Bruce Greenwald is an economist and authority on value investing who spent decades teaching at Columbia Business School. Known for modernizing the frameworks of Benjamin Graham and David Dodd, he shifted the focus of modern investing away from speculative forecasting and toward measurable earnings power and structural barriers to entry. This profile catalogs his specific frameworks for valuation, competitive advantage, strategy, and macroeconomic reality.

Part 1: Value Investing Framework

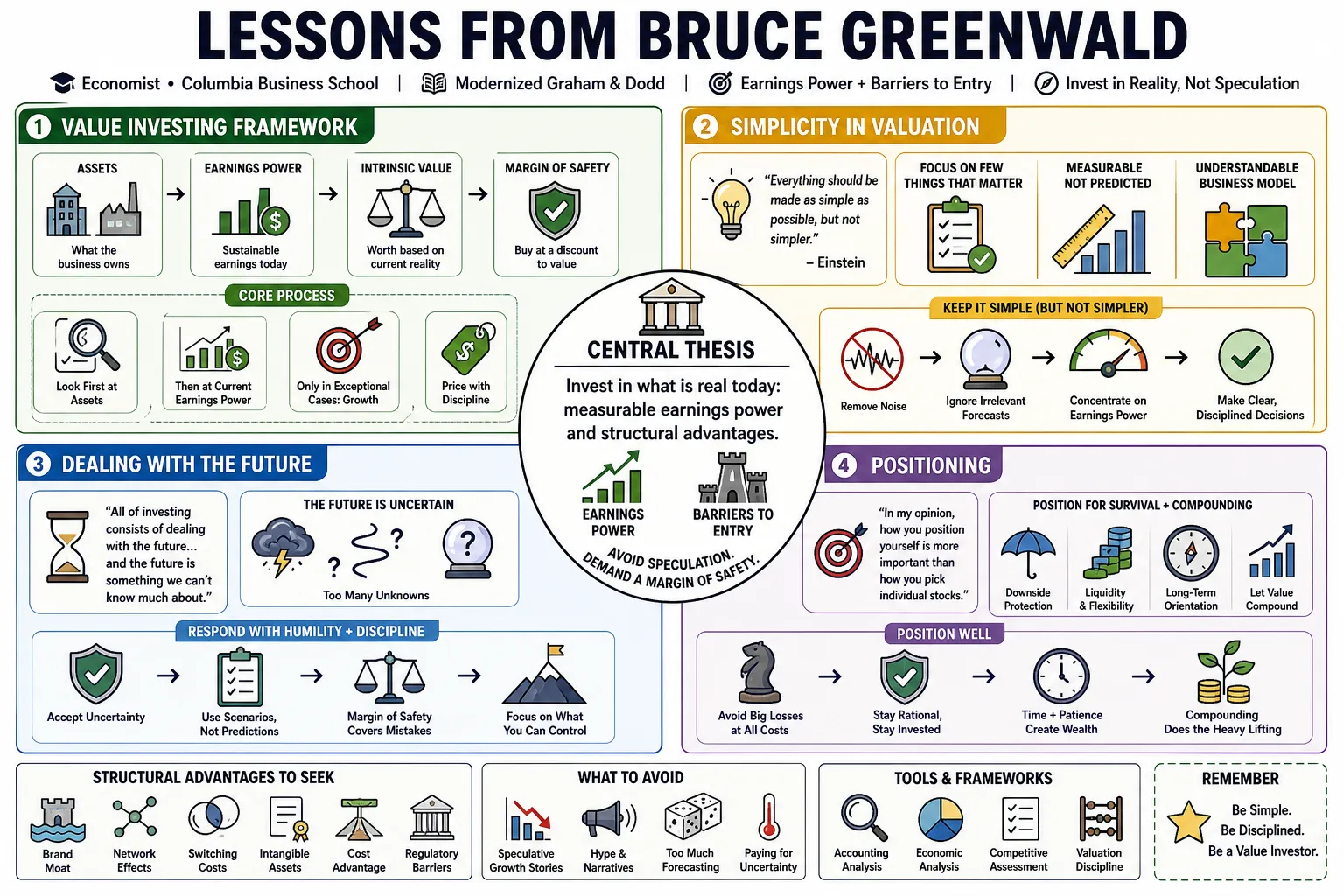

- On Simplicity in Valuation: "Keep in mind Einstein’s admonition that 'Everything should be made as simple as possible, but not simpler.'" — Source: Goodreads

