Lessons from Beezer Clarkson

Beezer Clarkson is a longtime Limited Partner at Sapphire Partners best known for clarifying the traditionally opaque relationship between GPs and LPs through the OpenLP initiative. This profile gathers her straightforward advice on fundraising, managing funds, and building a lasting venture firm.

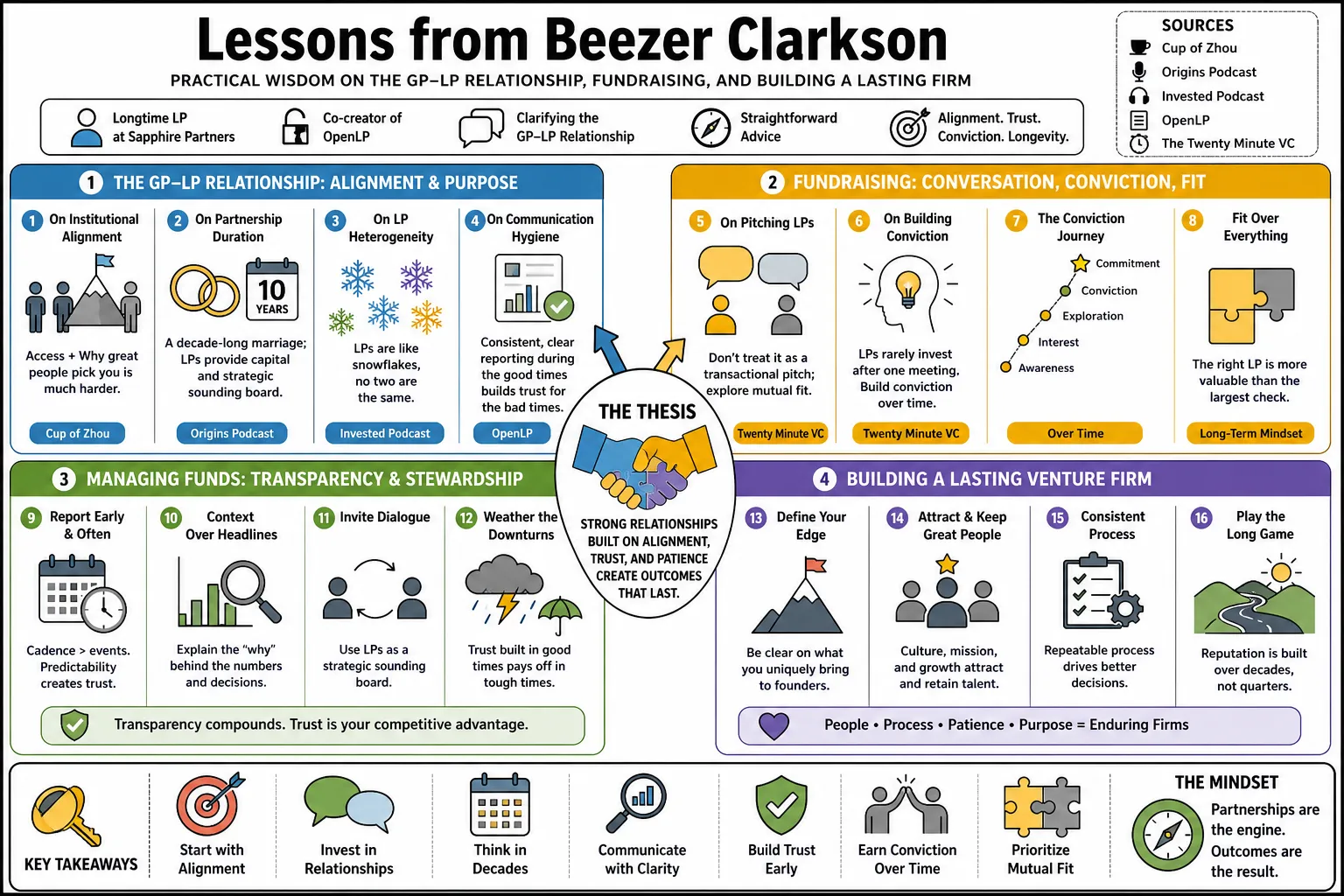

Part 1: The GP-LP Relationship

- On institutional alignment: "It's the access and why do the great people pick you that is much harder. And that speaks to what it is that you, the investor, are bringing to the table." — Source: Cup of Zhou

