Austan Goolsbee served as the Chairman of the Council of Economic Advisers under President Obama and currently leads the Federal Reserve Bank of Chicago. He is best known for his empirical research on how the internet changes consumer pricing and for advocating the "golden path" of reducing inflation without causing a recession. This profile catalogs his practical observations on taxation, central banking, and market behavior across three decades of economic shifts.

Part 1: The "Golden Path" and Monetary Policy

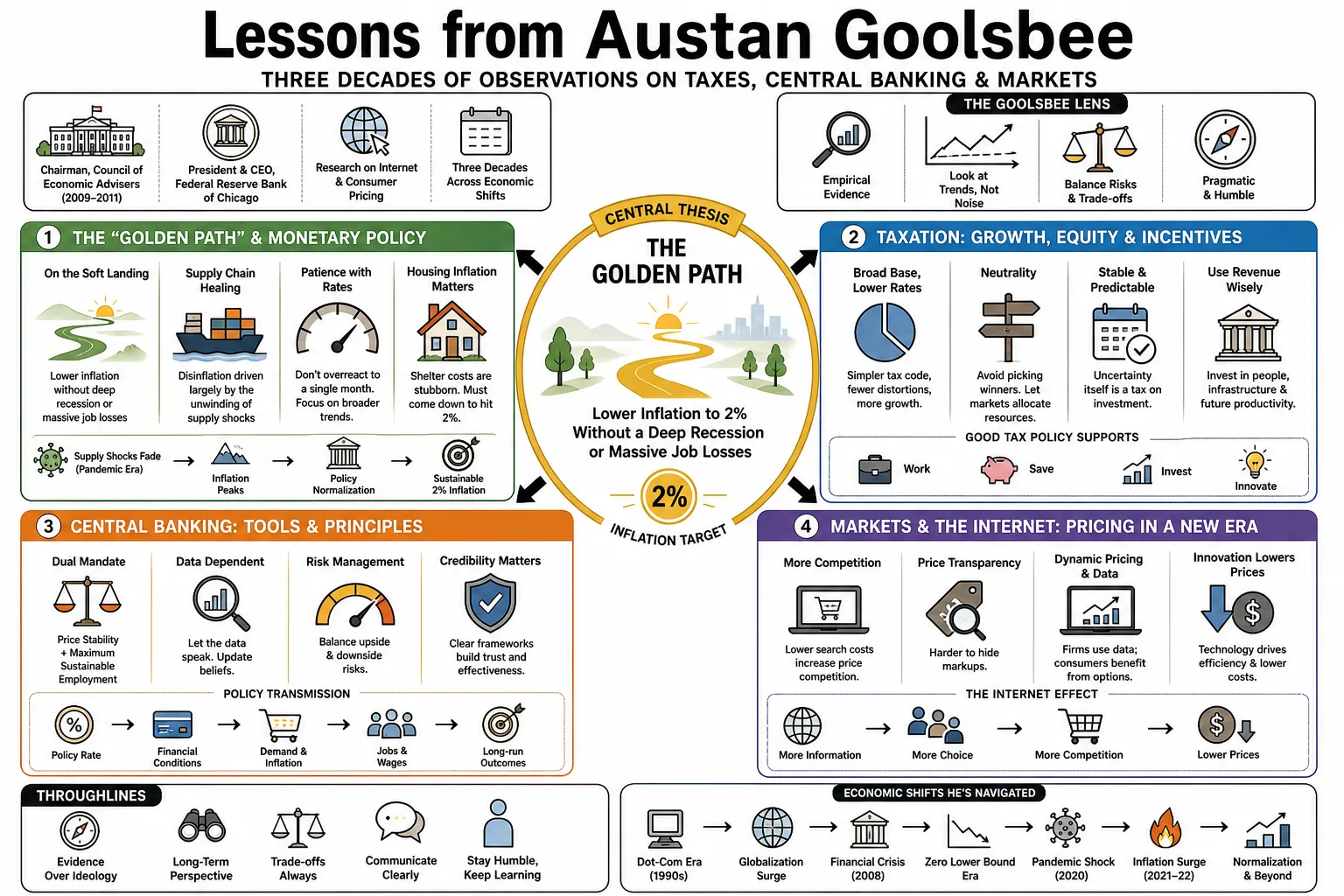

- On the soft landing: "The 'golden path' involves bringing inflation down to the 2% target without triggering a deep recession or massive job losses." — Source: [Chicago Fed]

