Campbell Harvey is a finance professor at Duke University best known for establishing that the inverted yield curve is a reliable leading indicator of economic recessions. Beyond macroeconomics, his research focuses on exposing flawed statistical practices in quantitative investing and evaluating the mechanics of decentralized finance. This collection synthesizes his views on identifying false discoveries in asset pricing, the practical limitations of inflation hedges, and the structural shifts brought by blockchain technology.

Part 1: The Yield Curve and Economic Forecasting

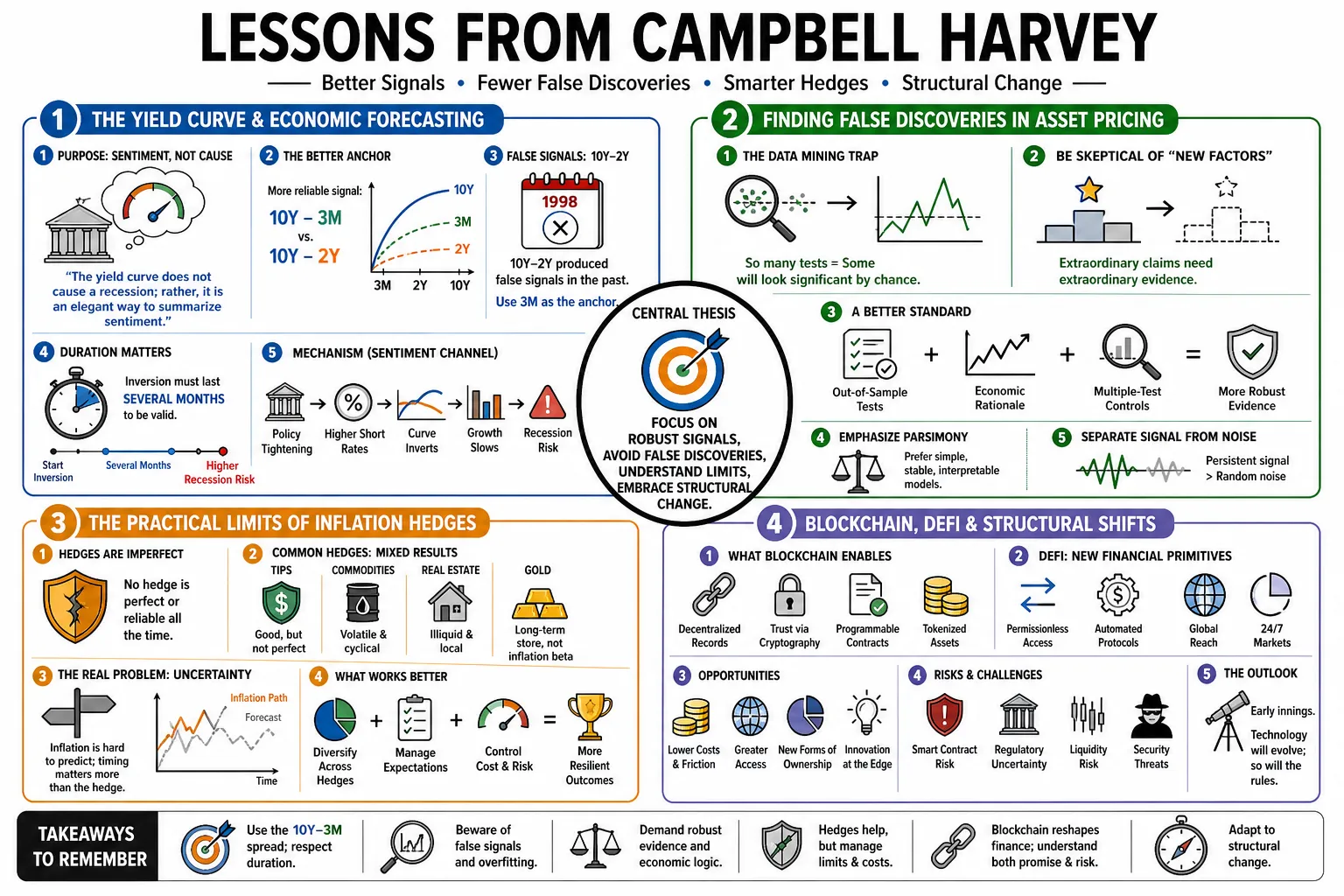

- On the Yield Curve's Purpose: "The yield curve does not cause a recession; rather, it is an elegant way to summarize sentiment." — Source: Duke University

- On Specific Indicators: "While commentators focus on the 10-year and 2-year Treasury spread, the more reliable signal comes from the spread between the 10-year note and the 3-month bill." — Source: Blockworks