- On partnership duration: "A fund relationship is a decade-long marriage; LPs provide capital but also serve as a long-term strategic sounding board." — Source: Origins Podcast

- On LP heterogeneity: "LPs are like snowflakes, no two are the same." — Source: Invested Podcast

- On communication hygiene: "Consistent, clear reporting during the good times builds the trust required to weather the bad times." — Source: OpenLP

- On pitching LPs: "Don't treat a meeting with an LP as a transactional pitch; treat it as an exploratory conversation about mutual fit." — Source: The Twenty Minute VC

- On building conviction: "LPs rarely invest after a single meeting; they need to see how a manager thinks and operates over multiple touchpoints." — Source: Capital Allocators

- On GP transparency: "Transparency is the currency of trust between GPs and LPs. If you hide the bad news, the relationship fractures." — Source: OpenLP

- On pre-filtering: "Emerging managers save massive amounts of time by researching an LP's mandate and checking if they actually write the size of check you need before reaching out." — Source: Sapphire Ventures Substack

- On early engagement: "It pays to meet LPs long before you are actively raising. Give them time to track your progression and observe your decision-making." — Source: Medium Profile

Part 2: The Realities of Fundraising

- On the primary challenge: "Raising a venture fund is a sales process where the product is your judgment and your network." — Source: The Twenty Minute VC

- On market conditions: "A challenging fundraising environment doesn't break the industry; it simply raises the bar for conviction and differentiation." — Source: Invested Podcast

- On pacing: "Deploying capital too quickly limits a GP's ability to learn from their initial investments and adjust to market feedback before raising the next fund." — Source: Sapphire Ventures Substack

- On the first close: "Securing a lead LP for a first close is the hardest part of fundraising, as it signals validation to the rest of the market." — Source: Origins Podcast

- On institutional hurdles: "Breaking into the institutional LP pool often requires surviving long enough to show real returns, usually around Fund III." — Source: Medium Profile

- On re-ups: "The easiest capital to raise is from existing LPs, provided the GP has maintained strong relationships and performed well." — Source: Capital Allocators

- On narrative consistency: "LPs compare the narrative you pitch in Fund I against the actual portfolio you built when you return for Fund II." — Source: OpenLP

- On managing rejection: "Rejection from an LP isn't always about the GP's quality; it often comes down to portfolio construction constraints on the LP's side." — Source: Invested Podcast

- On closing the gap: "The difference between a target fund size and a hard cap must be justified by deal flow, rather than just GP ambition." — Source: StrictlyVC

Part 3: Understanding the LP Perspective

- On LP constraints: "Every LP has a specific mandate, risk profile, and liquidity requirement that dictates their behavior." — Source: Invested Podcast

- On asset allocation: "Venture capital is a small, highly illiquid sleeve of a broader institutional portfolio, which means GPs are competing for a scarce resource." — Source: Capital Allocators

- On risk assessment: "LPs are fundamentally in the business of managing risk; they look for GPs who understand their own blind spots." — Source: Origins Podcast

- On venture returns: "To justify the illiquidity of venture, LPs need a premium over public market returns, driving the demand for top-quartile performance." — Source: Medium Profile

- On reference checks: "LPs do heavy back-channel referencing. How founders talk about a GP when things go wrong is the ultimate test." — Source: The Twenty Minute VC

- On evaluating process: "LPs invest in the process as much as the track record. A repeatable sourcing and evaluation engine is more valuable than one lucky hit." — Source: OpenLP

