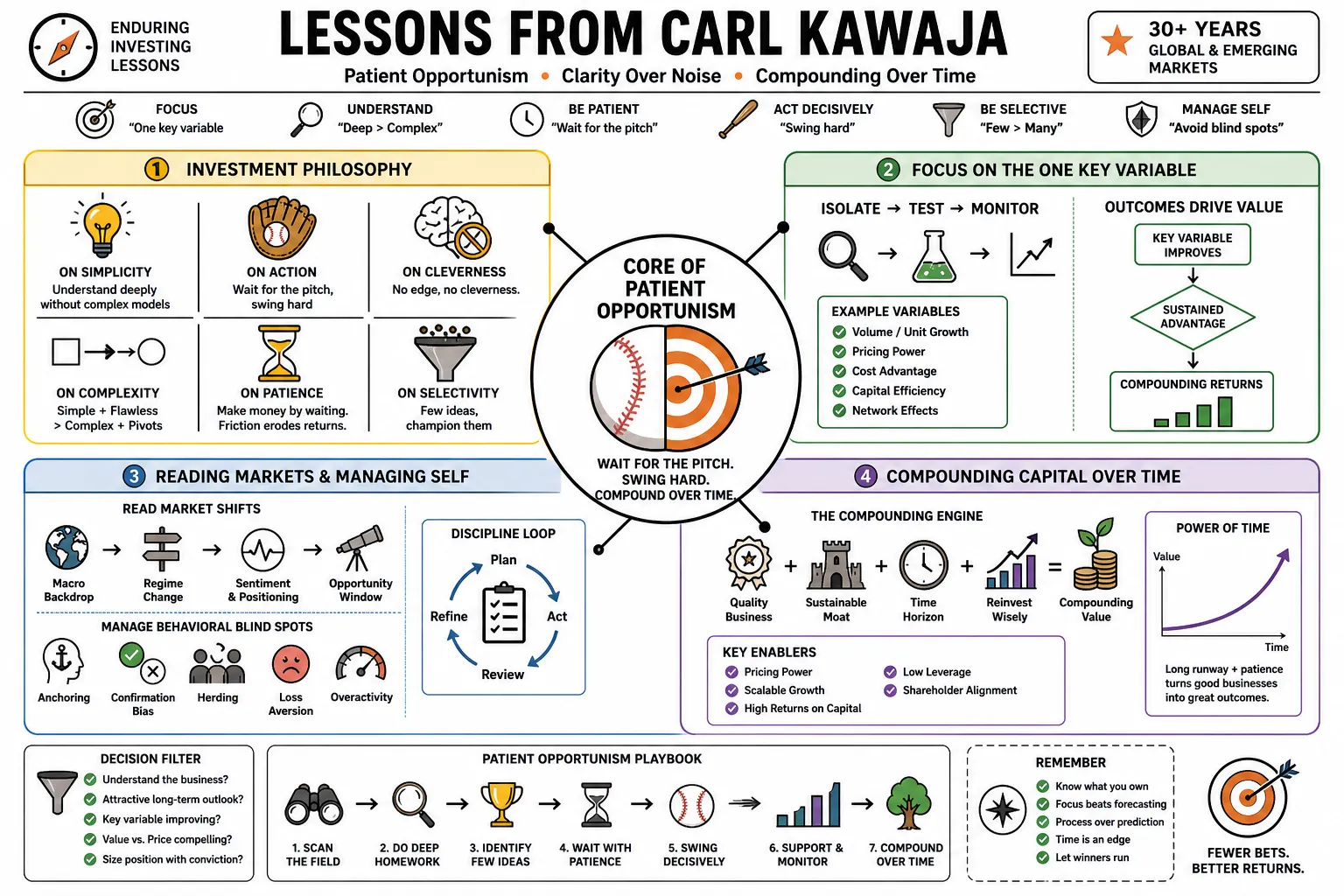

Lessons from Carl Kawaja

Carl Kawaja is a Capital Group portfolio manager who has invested in global and emerging markets for over thirty years. His approach relies on patient opportunism and isolating the single most important variable that drives a business. This collection covers his methods for managing behavioral blind spots, reading market shifts, and compounding capital.

