Lessons from Charles Ellis

Charles Ellis founded Greenwich Associates and wrote Winning the Loser's Game, arguing that modern investing is defined by avoiding mistakes rather than picking brilliant stocks. This collection outlines his case for market efficiency, behavioral discipline, and why doing less usually yields higher net returns.

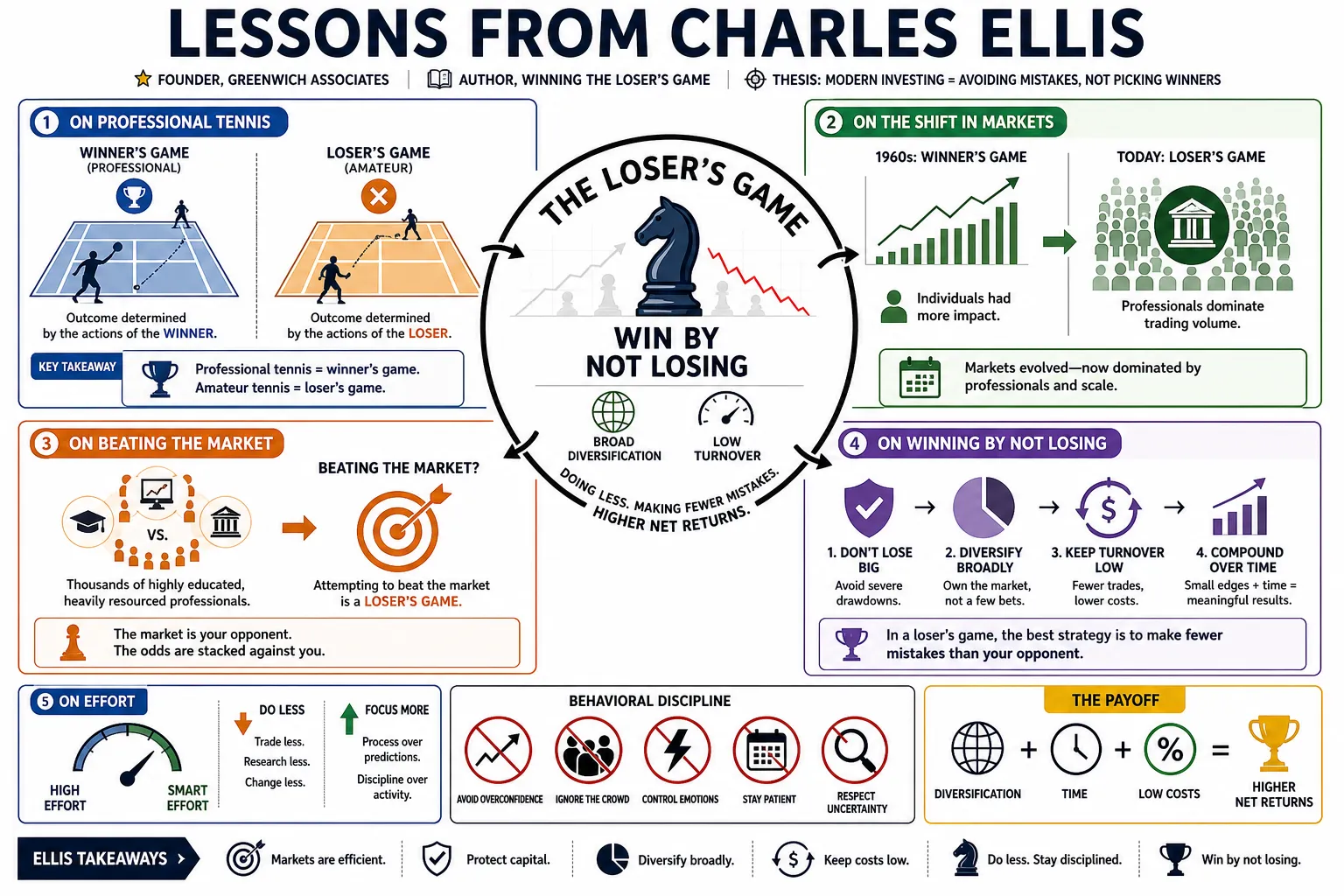

Part 1: The Loser's Game

- On Professional Tennis: "Professional tennis is a winner’s game—the outcome is determined by the actions of the winner. Amateur tennis is a loser’s game—the outcome is determined by the actions of the loser." — Source: [Winning the Loser's Game]

