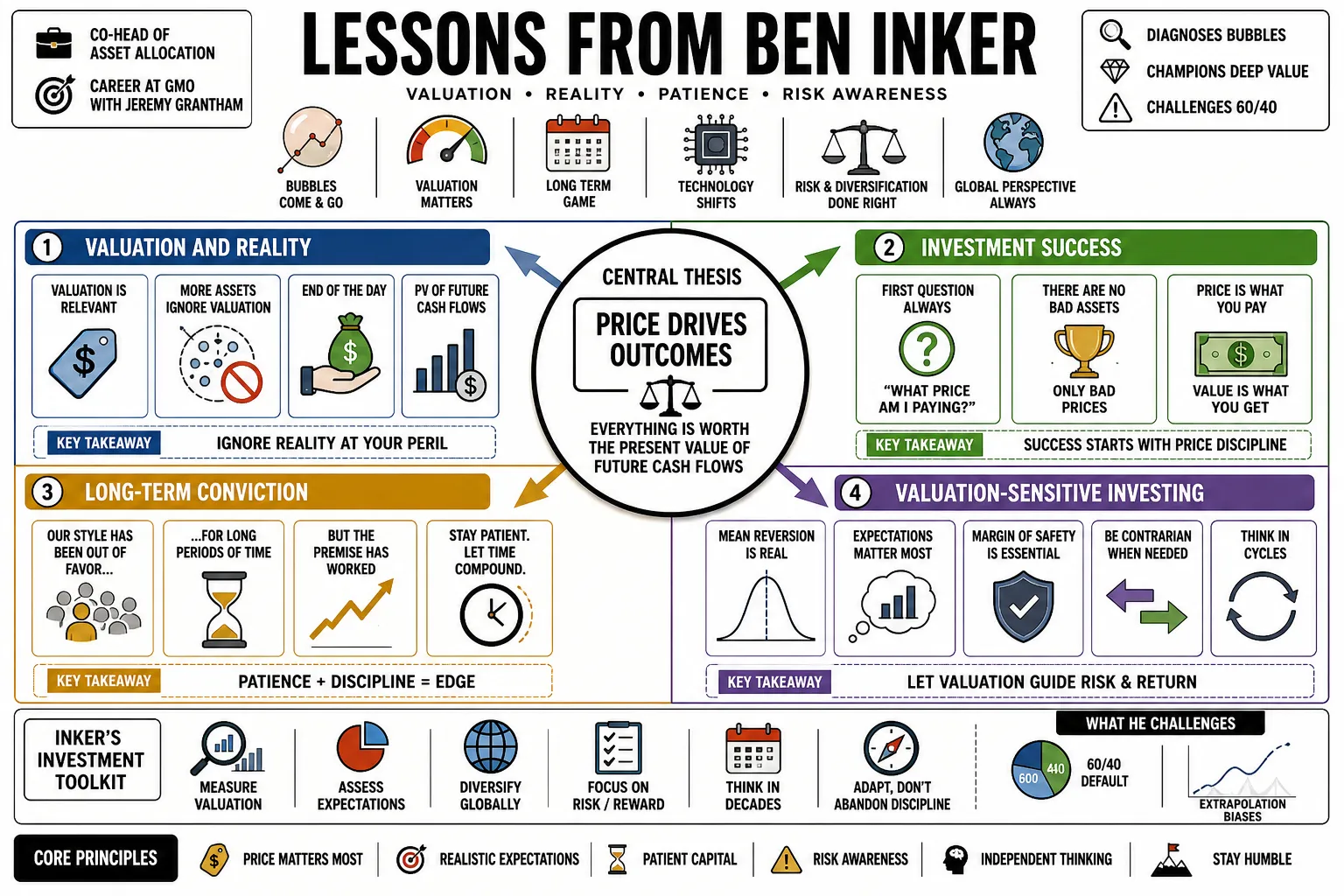

Ben Inker is the Co-Head of Asset Allocation at GMO, where he has spent his career refining valuation-based investment strategies alongside Jeremy Grantham. He is best known for diagnosing market bubbles, championing "deep value," and warning investors against the structural flaws of the traditional 60/40 portfolio. This profile distills his approach to navigating expensive markets, technological shifts, and the long-term realities of asset pricing.

