Lessons from Ashvin Chhabra

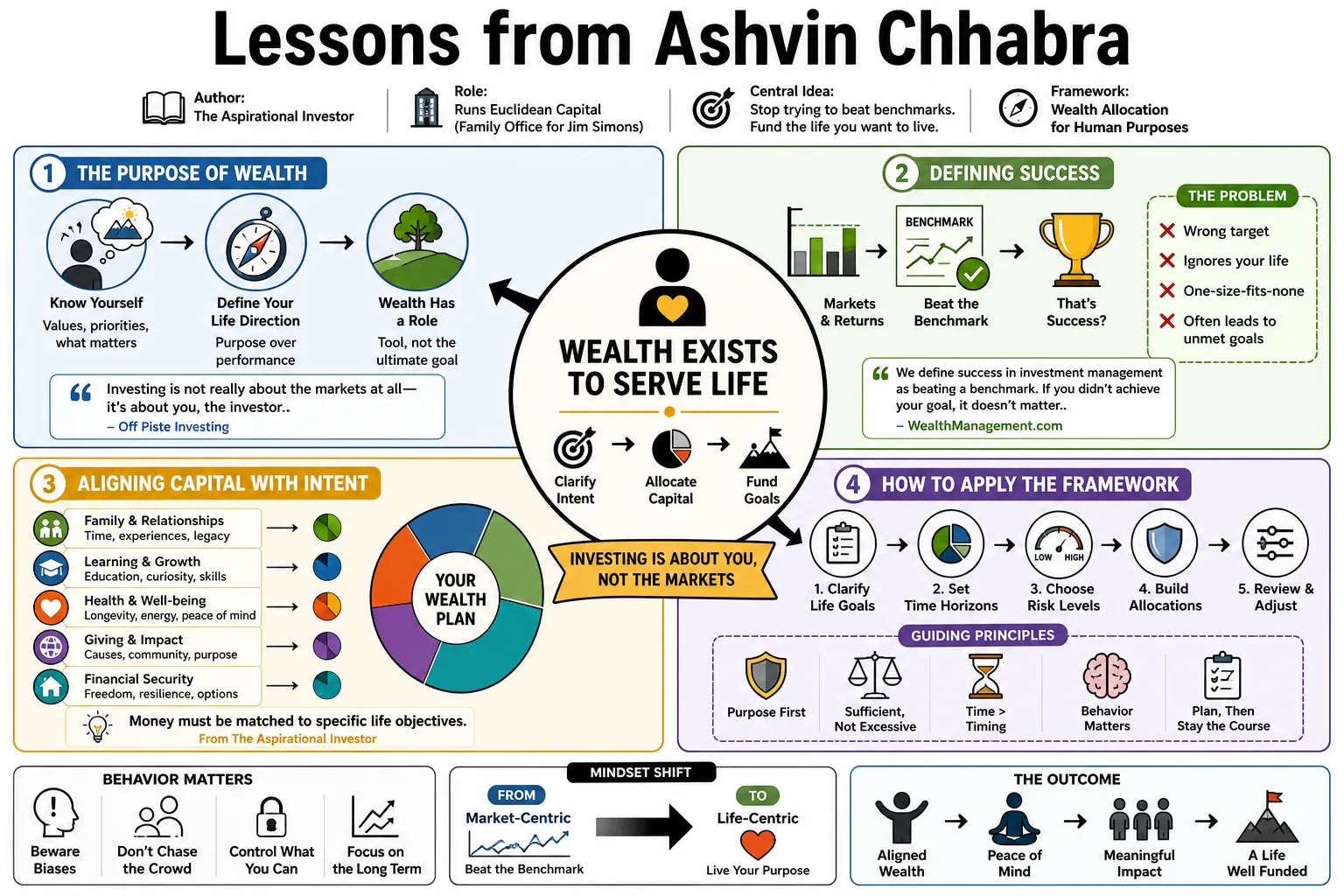

Ashvin Chhabra runs Euclidean Capital, the family office for Jim Simons, and wrote The Aspirational Investor. His Wealth Allocation Framework argues that investors should stop trying to beat market benchmarks and focus instead on funding specific life goals. This profile compiles his ideas on risk and behavioral finance, explaining how to structure wealth to serve human needs.

