility, but this is an artifact of delayed pricing rather than a true reduction in underlying economic risk." — Source: [Flirting with Models]

- On Performance Illusions: "Comparing artificially smoothed private returns to volatile public indices creates a dangerous illusion of superior risk-adjusted performance." — Source: [The Meb Faber Show]

- On Low Expected Returns: "Illiquid assets should not be treated as an automatic solution for the challenge of low expected returns in public markets." — Source: [AQR Capital Management]

- On Fee Drag: "High fees and increased institutional demand have steadily eroded whatever illiquidity premium may have existed in private markets decades ago." — Source: [Bogle Center for Financial Literacy]

- On Giving Up Liquidity: "Allocators must look past the sales pitch of private equity to recognize they are often giving up liquidity without adequate compensation." — Source: [AQR Insights]

- On Naïve Comparisons: "Naïve comparisons that fail to account for the implicit debt in private assets lead investors to vastly overestimate their alpha." — Source: [Rational Reminder]

- On Behavioral Crutches: "The smooth sailing experience of private assets functions as a behavioral crutch, masking the true beta exposure embedded in the portfolio." — Source: [The Meb Faber Show]

Part 6: Macroeconomic Sensitivities

- On Regime Sensitivities: "Different asset classes have distinct betas to specific macroeconomic regimes, such as inflation spikes or growth shocks." — Source: [AQR Capital Management]

- On Inflation Hedges: "Commodities serve as one of the few reliable diversifiers that offer a positive premium during periods of unexpected rising inflation." — Source: [Rational Reminder]

- On Offsetting Losses: "While stocks and bonds often struggle simultaneously in high-inflation environments, a diversified commodity basket tends to offset those losses." — Source: [The Meb Faber Show]

- On the Bond Premium: "Bonds provide a term premium as compensation for bearing interest rate risk, but they remain highly vulnerable to tightening monetary policy." — Source: [Bogle Center for Financial Literacy]

- On Commodity Volatility: "Investors should avoid single-commodity bets due to their extreme volatility, favoring a broad basket to capture the inflation-hedging premium." — Source: [AQR Insights]

- On Growth Sensitivities: "Stocks and bonds typically exhibit opposite sensitivities to economic growth, making them effective partners in a low-inflation environment." — Source: [Flirting with Models]

- On Balanced Exposures: "Commodities and bonds exhibit opposite sensitivities to inflation, necessitating both in a macroeconomically balanced portfolio." — Source: [Rational Reminder]

- On Regime Shifts: "A portfolio built solely for a disinflationary growth environment will suffer severe drawdowns when the macro regime unexpectedly shifts." — Source: [AQR Capital Management]

- On High-Quality Bonds: "Despite periods of low yields, high-quality bonds remain a foundational tool for mitigating severe equity market contractions." — Source: [The Meb Faber Show]

Part 7: Behavioral Pitfalls and Patience

- On Outcome Bias: "Outcome bias leads investors to equate the quality of a decision directly with its immediate short-term result." — Source: [AQR Insights]

- On Short-Term Noise: "Because luck dominates skill over short time horizons, sound decisions frequently yield poor outcomes in the near term." — Source: [Rational Reminder]

- On Strategy Execution: "The best investment strategy in the world is useless if the investor lacks the patience to stick with it through inevitable drawdowns." — Source: [The Meb Faber Show]

- On Assuming Discipline: "It is simple to backtest a strategy and assume discipline, but much harder to execute that discipline during live, painful market periods." — Source: [Flirting with Models]

- On Abandoning Strategies: "Investors frequently abandon structurally sound strategies right at the moment they are poised to revert to positive performance." — Source: [AQR Capital Management]

- On Bad Decades: "Good investments routinely go through bad decades, testing the resolve of professional institutional allocators." — Source: [Bogle Center for Financial Literacy]

- On Predictable Habits: "Return chasing and under-diversification are predictable habits that surface whenever a single asset class experiences an extended bull run." — Source: [Rational Reminder]

- On Overcoming Bias: "Overcoming outcome bias requires evaluating the rigorousness of the decision-making process before looking at the final results." — Source: [AQR Insights]

- On Frameworks: "A disciplined framework separates the emotional discomfort of short-term losses from the logical necessity of long-term factor exposure." — Source: [The Meb Faber Show]

Part 8: Ex-Ante vs. Ex-Post

- On Compensation vs. Reality: "Ex-ante expected return is the compensation you demand for taking a risk, while ex-post realized return is the noisy reality you actually get." — Source: [AQR Capital Management]

- On Exceeding Expectations: "When actual returns vastly exceed expected returns for a prolonged period, it usually indicates that future expectations must be drastically lowered." — Source: [Rational Reminder]

- On Valuation Changes: "Valuation changes can drive a wedge between long-term expectations and short-term outcomes, masking the underlying decay in structural yield." — Source: [The Meb Faber Show]

- On Planning Errors: "Investors error when they use ex-post historical data to confidently map out their ex-ante retirement planning." — Source: [Bogle Center for Financial Literacy]

- On Flawed Expectations: "A negative realized return over a five-year period does not prove that the initial ex-ante expectation was mathematically flawed." — Source: [Flirting with Models]

- On Anchoring to Yields: "The disconnect between expectations and outcomes requires a framework that anchors on current yields rather than historical averages." — Source: [AQR Insights]

- On Borrowing from the Future: "High realized returns often borrow from the future, inflating current portfolio values while suppressing the forward-looking expected yield." — Source: [Rational Reminder]

- On Staying Grounded: "Focusing heavily on ex-ante data prevents investors from being seduced by the temporary mirage of an overvalued market's ex-post performance." — Source: [AQR Capital Management]

- On Maintaining Conviction: "Understanding that ex-post returns are highly volatile helps investors maintain their conviction in a diversified ex-ante strategy during turbulent times." — Source: [The Meb Faber Show]