Part 1: The Core of Patient Opportunism

- On Simplicity: "The best investments usually come from businesses you understand deeply without needing complex models." — Source: [Invest Like the Best]

- On Action: "Patient opportunism means waiting for the pitch, but being ready to swing hard when it finally crosses the plate." — Source: [Capital Group Perspectives]

- On Cleverness: "Trying to be overly clever in markets where you have no distinct informational edge is a recipe for underperformance." — Source: [Advisor Analyst]

- On Complexity: "A simple business model executed flawlessly is vastly superior to a complex model that requires constant pivots." — Source: [Invest Like the Best]

- On Patience: "You make money by waiting, not merely by buying and selling. The friction of constant activity eats into long-term returns." — Source: [Morningstar]

- On Selectivity: "You do not need to have an opinion on every stock or every sector. Only play in the areas where you have genuine insight." — Source: [The Meb Faber Show]

- On Edge: "Your edge isn't usually knowing something nobody else knows; it's caring about something for a longer duration than the market is willing to." — Source: [Capital Group Perspectives]

- On Consistency: "It is better to be consistently good than occasionally brilliant." — Source: [Invest Like the Best]

- On Market Noise: "The market generates a tremendous amount of daily noise. The investor's primary job is to aggressively filter it out." — Source: [Morningstar]

Part 2: Identifying the "One Thing"

- On The Key Variable: "Usually there’s only one thing that’s important. Where there’s magic is when there’s one thing that’s important to get right, you understand what that one thing is better than other people, and you’ve come to a different conclusion." — Source: [Advisor Analyst]

- On Distraction: "When analyzing a company, there are fifty variables you could track. If you track them all, you lose sight of the one that actually drives the cash flow." — Source: [Invest Like the Best]

- On Consensus: "If your view on the 'one thing' matches the market's view exactly, the stock is likely fairly priced." — Source: [The Meb Faber Show]

- On Information Overload: "More information does not equate to higher conviction; it often dilutes your focus from the core thesis." — Source: [Capital Group Perspectives]

- On Frameworks: "Find the bottleneck of the industry. Whoever controls the bottleneck usually captures the economics." — Source: [Morningstar]

- On Semiconductors: "In semiconductors, the 'one thing' is often the sheer scale of manufacturing complexity and the moat that scale creates." — Source: [The Meb Faber Show]

- On Management: "Sometimes the single most important variable is the specific capital allocation track record of the CEO." — Source: [Invest Like the Best]

- On Differing Conclusions: "It is insufficient to know what matters. You have to be right, and the crowd has to be temporarily wrong." — Source: [Capital Group Perspectives]

- On Thesis Drift: "If the 'one thing' changes or breaks, you must exit. Do not invent a second thing to justify holding the position." — Source: [Morningstar]

Part 3: Managing Biases and Limitations

- On Self-Awareness: "The main difference between early in my career and now is that I’m much more receptive to my own biases and limitations." — Source: [Columbia Business School]

- On Blind Spots: "I’m more comfortable sitting with my own blind spots and trying to manage through them rather than pretending they don't exist." — Source: [Columbia Business School]

- On Changing Your Mind: "The hardest thing in investing is abandoning a thesis you have publicly or privately defended for years." — Source: [Invest Like the Best]

- On Overconfidence: "The market is a highly efficient mechanism for transferring wealth from the arrogant to the humble." — Source: [The Meb Faber Show]

- On Experience: "Experience doesn't mean you stop making mistakes. It means you recognize the shape of the mistake sooner and correct it faster." — Source: [Capital Group Perspectives]

- On Team Dynamics: "You need people around you who view the world differently to actively short-circuit your confirmation bias." — Source: [Morningstar]

- On Conviction vs. Stubbornness: "There is a very fine line between holding true to a long-term conviction and being pigheaded about a broken thesis." — Source: [Invest Like the Best]

- On Accepting Losses: "Tolerating failure is a prerequisite for long-term success. If you can't stomach being wrong, you won't survive the market." — Source: [Advisor Analyst]