- On capital calls: "GPs must be mindful of how and when they call capital; unpredictable capital calls can create cash flow issues for LPs." — Source: StrictlyVC

- On co-investments: "Many LPs view co-investment opportunities as a way to lower their blended fee rate and gain direct exposure to breakout companies." — Source: Sapphire Ventures Substack

- On reporting standards: "LPs appreciate standardization. GPs should focus on providing clear data rather than overly stylized quarterly updates." — Source: OpenLP

- On manager selection: "Selecting the right manager is an art form that combines quantitative analysis of past performance with qualitative assessment of team dynamics." — Source: Origins Podcast

Part 4: Evaluating Emerging Managers

- On the emerging manager premium: "New funds often outperform established ones because the GPs are hungry and highly aligned with their first LPs." — Source: Medium Profile

- On graduation rates: "The path from Fund I to Fund IV is steep. A very small percentage of emerging managers successfully navigate multiple fundraising cycles to become established firms." — Source: Sapphire Ventures Substack

- On differentiation: "A new fund needs a distinct edge, such as sector expertise or a unique sourcing model, to stand out." — Source: Origins Podcast

- On the first portfolio: "Fund I is the proof of concept. The GP has to prove they can win deals against established incumbents." — Source: The Twenty Minute VC

- On GP commitment: "LPs want to see emerging managers have significant skin in the game, tying their personal financial success directly to the fund's performance." — Source: Capital Allocators

- On building infrastructure: "Running a fund requires operational competence; emerging managers often underestimate the back-office requirements." — Source: OpenLP

- On track record attribution: "LPs heavily scrutinize an emerging manager's past deals to ensure they actually sourced, led, and managed the investments they claim." — Source: Invested Podcast

- On strategy drift: "Emerging managers must resist the temptation to drift from their stated strategy when faced with FOMO-inducing deals outside their mandate." — Source: StrictlyVC

- On sizing the fund: "A fund's size is its strategy. Raising too much capital in an early fund can fundamentally break a seed-stage return model." — Source: Sapphire Ventures Substack

Part 5: Portfolio Construction and Concentration Risk

- On concentration: "If you're overly concentrated, you better be damn good at your job 'cause you just raised the bar too high." — Source: Cup of Zhou

- On fund math: "A venture portfolio must be constructed so that a single breakout success can return the entire fund multiple times over." — Source: Medium Profile

- On diversification: "Diversification in venture doesn't mean safety; it means enough shots on goal to capture the power law." — Source: Origins Podcast

- On follow-on reserves: "Allocating the right amount of follow-on capital is a delicate balancing act between defending ownership and throwing good money after bad." — Source: Capital Allocators

- On position sizing: "Initial check sizes must be meaningful enough to achieve target ownership without burning through the fund prematurely." — Source: The Twenty Minute VC

- On discipline: "The best GPs have strict portfolio construction models and stick to them, regardless of market exuberance." — Source: OpenLP

- On recycling: "Reinvesting management fees and early returns is a highly effective way to maximize working capital and improve fund multiples." — Source: StrictlyVC

- On the power law: "Venture capital is inherently a game of outliers. Portfolios must be designed to accommodate extreme variance in outcomes." — Source: Invested Podcast

- On managing winners: "GPs must have a clear framework for when to hold their best positions and when to seek early liquidity to lock in returns." — Source: Sapphire Ventures Substack

Part 6: Team Dynamics and Firm Survival

- On partnership fracture: "Internal team dynamics and partnership splits are the most common reasons venture firms fail to raise their next fund." — Source: Sapphire Ventures Substack

- On shared vision: "A partnership only survives if the GPs are completely aligned on how decisions are made and how economics are shared." — Source: Origins Podcast

- On firm evolution: "As a firm grows from Fund I to Fund III, the skill set required shifts from pure investing to firm management and scaling." — Source: Capital Allocators

- On succession planning: "Generational transition is the hardest test for a venture firm. The transition of carry and leadership must be handled years in advance." — Source: OpenLP