- On the Core Process: "Value investors prefer to estimate the intrinsic value of a company by looking first at the assets and then at the current earnings power of a company." — Source: Value Investing: From Graham to Buffett and Beyond

- On Speculation: "Only in exceptional cases are they willing to factor in the value of potential growth." — Source: GuruFocus

- On Dealing with the Future: "All of investing consists of dealing with the future... and the future is something we can’t know much about." — Source: Goodreads

- On Positioning: "In my opinion, the key to dealing with the future lies in knowing where you are, even if you can’t know precisely where you’re going." — Source: Scribd

- On Search Strategies: Do not look everywhere; focus on specific pools of opportunity where you have an analytical advantage, such as ignored, distressed, or boring companies. — Source: Columbia Business School

- On the Margin of Safety: A true margin of safety provides three to five years for the market to come around to your valuation, removing the need for precise market timing. — Source: The Motley Fool

- On Enterprise Value: The margin of safety must be calculated at the enterprise level, including debt, because high leverage can quickly wipe out the equity margin of safety. — Source: Watchlist Investing

- On Market Efficiency: "When someone buys a stock, another active investor is selling the stock." — Source: Columbia News

- On Specialization: Because modern markets are highly competitive, generalist investors operate at a severe disadvantage against specialists with deep industry knowledge. — Source: MOI Global

Part 2: Earnings Power Value (EPV)

- On the Second Calculation: "The second most reliable measure of a firm's intrinsic value is the second calculation made by Graham and Dodd, namely, the value of its current earnings, properly adjusted." — Source: GuruFocus

- On Reliability: "This value can be estimated more accurately than future earnings or cash flows, and it is more relevant to today's values than earnings in the past." — Source: GuruFocus

- On the EPV Formula: The EPV of a firm is calculated as adjusted earnings times 1/R, with R representing the current cost of capital. — Source: MarketXLS

- On Zero Growth: EPV assumes zero growth, forcing the investor to determine if a company’s current profitability is sustainable strictly on its existing merits. — Source: Stockopedia

- On Franchise Value: Franchise value is defined directly as the amount by which the Earnings Power Value of the firm exceeds the reproduction cost of its assets. — Source: Medium

- On Asset Reproduction: The first step in valuation is calculating what it would cost a competitor to reproduce the assets of the business from scratch. — Source: Daniel Mnke

- On Bridging the Gap: EPV is designed to bridge the gap between tangible asset-based valuation and the highly speculative nature of traditional discounted cash flow models. — Source: Watchlist Investing

- On Getting Growth for Free: If you purchase a business at its Earnings Power Value, any future growth you receive is essentially free, creating a built-in margin of safety. — Source: EdgePoint Wealth

- On Earnings Adjustments: EPV requires normalizing earnings by adjusting for cyclicality, one-time charges, and distinguishing maintenance capital expenditures from growth expenditures. — Source: GuruFocus

- On Discounted Cash Flows: "There is a fundamental stupidity about discounted-cash-flow valuations," as they allow investors to manipulate outcomes by slightly tweaking terminal cash flows or discount rates. — Source: Tao Value

Part 3: Competitive Advantage and Moats

- On the Definition of a Moat: "Competitive advantages are actually barriers to entry." — Source: Reddit Investing

- On Impermanence: "No matter how complex and unique a product seems at the start, in the long run they are all toasters." — Source: Redeye Capital

- On Strategic Opportunities: "It is barriers to entry, not differentiation by itself, that creates strategic opportunities." — Source: Goodreads