- On Intellectual Honesty: "Write down why you are buying a stock. If you don't, your memory will revise history to make you look smarter when things go wrong." — Source: [Capital Group Perspectives]

- On Evolution: "An investor must continually adapt. The strategies that worked beautifully in the last decade will likely fail in the next." — Source: [The Meb Faber Show]

Part 4: Navigating Tangible and Intangible Assets

- On Regime Change: "There comes a time to trade the intangible for the tangible. We are entering an era that requires physical infrastructure." — Source: [Firstlinks]

- On Software Dominance: "For years, software ate the world and commanded the highest premiums. But software requires hardware, power, and physical commodities to run." — Source: [The Meb Faber Show]

- On Commodities: "The transition to electric vehicles and new infrastructure demands massive amounts of nickel, copper, and physical materials that software cannot code into existence." — Source: [Invest Like the Best]

- On Valuation Shifts: "Tangible asset companies have been starved of capital for a decade, creating a structural supply shortage that benefits long-term holders." — Source: [Capital Group Perspectives]

- On Energy Needs: "The rise of artificial intelligence is fundamentally a story about power consumption and the physical grid." — Source: [The Meb Faber Show]

- On Scarcity: "Intangible assets can be duplicated with near-zero marginal cost. Tangible assets face real-world physical constraints and scarcity." — Source: [Morningstar]

- On Capital Cycles: "We are rotating out of a cycle that rewarded asset-light models into one that will heavily reward those who own productive hard assets." — Source: [Advisor Analyst]

- On Supply Chains: "Global supply chain fragility has reminded the market that physical proximity and manufacturing capacity are actual competitive advantages." — Source: [Firstlinks]

- On Inflation Defense: "Tangible assets traditionally provide a more reliable defense against sticky inflation than purely digital business models." — Source: [Capital Group Perspectives]

Part 5: Building and Holding Conviction

- On Deep Research: "Conviction does not come from reading the same analyst reports as everyone else. It comes from primary research and understanding the granular details." — Source: [Invest Like the Best]

- On Volatility: "If you truly understand a business, a 20% drop in the stock price is an opportunity, not a reason to panic." — Source: [Morningstar]

- On Time Arbitrage: "The market's inability to look past the next two quarters is the structural advantage for anyone willing to look out three to five years." — Source: [Capital Group Perspectives]

- On Contrarianism: "Being a contrarian for the sake of it is foolish. You have to be an accurate contrarian." — Source: [Advisor Analyst]

- On Sizing: "Position sizing should be entirely dependent on the depth of your conviction, not the market capitalization of the company." — Source: [The Meb Faber Show]

- On Holding: "The real money is made in the holding, sitting quietly while the company executes its plan and compounds capital." — Source: [Invest Like the Best]

- On Trusting Management: "You can have a great thesis, but if you do not trust the management team to execute it and treat shareholders fairly, the thesis is worthless." — Source: [Capital Group Perspectives]

- On Valuation: "Valuation is a result, not a thesis. The thesis is the underlying business dynamic that will force the valuation to change over time." — Source: [Advisor Analyst]

- On Doubt: "True conviction requires you to deeply understand the bear case. If you cannot articulate the short seller's argument better than they can, you don't know the stock well enough." — Source: [Morningstar]

- On Selling: "The hardest decision isn't buying. It's knowing when a stock has reached its full potential and having the discipline to sell and move on." — Source: [Advisor Analyst]

Part 6: The Mechanics of Long-Term Compounding

- On the Math of Growth: "Compounding is the most powerful force in investing, but it requires an environment free of catastrophic interruptions." — Source: [Invest Like the Best]

- On Moats: "A competitive advantage is only a true moat if it allows the business to earn returns above its cost of capital for a decade or more." — Source: [Capital Group Perspectives]

- On Reinvestment Rates: "The ideal business generates significant free cash flow and has an internal mechanism to reinvest that cash at equally high rates of return." — Source: [Morningstar]

- On Survival: "To compound over decades, the first rule is survival. Avoid excessive debt and structural risks that can take you to zero." — Source: [The Meb Faber Show]