- On supply chain healing: "A significant portion of recent disinflation has come from the unwinding of post-pandemic supply chain shocks rather than restrictive monetary policy alone." — Source: [Marketplace]

- On patience with interest rates: "When inflation data is volatile, it is a mistake to overreact to a single month's reading; policy must be guided by broader trends." — Source: [Financial Times]

- On housing inflation: "Shelter costs have been one of the most stubborn components of inflation, and seeing them come down is a requirement for reaching our long-term targets." — Source: [Bloomberg]

- On the labor market: "You can achieve significant disinflation without requiring a dramatic spike in unemployment, provided inflation expectations remain anchored." — Source: [WSJ]

- On data dependence: "The Federal Reserve's decisions must be tied to incoming economic data rather than adherence to a pre-set ideological path." — Source: [Conversations with Tyler]

- On the dangers of overtightening: "There is a risk that holding rates too high for too long could unnecessarily damage the real economy just as inflation is already cooling." — Source: [Face the Nation]

- On historical comparisons: "We should be cautious about assuming the current inflation fight must look exactly like the Paul Volcker era; the drivers of this inflation are fundamentally different." — Source: [NPR]

- On the dual mandate: "The Fed must balance its commitment to price stability with its mandate for maximum employment, especially when the golden path is within reach." — Source: [Chicago Fed]

- On long-term rates: "Even as inflation cools, it is not guaranteed that interest rates will return to the rock-bottom levels seen in the decade before the pandemic." — Source: [The Economics Show]

Part 2: The Digital Economy and Internet Markets

- On e-commerce competition: "The rise of internet comparison shopping fundamentally reduced consumer search costs, forcing incumbent firms to lower prices." — Source: [NBER]

- On local taxes and online sales: "Early in the internet's development, avoiding local sales tax was a major driver of online retail adoption for consumers." — Source: [Quarterly Journal of Economics]

- On digital market entry: "Incumbent firms often adjust their pricing strategies aggressively the moment they face a credible threat of online entry, even before the competitor gains significant market share." — Source: [Journal of Political Economy]

- On measuring digital value: "Traditional GDP metrics struggle to capture the massive consumer surplus generated by free digital goods and services." — Source: [University of Chicago Booth]

- On broadband adoption: "The spread of high-speed internet changed how people consume media, how they shop, and how they evaluate prices in local markets." — Source: [NBER]

- On platform economics: "Network effects in digital platforms can lead to winner-take-all markets, making competition policy highly complex." — Source: [Economic Strategy Group]

- On the friction of physical retail: "The internet revealed how much localized pricing power brick-and-mortar retailers held due to the physical difficulty of comparison shopping." — Source: [American Economic Review]

- On tech and inflation: "Digital goods and software often experience deflationary trends, counteracting price increases in physical services over time." — Source: [Conversations with Tyler]

- On the limits of online sales: "Despite rapid growth, certain experiential goods still rely heavily on physical presence, showing the limits of the internet's disruption." — Source: [NBER]

- On data as an asset: "In the digital economy, a firm's ability to aggregate and analyze consumer data often becomes its primary competitive moat." — Source: [University of Chicago Booth]

Part 3: The Pandemic Economy

- On fear versus lockdowns: "During the early pandemic, voluntary social distancing driven by fear of the virus caused far more economic contraction than formal government lockdowns." — Source: [Journal of Public Economics]

- On the recovery shape: "The pandemic recovery was uniquely rapid because it was a public health shock rather than a traditional financial crisis, allowing demand to rebound quickly once restrictions eased." — Source: [NPR]

- On remote work: "The shift to remote work acted as a massive, unplanned structural change, permanently altering commercial real estate and local tax bases." — Source: [Chicago Fed]

- On goods vs. services: "The pandemic caused an unprecedented shift in consumer spending away from services and toward physical goods, instantly overwhelming global supply chains." — Source: [Marketplace]

- On stimulus checks: "Direct fiscal transfers were highly effective at preventing a collapse in consumer spending, though they ultimately contributed to demand-side inflation." — Source: [Face the Nation]

- On labor force participation: "The pandemic accelerated retirements and shifted childcare burdens, creating labor shortages that took years to resolve." — Source: [The Economics Show]

