Lessons from Bobby Jain

Bobby Jain spent two decades building trading and asset management businesses at Credit Suisse before becoming Co-CIO at Millennium Management. Known for scaling multi-manager platforms and risk systems, he eventually left to launch his own firm, Jain Global. This collection details his methods for managing portfolio managers and institutionalizing alpha across large-scale trading operations.

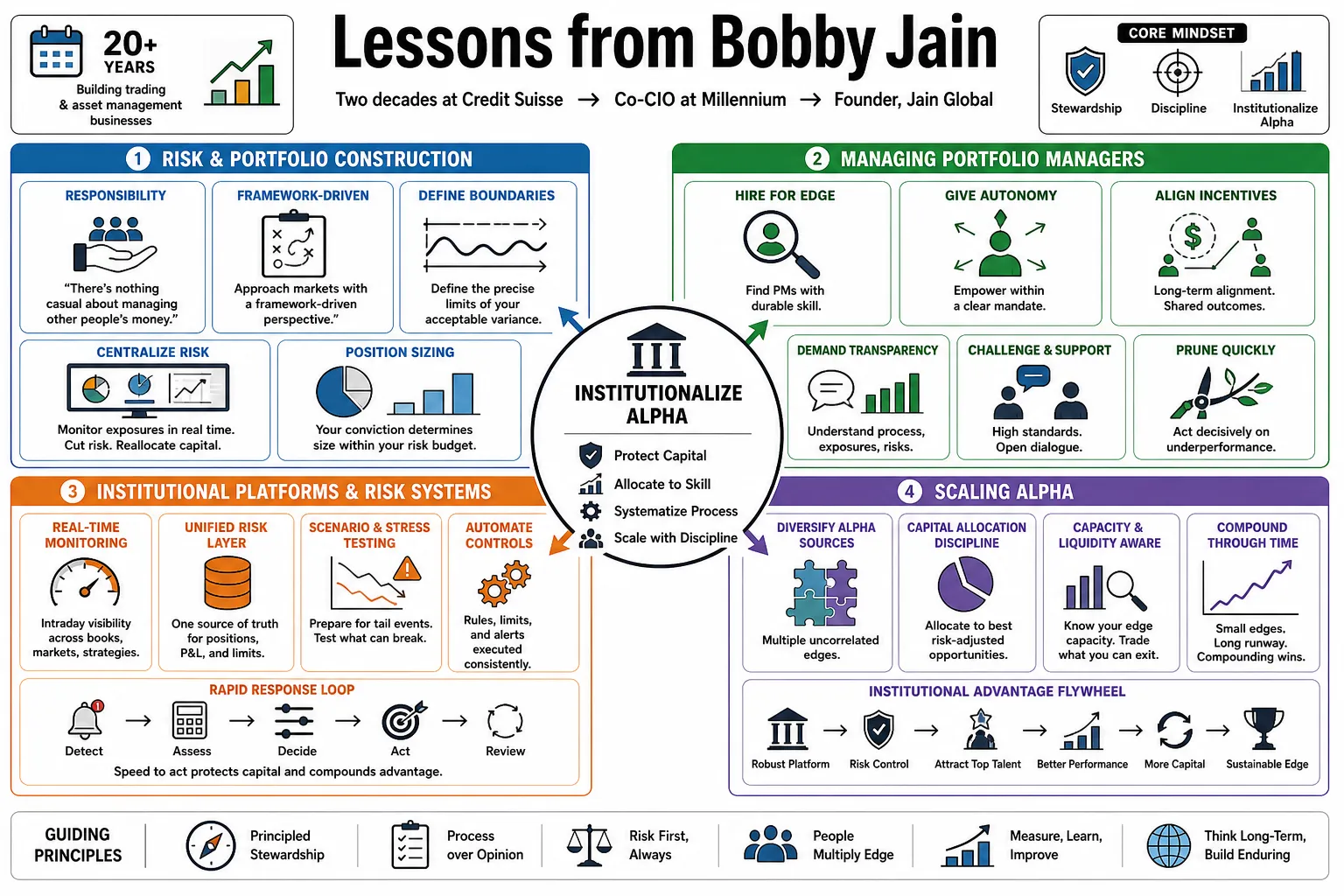

Part 1: Risk and Portfolio Construction

- On the responsibility of managing capital: "There's nothing casual about managing other people's money. I have that deeply embedded in my thinking." — Source: [Capital Allocators]