- On False Signals: "The 10-year to 2-year spread has produced false signals in the past, notably in 1998, which is why the 3-month bill is the correct anchor." — Source: Blockworks

- On Duration of Inversion: "For the yield curve signal to be considered valid, it must remain inverted for a full quarter, filtering out momentary market noise." — Source: Duke University

- On Predictive Track Record: "The 10-year and 3-month inversion has an unblemished track record, correctly predicting the last eight recessions without a false signal since the 1960s." — Source: CFA Institute

- On Self-Fulfilling Prophecies: In Duke Today, Harvey says the yield curve does not itself cause a recession, but public awareness of the signal can change behavior: firms may delay investment and consumers may save more, slowing growth while reducing hard-landing risk. — Reference: Duke Today Q&A on yield-curve warnings, behavior, and risk management

- On Economic Context: "The yield curve is a powerful tool, but it must be interpreted within the current economic context, including Federal Reserve policy and labor market strength." — Source: Business Insider

- On Corporate Risk Management: "When the curve inverts, it is a clear signal for corporations to delay major capital expenditures and build a cash cushion." — Source: Duke University

- On Inflation's Impact: "High inflation can distort the yield curve's signal, as central banks artificially hold short-term rates high to cool the economy." — Source: Business Insider

- On Market Sentiment: "An inverted curve fundamentally reflects investors' collective expectations that future economic growth and inflation will be lower than they are today." — Source: University of Wisconsin

Part 2: Decentralized Finance (DeFi)

- On Financial Inefficiency: "A centralized financial system has many inefficiencies. Perhaps the most egregious example is the credit card interchange rate that causes consumers and small businesses to lose up to 3 percent of a transaction's value." — Source: Goodreads

- On Settlement Times: "Time is wasted in the two days it takes to settle a stock transaction. In the Internet age, this seems utterly implausible." — Source: Goodreads

- On Eliminating Middlemen: "In decentralized finance, the algorithm basically takes the place of the functioning of a bank or a broker." — Source: The Big Picture

- On Financial Inclusion: "DeFi has the potential to provide essential financial services to the 1.7 billion people worldwide who are currently unbanked." — Source: Compound Maven

- On Legacy Infrastructure: "The legacy financial infrastructure is characterized by centralized control, limited access, opacity, and a severe lack of interoperability." — Source: Duke University

- On Smart Contracts: "Smart contracts enforce the rules of the financial transaction mathematically, removing the need for trust in a centralized counterparty." — Source: Goodreads

- On Rent-Seeking: "By moving to peer-to-peer interactions, the DeFi system eliminates the rent-seeking behavior that has historically enriched traditional financial intermediaries." — Source: The Big Picture

- On Innovation Speed: "The open-source nature of DeFi allows developers to rapidly iterate and compose new financial products, creating a speed of innovation traditional banks cannot match." — Source: Rational Reminder

- On the Future of Banks: "Traditional banks must adapt to blockchain technology or risk becoming obsolete as decentralized protocols offer superior yield and lower friction." — Source: Goodreads

Part 3: The Factor Zoo and Data Mining

- On Factor Proliferation: "The academic literature is overwhelmed by an unmanageable and often redundant collection of potential market drivers, creating a 'factor zoo'." — Source: ETF Stream

- On False Discoveries: "With enough data, it is easy to find patterns that look significant in a backtest but are actually the result of random noise or data mining." — Source: ETF Stream

- On Statistical Thresholds: "Because so many researchers are testing the same data, the conventional statistical threshold of a 2.0 t-statistic is far too low." — Source: Two Centuries

- On Raising the Bar: "To account for multiple testing and selection bias, the bar for statistical significance in asset pricing should be raised to t-statistics above 3.0." — Source: CXO Advisory

- On Publication Bias: "Academic journals have a tendency to publish positive results, encouraging researchers to keep mining data until they find a factor that appears to work." — Source: ETF Stream

- On Factor Redundancy: "Many factors in the zoo are essentially different ways of measuring the exact same underlying risk or market anomaly." — Source: Chicago Booth

- On Backtested Returns: "A high backtested return is not proof of future success; it is often just evidence that a computer searched long enough to find a historical coincidence." — Source: Duke University

- On Economic Intuition: "Before accepting any new factor, investors must demand a plausible economic mechanism, not just a strong statistical correlation." — Source: Robeco

- On Historical Data: "The stock market simply does not have enough independent historical data to validate the hundreds of factors currently claimed by academic literature." — Source: CXO Advisory