Part 1: The Purpose of Wealth

- On the Essence of Investing: "Investing is not really about the markets at all—it's about you, the investor. The person investing the money has to figure out what is the purpose of that money, the role that it plays in his or her life, and proceed from there." — Source: Off Piste Investing

- On Defining Success: "We think about markets, we think about returns, we talk about benchmarks, we talk about risk-adjusted returns, and we define success in investment management as beating a benchmark. If you didn't achieve your goal, it doesn't matter." — Source: WealthManagement.com

- On Aligning Capital with Intent: Money must be matched to specific life objectives, shifting the focus away from generic market performance toward personal utility. — Source: The Aspirational Investor

- On Wealth Creation versus Maintenance: People mistakenly use public market portfolios to try and get rich, when markets are primarily a tool for maintaining purchasing power over time. — Source: Capital Allocators, Episode 260

- On the Danger of Chasing Returns: Individuals give up significant wealth by constantly chasing hot trends and failing to establish a clear purpose for their capital. — Source: Barbara Stewart Interview

- On Life Goals as Benchmarks: True financial health is measured by whether an investor can fund their safety, maintain their living standard, and take calculated risks for their ambitions. — Source: The Aspirational Investor

- On Market Distractions: It is easy to get caught up in the noise of daily market movements and lose sight of the long-term reasons for investing in the first place. — Source: CFA Institute

- On the True Measure of Risk: Risk is not simply volatility; it is the probability of failing to meet the financial goals necessary to live the life you want. — Source: Collaborative Fund Conversations

- On Personalizing Portfolios: Every investor's allocation should be as unique as their own life trajectory and personal ambitions. — Source: The Aspirational Investor

Part 2: The Flaws of Traditional Finance

- On the Limits of Modern Portfolio Theory: "A lot of the investment advice roots from 1950s, from Harry Markowitz—diversification. But then the minute the first interesting company comes along, everybody jumps in and says, 'This is the next Google.' So people tend to be very interested in lottery tickets." — Source: WealthManagement.com

- On Standard Deviation as Risk: Defining risk purely as standard deviation ignores the severe human cost of extreme market drawdowns. — Source: Capital Allocators, Episode 260

- On the Flaws of the Mean-Variance Framework: The mean-variance model treats all capital identically, failing to account for how investors segment their money for different psychological and practical needs. — Source: The Aspirational Investor

- On Beating the Market: The obsession with beating a benchmark is a distraction created by the financial industry, which benefits from the resulting turnover and complexity. — Source: Off Piste Investing

- On One-Size-Fits-All Advice: The standard 60/40 portfolio is a blunt instrument that cannot address the specific safety constraints and aspirational needs of individual investors. — Source: CFA Institute

- On the Endowments Model: What works for a multi-billion dollar university endowment does not translate to an individual investor who has finite time horizons and emotional vulnerabilities. — Source: Capital Allocators, Episode 260

- On "Once in a Century" Events: "You start seeing someone stand up and say, 'oh, we've had a 1 in 100-year, 15 standard deviation collapse of markets, and how could we have anticipated this?' Then a part of you would say, this doesn't make sense from a pure scientist point of view, I know better." — Source: The Idea Farm

- On the Financial Industry's Priorities: The industry is designed to sell products and generate fees based on relative performance, not to secure a client's specific long-term outcomes. — Source: The Aspirational Investor

- On Acknowledging Failure: Traditional models fail because they expect rational actors; the reality of investing is driven by human emotion and unpredictable life events. — Source: WealthManagement.com

Part 3: The Wealth Allocation Framework

- On the Core Strategy: Investors should categorize their wealth into three distinct layers: Safety, Market Risk, and Aspirational Risk. — Source: Acme Reporter

- On Beyond Markowitz: The Wealth Allocation Framework moves beyond Markowitz by explicitly linking asset allocation to specific, categorized life goals. — Source: Capital Allocators, Episode 260

- On Compartmentalization: Mentally and practically separating assets into buckets helps investors maintain discipline when one segment of the portfolio underperforms. — Source: The Aspirational Investor

- On the Independence of Buckets: Each bucket serves a distinct purpose and must be evaluated on its own criteria, rather than blending them into a single aggregate portfolio return. — Source: CFA Institute

- On Aligning Risk with Purpose: The framework ensures that an investor never takes aspirational risks with capital needed for basic safety. — Source: Off Piste Investing

- On Managing Emotion: By knowing that basic needs are secured in a safety bucket, investors are less likely to panic and sell market assets during a downturn. — Source: The Aspirational Investor

