Lessons from Brian Portnoy

Behavioral finance expert Brian Portnoy, author of The Geometry of Wealth, centers his work on "funded contentment": the idea that financial planning should focus on supporting personal priorities rather than endless accumulation. This profile outlines his arguments for why investors struggle with complex choices and how to better align daily money habits with actual values.

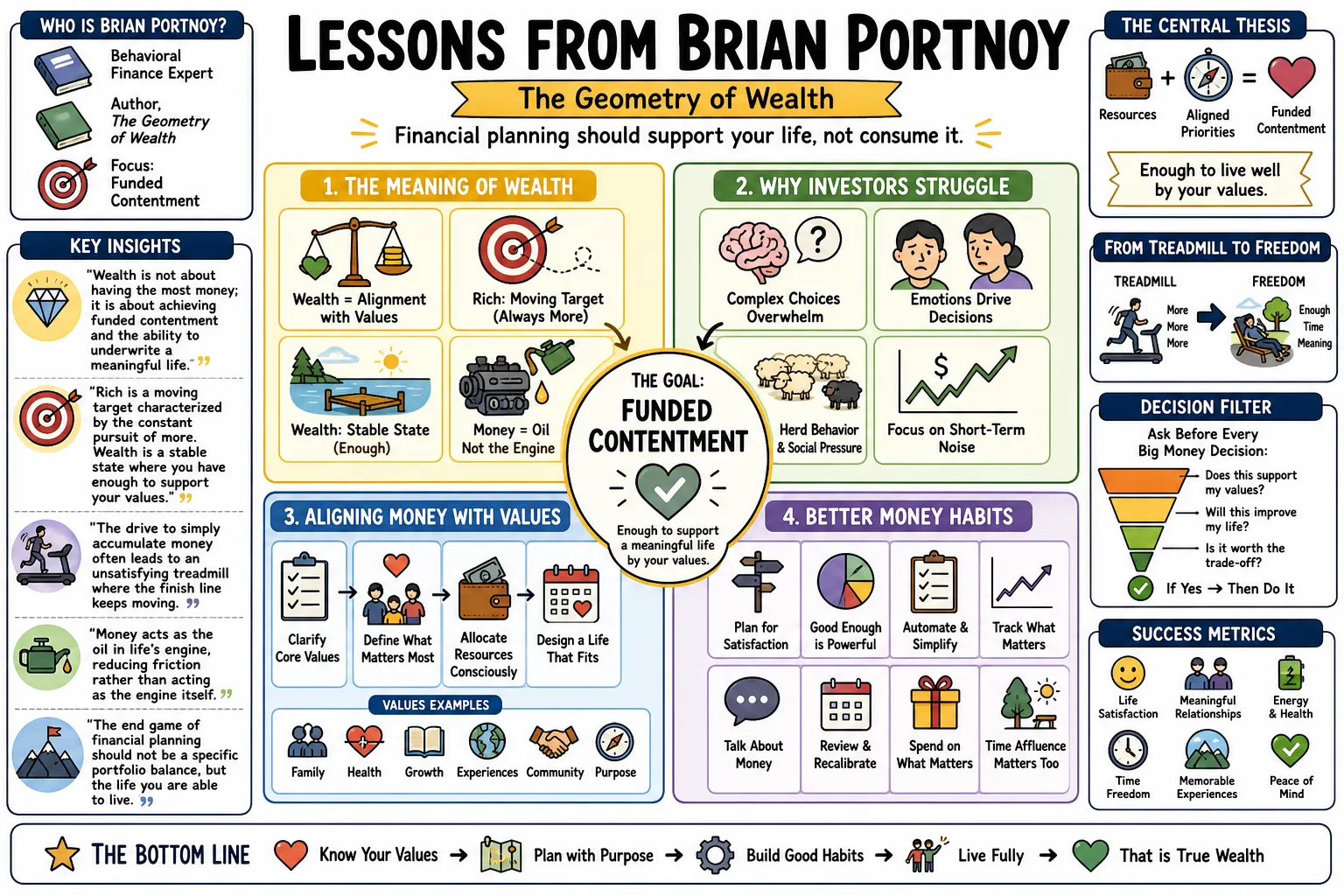

Part 1: The Meaning of Wealth

- On the definition of wealth: "Wealth is not about having the most money; it is about achieving funded contentment and the ability to underwrite a meaningful life." — Source: [The Geometry of Wealth]