- On the Shift in Markets: "The stock market transitioned from a winner’s game in the 1960s to a loser’s game today, simply because the professionals now dominate the trading volume." — Source: [The Financial Analysts Journal]

- On Beating the Market: "Attempting to beat the market is a loser’s game because the market is essentially composed of thousands of highly educated, heavily resourced professionals competing against each other." — Source: [Rational Reminder Episode 244]

- On Winning by Not Losing: "In a loser's game, the best strategy is to make fewer mistakes than your opponent, which in investing translates to broad diversification and low turnover." — Source: [Winning the Loser's Game]

- On Effort vs. Outcome: "In a loser's game, trying harder often leads to worse outcomes, as increased activity generates friction and errors." — Source: [Masters in Business]

- On Golf and Investing: "Like a high-handicap golfer trying to hit a spectacular shot out of the woods, active investors compound their problems by trying to be heroic instead of getting back on the fairway." — Source: [Winning the Loser's Game]

- On the Paradox of Skill: "The collective skill of professional investors has risen so high that the variance in their performance has shrunk, making it nearly impossible for any single manager to consistently exploit the others." — Source: [The Index Revolution]

- On the Illusion of Control: "Investors falsely believe they can control outcomes in the market, when in reality they are playing a game where the environment dictates the baseline results." — Source: [Morningstar The Long View]

- On the Core Strategy: "The great secret for success in long-term investing is to avoid serious losses." — Source: [Winning the Loser's Game]

Part 2: Market Efficiency and Competition

- On the Opponent: "When you buy a stock, the person selling it to you is likely a team of specialists at a major institution who spend all day studying that specific sector." — Source: [The Index Revolution]

- On the Speed of Information: "Institutional investors now receive and process information instantly, eliminating the informational edge that individual investors once possessed." — Source: [Rational Reminder Episode 244]

- On the Wisdom of the Crowd: "The stock market is not a monolith; it is a continuously updated consensus of the smartest minds in finance voting with real money." — Source: [WealthTrack Interview]

- On Trading Volume: "Today, over 95 percent of all trading is done by institutional professionals, compared to less than 10 percent in the mid-20th century." — Source: [CFA Institute]

- On Information Parity: "Because regulations and the internet mandate equal access to corporate information, finding a proprietary edge in public data is effectively impossible for individuals." — Source: [The Index Revolution]

- On Active Management Success Rates: "Over a decade or more, the overwhelming majority of active mutual funds fail to outpace their relevant benchmarks after accounting for fees." — Source: [Winning the Loser's Game]

- On the Zero-Sum Game: "Before fees, investing is a zero-sum game; after fees and taxes, active investing becomes a negative-sum game for the aggregate participant." — Source: [The Index Revolution]

- On the Limits of Hard Work: "A manager can work 80 hours a week and still underperform, because their competitors are equally dedicated and well-equipped." — Source: [Masters in Business]

- On Institutional Dominance: "The market is no longer a place where experts take advantage of amateurs; it is a place where experts trade with other experts, driving prices to fair value almost instantly." — Source: [Rational Reminder Episode 244]

Part 3: The Indexing Advantage

- On the Purpose of Indexing: "Indexing is not about settling for average; it is about guaranteeing that you capture the market's return, which historically places you ahead of most active investors." — Source: [The Index Revolution]

- On Vanguard: "Vanguard is a marvelous gift to the public, functioning as a steady, reliable mechanism for transferring market returns directly to individuals at cost." — Source: [Morningstar The Long View]

- On Simplicity: "A single, broad-market index fund provides all the diversification an equity investor needs without the complexity of managing multiple active managers." — Source: [Winning the Loser's Game]

- On Predictability: "You cannot predict which active manager will win over the next decade, but you can predict with near certainty that an index fund will deliver the market return minus a tiny fee." — Source: [Bogleheads Conference]

- On Tax Efficiency: "Index funds generate far fewer taxable events than active funds because they rarely sell holdings, allowing capital to compound uninterrupted." — Source: [The Index Revolution]

- On Manager Risk: "Buying an index fund eliminates the risk of a star manager retiring, changing styles, or losing their touch." — Source: [WealthTrack Interview]

- On the Burden of Proof: "The burden of proof is entirely on the active manager to justify their existence, as the default option of indexing is mathematically superior for the aggregate." — Source: [Rational Reminder Episode 244]