- On the Evolution of Advice: The Wealth Allocation Framework represents a necessary shift from product-centric advice to goals-centric advice in wealth management. — Source: WealthManagement.com

- On Tailoring Allocations: The size of each bucket changes over an individual's lifetime depending on their career stage, liabilities, and evolving ambitions. — Source: Collaborative Fund Conversations

- On Simplifying Complexity: While the math behind asset pricing is complex, the framework simplifies decision-making by forcing a clear categorization of capital. — Source: Capital Allocators, Episode 260

Part 4: The Safety Bucket

- On the Purpose of Safety: The safety bucket exists to protect against financial shocks and ensure essential needs like food, shelter, and healthcare are always covered. — Source: Acme Reporter

- On Defining Protective Assets: This layer should consist of assets with minimal volatility and high liquidity, such as cash, primary residences, and secure bonds. — Source: The Aspirational Investor

- On Peace of Mind: The true return on the safety bucket is not yield, but the psychological comfort that allows the investor to sleep at night during market crashes. — Source: Off Piste Investing

- On Immunity to Shocks: This capital must be completely insulated from broader market drawdowns; if it correlates with the stock market, it is not true safety. — Source: Capital Allocators, Episode 260

- On Human Capital as Safety: For many young professionals, their most significant safety asset is their own earning power and career stability. — Source: The Aspirational Investor

- On the Cost of Safety: Investors must accept that true safety comes at the cost of giving up high returns; trying to stretch for yield here defeats the purpose. — Source: Forbes Iconoclast Summit

- On Downside Protection: A properly funded safety bucket is what prevents forced liquidations of growth assets at the bottom of a market cycle. — Source: CFA Institute

- On the Foundation of Wealth: You cannot responsibly pursue aspirational wealth without first securing the foundational safety layer. — Source: WealthManagement.com

- On Recognizing True Risk: The risk in this bucket is a loss of nominal value when liquidity is needed, which is why government-backed instruments are preferred here. — Source: The Aspirational Investor

Part 5: The Market Bucket

- On Maintaining Purchasing Power: The market bucket is intended to maintain an investor's standard of living over time by keeping pace with inflation. — Source: Goodreads

- On the Role of Diversification: This is the layer where traditional Modern Portfolio Theory applies perfectly—using broad diversification to capture global economic growth. — Source: The Aspirational Investor

- On Setting Expectations: Investors should expect to earn the market return here, no more and no less, and must be willing to endure standard market volatility. — Source: Capital Allocators, Episode 260

- On Avoiding Idiosyncratic Risk: The market bucket should avoid concentrated bets on single stocks or specific sectors that could permanently impair capital. — Source: Off Piste Investing

- On the Folly of Stock Picking: Attempting to achieve aspirational returns in the market bucket usually leads to underperformance and unnecessary stress. — Source: Collaborative Fund Conversations

- On Passive vs. Active: For the vast majority of individuals, low-cost index funds are the optimal vehicle for fulfilling the goals of the market bucket. — Source: The Aspirational Investor

- On Market Risk vs. Personal Risk: The risk here is systemic market decline, which is acceptable as long as the safety bucket is secure. — Source: CFA Institute

- On Long-Term Compounding: The power of the market bucket is realized over decades, requiring the discipline to do nothing during periods of panic. — Source: WealthManagement.com

- On Benchmark Relevance: This is the only bucket where comparing returns to a broad index like the S&P 500 actually makes logical sense. — Source: The Aspirational Investor

Part 6: The Aspirational Bucket

- On Wealth Creation: Aspirational assets are where significant wealth is actually created, usually through concentrated risk and entrepreneurship. — Source: Acme Reporter

- On Idiosyncratic Risk: This bucket is characterized by highly concentrated, idiosyncratic risk that carries the very real possibility of total loss. — Source: The Aspirational Investor

- On the Nature of Aspirational Assets: These investments include private businesses, concentrated stock positions, angel investments, or highly speculative assets. — Source: Capital Allocators, Episode 260

- On Asymmetric Returns: The goal in the aspirational bucket is to find opportunities with asymmetric upside that can fundamentally change an investor's socioeconomic status. — Source: Forbes Iconoclast Summit

- On the Lottery Ticket Mentality: People naturally crave the excitement of aspirational bets; the framework allows for this, but restricts it to a specific, safe proportion of wealth. — Source: WealthManagement.com

- On Accepting Failure: Investors must be emotionally and financially prepared for aspirational investments to go to zero without it impacting their standard of living. — Source: The Aspirational Investor