- On the bullwhip effect: "Supply chains experienced extreme whiplash during the pandemic, moving from massive shortages to sudden inventory gluts as consumer habits normalized." — Source: [Bloomberg]

- On behavioral economics: "The pandemic highlighted how heavily economic activity relies on consumer psychology and the subjective feeling of physical safety." — Source: [University of Chicago Booth]

- On policy agility: "The crisis required policymakers to deploy new tools in real-time, demonstrating that traditional monetary policy alone is insufficient for biological shocks." — Source: [NBER]

Part 4: Productivity and Innovation

- On construction stagnation: "Productivity in the U.S. construction sector has remained shockingly stagnant for decades, a trend that cannot be entirely explained by measurement errors." — Source: [NBER]

- On R&D subsidies: "Government R&D subsidies often inadvertently drive up the wages of existing scientists and engineers rather than proportionately increasing the actual volume of innovation." — Source: [American Economic Review]

- On artificial intelligence: "If AI delivers on its promise to boost worker productivity, it could act as a structural disinflationary force, allowing the economy to grow faster without triggering price hikes." — Source: [Financial Times]

- On manufacturing: "The decline of manufacturing employment is largely a story of productivity and automation, rather than merely offshoring and trade." — Source: [Council of Economic Advisers Archives]

- On human capital: "Long-term economic growth is fundamentally constrained by the quality of a nation's education system and its ability to produce skilled labor." — Source: [University of Chicago Booth]

- On the restaurant industry: "Some sectors, like restaurants, have shown surprising productivity gains through technological adoption and optimized scheduling, contradicting the idea of stagnant service sectors." — Source: [NBER]

- On technology diffusion: "The economic benefit of a new technology is fully realized when it is widely adopted by small and medium-sized businesses, rather than merely when it is invented." — Source: [Conversations with Tyler]

- On investment cycles: "Firms often delay major capital investments during periods of high uncertainty, dragging down national productivity figures." — Source: [Chicago Fed]

- On the gig economy: "Gig platforms have improved matching efficiency between labor and demand, but they complicate traditional metrics of employment and wage growth." — Source: [Economic Strategy Group]

Part 5: Taxation and Public Policy

- On corporate taxes: "Cutting corporate tax rates does not automatically lead to massive wage increases for workers; much of the benefit often flows to shareholders." — Source: [University of Chicago Booth]

- On tax complexity: "The complexity of the tax code acts as a regressive tax in itself, disproportionately burdening small businesses while rewarding large corporations with lobbying power." — Source: [NBER]

- On inequality: "Rising income inequality is driven heavily by the premium on higher education and the outsized returns to specialized skills in a globalized economy." — Source: [Council of Economic Advisers Archives]

- On the estate tax: "Arguments against the estate tax often rely on the myth of the small family farm being sold to pay taxes, a scenario that is statistically exceedingly rare." — Source: [NYT]

- On marginal rates: "Historically, very high marginal income tax rates have led to increased tax avoidance behavior rather than proportionately higher government revenue." — Source: [Journal of Political Economy]

- On carbon pricing: "From an economic standpoint, pricing carbon is the most efficient mechanism to combat climate change, though it remains politically perilous." — Source: [University of Chicago Booth]

- On infrastructure: "Public investment in infrastructure has a high multiplier effect on the economy, provided the projects are selected based on economic merit rather than political patronage." — Source: [Council of Economic Advisers Archives]

- On tax holidays: "Temporary tax holidays generally fail to stimulate long-term economic growth, as consumers and businesses merely shift the timing of their spending." — Source: [NBER]

- On the safety net: "A well-designed social safety net protects the vulnerable and encourages economic dynamism by allowing workers to take entrepreneurial risks." — Source: [American Economic Review]

Part 6: The Great Recession and the Obama Administration

- On the auto bailout: "The decision to rescue the auto industry was heavily criticized at the time, but it ultimately saved millions of jobs up and down the supply chain and prevented the collapse of the Midwest economy." — Source: [Council of Economic Advisers Archives]

- On the speed of the crash: "The financial crisis moved with a velocity that standard macroeconomic models completely failed to predict, requiring immediate and unprecedented interventions." — Source: [NPR]