- On the Dominant Force: In business strategy, the presence of barriers to entry is the one force that dominates all others in determining sustained profitability. — Source: Morgan Stanley

- On Supply-Side Advantages: Supply-side moats are strictly rooted in proprietary technology or structural access to lower production costs. — Source: Columbia Business School

- On Demand-Side Advantages: Demand-side moats are created through customer captivity, which is driven by habit, high search costs, or high switching costs. — Reference: Competition Demystified notes on customer captivity, habit, switching costs, and search costs

- On Economies of Scale: Economies of scale act as a moat primarily when they are localized or niche-specific, rather than global. — Source: Medium

- On Market Dominance: Dominance in a specific, smaller local market is often far more defensible and valuable than holding a small share of a massive global market. — Source: Substack

- On Evaluating Competitors: Understanding a moat requires calculating the specific scale a new entrant would need to achieve just to become economically viable. — Source: Substack

- On Capital Destruction: Companies destroy shareholder value when they attempt to invest outside of their existing moats, effectively sending capital outside the castle walls. — Source: Australian Shareholders Association

Part 4: Growth vs. Value

- On Chasing Growth: "Growth investing is the unsafe sex of the investment process." — Source: EdgePoint Wealth

- On the Value of Growth: "When you have no barriers to entry, the value of growth is 0." — Source: Andrew Liu

- On ROIC Requirement: Growth is only economically valuable if the company earns a higher return on its invested capital than its cost of capital. — Source: Wall Street Prep

- On Destroying Value: "Your costs of growth are higher than the return on invested capital. That's why return on invested capital (ROIC) is such an important metric. You want to earn excess capital for every $1 invested." — Source: Daniel Mnke

- On Competitive Markets: If ROIC exactly equals the cost of capital, the company is operating in a perfectly competitive market, meaning growth adds no fundamental value. — Source: HHS.se

- On Sustainable Earnings: High returns on invested capital over a long period are the primary indicator that a company's earnings power is sustainable and protected. — Source: Goodreads

- On the Franchise Requirement: Any growth achieved without the protection of a competitive advantage will eventually be competed away by new entrants. — Source: Medium

- On Separating Value Components: Valuation should rigorously separate asset value, earnings power value, and growth value, rather than blending them into a single projection. — Source: Watchlist Investing

- On Defining Value Stocks: "Value investing is about buying the diseased stocks that are beaten down in price." — Source: EdgePoint Wealth

Part 5: Strategy vs. Tactics

- On Strategic Definition: Strategic decisions are exclusively those that must account for the anticipated reactions of competitors. — Source: Tianpan

- On Tactics: Internal operational improvements, such as cost-cutting or quality control, are tactical, not strategic, if they do not alter the competitive landscape. — Source: Prasad Capital

- On Operational Necessity: "Without the protection of barriers to entry, the only option a company has is to run itself as efficiently and effectively as possible." — Source: Goodreads

- On Survival: "Operational effectiveness can be the single most important factor in the success, or indeed in the survival, of any business." — Source: Goodreads

- On Normal Returns: "If no forces interfere with the process of entry by competitors, profitability will be driven to levels at which efficient firms earn no more than a 'normal' return." — Source: Goodreads

- On Differentiation: Differentiation alone does not create a strategic advantage unless it translates directly into a measurable barrier to entry. — Source: SlideShare

- On Franchise Fade: Even great franchises eventually fade; strategic planning must model the timeline of returns normalizing to free-entry levels. — Source: Jim Bouman

- On Looking Outward: True strategy looks outward at the market structure, while tactical management looks inward at process execution. — Source: Prasad Capital

- On Simplified Strategy: Business strategy is radically simplified when executives realize almost all strategic value stems from identifying, building, or defending barriers to entry. — Source: Tianpan

Part 6: Management and Capital Allocation

- On Industry vs. Management: "When a management with a good reputation meets an industry with a bad reputation, it is invariably the reputation of the industry that survives." — Source: MOI Global