- On framework-driven investing: "You must approach markets with a framework-driven perspective; otherwise, the noise of daily trading will overwhelm your fundamental edge." — Source: [Capital Allocators]

- On setting boundaries: "Risk management is less about predicting the future and more about defining the precise limits of your acceptable variance today." — Source: [Bloomberg]

- On centralizing risk: "The platform must maintain rigorous oversight to monitor exposures in real time, allowing the firm to quickly cut risk or reallocate capital to the best-performing teams." — Source: [HedgeCo]

- On position sizing: "Your conviction should dictate your sizing, but your risk limits must dictate your survival." — Source: [Financial Times]

- On drawdowns: "Handling a drawdown correctly is what separates a career portfolio manager from a temporary market participant." — Source: [eFinancialCareers]

- On liquidity: "Never assume liquidity will be there when you need it most; structure your portfolio for the environment you hope never happens." — Source: [Bloomberg]

- On correlation: "True diversification requires understanding the hidden correlations that only reveal themselves during a stress event." — Source: [Capital Allocators]

- On the role of a CIO: "The Chief Investment Officer is ultimately the Chief Risk Officer of the firm's collective culture and capital." — Source: [eFinancialCareers]

- On adapting to volatility: "Volatility is a tool for those who have built the right infrastructure, and a weapon against those who haven't." — Source: [Financial Times]

Part 2: The Multi-Manager Model

- On platform architecture: "Start a billion and a half dollar fundamental equities business or quant equities. When that works, go do the next thing normal. The problem is now you started that first thing, you built everything for that. You've built your risk system for that. You've hired your lawyers for that." — Source: [Capital Allocators]

- On structural advantages: "The multi-manager model functions as a platform that allocates capital across numerous semi-autonomous teams, reducing reliance on any single strategy." — Source: [HedgeCo]

- On pass-through fees: "Pass-through structures allow firms to offer highly competitive, performance-linked compensation packages to elite talent, which is essential for running an expensive trading factory." — Source: [Financial Times]

- On economies of scale: "Building a pod shop requires sophisticated, high-cost technology and data infrastructure to ensure that risk controls can function across diverse asset classes and time zones." — Source: [eFinancialCareers]

- On capital allocation: "The speed at which a platform can shift capital from underperforming pods to high-conviction ideas is its true alpha." — Source: [Bloomberg]

- On pod autonomy: "Portfolio managers need the autonomy to execute their specific mandates, but they must operate within the strict boundaries of the firm's central risk parameters." — Source: [Capital Allocators]

- On strategy diversification: "Launching with a seven-legged stool—fundamental, quant, arbitrage, rates, macro, credit, and Asia—provides a diversified foundation from the start." — Source: [Capital Allocators]

- On the trading factory: "A modern hedge fund is less a boutique investment shop and more a highly engineered trading factory." — Source: [HedgeCo]

- On survival of the fittest: "The model is inherently high-pressure; capital can be pulled and pods can be closed rapidly if performance targets are not met." — Source: [eFinancialCareers]

- On infrastructure costs: "The fixed costs of competing at the highest level of this industry are staggering, which is why scale is no longer an option, it's a prerequisite." — Source: [Financial Times]

Part 3: Talent and Culture

- On hiring criteria: "We are looking for '35-year-old killers'—traders and analysts in their prime who are often overlooked or underappreciated at larger, established firms." — Source: [eFinancialCareers]

- On talent acceleration: "Our business proposition is talent acceleration. We want to take good people and make them great by providing them with institutional-grade infrastructure." — Source: [Capital Allocators]

- On team balance: "In addition to the aggressive risk-takers, you must hire steady producers to balance the firm's investment teams." — Source: [eFinancialCareers]