- On being rich versus being wealthy: "Rich is a moving target characterized by the constant pursuit of more. Wealth is a stable state where you have enough to support your values." — Source: [The Rational Reminder Podcast]

- On the treadmill of accumulation: "The drive to simply accumulate money often leads to an unsatisfying treadmill where the finish line keeps moving." — Source: [Boldin Your Money Podcast]

- On money as a tool: "Money acts as the oil in life's engine, reducing friction rather than acting as the engine itself." — Source: [The Geometry of Wealth]

- On the ultimate goal: "The end game of financial planning should not be a specific portfolio balance, but the peace of mind that comes with funded contentment." — Source: [Shaping Wealth]

- On buying happiness: "Money does buy more happiness when spent wisely, especially when directed toward experiences, other people, and buying back your time." — Source: [The Geometry of Wealth]

- On relativity: "Our perception of wealth is often ruined by comparing our current financial state to the visible consumption of others." — Source: [The Rational Reminder Podcast]

- On stability: "A wealthy life is marked by the emotional stability that arises when your finances align with your personal definition of enough." — Source: [Rhodes to Wealth Podcast]

- On shifting focus: "We spend too much time calculating returns and too little time defining what the returns are actually meant to achieve." — Source: [The Geometry of Wealth]

- On genuine success: "Financial success is achieved the moment you stop worrying about money and start focusing on the life it allows you to live." — Source: [ReSolve Asset Management]

Part 2: The Geometry of Wealth

- On the order of operations: "Financial planning fails when we skip straight to tactics without first defining our purpose." — Source: [The Geometry of Wealth]

- On the Circle of purpose: "Purpose is about defining what truly matters to you. It is the necessary starting point for any financial strategy." — Source: [The Geometry of Wealth]

- On the Triangle of priorities: "Setting priorities bridges the gap between your abstract purpose and your concrete financial tactics, dictating how you earn, spend, and save." — Source: [The Geometry of Wealth]

- On the Square of tactics: "Tactics are the everyday decisions regarding asset allocation, tax optimization, and budgeting that execute your priorities." — Source: [The Geometry of Wealth]

- On simplicity: "The most effective financial tactics are usually simple, but simple is rarely easy to execute consistently." — Source: [The Rational Reminder Podcast]

- On adaptability: "Your geometric framework must remain flexible. As your purpose evolves over time, your priorities and tactics must adjust accordingly." — Source: [Shaping Wealth]

- On alignment: "Friction occurs when your investment tactics do not align with your stated priorities, usually due to chasing short-term performance." — Source: [ReSolve Asset Management]

- On starting with 'why': "Until you can clearly articulate why you are investing, any discussion about how you are investing is premature." — Source: [The Geometry of Wealth]

- On measuring progress: "Progress is measured by how well your tactics support your purpose, not by whether you beat a benchmark index." — Source: [Boldin Your Money Podcast]

- On structural integrity: "A solid financial life relies on the structural integrity of all three shapes working together: clear purpose, strict priorities, and simple tactics." — Source: [The Geometry of Wealth]

Part 3: The Investor's Paradox

- On the paradox of choice: "We crave abundant investment choices, but more choices often leave us overwhelmed, less empowered, and ultimately less successful." — Source: [The Investor's Paradox]

- On the illusion of control: "A wider menu of investment options gives us the illusion of control, while actually increasing the probability of making a behavioral error." — Source: [The Investor's Paradox]

- On complex times: "Because volatile markets prompt us to seek complex solutions, investors mistakenly gravitate toward convoluted strategies that often underperform." — Source: [The Investor's Paradox]

- On information overload: "We are drowning in financial data but starved for the wisdom required to apply it to our own lives." — Source: [Boldin Your Money Podcast]