- On Capital Allocation: "Indexing frees up an investor's time and mental energy to focus on asset allocation and savings rates, which actually drive long-term wealth." — Source: [Elements of Investing]

- On the Growth of Indexing: "The shift toward passive investing is not a fad; it is the rational response of a market that has finally recognized the structural disadvantage of active management." — Source: [CFA Institute]

Part 4: Time Horizon and Long-Term Investing

- On the Short Term vs. Long Term: "The average long-term experience in investing is never surprising, but the short term experience is always surprising." — Source: [IFA Transcript]

- On Time and Risk: "The probability of suffering a loss in a diversified equity portfolio approaches zero as your holding period extends past 15 or 20 years." — Source: [Winning the Loser's Game]

- On Market Volatility: "Treat market volatility as a natural feature of the system, not a bug that needs to be fixed or avoided through trading." — Source: [Elements of Investing]

- On Compounding: "The most powerful force in investing is time, and interrupting the compounding process through panic selling is the most expensive mistake you can make." — Source: [The Index Revolution]

- On Benign Neglect: "Benign neglect is the secret to long-term investing success." — Source: [Novel Investor]

- On Evaluating Performance: "Looking at portfolio performance every day or even every month is counterproductive; long-term money should be evaluated on long-term intervals." — Source: [Winning the Loser's Game]

- On Outliving the Bear: "A properly constructed portfolio will survive multiple bear markets, provided the investor has the time horizon to let prices recover." — Source: [Morningstar The Long View]

- On Patience: "Patience is the single most important behavioral trait for an investor, as it bridges the gap between current volatility and future returns." — Source: [WealthTrack Interview]

- On Life Expectancy: "Most investors underestimate their true time horizon by failing to account for how long their surviving spouse or heirs will need the capital." — Source: [Winning the Loser's Game]

Part 5: Avoiding Mistakes and Defensive Play

- On the Defensive Posture: "Even though most investors see their work as active, assertive, and on the offensive, the reality is and should be that stock and bond investing alike are primarily a defensive process." — Source: [Winning the Loser's Game]

- On the Permanence of Losses: "Large losses are forever, in investing, in teenage driving, and in fidelity. If you avoid large losses with a strong defense, the winnings will have every opportunity to take care of themselves." — Source: [Novel Investor]

- On Action Bias: "Doing nothing is often the mathematically correct decision, yet the financial industry is built on the false premise that constant action adds value." — Source: [Rational Reminder Episode 244]

- On Self-Inflicted Wounds: "The most severe damage to an individual's wealth is rarely caused by the market; it is caused by the investor's own poorly timed interventions." — Source: [The Index Revolution]

- On Margin of Safety: "A sound investment strategy must have enough margin of safety to survive the inevitable periods when everything goes wrong at once." — Source: [Winning the Loser's Game]

- On Overconfidence: "Believing you are smarter than the collective market is the first step toward a catastrophic portfolio error." — Source: [CFA Institute]

- On Saying No: "At least 80 percent of Capital's most important decisions have been 'No' decisions: active, carefully thought-through decisions not to take a specific action." — Source: [Capital: The Story of Long-Term Investment Excellence]

- On Complexity: "Avoid complex financial products that require a glossary to understand; opacity is usually a cloak for high fees and hidden risks." — Source: [Elements of Investing]

- On Market Timing: "Getting out of the market requires being right twice, when you sell and when you buy back in, which is statistically impossible to do consistently." — Source: [Winning the Loser's Game]

Part 6: Human Behavior and Psychology

- On Boredom: "If you go to the stock market because you want excitement, then sooner or later you will lose." — Source: [Novel Investor]

- On Mr. Market: "The mistake most people make is answering the door just because Mr. Market knocks. You don't have to let him in." — Source: [Novel Investor]

- On Bear Market Psychology: "It's absolute cockamamie crazy to sell stocks after they drop. Instead, you should say, 'Today there's a first-rate bargain and I'm buying'." — Source: [Novel Investor]

- On Greed and Fear: "The market cycle is driven by the oscillation between greed and fear, and the successful investor must cultivate the emotional discipline to ignore both." — Source: [Winning the Loser's Game]

- On the Illusion of Activity: "We are wired to believe that trying harder produces better results, but in investing, activity often subtracts value." — Source: [Elements of Investing]

- On Media Noise: "The financial media exists to sell advertising by generating anxiety and excitement, neither of which is helpful for managing a long-term portfolio." — Source: [Morningstar The Long View]