- On hiring talent: "Adding partners is inherently risky. Firms must rigorously evaluate how new additions alter the existing decision-making chemistry." — Source: The Twenty Minute VC

- On ego management: "A successful firm requires partners who can vigorously debate an investment thesis without letting ego destroy the relationship." — Source: Invested Podcast

- On attribution: "It is essential for a firm to track who sourced a deal, who helped the founder, and who recognized when to sell." — Source: Medium Profile

- On institutionalizing: "A lasting firm institutionalizes its network and brand, ensuring it does not rely entirely on the reputation of one star partner." — Source: StrictlyVC

- On decision-making: "The best partnerships have mechanisms to prevent groupthink and ensure high-conviction contrarian bets can be made." — Source: Origins Podcast

- On dead VCs: "The venture industry has many 'dead' firms that technically exist to manage out legacy portfolios but will never raise another fund." — Source: Sapphire Ventures Substack

Part 7: Market Cycles and Adaptability

- On market corrections: "Downturns serve as a forcing function, clearing out excess capital and testing which GPs have genuine discipline." — Source: Invested Podcast

- On vintage years: "A fund's vintage year heavily dictates its macro environment, but strong GPs can generate returns across any market cycle." — Source: Capital Allocators

- On valuation discipline: "Paying top-of-market prices in a frothy environment fundamentally impairs a fund's ability to generate target multiples." — Source: Sapphire Ventures Substack

- On adapting to change: "The venture model must continuously evolve as capital flows shift. Managers who refuse to adapt their sourcing strategies will be left behind." — Source: The Twenty Minute VC

- On the illusion of speed: "Fast deployment cycles in bull markets often mask a lack of deep diligence and lead to overlapping, poorly constructed portfolios." — Source: Medium Profile

- On market resilience: "Long-term venture success requires the psychological resilience to make investments when the broader market is fearful." — Source: Origins Podcast

- On Series A shifts: "The definition and expectations of a Series A round constantly fluctuate; GPs must stay attuned to what downstream investors actually require for a markup." — Source: Medium Profile

- On secondary markets: "The maturation of the secondary market provides essential liquidity relief valves for both GPs and LPs during extended hold periods." — Source: OpenLP

- On capital concentration: "The increasing concentration of capital into mega-funds creates unique opportunities for nimble, early-stage specialists to exploit overlooked gaps." — Source: StrictlyVC

- On surviving winters: "The firms that survive a venture winter do so through aggressive portfolio triage and highly transparent LP communication." — Source: Sapphire Ventures Substack

Part 8: Transparency and the OpenLP Initiative

- On the motivation for OpenLP: "The venture ecosystem suffered from a massive information asymmetry between LPs and GPs, making the fundraising process needlessly opaque." — Source: OpenLP

- On sharing the playbook: "Demystifying the LP mindset helps emerging managers build better firms and ultimately creates a healthier asset class." — Source: Origins Podcast

- On community building: "Venture capital thrives on shared knowledge; an open community benefits both allocators and fund managers." — Source: Capital Allocators

- On breaking down barriers: "Transparency in how LPs make decisions lowers the barrier to entry for diverse fund managers who lack established insider networks." — Source: Invested Podcast

- On educational resources: "Open sourcing term sheets, reporting templates, and best practices elevates the operational standard of the entire industry." — Source: OpenLP

- On managing expectations: "Clear public communication about LP constraints helps GPs understand why a 'no' is often a structural issue, rather than a personal rejection." — Source: The Twenty Minute VC

- On industry maturity: "The move toward radical transparency is a sign of venture capital maturing from a cottage industry into a standardized institutional asset class." — Source: Medium Profile

- On continuous learning: "What would you do if you knew you couldn't fail? Approaching venture with curiosity rather than fear drives better long-term decision making." — Source: Forty Over 40

- On the end goal: "The ultimate purpose of increased LP transparency is to ensure capital flows efficiently to the managers best equipped to back transformative founders." — Source: Sapphire Ventures Substack