- On mentorship: "Mentorship and coaching are critical; providing a PM with capital is only half the job, you must also provide them with guidance." — Source: [Capital Allocators]

- On performance culture: "You have to build a culture where excellence is the baseline, and anything less is immediately addressed." — Source: [Bloomberg]

- On retaining top talent: "Compensation is a factor, but top tier talent stays for the infrastructure, the data, and the execution capabilities." — Source: [Financial Times]

- On interview questions: "The interview question was, what's 49 times 28? And I say 1372. They say, Mets play the Yankees in the World Series. What are the chances? Mets winning four. I say one out of 16. They say, you're hired." — Source: [Capital Allocators]

- On the human element: "Despite all the quantitative models, this remains a fundamentally human business driven by the psychology of the portfolio managers." — Source: [eFinancialCareers]

- On identifying edge: "When interviewing a PM, you are trying to isolate their specific, repeatable edge from the noise of market beta." — Source: [Capital Allocators]

- On career longevity: "The people who last in this business are those who are intellectually honest about their mistakes and relentlessly curious about the markets." — Source: [Bloomberg]

Part 4: Scaling a Hedge Fund

- On intentional design: "The firm must be carefully constructed so that it can easily scale, rather than having to rebuild its foundation with every new strategy." — Source: [Capital Allocators]

- On the difficulty of launching: "Building a large-scale platform from scratch is like landing three airplanes at once." — Source: [eFinancialCareers]

- On operational drag: "Every manual process in your back office is a tax on your alpha generation." — Source: [HedgeCo]

- On technological supremacy: "In the current era, your technology stack is as important as your investment thesis." — Source: [Financial Times]

- On barriers to entry: "Obviously, there's gigantic barriers to entry in this business, but I felt like Millennium was in a great place... and so I said, 'This is a time when I can get off and do it on my own.'" — Source: [Capital Allocators]

- On global reach: "You cannot build a true multi-strategy platform today without a dedicated, sophisticated presence in Asia and Europe from day one." — Source: [Bloomberg]

- On managing growth: "Rapid headcount expansion requires a commensurate expansion in risk oversight; they must grow in lockstep." — Source: [eFinancialCareers]

- On execution infrastructure: "The best idea in the world is worthless if your execution infrastructure cannot capture the spread before it disappears." — Source: [Capital Allocators]

- On consolidation: "The industry is increasingly consolidated, and scale is often viewed as a requirement for survival against established competitors." — Source: [HedgeCo]

Part 5: Leadership and Career Growth

- On formative experiences: "Credit Suisse was a clever place where I gained foundational experience in proprietary trading, derivatives, and asset management." — Source: [Capital Allocators]

- On career transitions: "Moving from managing a single proprietary desk to overseeing global asset management requires a complete rewiring of how you view risk and delegation." — Source: [Bloomberg]

- On decision making: "As a leader, your job is not to make every decision, but to build the framework that allows your team to make the right decisions." — Source: [Financial Times]

- On continuous learning: "The markets evolve constantly; the moment you rely entirely on what worked yesterday, you become obsolete." — Source: [Capital Allocators]

- On handling pressure: "Leadership in a multi-manager environment means absorbing the macro anxiety so your portfolio managers can focus on the micro execution." — Source: [eFinancialCareers]

- On building trust: "Trust with your investors is built over decades of transparency, especially during periods of underperformance." — Source: [HedgeCo]

- On taking leaps: "Leaving an established, successful seat to build something new requires a specific type of calculated irrationality." — Source: [Capital Allocators]

- On accountability: "You have to own the bad prints just as much as the good ones; radical accountability is the only way to run a firm." — Source: [Bloomberg]

- On resilience: "Setbacks are inevitable when building something of scale; the architecture of your firm must be designed to withstand those shocks." — Source: [Financial Times]

Part 6: Trading and Markets

- On market efficiency: "Markets are more efficient than ever, which means the required infrastructure to extract alpha has become exponentially more complex." — Source: [Capital Allocators]