Part 1: Valuation-Sensitive Investing

- On Valuation and Reality: "Valuation is relevant and it is astonishing that we live in a world where there are more assets where valuation is not a relevant thing anymore. But for the vast majority of financial assets out there... at the end of the day, everything is worth the present value of the future cash flows." — Source: Ritholtz Masters in Business

- On Investment Success: No investor can intelligently assess any situation before answering the question: "What price am I paying?" — Source: Dokumen Pub

- On the Importance of Price: There are no bad assets in the financial markets, there are simply bad prices that investors pay for them. — Source: GMO Research Library

- On Long-Term Conviction: "Our strong preference is to focus on long-term value, despite the inevitable periods of tough performance that strategy will entail... in the long run no factor is as important to investment returns as valuations." — Source: Advisor Analyst

- On Reflexive vs. Sensitive Investing: Being a valuation-sensitive investor is entirely different from being a reflexive value investor; you must determine if the "cheap" half of the market is actually priced attractively enough to buy. — Source: GMO Research Library

- On Forecasting Returns: We build our seven-year asset class forecasts based on the assumption that extreme valuation dislocations will eventually revert to their historical mean. — Source: GMO Research Library

- On Market Inefficiencies: The concentration you see in the US equity market today is generating an inefficient allocation of both human and financial capital. — Source: Schroders

- On Risk Management: The best defense against permanent capital impairment is refusing to pay peak multiples for cyclical peak earnings. — Source: Barron's Live Podcast

- On Patience: Valuation-based investing requires accepting that you will look foolish before you look smart, as the market can ignore fundamentals for longer than most expect. — Source: FEG Insight Bridge

- On Historical Precedent: The single most reliable indicator of poor future returns is an elevated starting valuation across major asset classes. — Source: GMO Research Library

Part 2: The Evolution of Value and Deep Value

- On the Cycles of Value: "If history is to be our guide…we shouldn't expect any outperformance by value over the next few years, and it may very well underperform." — Source: GMO Quarterly Letter

- On Deep Value: While the broader value factor may struggle in certain regimes, "deep value"—the cheapest 20% of stocks—often presents significant and distinct valuation dislocations. — Source: MOI Global

- On Value Traps: A low price-to-book ratio is not an excuse to buy a structurally declining business; distinguishing deep value from a value trap requires assessing the durability of the underlying cash flows. — Source: GMO Research Library

- On Intangible Assets: Traditional value metrics like price-to-book often fail to capture the true worth of modern companies, requiring adjustments for intellectual property, networks, and specialized expertise. — Source: Ritholtz Masters in Business

- On Quality Stocks: "While a glancing punch can knock a junk company to the mat, quality companies absorb body blows like Rocky Balboa and come back for more." — Source: Meb Faber Show

- On Value During Recessions: Deep value stocks routinely present the most compelling long-term opportunities even, and sometimes especially, during economic recessions. — Source: Smead Capital

- On the Spread: When the valuation spread between value and growth stocks stretches to extremes, the subsequent reversion is often swift and brutal for those holding expensive growth. — Source: Business Insider

- On Margin of Superiority: Investors must look for a clear margin of superiority in value stocks rather than settling for mediocre companies that happen to trade at a discount. — Source: GMO Research Library

- On Modern Value Investing: Value investing is not dead; it has simply evolved beyond accounting ratios to demand a deeper understanding of normalized earnings power. — Source: FEG Insight Bridge

- On Growth vs. Value: The market consistently overpays for the comfort of current growth and underpays for the discomfort of current distress. — Source: GMO Research Library

Part 3: Challenging the 60/40 Portfolio

- On the Default Portfolio: The traditional 60/40 stock-bond portfolio is composed of expensive U.S. growth equities and low-yielding credit, leaving it structurally vulnerable to a "lost decade" of real returns. — Source: Business Insider

- On Changing Regimes: In an environment of elevated equity valuations and compressed yields, the 60/40 mix is no longer an effective strategy for risk management. — Source: Fund Selector Asia

- On Real Returns: Investors relying on a static 60/40 allocation are mathematically unlikely to meet their long-term real return requirements over the next seven years. — Source: Advisor Perspectives

- On Fixed Income Constraints: When bond yields fall to historic lows, fixed income loses its ability to serve as a reliable shock absorber during equity market drawdowns. — Source: Morningstar

- On Alternative Approaches: Investors need a more valuation-sensitive, dynamic, and globally diversified approach than the static 60/40 benchmark can provide. — Source: Business Insider

- On Institutional Inertia: The persistence of the 60/40 allocation is driven more by institutional comfort and peer risk than by sound forward-looking math. — Source: GMO Research Library

- On Equity Risk Premiums: Buying the S&P 500 at peak multiples severely compresses the equity risk premium, eroding the foundational premise of a heavy equity allocation. — Source: GMO Research Library