- On the value of constraints: "Limiting your investment choices deliberately is one of the most effective ways to improve your long-term returns." — Source: [The Investor's Paradox]

- On outsourcing decisions: "The vocation of outsourcing investment discretion to professional money managers is a modern response to the overwhelming burden of choice." — Source: [The Investor's Paradox]

- On the financial supermarket: "Navigating the global financial supermarket requires a framework of simplicity, otherwise you will buy items you don't need." — Source: [ReSolve Asset Management]

- On having less: "In the context of portfolio construction, adding more moving parts usually detracts from the reliability of the outcome." — Source: [The Investor's Paradox]

- On decision fatigue: "Constantly evaluating new investment products depletes the mental energy required to stick to a long-term plan." — Source: [The Rational Reminder Podcast]

- On filtering noise: "The investor's primary job has shifted from finding information to fiercely filtering out the noise." — Source: [The Investor's Paradox]

Part 4: The Psychology of Money

- On human wiring: "Our brains are fundamentally wired for survival in the short term, which makes us naturally terrible at long-term compounding." — Source: [Shaping Wealth]

- On managing expectations: "Met expectations lead to happiness, while unmet expectations create sadness. Managing what you expect is as important as managing what you earn." — Source: [The Geometry of Wealth]

- On behavioral reality: "We do not optimize for economic utility; we optimize to sleep well at night and avoid immediate emotional pain." — Source: [The Rational Reminder Podcast]

- On self-awareness: "Understanding your own cognitive biases is the first defense against making catastrophic financial mistakes during a market panic." — Source: [Boldin Your Money Podcast]

- On fear and greed: "Fear of loss heavily outweighs the joy of gain, causing investors to abandon sound strategies exactly when they should hold firm." — Source: [Rhodes to Wealth Podcast]

- On overconfidence: "Intellectual humility is an investor's greatest asset. Assuming you can predict the future is a quick path to capital destruction." — Source: [ReSolve Asset Management]

- On emotional regulation: "Good investing is less about raw intelligence and more about the ability to regulate your emotions when everyone else is losing theirs." — Source: [The Geometry of Wealth]

- On the impact of news: "Manic financial news flow is designed to trigger your fight-or-flight response, making it toxic for long-term decision making." — Source: [The Investor's Paradox]

- On resilience: "Financial resilience is built by accepting that bad times will occur and planning your emotional response before the crisis hits." — Source: [The Geometry of Wealth]

Part 5: The Four Dimensions of Contentment

- On Connection: "A meaningful life is deeply rooted in connection and the quality of how we engage with family and community." — Source: [Shaping Wealth]

- On Control: "Money's greatest utility is buying control over your own time, allowing you to choose how and when you work." — Source: [Boldin Your Money Podcast]

- On Competence: "We find deep satisfaction in getting better at things. Funded contentment allows us the space to pursue mastery and competence." — Source: [The Geometry of Wealth]

- On Context: "Understanding your place in the world gives purpose to your financial decisions beyond mere survival." — Source: [The Rational Reminder Podcast]

- On the non-financial: "True wealth management must address physical, emotional, and spiritual wellbeing, because financial capital is useless without them." — Source: [Boldin Your Money Podcast]

- On evaluating spending: "Every purchase should be evaluated by asking whether it increases your connection, control, competence, or context." — Source: [The Geometry of Wealth]

- On identifying purpose: "Purpose is rarely found in a spreadsheet; it is discovered by observing what you do with your time when you have no obligations." — Source: [ReSolve Asset Management]

- On the limits of money: "Once basic needs and a sense of security are met, additional dollars yield rapidly diminishing returns in terms of actual contentment." — Source: [The Rational Reminder Podcast]

- On intentionality: "A meaningful life does not happen by accident; it requires intentionally directing your financial resources toward what you value most." — Source: [Shaping Wealth]

Part 6: How the Experts Invest

- On personal variance: "There is no single right way to invest; the best strategy is the one you can stick with during terrible times." — Source: [How I Invest My Money]

- On expert vulnerability: "Even financial experts have diverse, human-centered paths to success that are heavily influenced by their upbringing and personal fears." — Source: [How I Invest My Money]