- On Multi-Factor Models: "While many individual factors may be noise, the approach of using multi-factor models remains valuable if applied with greater statistical discipline." — Source: Chicago Booth

Part 4: Inflation Hedging and Commodities

- On Commodities as Hedges: "Commodities are, at best, an inconsistent and often tenuous hedge against unexpected inflation." — Source: NBER

- On Passive Commodity Exposure: "Long-only passive investments in commodity futures have historically been questionable as reliable inflation hedges for long-term investors." — Source: Duke University

- On Tactical Implementation: "The success of a commodity-based inflation hedge often depends on tactical implementation, such as active management and momentum, rather than a simple buy-and-hold approach." — Source: NBER

- On The Golden Dilemma: "While gold may preserve purchasing power over centuries, it is an unreliable hedge for the short- to medium-term horizons relevant to most investors." — Source: Quantpedia

- On Gold's Volatility: "Gold's volatility is comparable to that of equities, making it a poor tool for protecting against inflation in standard investment timeframes." — Source: Quantpedia

- On Gold Valuation: "Investors must look at the gold-to-CPI ratio; if gold is already expensive relative to its long-term average, its potential to act as a buffer against inflation is diminished." — Source: Wealth Professional

- On the Common Sense Fallacy: "The popular narrative that real assets always provide reliable protection against inflation is a fallacy that breaks down under rigorous historical scrutiny." — Source: Quantpedia

- On Alternative Hedges: "Investors are better served by looking at more sophisticated, tactical strategies—such as trend following—to manage inflation risk in a portfolio." — Source: Duke University

- On Commodity Diversity: "Commodities are a diverse asset class, and their hedging properties vary so significantly by type that broad index exposure often dilutes any specific inflation protection." — Source: Duke University

Part 5: Corporate Finance and Capital Allocation

- On Academic Theory vs. Practice: "There is a significant gap between the corporate finance methods taught in business schools and how Chief Financial Officers actually make capital budgeting decisions." — Source: RePEc

- On the CAPM in Practice: "While large firms frequently use NPV and the Capital Asset Pricing Model, smaller firms still heavily rely on simpler, flawed metrics like the payback period." — Source: Scribd

- On Emerging Market Risk: "Calculating the cost of capital in emerging markets often requires ad hoc approaches because global risk factors are far more complex than standard models assume." — Source: Duke University

- On Agency Costs: "Capital structure decisions, such as the strategic use of debt, can mitigate agency costs and influence shareholder value, especially in firms with complex ownership." — Source: ResearchGate

- On the CFO Survey: "Surveying CFOs directly reveals that behavioral factors and corporate culture play a much larger role in capital structure than textbook models suggest." — Source: RePEc

- On Financial Liberalization: "When emerging markets liberalize their financial sectors, the cost of capital typically falls, but local firms face increased exposure to global market volatility." — Source: Duke University

- On Investment Evaluation: "Rigorous, data-driven approaches to valuation are essential; relying solely on intuition or outdated spreadsheet models destroys shareholder wealth." — Source: Duke University

- On Global Risk Premiums: "Time-varying risk premiums mean that a static hurdle rate for corporate investments will inevitably lead to misallocation of capital across market cycles." — Source: Duke University

- On Corporate Debt: "Debt acts as a disciplinary mechanism for management in emerging markets, forcing them to generate cash flows rather than engage in empire-building." — Source: ResearchGate

Part 6: Machine Learning in Finance

- On Machine Learning Pitfalls: "While machine learning is powerful, it can exacerbate the risk of false discoveries in finance if not applied with a strict, rigorous scientific protocol." — Source: Top1000Funds

- On the Blessings of Dimensionality: "The high dimensionality of machine learning models provides more degrees of freedom, which easily leads to capturing spurious patterns if researchers aren't careful." — Source: UQAM

- On Scientific Outlook: "Applying machine learning to asset pricing requires a scientific outlook and disciplined validation to prevent it from becoming a sophisticated mechanism for finding false gold." — Source: Forbes

- On Markowitz and ML: "Integrating forecasting and optimization stages in portfolio selection is essential; the standard two-step approach often leads to problematic outcomes when using ML." — Source: Duke University

- On Overfitting: "Machine learning models are exceptional at fitting historical financial data perfectly, which is precisely why they often fail spectacularly in out-of-sample trading." — Source: Research Affiliates

- On Black Boxes: "The opacity of machine learning models makes them dangerous in finance; if you cannot economically explain why a model is taking a trade, you shouldn't deploy it." — Source: Duke University