- On Diversification Failures: True diversification requires uncorrelated asset classes, not just a mix of expensive stocks and expensive bonds that will suffer simultaneously if inflation persists. — Source: Advisor Perspectives

- On Moving Beyond Benchmarks: Beating a flawed benchmark like the 60/40 should not be the goal; preserving purchasing power and generating absolute real returns is the actual mandate. — Source: GMO Research Library

Part 4: Dynamic Asset Allocation

- On Active Shifts: Dynamic asset allocation means having the willingness to abandon expensive segments of the market entirely and shift heavily toward undervalued opportunities. — Source: GMO Research Library

- On Career Risk: Tilting heavily away from the dominant market index is necessary for long-term outperformance, even though it introduces significant short-term career risk for managers. — Source: Barron's Live Podcast

- On Opportunity Cost: "Plenty of other risk assets are trading at fair or even compelling valuations... there is no long-run expected return give-up for tilting your portfolio away from the AI darlings." — Source: Tideway Wealth

- On Global Mandates: Restricting an allocation to U.S. markets handcuffs a manager; the ability to allocate dynamically across global regions is essential for capturing mispricings. — Source: GMO Research Library

- On Tactical Patience: Dynamic allocation does not mean high turnover; it means taking a definitive stance when prices dictate it and waiting patiently for the thesis to play out. — Source: Ritholtz Masters in Business

- On Absolute Return: The objective of an unconstrained allocation model is to target absolute return opportunities regardless of what the broader market indices are doing. — Source: GMO Research Library

- On Contrarian Strategy: Taking a contrarian stance is uncomfortable but mathematically necessary when popular asset classes become dangerously overvalued. — Source: FEG Insight Bridge

- On Future Unpredictability: "More things can happen than will happen," which requires allocators to build portfolios robust enough to survive multiple economic scenarios. — Source: Substack

- On Avoiding the Worst: The primary benefit of dynamic allocation is not perfectly timing the exact bottom, but successfully avoiding the catastrophic losses that occur at market tops. — Source: GMO Research Library

Part 5: Navigating Market Bubbles

- On Defining Bubbles: A true bubble is defined mathematically as a two-standard deviation divergence of the price of any asset class above its long-term real price trend. — Source: GMO Research Library

- On Earnings vs. Valuation Bubbles: Inker argues that today's AI-heavy market risk may be an earnings bubble as much as a valuation bubble: reported profits can look reasonable while capital spending and unusually high margins make those earnings hard to sustain. — Reference: Excess Returns full transcript on Inker discussing AI, earnings bubbles, and capital cycles

- On Speculation: We frequently see periods characterized by very high valuations combined with clear signs of rampant retail and institutional speculation. — Source: Business Insider

- On Timing the Pop: Identifying a bubble is entirely different from timing its collapse; bubbles can persist and stretch further than rational analysis suggests is possible. — Source: GMO Research Library

- On Psychological Momentum: During the late stages of a bubble, fear of missing out overrides traditional risk management frameworks across the industry. — Source: Caplan Capital

- On Navigating the Decline: Avoiding a bubble entirely is often less damaging to long-term compounding than trying to ride it up and hoping to exit right before the crash. — Source: GMO Research Library

- On Institutional Pressure: The institutional imperative forces many asset managers to stay fully invested in a bubble because underperforming on the way up leads to client redemptions. — Source: GMO Research Library

- On Distinguishing Eras: The 2021 market environment exhibited classic bubble characteristics in speculative assets, fundamentally differing from normal bull markets. — Source: GMO Research Library

- On Historical Rhymes: Inker frames AI alongside earlier buildouts such as railroads, electricity, autos, the internet, and fiber optics: real technologies can change the world while excessive capital spending still destroys investor returns. — Reference: Excess Returns full transcript on Inker comparing AI capital spending with earlier infrastructure buildouts

- On Recovery Timelines: Investors who buy at the absolute peak of a two-standard deviation bubble often face decades before recovering their real purchasing power. — Source: GMO Research Library

Part 6: Assessing AI and Technological Shifts

- On the AI Boom: The current AI market surge carries the hallmarks of a "classic investment bubble," despite the underlying technology being undeniably real. — Source: Business Insider

- On Technological Disconnects: Inker cautions that transformational technologies do not automatically reward the builders: railroads, electricity, autos, the internet, and fiber changed the world, but overbuilding often destroyed the returns on the capital invested. — Reference: Excess Returns full transcript on Inker explaining why transformational technology does not guarantee builder profits