- On the index fund superpower: "Being willing to stick to a diversified portfolio of index funds is the closest thing to an investing superpower that exists." — Source: [How I Invest My Money]

- On optimizing for peace: "Many professionals do not optimize for the highest possible return; they optimize for liquidity, security, and peace of mind." — Source: [How I Invest My Money]

- On financial jargon: "The financial industry uses jargon to confuse consumers and justify fees; clear transparency reveals that investing can be deeply personal and simple." — Source: [How I Invest My Money]

- On evolving strategies: "An investor's strategy should naturally evolve as they age, shifting from aggressive accumulation to capital preservation and meaning." — Source: [Rhodes to Wealth Podcast]

- On values-driven choices: "The portfolios of experts often reflect their deepest values, proving that where you put your money is a vote for the life you want." — Source: [How I Invest My Money]

- On discarding complexity: "Those who know the most about the financial markets often choose the simplest investment vehicles for their own money." — Source: [How I Invest My Money]

- On the role of history: "Personal financial decisions are deeply rooted in family history; we often invest to avoid the financial trauma experienced by our parents." — Source: [How I Invest My Money]

Part 7: Financial Planning as Life Planning

- On the true nature of planning: "Financial planning is not math; it is life planning disguised as math." — Source: [Shaping Wealth]

- On adapting to change: "A good financial plan is a living document that adapts to the inevitable changes in your personal circumstances and worldview." — Source: [The Geometry of Wealth]

- On setting priorities: "If everything is a priority, nothing is. Financial planning forces the difficult trade-offs required to allocate finite resources." — Source: [The Geometry of Wealth]

- On retirement: "Retirement should not be viewed as the end of work, but as the beginning of a phase where your time is fully your own." — Source: [The Rational Reminder Podcast]

- On early conversations: "Discussions about money should start with questions about meaning and purpose long before discussing risk tolerance or asset allocation." — Source: [ReSolve Asset Management]

- On saving versus investing: "Saving is the act of deferring current consumption; investing is the act of protecting that deferred consumption from inflation." — Source: [The Geometry of Wealth]

- On defining 'enough': "The most powerful financial calculation you can make is determining your personal number for enough." — Source: [Boldin Your Money Podcast]

- On goal ambiguity: "Unclear goals lead to erratic portfolios. Clarity in what you want your life to look like dictates the risk you need to take." — Source: [The Investor's Paradox]

- On continuous learning: "Your priorities will change as you gain wisdom. The financial plan must gracefully accommodate the person you will become." — Source: [Rhodes to Wealth Podcast]

Part 8: The Financial Advice Industry

- On the role of an advisor: "A great financial advisor acts less like a stock picker and more like a behavioral coach, keeping you from making emotional errors." — Source: [Shaping Wealth]

- On the illusion of expertise: "Investors often mistake complexity for expertise, willingly paying high fees for strategies that fail to deliver basic market returns." — Source: [The Investor's Paradox]

- On transparency: "The shift toward transparent, fee-only advice is forcing the industry to compete on the value of guidance rather than the sale of products." — Source: [ReSolve Asset Management]

- On bridging the gap: "The primary gap in modern finance is not a lack of data, but the inability to translate that data into human wisdom." — Source: [The Geometry of Wealth]

- On manager selection: "Chasing hot fund managers is pointless if you haven't first defined your own priorities and what a meaningful life looks like." — Source: [The Investor's Paradox]

- On industry incentives: "The financial industry is largely incentivized to sell you action and complexity, while your success depends on patience and simplicity." — Source: [Boldin Your Money Podcast]

- On behavioral guardrails: "An advisor's most valuable function is building structural guardrails that prevent you from acting on your worst impulses." — Source: [Shaping Wealth]

- On standardizing advice: "We cannot standardize advice because personal finance is deeply personal; each plan must reflect the unique wiring of the individual." — Source: [How I Invest My Money]

- On the future of wealth management: "The future of wealth management belongs to those who integrate financial capital with emotional and psychological wellbeing." — Source: [ReSolve Asset Management]