- On the stimulus size: "In retrospect, the initial 2009 stimulus package likely should have been larger to fill the massive output gap created by the housing collapse." — Source: [Marketplace]

- On housing markets: "The recession proved that when a bubble fueled by massive household debt bursts, the resulting economic contraction is exceptionally deep and difficult to reverse." — Source: [NBER]

- On political constraints: "As an economic adviser, you frequently find that the theoretically optimal policy is impossible to execute due to legislative realities." — Source: [University of Chicago Booth]

- On financial regulation: "The Dodd-Frank Act was necessary to increase capital requirements and prevent banks from taking systemic risks with implicit government backing." — Source: [Council of Economic Advisers Archives]

- On unemployment persistence: "Following a financial crisis, long-term unemployment can cause skills to atrophy, leading to structural damage in the labor market." — Source: [American Economic Review]

- On global coordination: "The recovery from the 2008 crisis required central banks around the world to coordinate policy to prevent a global depression." — Source: [WSJ]

- On public perception: "Even when economic metrics begin to improve, public sentiment often lags behind for years because the trauma of a recession is sticky." — Source: [Face the Nation]

Part 7: Economic Data and Measurement

- On traditional metrics: "Standard economic indicators are frequently revised months after they are published, making them a flawed tool for managing real-time monetary policy." — Source: [Conversations with Tyler]

- On alternative data: "During rapidly changing environments like a pandemic, high-frequency data such as restaurant reservations and credit card swipes become more valuable than lagging official reports." — Source: [Chicago Fed]

- On inflation indexes: "The difference between CPI and PCE inflation matters significantly for policy, as they weigh housing and healthcare differently." — Source: [Bloomberg]

- On the limitations of models: "Macroeconomic models are excellent for understanding historical trends but often fail spectacularly at predicting turning points in the business cycle." — Source: [University of Chicago Booth]

- On survey data: "Consumer sentiment surveys often reflect political partisanship and gas prices more heavily than underlying macroeconomic health." — Source: [The Economics Show]

- On measuring GDP: "GDP is a measure of output, not welfare; it completely misses the value of leisure time and the environmental costs of production." — Source: [NBER]

- On the Sahm Rule: "Heuristics like the Sahm Rule are highly useful for identifying recessions in real-time, relying on the momentum of unemployment rather than GDP." — Source: [Marketplace]

- On core vs. headline inflation: "Central bankers focus on core inflation because food and energy prices are highly volatile and largely outside the control of domestic monetary policy." — Source: [Chicago Fed]

- On wage growth: "To understand the labor market, you have to look past average hourly earnings and examine wage growth across different quartiles of the income distribution." — Source: [WSJ]

- On big data in economics: "The integration of massive private-sector datasets into economic research is fundamentally changing how we understand consumer behavior." — Source: [American Economic Review]

Part 8: Central Banking and Communication

- On forward guidance: "When a central bank communicates its future intentions clearly, it can influence financial conditions immediately, long before it actually changes interest rates." — Source: [Chicago Fed]

- On Fed independence: "The credibility of the Federal Reserve rests entirely on its political independence and its commitment to following the data." — Source: [Financial Times]

- On speaking plainly: "Economics is too often obscured by jargon; a central banker's job is to explain complex policy decisions in terms that the public can actually understand." — Source: [Marketplace]

- On groupthink: "Regional Fed banks are essential because they bring diverse geographic and industrial perspectives to a policy table that might otherwise suffer from East Coast groupthink." — Source: [Conversations with Tyler]

- On dot plots: "The Fed's Summary of Economic Projections can sometimes confuse markets because they are individual forecasts, not a collective promise of future policy." — Source: [Bloomberg]

- On the yield curve: "An inverted yield curve has historically been a reliable recession indicator, but in modern environments with massive central bank balance sheets, its predictive power may be distorted." — Source: [NPR]

- On humility in forecasting: "Anyone making macroeconomic forecasts must maintain a deep sense of humility, as the economy constantly invents new ways to surprise you." — Source: [University of Chicago Booth]

- On market reactions: "The Fed must set policy for Main Street, not Wall Street; reacting to daily stock market volatility is a recipe for policy errors." — Source: [Face the Nation]

- On the role of a Fed President: "My job is to gather the best data from the businesses and workers in the Seventh District and ensure their reality is reflected in national monetary policy." — Source: [Chicago Fed]