- On Capital Spending: The current market risks in the technology sector are deeply tied to whether aggressive capital spending by mega-cap companies will actually yield proportional earnings growth. — Source: Substack

- On Navigating Tech Hype: Investors frequently misprice technological shifts by assuming that a high growth rate in adoption translates directly to high profit margins for incumbents. — Source: GMO Research Library

- On the Internet Parallel: The AI boom might be easier to navigate than the 2000 dot-com bubble, but investors are still making similar errors regarding terminal growth rates. — Source: Substack

- On Concentration Risk: Heavy index concentration in a few AI-driven tech names creates a fragile market structure that is highly vulnerable to a single point of failure in earnings expectations. — Source: FEG Insight Bridge

- On the Price of Innovation: Paying any price for innovation is a guaranteed path to capital destruction; even the most revolutionary companies have a maximum rational valuation. — Source: GMO Research Library

- On Capital Misallocation: The immense gravitational pull of high valuations in tech leads to an unhealthy misallocation of capital away from vital physical economy sectors. — Source: Schroders

- On Secondary Winners: The ultimate financial winners of a technological revolution are often the traditional businesses that figure out how to deploy the tech to lower their own costs, not the creators. — Source: GMO Research Library

Part 7: Private Equity Skepticism

- On PE Soundness: The traditional private equity allocation model relies on assumptions of persistent outperformance that are largely unsupported by current empirical data. — Source: Portfolio Adviser

- On Performance Persistence: Performance persistence among private equity managers has largely disappeared over the last decade, making manager selection vastly more difficult. — Source: GMO Research Library

- On Justifying Fees: It is increasingly difficult for institutional investors to justify the high fees and total lack of liquidity in PE given the narrowing spread over public market equivalents. — Source: Portfolio Adviser

- On Quality Degradation: Private equity portfolios have demonstrated a concerning tendency to skew toward smaller, highly levered, and fundamentally lower-quality companies. — Source: GMO Research Library

- On Valuation Lags: The apparent low volatility of private equity is often a mirage created by smoothed pricing and delayed mark-to-market valuations rather than true stability. — Source: Advisor Perspectives

- On the Institutional Trend: Allocators blindly following the trend into private and alternative assets risk locking up capital at exactly the point in the cycle when flexibility is most valuable. — Source: GMO Research Library

- On Leverage Sensitivity: High interest rates disproportionately damage private equity returns by removing the cheap debt that previously papered over operational stagnation. — Source: GMO Research Library

- On Public Alternatives: In many regimes, public deep value stocks offer similar structural characteristics to private equity buyouts but with daily liquidity and lower fees. — Source: GMO Research Library

- On Asset Class Myths: Private equity is simply levered equity; it is not a distinct asset class immune to the gravitational pull of macroeconomic cycles and broad market multiples. — Source: GMO Research Library

Part 8: Emerging Markets and Global Opportunities

- On U.S. Premiums: The U.S. market has routinely traded at extreme and unjustified premiums to both its own historical average and the rest of the global market. — Source: Advisor Perspectives

- On Cheaper Valuations: Non-U.S. equities, and emerging markets in particular, frequently offer significantly cheaper valuations that provide a greater margin of safety. — Source: RBC Wealth Management

- On Navigating Inflation: "If there is one group of equities that deals with inflation on a pretty much continuous basis, it is emerging equities." — Source: RBC Wealth Management

- On Strategic Hedging: "In our BenchmarkFree Allocation Strategy we are currently hedging a piece of the risk in emerging markets to protect against the possibility of US dollar strength." — Source: Advisor Perspectives

- On Emerging Value: Identifying quality within emerging market value stocks is one of the few remaining areas where active management can consistently exploit pricing inefficiencies. — Source: GMO Research Library

- On Geopolitical Risk: Geopolitical concerns often cause indiscriminate selling in international markets, creating mispricings for allocators willing to look past immediate headlines. — Source: Barron's Live Podcast

- On Dividend Yields: Emerging markets often compensate investors for perceived political and currency risks through substantially higher dividend yields compared to U.S. counterparts. — Source: GMO Research Library

- On Currency Fluctuations: True global allocation requires an active approach to currency risk, as currency movements can completely overwhelm the underlying equity returns in international markets. — Source: GMO Research Library

- On Long-Term Tailwinds: Despite short-term volatility, emerging markets benefit from demographic tailwinds and expanding middle classes that provide a structurally sound backdrop for long-term compounding. — Source: GMO Research Library