- On Peer Pressure: "It is psychologically painful to hold a boring index fund when your neighbor is bragging about a hot stock, but discipline requires ignoring the noise." — Source: [Rational Reminder Episode 244]

- On Past Performance: "Investors instinctively chase recent top-performing funds, precisely at the moment those funds are most likely to revert to the mean." — Source: [The Index Revolution]

- On Behavioral Coaching: "The most valuable role of a financial advisor is not picking stocks, but serving as a behavioral coach to prevent clients from making emotional errors during panics." — Source: [WealthTrack Interview]

- On Objectivity: "Emotional detachment is the ultimate advantage; you must view your portfolio as a mechanism for funding your future, not a reflection of your ego." — Source: [Winning the Loser's Game]

Part 7: Fees, Costs, and Taxes

- On the Impact of Fees: "A 1% annual fee might sound small, but compounded over an investing lifetime, it will confiscate a massive portion of your terminal wealth." — Source: [Elements of Investing]

- On the Math of Active Management: "Active management fees are not charged on the total return; they are charged on the incremental return above the index, making the effective fee astronomically high." — Source: [The Index Revolution]

- On Wall Street's Business Model: "The financial services industry is designed to transfer wealth from the client to the manager through a constant drip of fees, commissions, and hidden costs." — Source: [CFA Institute]

- On Hidden Friction: "Transaction costs and bid-ask spreads create an invisible drag on actively managed portfolios that is rarely fully understood by the end investor." — Source: [Winning the Loser's Game]

- On Tax Drag: "Taxes on short-term capital gains and dividends in high-turnover funds are the largest single expense for many investors, yet they are excluded from the expense ratio." — Source: [The Index Revolution]

- On Keeping What You Earn: "In investing, you get exactly what you don't pay for; lowering your costs is the only guaranteed way to increase your net return." — Source: [Elements of Investing]

- On Asset-Based Fees: "Paying an advisor a percentage of assets under management only makes sense if the advisor provides comprehensive financial planning and behavioral coaching, not just investment selection." — Source: [WealthTrack Interview]

- On Mutual Fund Disclosures: "The standard mutual fund prospectus obscures the true total cost of ownership by splitting fees, trading costs, and tax impacts into separate, hard-to-reconcile categories." — Source: [Winning the Loser's Game]

- On Index Fund Pricing: "The beauty of the index fund is that it operates as a commodity; fierce competition has driven the price of market exposure down to essentially zero." — Source: [Morningstar The Long View]

- On the True Cost of Outperformance: "To beat the market by 1% after charging a 1% fee and incurring 1% in trading costs, a manager must actually generate 3% in excess returns, an almost impossible hurdle." — Source: [The Index Revolution]

Part 8: Investment Policy, Planning, and the Industry

- On Asset Allocation: "The asset allocation decision between stocks and bonds determines over 90 percent of long-term returns." — Source: [Elements of Investing]

- On Investment Policy Statements: "Every institution and individual needs a written investment policy statement to serve as an anchor of rationality during periods of market hysteria." — Source: [Winning the Loser's Game]

- On Individual Responsibility: "If investing is all about creativity and making unusual, unconventional, and even unpopular decisions, great investment decisions are best made by individuals taking direct responsibility for the results of their own acts." — Source: [Goodreads Quotes]

- On Defining Risk: "We now know to focus not on the rate of return, but on the informed management of risk, which is the true job of the fiduciary." — Source: [IFA Transcript]

- On Core Principles: "The core principles of successful investing never change and never will." — Source: [Winning the Loser's Game]

- On Buying Companies: "Don't pay more per share for a company's stock than you'd be willing to pay if you were buying the whole company." — Source: [Capital: The Story of Long-Term Investment Excellence]

- On Committees: "Investment committees often fail because they focus on short-term manager selection rather than maintaining discipline over long-term strategic asset allocation." — Source: [CFA Institute Journal]

- On Savings Rates: "The most neglected aspect of wealth building is simply saving a sufficient percentage of your income; no investment strategy can rescue an inadequate savings rate." — Source: [Elements of Investing]

- On Defining the Goal: "The purpose of investing is not to beat the benchmark; it is to fund your liabilities and achieve your personal financial goals." — Source: [Rational Reminder Episode 244]

- On the Ultimate Lesson: "The greatest irony of investing is that by simply accepting average market returns through low-cost indexing, you will inevitably end up in the top decile of all investors over a lifetime." — Source: [The Index Revolution]