- On Growth Trajectories: "Growth is rarely linear. A great company will have periods of consolidation that shake out the weak holders." — Source: [Advisor Analyst]

- On Capital Allocation: "Over a twenty-year period, the CEO's capital allocation decisions will define the shareholder return more than the underlying product." — Source: [Invest Like the Best]

- On Market Cycles: "A compounding machine doesn't care whether we are in a bull or bear market; it just keeps generating and reinvesting cash." — Source: [Capital Group Perspectives]

- On Dividends vs. Growth: "Dividends are great, but a company that can reinvest its cash internally at 20% should never pay a dividend." — Source: [Morningstar]

- On Patience and Returns: "The greatest returns often occur in years seven through ten of holding a stock, a duration most modern investors never reach." — Source: [The Meb Faber Show]

Part 7: Adapting to Market Regimes

- On Macroeconomics: "You don't need to be a macroeconomist to invest, but you do need to recognize when the foundational rules of the market are shifting." — Source: [The Meb Faber Show]

- On Interest Rates: "Zero percent interest rates disguised a lot of bad business models. Normalizing rates reveals who actually generates cash." — Source: [Capital Group Perspectives]

- On Globalization: "The unspooling of globalization changes the margin structure of multinationals. Supply chain resilience is now prioritized over pure cost efficiency." — Source: [Invest Like the Best]

- On Tariffs: "Trade barriers act as a tax on the consumer, but they also create protected domestic champions that investors can identify and own." — Source: [Morningstar]

- On Inflationary Eras: "In an inflationary regime, pricing power is the single most important metric. If a company cannot raise prices, its margins will be destroyed." — Source: [Advisor Analyst]

- On Geopolitics: "Geopolitical risk is often mispriced. The market either ignores it completely or overreacts to it in the short term." — Source: [The Meb Faber Show]

- On Market Leadership: "The companies that led the last bull market are rarely the ones that lead the next one. You have to be willing to look in new sectors." — Source: [Capital Group Perspectives]

- On Emerging Markets: "Demographics in emerging markets offer a structural tailwind, but you must demand a higher margin of safety due to governance risks." — Source: [Invest Like the Best]

- On Flexibility: "The rigid investor breaks when the regime changes. The flexible investor adapts their playbook to fit the new reality." — Source: [Morningstar]

- On Opportunity Cost: "Every dollar deployed is a dollar you cannot deploy tomorrow when a better opportunity might present itself." — Source: [Advisor Analyst]

Part 8: Evaluating Emerging Technologies and Trends

- On Artificial Intelligence: "AI will permeate every industry, but the immediate beneficiaries are the companies building the foundational hardware and infrastructure." — Source: [The Meb Faber Show]

- On Semiconductor Dominance: "Foundries like TSMC possess a technical moat and manufacturing scale that is nearly impossible for competitors to replicate from scratch." — Source: [Invest Like the Best]

- On Healthcare Innovation: "New weight-loss drugs represent more than a pharmaceutical breakthrough; they trigger ripple effects across consumer behavior, food consumption, and broader healthcare costs." — Source: [Capital Group Perspectives]

- On Hype Cycles: "It is easy to overpay for a transformational technology. The technology can change the world while the stock still loses you money." — Source: [Morningstar]

- On Consumer Shifts: "The legalization and normalization of sports gambling is shifting discretionary consumer spend in ways the market is still mapping out." — Source: [The Meb Faber Show]

- On Second-Order Effects: "The most lucrative investments in a new technology are often found in the second-order derivatives—the companies supplying the tools, not the end product." — Source: [Invest Like the Best]

- On Legacy Disruption: "Incumbents rarely disrupt themselves. You have to look for the companies that have nothing to lose by breaking the old business model." — Source: [Advisor Analyst]

- On Data as an Asset: "The companies that own unique, proprietary datasets will be the ultimate winners in an AI-driven economy, as models become commoditized." — Source: [Capital Group Perspectives]

- On Enduring Value: "No matter the technology, the fundamental question remains: does this create undeniable value for the customer, and can the company capture a portion of that value?" — Source: [The Meb Faber Show]