- On Founder Concentration: Most extremely wealthy individuals made their fortune by taking massive concentrated risk in a single enterprise, defying standard diversification advice. — Source: Collaborative Fund Conversations

- On Skill and Alpha: If genuine alpha exists, it resides in the aspirational bucket, requiring specialized skill, deep knowledge, or unique access. — Source: Off Piste Investing

- On Managing Windfalls: When an aspirational investment succeeds wildly, the prudent move is to harvest some gains and redistribute them into the safety and market buckets. — Source: The Aspirational Investor

- On the Meaning of Wealth: Ultimately, the aspirational bucket is about pursuing goals that give life deeper meaning beyond just paying the bills. — Source: CFA Institute

Part 7: Behavioral Biases and the Human Element

- On Integrating Kahneman and Tversky: The Wealth Allocation Framework is heavily influenced by behavioral finance, acknowledging that humans do not make rational financial decisions in a vacuum. — Source: Archive.org

- On the Investor's Worst Enemy: Individual investors routinely sabotage their own returns through poorly timed buying and selling driven by emotional extremes. — Source: Barbara Stewart Interview

- On Loss Aversion: People feel the pain of a loss much more acutely than the joy of a gain, which is why a dedicated safety bucket is psychologically necessary. — Source: The Aspirational Investor

- On Mental Accounting: While economists view mental accounting as a flaw, Chhabra uses it as a feature, using our tendency to compartmentalize to enforce financial discipline. — Source: Acme Reporter

- On the Illusion of Control: Investors often believe they can outsmart the market; the framework curtails this hubris by isolating speculation to the aspirational bucket. — Source: Capital Allocators, Episode 260

- On Reacting to Crises: Having a predetermined framework prevents investors from making impulsive, panic-driven decisions during severe market dislocations. — Source: WealthManagement.com

- On the Role of the Advisor: A financial advisor's primary job is not to pick stocks, but to act as a behavioral coach who keeps the client committed to their goals-based framework. — Source: Off Piste Investing

- On Regret Minimization: A well-structured portfolio minimizes the regret of both losing essential capital and missing out on transformative opportunities. — Source: The Aspirational Investor

- On Narrative Bias: Investors are too easily seduced by compelling stories of the "next big thing," leading them to misallocate capital intended for market maintenance. — Source: Collaborative Fund Conversations

- On Knowing Thyself: Successful investing requires a deep, honest assessment of one's own risk tolerance, anxieties, and true life priorities. — Source: CFA Institute

Part 8: Markets, Risk, and Complexity

- On Lessons from Physics: His background in physics taught him to look for underlying structures and to be skeptical of elegant mathematical models that fail in the real world. — Source: Capital Allocators, Episode 260

- On Fat Tails: Traditional models assume normal distributions, but financial markets exhibit "fat tails" where extreme, devastating events happen much more frequently than theory predicts. — Source: The Idea Farm

- On Evaluating Managers: When allocating capital, one must discern whether a manager's past success was due to replicable skill or simply taking hidden tail risks. — Source: Capital Allocators, Episode 260

- On Working with Jim Simons: At Euclidean Capital, the focus is on rigorous analysis and understanding complex systems, applying scientific principles to wealth preservation. — Source: Forbes Iconoclast Summit

- On the Limits of Prediction: It is impossible to consistently predict short-term market movements; portfolios must be durable enough to survive the unpredictable. — Source: The Aspirational Investor

- On Complexity as a Trap: The financial industry often uses complexity to justify high fees; true elegance in investing comes from clarity of purpose, not complicated instruments. — Source: Off Piste Investing

- On the Allocator's Dilemma: Capital allocators constantly face the tension between protecting capital in an uncertain world and finding yield in a competitive market. — Source: Forbes Iconoclast Summit

- On Interest Rates: Macroeconomic factors like interest rates fundamentally alter the pricing of risk, requiring adjustments in how aspirational and market assets are evaluated. — Source: Capital Allocators, Episode 260

- On Institutional vs. Individual Risk: Institutions can endure multi-year drawdowns because they exist in perpetuity; individuals have mortal constraints and cannot afford the same volatility. — Source: The Aspirational Investor

- On Navigating Uncertainty: The ultimate goal of an investment framework is not to eliminate uncertainty, which is impossible, but to build a structure that can withstand it. — Source: Collaborative Fund Conversations