- On quantitative and fundamental convergence: "The dividing line between fundamental analysis and quantitative modeling is dissolving; the best PMs utilize both seamlessly." — Source: [Bloomberg]

- On arbitrage: "Index arbitrage taught me early on that small, consistent edges, when scaled appropriately, create formidable businesses." — Source: [Capital Allocators]

- On market noise: "A disciplined trader learns to filter out the headline noise and focus strictly on the structural flows of capital." — Source: [eFinancialCareers]

- On macro environments: "You cannot control the macro environment, but you can control your portfolio's sensitivity to it." — Source: [Financial Times]

- On trading psychology: "The most dangerous emotion in trading is not fear, but the need to be proven right by the market." — Source: [HedgeCo]

- On adapting to change: "The strategies that worked in a zero-interest-rate environment require fundamental recalibration when the cost of capital normalizes." — Source: [Bloomberg]

- On liquidity premiums: "You have to deeply understand what you are getting paid for—are you generating alpha, or simply harvesting a liquidity premium?" — Source: [Capital Allocators]

- On data utilization: "Data is commoditized; the edge lies in how quickly your systems can ingest, clean, and act upon that data." — Source: [eFinancialCareers]

Part 7: The Institutionalization of Alpha

- On industry evolution: "The biggest trend in our business is the privatization of alpha... the multi-strategy firms over time have more and more employee money and less and less available to investors." — Source: [Capital Allocators]

- On the migration of risk: "Risk-taking has steadily migrated from the proprietary desks of investment banks to large, institutionalized hedge funds and private credit firms." — Source: [Financial Times]

- On institutional requirements: "Today's allocators demand institutional-grade reporting, compliance, and risk frameworks before they will even consider the performance." — Source: [HedgeCo]

- On competitive moats: "The technological and operational infrastructure of a tier-one multi-manager is a nearly insurmountable moat for new entrants." — Source: [Bloomberg]

- On fee structures: "Investors will tolerate pass-through structures only as long as the net returns consistently justify the operational load." — Source: [eFinancialCareers]

- On the war for talent: "The institutionalization of alpha means the war for talent is no longer just about hiring PMs, but hiring the best engineers and data scientists." — Source: [Capital Allocators]

- On structural advantages: "Large platforms have a structural advantage in their ability to internalize costs and spread them across a massive capital base." — Source: [Financial Times]

- On regulatory landscapes: "Navigating global compliance and regulation is no longer a back-office function; it is a core component of the firm's strategic architecture." — Source: [Bloomberg]

- On capacity constraints: "Alpha is ultimately capacity constrained; the challenge for a large platform is finding new vectors of return without diluting the overall quality." — Source: [HedgeCo]

Part 8: Patience and Long-Term Capital

- On setting expectations: "Patience is required when evaluating the performance and evolution of a newly launched platform." — Source: [eFinancialCareers]

- On compounding: "The magic of this business isn't in hitting home runs; it's in the quiet, relentless compounding of capital over long horizons." — Source: [Capital Allocators]

- On investor alignment: "You must align your capital base with the duration of your investment strategies to prevent forced liquidations during drawdowns." — Source: [Bloomberg]

- On strategic pivots: "When the market dictates that the independent path is less viable than a strategic partnership, the pragmatic leader adapts the structure to protect the talent." — Source: [Financial Times]

- On building for the future: "We are not building a firm for the next quarter; we are architecting a platform that will be relevant a decade from now." — Source: [Capital Allocators]

- On the nature of setbacks: "Early performance friction is a feature, not a bug, of building complex systems; it shows you exactly where the plumbing needs tightening." — Source: [eFinancialCareers]

- On capital velocity: "The true measure of a firm's efficiency is the velocity at which it can deploy and recycle capital into high-conviction ideas." — Source: [HedgeCo]

- On staying grounded: "No matter how sophisticated the models become, you must never lose sight of the foundational mechanics of supply and demand." — Source: [Bloomberg]

- On ultimate objectives: "The goal is not simply to generate returns, but to build an enduring institution that reliably solves the asset allocation problems of our clients." — Source: [Capital Allocators]