- On Cross-Validation: "Standard cross-validation techniques from computer science often fail in finance due to the severe time-series dependency and non-stationarity of market data." — Source: Hudson & Thames

- On Data Quality: "An advanced machine learning algorithm fed with noisy, unstructured financial data will simply learn the noise faster and more efficiently than a linear regression." — Source: Duke University

- On Strategy Decay: "Machine learning strategies decay significantly faster than traditional economic factors because they often capture transient market micro-structure anomalies rather than fundamental risks." — Source: NBER

Part 7: Cryptocurrencies and Blockchain

- On Bitcoin vs. Gold: In Wharton's Future of Finance discussion, Harvey treats Bitcoin as a risky store of value: its supply is algorithmic, but it is untested, highly volatile, and roughly four times as volatile as the S&P 500, making it unreliable as a corporate reserve. — Reference: Wharton transcript on Bitcoin volatility and risky store-of-value limits

- On Tokenization: In Wharton's transcript, Harvey says tokenization makes the idea of money more flexible: future wallets could pay with tokens linked to gold, equities, or real estate rather than only fiat currency. — Reference: Wharton transcript on tokenizing assets such as gold, equities, and real estate

- On the Digital Gold Narrative: Harvey tempers the digital-gold narrative in Wharton: even if Bitcoin has performed well as a risky store of value, he calls it untested, highly volatile, and potentially momentum-driven rather than a dependable hedge. — Reference: Wharton transcript on Bitcoin as an untested, volatile store of value

- On Cryptographic Trust: "Blockchain shifts the burden of trust from centralized institutions with human biases to decentralized cryptographic proofs and immutable ledgers." — Source: Rational Reminder

- On Stablecoins: In Wharton, Harvey says centralized stablecoins such as USDC and Tether are widely used inside decentralized finance, calls stablecoins the most successful innovation in the space to date, and expects yield-bearing tokenized bonds to improve the model. — Reference: Wharton transcript on centralized stablecoins and yield-bearing tokenized bonds

- On Institutional Adoption: "Institutional adoption of crypto will not happen through direct exposure to volatile tokens, but through the integration of blockchain infrastructure into backend settlement processes." — Source: Knowledge at Wharton

- On Crypto Portfolios: "Adding a small allocation of cryptocurrency to a diversified portfolio can improve the Sharpe ratio purely due to its historically low correlation with traditional assets, though this correlation is rising." — Source: Rational Reminder

- On Programmable Money: "The invention of programmable money allows for conditional transactions that execute automatically, eliminating counterparty risk without requiring a legal mediator." — Source: The Big Picture

- On Regulatory Clarity: "Innovation in the blockchain space is severely hindered by regulation by enforcement; the industry needs clear, legislative guidelines to realize its economic potential." — Source: Rational Reminder

- On the Bitcoin Experiment: "Gifting students Bitcoin was not about speculation; it was a pedagogical tool to force them to understand public and private keys, wallets, and on-chain transactions." — Source: The Big Picture

Part 8: Backtesting Protocols and False Discoveries

- On Evaluating Managers: "When evaluating portfolio managers, we must address the trade-off between Type I false positive and Type II false negative errors to distinguish skill from luck." — Source: Duke University

- On Backtesting Protocols: "The financial industry desperately needs a strict backtesting protocol; without guidelines, practitioners will continually fall victim to snooping bias." — Source: Duke University

- On Snooping Bias: "If you test twenty different trading strategies on the same dataset, one will look brilliant purely by chance; this snooping bias is the most pervasive error in quantitative finance." — Source: Alpha Architect

- On Out-of-Sample Testing: "True out-of-sample testing requires completely locking down a strategy's parameters before evaluating it on new data, a practice that is rarely followed in industry." — Source: Man Group

- On Transaction Costs: "Many academic anomalies completely disappear once realistic transaction costs, market impact, and shorting constraints are incorporated into the backtest." — Source: CXO Advisory

- On the Multiple Testing Problem: "The multiple testing problem means that as the number of researchers mining a dataset increases, the statistical significance of any new discovery mathematically decreases." — Source: WisdomTree

- On Haircutting Sharpe Ratios: "Practitioners should routinely apply a 'haircut' to backtested Sharpe ratios—often reducing them by half—to estimate a strategy's realistic live performance." — Source: Risk.net

- On Institutional Incentives: "Asset management firms are incentivized to launch products based on over-optimized backtests because they raise assets, even if the underlying signal is entirely false." — Source: Duke University

- On the Scientific Method: "Finance must adopt the rigorous replication standards found in physics and medicine; otherwise, empirical asset pricing will remain more art than science." — Source: ML Factor