- On the Limits of Leadership: Management cannot sustain high profitability indefinitely against determined competition unless the business has structural barriers to entry. — Source: Marcellus Investment Managers

- On Double-Counting Value: Paying a premium multiple for "great management" often results in double-counting, as the management's value should already be reflected in the company's earnings power. — Source: MOI Global

- On Capital Distribution: "The management capability of allocating that capital plays a vital role." — Source: Substack

- On Operational Skill: The first pillar of management skill is the efficient operation of the existing business model. — Source: Medium

- On Financing: The second pillar of management skill is securing efficient financing to optimize the cost of capital. — Source: Medium

- On Intelligent Expansion: The third pillar is intelligent expansion, specifically limiting growth initiatives to areas that directly leverage existing competitive advantages. — Source: Medium

- On Human Resources: The fourth pillar is human resource planning, ensuring the organizational structure tightly supports operational effectiveness. — Source: Medium

- On Franchise Growth: When assessing a protected franchise, investors should focus on management's specific track record of making the earnings from that franchise grow. — Source: MOI Global

Part 7: Markets, Cycles, and Forecasting

- On Macro Forecasting: "There are a few things I dismiss and a few I believe in thoroughly. The former include economic forecasts, which I think don't add value." — Source: Goodreads

- On Market Psychology: "There are no bad days in the market. When the market is down, you’ve got bargains, and it’s lovely to think of what you are buying at low prices." — Source: Scribd

- On Bull Markets: "When the market is up, the bargains have gone, but you’re rich." — Source: AZ Quotes

- On Expectations: "In a tough environment, one of the things you may have to adjust is your expectations. There are stocks out there that won’t return the 10 to 11 percent you’re used to, but they will do better than the 6 to 7 percent you’re looking at." — Source: Columbia News

- On Economic Cycles: While timing economic forecasts is useless, understanding cycles and the need to prepare for them is foundational to managing risk. — Source: Goodreads

- On Navigating Cycles: Knowing where you are in a cycle and what that implies for the future is fundamentally different from trying to predict the exact timing and shape of the move. — Source: Goodreads

- On Hidden Risks: "It turns out the most dangerous times are when nobody thinks there's any danger, and those are the times where derivatives are cheapest." — Source: The Motley Fool

- On Structural Problems: Forecasting indicators like unemployment using past statistical patterns is flawed if it ignores underlying structural problems in the economy. — Source: Advisor Perspectives

- On Long-Term Commodities: "In the long run, everything is a toaster." — Source: QuoteFancy

Part 8: Macroeconomics and Globalization

- On the Threat of Globalization: "Globalization: n. the irrational fear that someone in China will take your job." — Source: Advisor Perspectives

- On Overselling Global Forces: The impact of globalization is frequently exaggerated; domestic factors remain the primary drivers of economic stability and growth. — Source: Roosevelt Institute

- On Global Dominance: "Whenever you think of one force dominating the world, it's never that simple." — Source: Forbes

- On the Death of Manufacturing: The decline of global manufacturing as an employment driver has led to a necessary shift toward services and the "return of the local" economy. — Reference: MOI Global transcript on manufacturing, services, and local markets

- On Diminishing Scale Advantages: As markets become increasingly global, the traditional economies of scale that protected incumbent national firms tend to diminish in effectiveness. — Source: MOI Global

- On Productivity Shocks: When massive productivity gains occur in sectors like manufacturing without matching demand, the structural mismatch creates severe economic slowdowns. — Source: NFRD Blog

- On Information Asymmetry: "Whenever information is imperfect – that is, always – markets are inefficient; hence the need for government action." — Source: Wikiquote

- On the Learning Society: Broad economic growth and development are best achieved by fostering a "learning society" where information and technological progress are widely distributed. — Source: Columbia University Press

- On Defining a Healthy Economy: A truly healthy economy is not just measured by total output, but by its structural capacity to provide sufficient, stable employment for its population. — Source: NFRD Blog